Pilgrim's Pride Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Pilgrim’s Pride faces intense buyer power, concentrated retail channels, and margin pressure from commodity-fed cost swings, while supplier dynamics and regulatory burdens shape capacity and pricing flexibility. Competitive rivalry among protein producers drives innovation and scale advantages. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Feed commodity volatility

Maize and soymeal suppliers drive cost volatility for Pilgrim's through weather- and trade-linked price swings; US corn averaged about 4.50 USD/bu and soybean meal near 400 USD/short ton in 2024, pressuring margins. Pilgrim's hedging and scale give negotiating leverage but cannot fully offset sharp spikes, which compress gross margins quickly. Diversified sourcing reduces single-supplier risk.

Contract grower dynamics

Pilgrim's Pride depends on thousands of contract growers for live production, so individual growers have limited bargaining power but collective retention is critical to maintaining capacity. Tournament-style pay systems, under scrutiny in 2024 for fairness and stability, balance performance incentives with retention risks. Switching growers is slow and costly due to biosecurity protocols and geographic concentration of flocks.

Specialty inputs and genetics

Breeding stock, vaccines and animal-health inputs for Pilgrim's Pride come from a concentrated set of specialized firms—three primary breeding companies supply roughly 80% of global commercial broiler genetics—raising switching costs and giving suppliers leverage. Long-term contracts and integrated partnerships with these providers mitigate supply and biosecurity risk. Any disruption in seed stock or vaccine supply can quickly ripple through flock performance and production volumes.

Packaging and logistics

Packaging and logistics suppliers — resin, corrugate and cold-chain providers — tightened in 2024, pushing input-cost volatility and lifting packaging costs during peak weeks; diesel averaged about $3.80/gal in 2024, adding freight pressure. Pilgrim's scale secures multi-year contracts, but peak-season shortages and service failures still strain availability, lower fill rates and trigger penalties.

- Resin/corrugate tightness — 2024 peaks raised spot costs

- Diesel ~3.80/gal — adds freight volatility

- Scale secures contracts, but peak demand strains supply

- Service failures → fill-rate drops, contract penalties

Energy and utilities

Processing is energy- and water-intensive, exposing Pilgrim's to utility pricing volatility; US Henry Hub averaged about 3.5 USD/MMBtu in 2024 and industrial electricity averaged ~7.5 ¢/kWh, impacting plant margins regionally. Regional grids and local gas markets create uneven cost exposure across US and Mexican plants. Energy hedges and ongoing efficiency projects reduced short-term spikes, but sustained high energy prices erode operating leverage and compress gross margins.

- 2024 Henry Hub ~3.5 USD/MMBtu

- US industrial electricity ~7.5 ¢/kWh (2024)

- Hedges + efficiency = partial mitigation; sustained rises hurt margins

Feed volatility, concentrated genetics and logistics raise supplier power over growers

Maize ($4.50/bu 2024) and soybean meal (~$400/short ton 2024) drive cost volatility that hedges and scale only partly offset. Thousands of contract growers limit individual leverage but retention is critical; switching is slow. Concentrated genetics/providers (~3 firms ≈80% supply) and tight packaging/logistics (diesel $3.80/gal 2024) raise supplier power.

| Input | 2024 |

|---|---|

| Corn | $4.50/bu |

| Soybean meal | $400/short ton |

| Diesel | $3.80/gal |

| Henry Hub | $3.5/MMBtu |

What is included in the product

Tailored Porter's Five Forces analysis for Pilgrim's Pride uncovering competitive drivers, supplier/buyer power, entry barriers, substitutes, and strategic risks to profitability.

One-sheet Porter's Five Forces for Pilgrim's Pride—instantly visualize supplier, buyer, competitive, entrant and substitute pressures with a clean radar chart and customizable inputs so analysts and executives can quickly adapt scenarios for board decks or strategy sessions.

Customers Bargaining Power

Concentrated retail

Large grocers and club stores command volume and shelf space, with the top 10 U.S. retailers capturing roughly 65% of grocery sales in 2024, enabling aggressive price, promotion, and chargeback negotiations with suppliers like Pilgrim's Pride. Private label penetration—often 15–25% of category sales—increases retailer leverage, and losing a top account can create multi-million-pound volume gaps and margin pressure.

Foodservice chains

QSRs and casual-dining customers demand tight, consistent specs and pricing, forcing Pilgrim's Pride into low-margin, high-volume fulfillment; Pilgrim's Pride reported $14.6 billion net sales in 2023, underscoring foodservice importance. Multi-year contracts stabilize volumes but lock in slim margins and limit price flexibility. Frequent menu rotations and stringent service-level audits increase switching ease and make audit performance decisive for supplier retention.

Price sensitivity

Chicken is a staple protein with high price elasticity; USDA reports US per-capita chicken consumption of 101.6 pounds in 2023 and academic estimates place own-price elasticity between -0.6 and -1.2, so buyers shift quickly across cuts, brands and pack sizes. Retail promotions materially drive mix and velocity. Value-added premiums face greater resistance during downturns.

Switching costs

Switching costs are low for commodity cuts due to standardized specs and spot-market pricing, but rise for marinated, cooked, or custom items where formulations, HACCP audits and label certifications create supplier-specific costs; Pilgrim's Pride reported value-added products ∼30% of sales in 2024, raising buyer friction.

- Low switching: standardized cuts, spot pricing

- Higher: formulations, certifications, plant qual

- Cross-plant quals add friction, not full barriers

- Buyers multisource to retain leverage

International customers

International customers exert strong bargaining power as export buyers arbitrage global pricing and FX; Pilgrim's Pride reported 2024 net sales of $15.6 billion, making export pricing and currency swings material to margins. Rapid shifts in trade policy and sanitary rules have redirected demand and tightened spot markets. Distributors in Mexico and Europe press on volume and currency terms, and sudden market-access changes can re-route flows overnight.

Retail concentration (~65% top-10) and private-label growth amplify buyer leverage

Retail concentration (top 10 ≈65% grocery sales in 2024) and private-label growth give buyers strong price/shelf leverage; commodity cuts face low switching, while value-added (≈30% of Pilgrim's Pride sales in 2024) raises buyer friction. Exports and FX intensify bargaining; Pilgrim's Pride 2024 net sales $15.6B. QSRs lock slim-margin, high-volume contracts, limiting price flexibility.

| Metric | Value |

|---|---|

| Top-10 retailer share (US) | ≈65% (2024) |

| Pilgrim's Pride net sales | $15.6B (2024) |

| Value-added share | ≈30% (2024) |

| US per-capita chicken | 101.6 lb (2023) |

Same Document Delivered

Pilgrim's Pride Porter's Five Forces Analysis

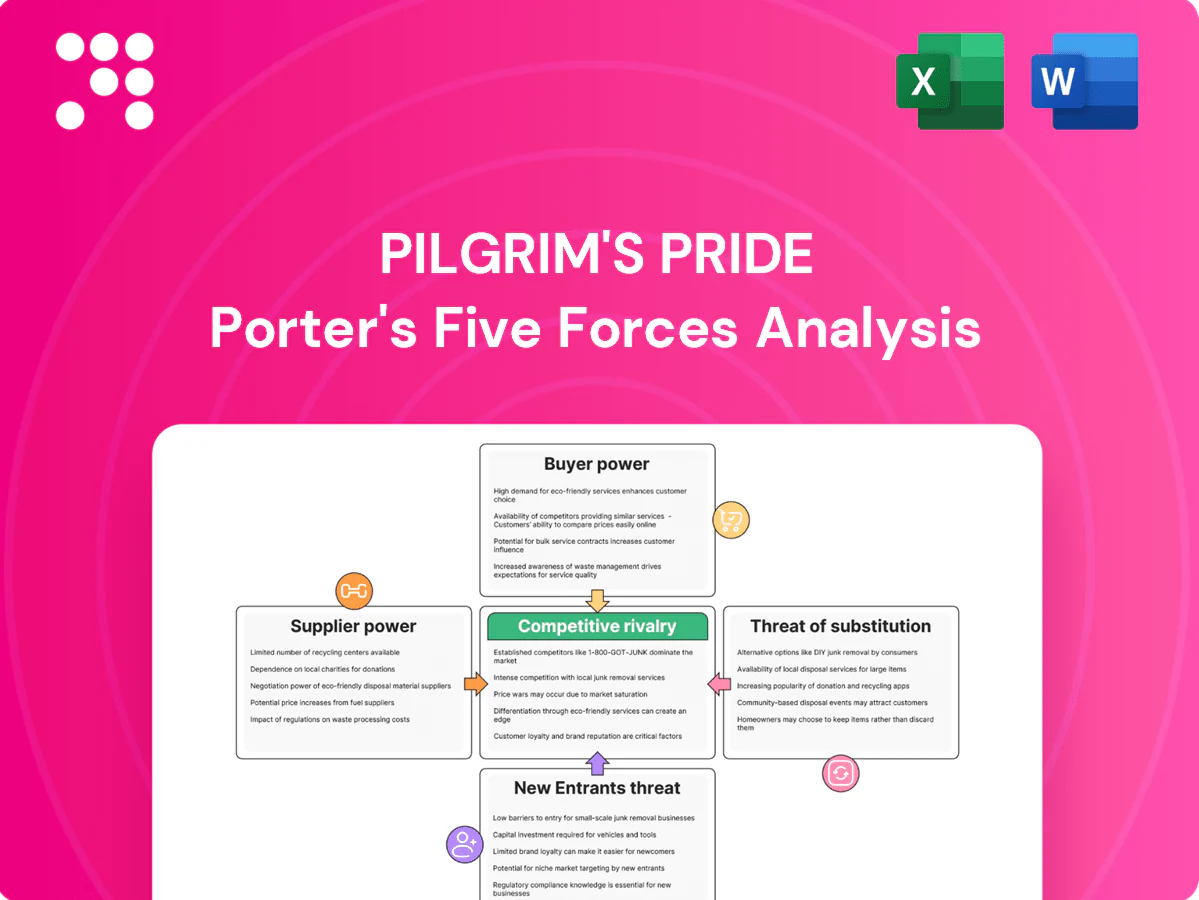

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Pilgrim's Pride Porter's Five Forces Analysis assesses intense industry rivalry from large competitors and price pressure, moderate supplier power, strong buyer power from retailers and foodservice, and low-to-moderate threats from substitutes and new entrants. It highlights strategic risks and opportunities for pricing, vertical integration, and supplier management, and is ready for immediate download and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Pilgrim’s Pride faces intense buyer power, concentrated retail channels, and margin pressure from commodity-fed cost swings, while supplier dynamics and regulatory burdens shape capacity and pricing flexibility. Competitive rivalry among protein producers drives innovation and scale advantages. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Feed commodity volatility

Maize and soymeal suppliers drive cost volatility for Pilgrim's through weather- and trade-linked price swings; US corn averaged about 4.50 USD/bu and soybean meal near 400 USD/short ton in 2024, pressuring margins. Pilgrim's hedging and scale give negotiating leverage but cannot fully offset sharp spikes, which compress gross margins quickly. Diversified sourcing reduces single-supplier risk.

Contract grower dynamics

Pilgrim's Pride depends on thousands of contract growers for live production, so individual growers have limited bargaining power but collective retention is critical to maintaining capacity. Tournament-style pay systems, under scrutiny in 2024 for fairness and stability, balance performance incentives with retention risks. Switching growers is slow and costly due to biosecurity protocols and geographic concentration of flocks.

Specialty inputs and genetics

Breeding stock, vaccines and animal-health inputs for Pilgrim's Pride come from a concentrated set of specialized firms—three primary breeding companies supply roughly 80% of global commercial broiler genetics—raising switching costs and giving suppliers leverage. Long-term contracts and integrated partnerships with these providers mitigate supply and biosecurity risk. Any disruption in seed stock or vaccine supply can quickly ripple through flock performance and production volumes.

Packaging and logistics

Packaging and logistics suppliers — resin, corrugate and cold-chain providers — tightened in 2024, pushing input-cost volatility and lifting packaging costs during peak weeks; diesel averaged about $3.80/gal in 2024, adding freight pressure. Pilgrim's scale secures multi-year contracts, but peak-season shortages and service failures still strain availability, lower fill rates and trigger penalties.

- Resin/corrugate tightness — 2024 peaks raised spot costs

- Diesel ~3.80/gal — adds freight volatility

- Scale secures contracts, but peak demand strains supply

- Service failures → fill-rate drops, contract penalties

Energy and utilities

Processing is energy- and water-intensive, exposing Pilgrim's to utility pricing volatility; US Henry Hub averaged about 3.5 USD/MMBtu in 2024 and industrial electricity averaged ~7.5 ¢/kWh, impacting plant margins regionally. Regional grids and local gas markets create uneven cost exposure across US and Mexican plants. Energy hedges and ongoing efficiency projects reduced short-term spikes, but sustained high energy prices erode operating leverage and compress gross margins.

- 2024 Henry Hub ~3.5 USD/MMBtu

- US industrial electricity ~7.5 ¢/kWh (2024)

- Hedges + efficiency = partial mitigation; sustained rises hurt margins

Feed volatility, concentrated genetics and logistics raise supplier power over growers

Maize ($4.50/bu 2024) and soybean meal (~$400/short ton 2024) drive cost volatility that hedges and scale only partly offset. Thousands of contract growers limit individual leverage but retention is critical; switching is slow. Concentrated genetics/providers (~3 firms ≈80% supply) and tight packaging/logistics (diesel $3.80/gal 2024) raise supplier power.

| Input | 2024 |

|---|---|

| Corn | $4.50/bu |

| Soybean meal | $400/short ton |

| Diesel | $3.80/gal |

| Henry Hub | $3.5/MMBtu |

What is included in the product

Tailored Porter's Five Forces analysis for Pilgrim's Pride uncovering competitive drivers, supplier/buyer power, entry barriers, substitutes, and strategic risks to profitability.

One-sheet Porter's Five Forces for Pilgrim's Pride—instantly visualize supplier, buyer, competitive, entrant and substitute pressures with a clean radar chart and customizable inputs so analysts and executives can quickly adapt scenarios for board decks or strategy sessions.

Customers Bargaining Power

Concentrated retail

Large grocers and club stores command volume and shelf space, with the top 10 U.S. retailers capturing roughly 65% of grocery sales in 2024, enabling aggressive price, promotion, and chargeback negotiations with suppliers like Pilgrim's Pride. Private label penetration—often 15–25% of category sales—increases retailer leverage, and losing a top account can create multi-million-pound volume gaps and margin pressure.

Foodservice chains

QSRs and casual-dining customers demand tight, consistent specs and pricing, forcing Pilgrim's Pride into low-margin, high-volume fulfillment; Pilgrim's Pride reported $14.6 billion net sales in 2023, underscoring foodservice importance. Multi-year contracts stabilize volumes but lock in slim margins and limit price flexibility. Frequent menu rotations and stringent service-level audits increase switching ease and make audit performance decisive for supplier retention.

Price sensitivity

Chicken is a staple protein with high price elasticity; USDA reports US per-capita chicken consumption of 101.6 pounds in 2023 and academic estimates place own-price elasticity between -0.6 and -1.2, so buyers shift quickly across cuts, brands and pack sizes. Retail promotions materially drive mix and velocity. Value-added premiums face greater resistance during downturns.

Switching costs

Switching costs are low for commodity cuts due to standardized specs and spot-market pricing, but rise for marinated, cooked, or custom items where formulations, HACCP audits and label certifications create supplier-specific costs; Pilgrim's Pride reported value-added products ∼30% of sales in 2024, raising buyer friction.

- Low switching: standardized cuts, spot pricing

- Higher: formulations, certifications, plant qual

- Cross-plant quals add friction, not full barriers

- Buyers multisource to retain leverage

International customers

International customers exert strong bargaining power as export buyers arbitrage global pricing and FX; Pilgrim's Pride reported 2024 net sales of $15.6 billion, making export pricing and currency swings material to margins. Rapid shifts in trade policy and sanitary rules have redirected demand and tightened spot markets. Distributors in Mexico and Europe press on volume and currency terms, and sudden market-access changes can re-route flows overnight.

Retail concentration (~65% top-10) and private-label growth amplify buyer leverage

Retail concentration (top 10 ≈65% grocery sales in 2024) and private-label growth give buyers strong price/shelf leverage; commodity cuts face low switching, while value-added (≈30% of Pilgrim's Pride sales in 2024) raises buyer friction. Exports and FX intensify bargaining; Pilgrim's Pride 2024 net sales $15.6B. QSRs lock slim-margin, high-volume contracts, limiting price flexibility.

| Metric | Value |

|---|---|

| Top-10 retailer share (US) | ≈65% (2024) |

| Pilgrim's Pride net sales | $15.6B (2024) |

| Value-added share | ≈30% (2024) |

| US per-capita chicken | 101.6 lb (2023) |

Same Document Delivered

Pilgrim's Pride Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Pilgrim's Pride Porter's Five Forces Analysis assesses intense industry rivalry from large competitors and price pressure, moderate supplier power, strong buyer power from retailers and foodservice, and low-to-moderate threats from substitutes and new entrants. It highlights strategic risks and opportunities for pricing, vertical integration, and supplier management, and is ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Pilgrim’s Pride faces intense buyer power, concentrated retail channels, and margin pressure from commodity-fed cost swings, while supplier dynamics and regulatory burdens shape capacity and pricing flexibility. Competitive rivalry among protein producers drives innovation and scale advantages. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Feed commodity volatility

Maize and soymeal suppliers drive cost volatility for Pilgrim's through weather- and trade-linked price swings; US corn averaged about 4.50 USD/bu and soybean meal near 400 USD/short ton in 2024, pressuring margins. Pilgrim's hedging and scale give negotiating leverage but cannot fully offset sharp spikes, which compress gross margins quickly. Diversified sourcing reduces single-supplier risk.

Contract grower dynamics

Pilgrim's Pride depends on thousands of contract growers for live production, so individual growers have limited bargaining power but collective retention is critical to maintaining capacity. Tournament-style pay systems, under scrutiny in 2024 for fairness and stability, balance performance incentives with retention risks. Switching growers is slow and costly due to biosecurity protocols and geographic concentration of flocks.

Specialty inputs and genetics

Breeding stock, vaccines and animal-health inputs for Pilgrim's Pride come from a concentrated set of specialized firms—three primary breeding companies supply roughly 80% of global commercial broiler genetics—raising switching costs and giving suppliers leverage. Long-term contracts and integrated partnerships with these providers mitigate supply and biosecurity risk. Any disruption in seed stock or vaccine supply can quickly ripple through flock performance and production volumes.

Packaging and logistics

Packaging and logistics suppliers — resin, corrugate and cold-chain providers — tightened in 2024, pushing input-cost volatility and lifting packaging costs during peak weeks; diesel averaged about $3.80/gal in 2024, adding freight pressure. Pilgrim's scale secures multi-year contracts, but peak-season shortages and service failures still strain availability, lower fill rates and trigger penalties.

- Resin/corrugate tightness — 2024 peaks raised spot costs

- Diesel ~3.80/gal — adds freight volatility

- Scale secures contracts, but peak demand strains supply

- Service failures → fill-rate drops, contract penalties

Energy and utilities

Processing is energy- and water-intensive, exposing Pilgrim's to utility pricing volatility; US Henry Hub averaged about 3.5 USD/MMBtu in 2024 and industrial electricity averaged ~7.5 ¢/kWh, impacting plant margins regionally. Regional grids and local gas markets create uneven cost exposure across US and Mexican plants. Energy hedges and ongoing efficiency projects reduced short-term spikes, but sustained high energy prices erode operating leverage and compress gross margins.

- 2024 Henry Hub ~3.5 USD/MMBtu

- US industrial electricity ~7.5 ¢/kWh (2024)

- Hedges + efficiency = partial mitigation; sustained rises hurt margins

Feed volatility, concentrated genetics and logistics raise supplier power over growers

Maize ($4.50/bu 2024) and soybean meal (~$400/short ton 2024) drive cost volatility that hedges and scale only partly offset. Thousands of contract growers limit individual leverage but retention is critical; switching is slow. Concentrated genetics/providers (~3 firms ≈80% supply) and tight packaging/logistics (diesel $3.80/gal 2024) raise supplier power.

| Input | 2024 |

|---|---|

| Corn | $4.50/bu |

| Soybean meal | $400/short ton |

| Diesel | $3.80/gal |

| Henry Hub | $3.5/MMBtu |

What is included in the product

Tailored Porter's Five Forces analysis for Pilgrim's Pride uncovering competitive drivers, supplier/buyer power, entry barriers, substitutes, and strategic risks to profitability.

One-sheet Porter's Five Forces for Pilgrim's Pride—instantly visualize supplier, buyer, competitive, entrant and substitute pressures with a clean radar chart and customizable inputs so analysts and executives can quickly adapt scenarios for board decks or strategy sessions.

Customers Bargaining Power

Concentrated retail

Large grocers and club stores command volume and shelf space, with the top 10 U.S. retailers capturing roughly 65% of grocery sales in 2024, enabling aggressive price, promotion, and chargeback negotiations with suppliers like Pilgrim's Pride. Private label penetration—often 15–25% of category sales—increases retailer leverage, and losing a top account can create multi-million-pound volume gaps and margin pressure.

Foodservice chains

QSRs and casual-dining customers demand tight, consistent specs and pricing, forcing Pilgrim's Pride into low-margin, high-volume fulfillment; Pilgrim's Pride reported $14.6 billion net sales in 2023, underscoring foodservice importance. Multi-year contracts stabilize volumes but lock in slim margins and limit price flexibility. Frequent menu rotations and stringent service-level audits increase switching ease and make audit performance decisive for supplier retention.

Price sensitivity

Chicken is a staple protein with high price elasticity; USDA reports US per-capita chicken consumption of 101.6 pounds in 2023 and academic estimates place own-price elasticity between -0.6 and -1.2, so buyers shift quickly across cuts, brands and pack sizes. Retail promotions materially drive mix and velocity. Value-added premiums face greater resistance during downturns.

Switching costs

Switching costs are low for commodity cuts due to standardized specs and spot-market pricing, but rise for marinated, cooked, or custom items where formulations, HACCP audits and label certifications create supplier-specific costs; Pilgrim's Pride reported value-added products ∼30% of sales in 2024, raising buyer friction.

- Low switching: standardized cuts, spot pricing

- Higher: formulations, certifications, plant qual

- Cross-plant quals add friction, not full barriers

- Buyers multisource to retain leverage

International customers

International customers exert strong bargaining power as export buyers arbitrage global pricing and FX; Pilgrim's Pride reported 2024 net sales of $15.6 billion, making export pricing and currency swings material to margins. Rapid shifts in trade policy and sanitary rules have redirected demand and tightened spot markets. Distributors in Mexico and Europe press on volume and currency terms, and sudden market-access changes can re-route flows overnight.

Retail concentration (~65% top-10) and private-label growth amplify buyer leverage

Retail concentration (top 10 ≈65% grocery sales in 2024) and private-label growth give buyers strong price/shelf leverage; commodity cuts face low switching, while value-added (≈30% of Pilgrim's Pride sales in 2024) raises buyer friction. Exports and FX intensify bargaining; Pilgrim's Pride 2024 net sales $15.6B. QSRs lock slim-margin, high-volume contracts, limiting price flexibility.

| Metric | Value |

|---|---|

| Top-10 retailer share (US) | ≈65% (2024) |

| Pilgrim's Pride net sales | $15.6B (2024) |

| Value-added share | ≈30% (2024) |

| US per-capita chicken | 101.6 lb (2023) |

Same Document Delivered

Pilgrim's Pride Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Pilgrim's Pride Porter's Five Forces Analysis assesses intense industry rivalry from large competitors and price pressure, moderate supplier power, strong buyer power from retailers and foodservice, and low-to-moderate threats from substitutes and new entrants. It highlights strategic risks and opportunities for pricing, vertical integration, and supplier management, and is ready for immediate download and use.