Piston Group SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

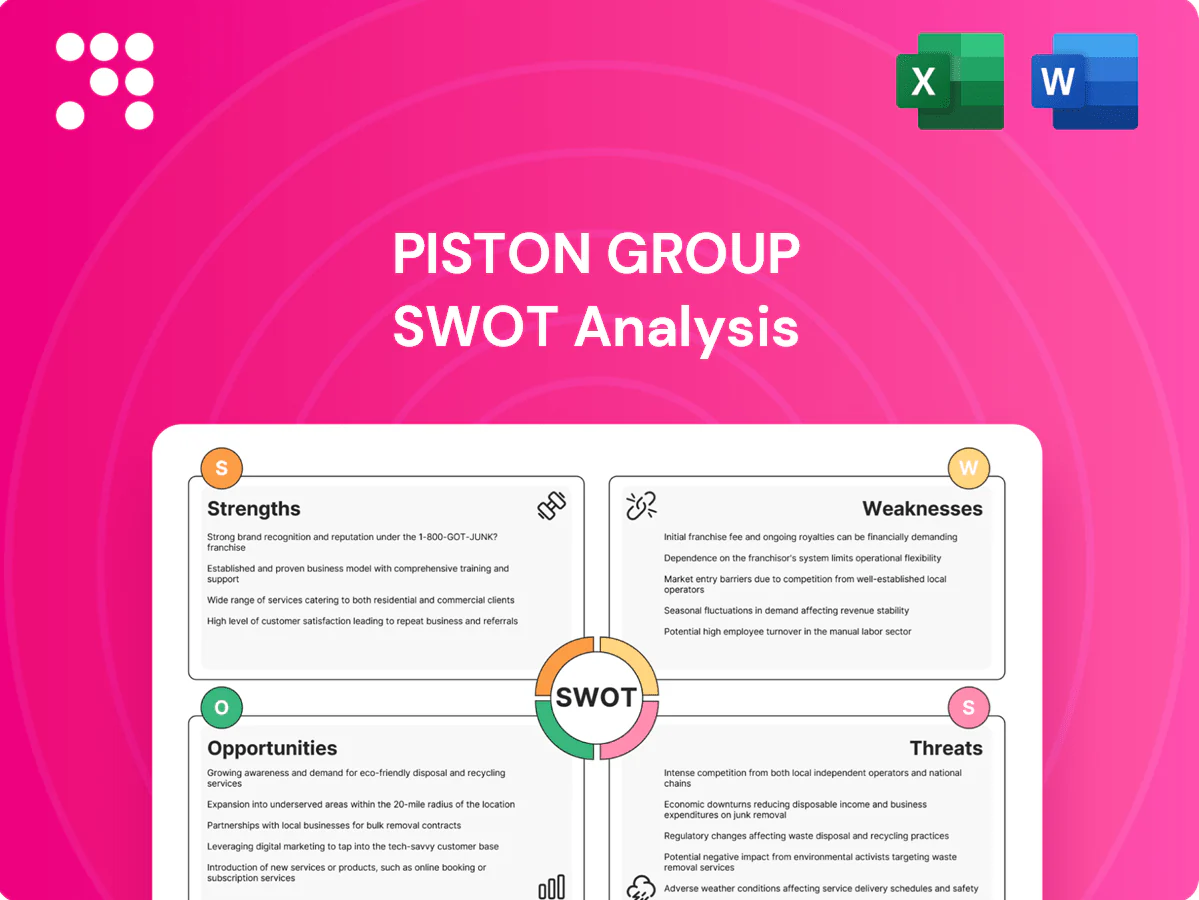

Piston Group’s SWOT snapshot reveals key strengths, vulnerabilities, market opportunities, and competitive threats to inform smarter decisions. Ready for deeper, research-backed insights? Purchase the full SWOT report—editable Word and Excel deliverables included to support strategy, pitching, and investment planning.

Strengths

Integrated design-to-assembly model

Piston Group’s integrated design-to-assembly model minimizes handoffs and accelerates launch timing, enabling faster NPI—concurrent engineering with OEMs can cut development cycles by up to 30% and Piston reports faster module launches versus industry peers. Vertical integration strengthens cost control and quality traceability, positioning the group as a preferred partner for complex modules and rapid problem resolution.

Diverse product and systems portfolio

Diverse product and systems portfolio across powertrain, interior and chassis smooths demand swings and reduced cyclicality; top 100 suppliers still capture roughly 70% of OEM content in 2024, benefiting scaled suppliers. Cross-domain expertise enables systems-level optimization and value engineering, raising margins. Breadth increases share-of-wallet with key OEMs and creates cross-selling in platform programs.

Strong OEM relationships and program wins

Piston Group's deep ties with major automakers underpin stable, multi-year revenue streams by securing program commitments early in vehicle development. Early involvement in vehicle programs locks in design-in positions and reduces aftermarket competition. Proven on-time, quality launch performance strengthens renewal odds, while strong referenceability with top OEMs accelerates wins on new platforms.

Quality, reliability, and operational excellence

Robust APQP/PPAP and lean practices drive defect rates toward Six Sigma benchmarks (3.4 DPMO), cutting scrap and rework. Consistent delivery performance (>98% on-time) preserves OEM production uptime and reduces penalty exposure. Data-driven continuous improvement has driven conversion-cost reductions of roughly 10–20% in comparable supplier programs, and a strong quality reputation wins competitive sourcing awards.

- APQP/PPAP: 3.4 DPMO

- On-time delivery: >98%

- CI savings: 10–20%

- Quality = sourcing win

Flexible manufacturing footprint

Modular lines and adaptable tooling let Piston Group shift mix and volume rapidly, supporting just-in-time delivery and minimizing changeover time.

Facilities located near OEM plants reduce inbound logistics risk and costs while enabling rapid response to platform changes and launch cadence.

Footprint flexibility allows efficient localization for new platforms, shortening lead times and supporting OEM capacity swings.

- Modular lines

- Near OEMs

- JIT-ready

- Efficient localization

Vertical-integrated model trims NPI 30%, keeps on-time > 98%

Piston Group’s integrated, vertically aligned model shortens NPI by up to 30%, sustains >98% on-time delivery and 3.4 DPMO, delivers 10–20% CI conversion-cost savings, and secures durable OEM program share amid 2024 industry concentration (top 100 suppliers ≈70% OEM content).

| Metric | Value |

|---|---|

| NPI cycle reduction | up to 30% |

| On-time delivery | >98% |

| Quality (DPMO) | 3.4 |

| CI savings | 10–20% |

| 2024 OEM concentration | Top 100 ≈70% |

What is included in the product

Provides a clear SWOT framework analyzing Piston Group’s internal capabilities, market strengths, growth opportunities, operational weaknesses, and external threats shaping its competitive position.

Provides a concise, editable SWOT matrix for Piston Group that streamlines stakeholder alignment and enables rapid strategic decisions; ideal for quick updates and easy integration into reports and presentations.

Weaknesses

High customer concentration

Dependence on a few OEMs heightens revenue volatility: for many tier-1 suppliers the top three customers account for over 60% of sales, leaving Piston Group exposed to demand swings. Loss or delay of a single platform can materially cut utilization and margins, with single-program shortfalls often reducing capacity use by 20–40%. Pricing leverage skews toward large buyers, and diversification across customers and regions remains a priority.

Capital-intensive operations

Equipment, tooling and launch investments exert steady pressure on free cash flow, with initial capex often concentrated in the first 12–36 months. Payback depends on sustained production volumes and stable programs, raising risk if orders slip. Higher interest rates (federal funds ~5.25–5.50% mid-2025) raise financing costs for capex. Large, heavy assets reduce agility and increase fixed-cost burdens during downturns.

Exposure to auto cycle

Piston Group's production volumes closely track macro auto demand and OEM schedules, with industry production swings of roughly 20-30% across cycles driving large revenue variability. Sudden downturns make inventory and labour balancing difficult, causing overtime or layoffs and higher per-unit costs. High fixed costs magnify margin swings; forecast errors force costly expediting or risk of parts obsolescence.

Limited end-consumer brand visibility

- Tier supplier visibility low — limited consumer pull

- Pricing pressure vs branded parts

- Must compete on performance, cost, delivery

- Marketing channels constrained vs OEMs

ICE-heavy legacy mix

ICE-heavy legacy mix leaves Piston Group exposed as EVs reached about 14% of global new car sales in 2024 and global electric car stock was ~26 million at end-2023 (IEA), implying secular decline in ICE content; shifting engineering into EV systems and software requires capital and skills investment, while some legacy lines risk underutilization and margin erosion if the portfolio shift is mistimed.

- Industry EV share: 14% (2024)

- Global EV stock: ~26M (end-2023)

- Requires capex and retooling

- Timing critical to protect margins

Concentration with top OEMs >60% and capex strain amid 5.25–5.50% rates

Concentration with top OEMs (>60% sales) creates high revenue volatility and pricing pressure; single-program shortfalls can cut utilization 20–40%. Heavy capex/tooling (payback 12–36 months) and federal funds ~5.25–5.50% (mid-2025) squeeze free cash flow. ICE-heavy mix risks margin erosion as EV share reached 14% in 2024 and global EV stock ~26M (end-2023).

| Metric | Value | Impact |

|---|---|---|

| Top-3 OEM share | >60% | Revenue concentration |

| Program shortfall | 20–40% utiliz. | Margin hit |

| Capex payback | 12–36 mo | Cash pressure |

| Fed funds | 5.25–5.50% (mid-2025) | Higher financing cost |

| EV share | 14% (2024) | ICE obsolescence risk |

| Global EV stock | ~26M (end-2023) | Secular shift |

What You See Is What You Get

Piston Group SWOT Analysis

This is the actual Piston Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects its structure, findings, and recommendations. Buy now to unlock the complete, editable version ready for immediate use.

Dive Deeper Into the Company’s Strategic Blueprint

Piston Group’s SWOT snapshot reveals key strengths, vulnerabilities, market opportunities, and competitive threats to inform smarter decisions. Ready for deeper, research-backed insights? Purchase the full SWOT report—editable Word and Excel deliverables included to support strategy, pitching, and investment planning.

Strengths

Integrated design-to-assembly model

Piston Group’s integrated design-to-assembly model minimizes handoffs and accelerates launch timing, enabling faster NPI—concurrent engineering with OEMs can cut development cycles by up to 30% and Piston reports faster module launches versus industry peers. Vertical integration strengthens cost control and quality traceability, positioning the group as a preferred partner for complex modules and rapid problem resolution.

Diverse product and systems portfolio

Diverse product and systems portfolio across powertrain, interior and chassis smooths demand swings and reduced cyclicality; top 100 suppliers still capture roughly 70% of OEM content in 2024, benefiting scaled suppliers. Cross-domain expertise enables systems-level optimization and value engineering, raising margins. Breadth increases share-of-wallet with key OEMs and creates cross-selling in platform programs.

Strong OEM relationships and program wins

Piston Group's deep ties with major automakers underpin stable, multi-year revenue streams by securing program commitments early in vehicle development. Early involvement in vehicle programs locks in design-in positions and reduces aftermarket competition. Proven on-time, quality launch performance strengthens renewal odds, while strong referenceability with top OEMs accelerates wins on new platforms.

Quality, reliability, and operational excellence

Robust APQP/PPAP and lean practices drive defect rates toward Six Sigma benchmarks (3.4 DPMO), cutting scrap and rework. Consistent delivery performance (>98% on-time) preserves OEM production uptime and reduces penalty exposure. Data-driven continuous improvement has driven conversion-cost reductions of roughly 10–20% in comparable supplier programs, and a strong quality reputation wins competitive sourcing awards.

- APQP/PPAP: 3.4 DPMO

- On-time delivery: >98%

- CI savings: 10–20%

- Quality = sourcing win

Flexible manufacturing footprint

Modular lines and adaptable tooling let Piston Group shift mix and volume rapidly, supporting just-in-time delivery and minimizing changeover time.

Facilities located near OEM plants reduce inbound logistics risk and costs while enabling rapid response to platform changes and launch cadence.

Footprint flexibility allows efficient localization for new platforms, shortening lead times and supporting OEM capacity swings.

- Modular lines

- Near OEMs

- JIT-ready

- Efficient localization

Vertical-integrated model trims NPI 30%, keeps on-time > 98%

Piston Group’s integrated, vertically aligned model shortens NPI by up to 30%, sustains >98% on-time delivery and 3.4 DPMO, delivers 10–20% CI conversion-cost savings, and secures durable OEM program share amid 2024 industry concentration (top 100 suppliers ≈70% OEM content).

| Metric | Value |

|---|---|

| NPI cycle reduction | up to 30% |

| On-time delivery | >98% |

| Quality (DPMO) | 3.4 |

| CI savings | 10–20% |

| 2024 OEM concentration | Top 100 ≈70% |

What is included in the product

Provides a clear SWOT framework analyzing Piston Group’s internal capabilities, market strengths, growth opportunities, operational weaknesses, and external threats shaping its competitive position.

Provides a concise, editable SWOT matrix for Piston Group that streamlines stakeholder alignment and enables rapid strategic decisions; ideal for quick updates and easy integration into reports and presentations.

Weaknesses

High customer concentration

Dependence on a few OEMs heightens revenue volatility: for many tier-1 suppliers the top three customers account for over 60% of sales, leaving Piston Group exposed to demand swings. Loss or delay of a single platform can materially cut utilization and margins, with single-program shortfalls often reducing capacity use by 20–40%. Pricing leverage skews toward large buyers, and diversification across customers and regions remains a priority.

Capital-intensive operations

Equipment, tooling and launch investments exert steady pressure on free cash flow, with initial capex often concentrated in the first 12–36 months. Payback depends on sustained production volumes and stable programs, raising risk if orders slip. Higher interest rates (federal funds ~5.25–5.50% mid-2025) raise financing costs for capex. Large, heavy assets reduce agility and increase fixed-cost burdens during downturns.

Exposure to auto cycle

Piston Group's production volumes closely track macro auto demand and OEM schedules, with industry production swings of roughly 20-30% across cycles driving large revenue variability. Sudden downturns make inventory and labour balancing difficult, causing overtime or layoffs and higher per-unit costs. High fixed costs magnify margin swings; forecast errors force costly expediting or risk of parts obsolescence.

Limited end-consumer brand visibility

- Tier supplier visibility low — limited consumer pull

- Pricing pressure vs branded parts

- Must compete on performance, cost, delivery

- Marketing channels constrained vs OEMs

ICE-heavy legacy mix

ICE-heavy legacy mix leaves Piston Group exposed as EVs reached about 14% of global new car sales in 2024 and global electric car stock was ~26 million at end-2023 (IEA), implying secular decline in ICE content; shifting engineering into EV systems and software requires capital and skills investment, while some legacy lines risk underutilization and margin erosion if the portfolio shift is mistimed.

- Industry EV share: 14% (2024)

- Global EV stock: ~26M (end-2023)

- Requires capex and retooling

- Timing critical to protect margins

Concentration with top OEMs >60% and capex strain amid 5.25–5.50% rates

Concentration with top OEMs (>60% sales) creates high revenue volatility and pricing pressure; single-program shortfalls can cut utilization 20–40%. Heavy capex/tooling (payback 12–36 months) and federal funds ~5.25–5.50% (mid-2025) squeeze free cash flow. ICE-heavy mix risks margin erosion as EV share reached 14% in 2024 and global EV stock ~26M (end-2023).

| Metric | Value | Impact |

|---|---|---|

| Top-3 OEM share | >60% | Revenue concentration |

| Program shortfall | 20–40% utiliz. | Margin hit |

| Capex payback | 12–36 mo | Cash pressure |

| Fed funds | 5.25–5.50% (mid-2025) | Higher financing cost |

| EV share | 14% (2024) | ICE obsolescence risk |

| Global EV stock | ~26M (end-2023) | Secular shift |

What You See Is What You Get

Piston Group SWOT Analysis

This is the actual Piston Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects its structure, findings, and recommendations. Buy now to unlock the complete, editable version ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Piston Group’s SWOT snapshot reveals key strengths, vulnerabilities, market opportunities, and competitive threats to inform smarter decisions. Ready for deeper, research-backed insights? Purchase the full SWOT report—editable Word and Excel deliverables included to support strategy, pitching, and investment planning.

Strengths

Integrated design-to-assembly model

Piston Group’s integrated design-to-assembly model minimizes handoffs and accelerates launch timing, enabling faster NPI—concurrent engineering with OEMs can cut development cycles by up to 30% and Piston reports faster module launches versus industry peers. Vertical integration strengthens cost control and quality traceability, positioning the group as a preferred partner for complex modules and rapid problem resolution.

Diverse product and systems portfolio

Diverse product and systems portfolio across powertrain, interior and chassis smooths demand swings and reduced cyclicality; top 100 suppliers still capture roughly 70% of OEM content in 2024, benefiting scaled suppliers. Cross-domain expertise enables systems-level optimization and value engineering, raising margins. Breadth increases share-of-wallet with key OEMs and creates cross-selling in platform programs.

Strong OEM relationships and program wins

Piston Group's deep ties with major automakers underpin stable, multi-year revenue streams by securing program commitments early in vehicle development. Early involvement in vehicle programs locks in design-in positions and reduces aftermarket competition. Proven on-time, quality launch performance strengthens renewal odds, while strong referenceability with top OEMs accelerates wins on new platforms.

Quality, reliability, and operational excellence

Robust APQP/PPAP and lean practices drive defect rates toward Six Sigma benchmarks (3.4 DPMO), cutting scrap and rework. Consistent delivery performance (>98% on-time) preserves OEM production uptime and reduces penalty exposure. Data-driven continuous improvement has driven conversion-cost reductions of roughly 10–20% in comparable supplier programs, and a strong quality reputation wins competitive sourcing awards.

- APQP/PPAP: 3.4 DPMO

- On-time delivery: >98%

- CI savings: 10–20%

- Quality = sourcing win

Flexible manufacturing footprint

Modular lines and adaptable tooling let Piston Group shift mix and volume rapidly, supporting just-in-time delivery and minimizing changeover time.

Facilities located near OEM plants reduce inbound logistics risk and costs while enabling rapid response to platform changes and launch cadence.

Footprint flexibility allows efficient localization for new platforms, shortening lead times and supporting OEM capacity swings.

- Modular lines

- Near OEMs

- JIT-ready

- Efficient localization

Vertical-integrated model trims NPI 30%, keeps on-time > 98%

Piston Group’s integrated, vertically aligned model shortens NPI by up to 30%, sustains >98% on-time delivery and 3.4 DPMO, delivers 10–20% CI conversion-cost savings, and secures durable OEM program share amid 2024 industry concentration (top 100 suppliers ≈70% OEM content).

| Metric | Value |

|---|---|

| NPI cycle reduction | up to 30% |

| On-time delivery | >98% |

| Quality (DPMO) | 3.4 |

| CI savings | 10–20% |

| 2024 OEM concentration | Top 100 ≈70% |

What is included in the product

Provides a clear SWOT framework analyzing Piston Group’s internal capabilities, market strengths, growth opportunities, operational weaknesses, and external threats shaping its competitive position.

Provides a concise, editable SWOT matrix for Piston Group that streamlines stakeholder alignment and enables rapid strategic decisions; ideal for quick updates and easy integration into reports and presentations.

Weaknesses

High customer concentration

Dependence on a few OEMs heightens revenue volatility: for many tier-1 suppliers the top three customers account for over 60% of sales, leaving Piston Group exposed to demand swings. Loss or delay of a single platform can materially cut utilization and margins, with single-program shortfalls often reducing capacity use by 20–40%. Pricing leverage skews toward large buyers, and diversification across customers and regions remains a priority.

Capital-intensive operations

Equipment, tooling and launch investments exert steady pressure on free cash flow, with initial capex often concentrated in the first 12–36 months. Payback depends on sustained production volumes and stable programs, raising risk if orders slip. Higher interest rates (federal funds ~5.25–5.50% mid-2025) raise financing costs for capex. Large, heavy assets reduce agility and increase fixed-cost burdens during downturns.

Exposure to auto cycle

Piston Group's production volumes closely track macro auto demand and OEM schedules, with industry production swings of roughly 20-30% across cycles driving large revenue variability. Sudden downturns make inventory and labour balancing difficult, causing overtime or layoffs and higher per-unit costs. High fixed costs magnify margin swings; forecast errors force costly expediting or risk of parts obsolescence.

Limited end-consumer brand visibility

- Tier supplier visibility low — limited consumer pull

- Pricing pressure vs branded parts

- Must compete on performance, cost, delivery

- Marketing channels constrained vs OEMs

ICE-heavy legacy mix

ICE-heavy legacy mix leaves Piston Group exposed as EVs reached about 14% of global new car sales in 2024 and global electric car stock was ~26 million at end-2023 (IEA), implying secular decline in ICE content; shifting engineering into EV systems and software requires capital and skills investment, while some legacy lines risk underutilization and margin erosion if the portfolio shift is mistimed.

- Industry EV share: 14% (2024)

- Global EV stock: ~26M (end-2023)

- Requires capex and retooling

- Timing critical to protect margins

Concentration with top OEMs >60% and capex strain amid 5.25–5.50% rates

Concentration with top OEMs (>60% sales) creates high revenue volatility and pricing pressure; single-program shortfalls can cut utilization 20–40%. Heavy capex/tooling (payback 12–36 months) and federal funds ~5.25–5.50% (mid-2025) squeeze free cash flow. ICE-heavy mix risks margin erosion as EV share reached 14% in 2024 and global EV stock ~26M (end-2023).

| Metric | Value | Impact |

|---|---|---|

| Top-3 OEM share | >60% | Revenue concentration |

| Program shortfall | 20–40% utiliz. | Margin hit |

| Capex payback | 12–36 mo | Cash pressure |

| Fed funds | 5.25–5.50% (mid-2025) | Higher financing cost |

| EV share | 14% (2024) | ICE obsolescence risk |

| Global EV stock | ~26M (end-2023) | Secular shift |

What You See Is What You Get

Piston Group SWOT Analysis

This is the actual Piston Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects its structure, findings, and recommendations. Buy now to unlock the complete, editable version ready for immediate use.