PKO Bank Polski Porter's Five Forces Analysis

Don't Miss the Bigger Picture

PKO Bank Polski faces moderate competitive intensity with regulatory constraints and rising fintech substitution. This snapshot flags key pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for detailed metrics, strategic implications, and charts. Purchase the complete report to inform investment or strategy.

Suppliers Bargaining Power

Concentrated tech vendors

In 2024 PKO Bank Polski, Poland's largest bank by assets, relies on a handful of core banking, cloud and cybersecurity providers, creating switching costs and supplier leverage. Contract renewals can pressure pricing and service levels, but PKO’s scale supports multi-vendor strategies and tougher negotiations. Ongoing KNF and EBA operational resilience scrutiny further disciplines suppliers.

Wholesale funding providers

Wholesale funding—interbank lines, capital markets, and covered bonds—supplements deposits, but in stressed markets spreads can widen and covenants tighten, increasing supplier power. PKO Bank Polski, Poland’s largest bank by assets, mitigates this through a strong brand, deep collateral pools and a robust balance sheet. Diversified maturities and instruments reduce concentration risk and reliance on any single provider.

Payment schemes and processors

Card networks and payment rails set fees and technical standards—Visa processed about $14.9tn TPV in FY2023—giving them leverage, particularly on interchange and compliance mandates. EU interchange caps (0.2% debit, 0.3% credit) limit fees but do not eliminate scheme rule power. PKO mitigates through scale, co‑brand deals and routing to domestic switches. Rising instant payments (growing adoption in 2023–24) may rebalance dynamics.

Talent and specialist skills

- Talent pool: c.500,000 IT specialists (2024)

- PKO scale: c.25,000 employees

- Mitigants: training, automation, nearshoring

Data and credit bureaus

External data, ratings and credit bureau inputs (notably BIK and BIG InfoMonitor) materially shape PKO Bank Polski underwriting and compliance, creating supplier leverage where niche datasets have limited alternatives and can raise costs and lock-in. PKO can blend rich internal customer data with PSD2 open-banking feeds to reduce dependence, while EU and Polish regulatory open-data initiatives from 2018 onward may further weaken supplier clout.

- BIK, BIG InfoMonitor: primary bureau providers

- PSD2 (2018): enables open-banking data aggregation

- Internal data + open banking: lowers bureau reliance

Polish bank balances vendor leverage, funding stress and IT talent squeeze

PKO faces supplier leverage from core IT, cloud and cybersecurity vendors and card schemes, but its scale and multi-vendor approach strengthen negotiating power. Wholesale funding lines and capital markets raise supplier risk in stress, partially offset by deep collateral and diversified maturities. Talent scarcity (c.500,000 IT specialists in Poland) and bureau reliance raise costs, mitigated by PKO’s c.25,000 staff, training and automation.

| Item | 2024 figure | Impact |

|---|---|---|

| PKO employees | c.25,000 | negotiation scale |

| Poland IT pool | c.500,000 | talent pressure |

| Visa TPV | $14.9tn (FY2023) | scheme leverage |

| Interchange caps | 0.2% debit / 0.3% credit | fee limits |

What is included in the product

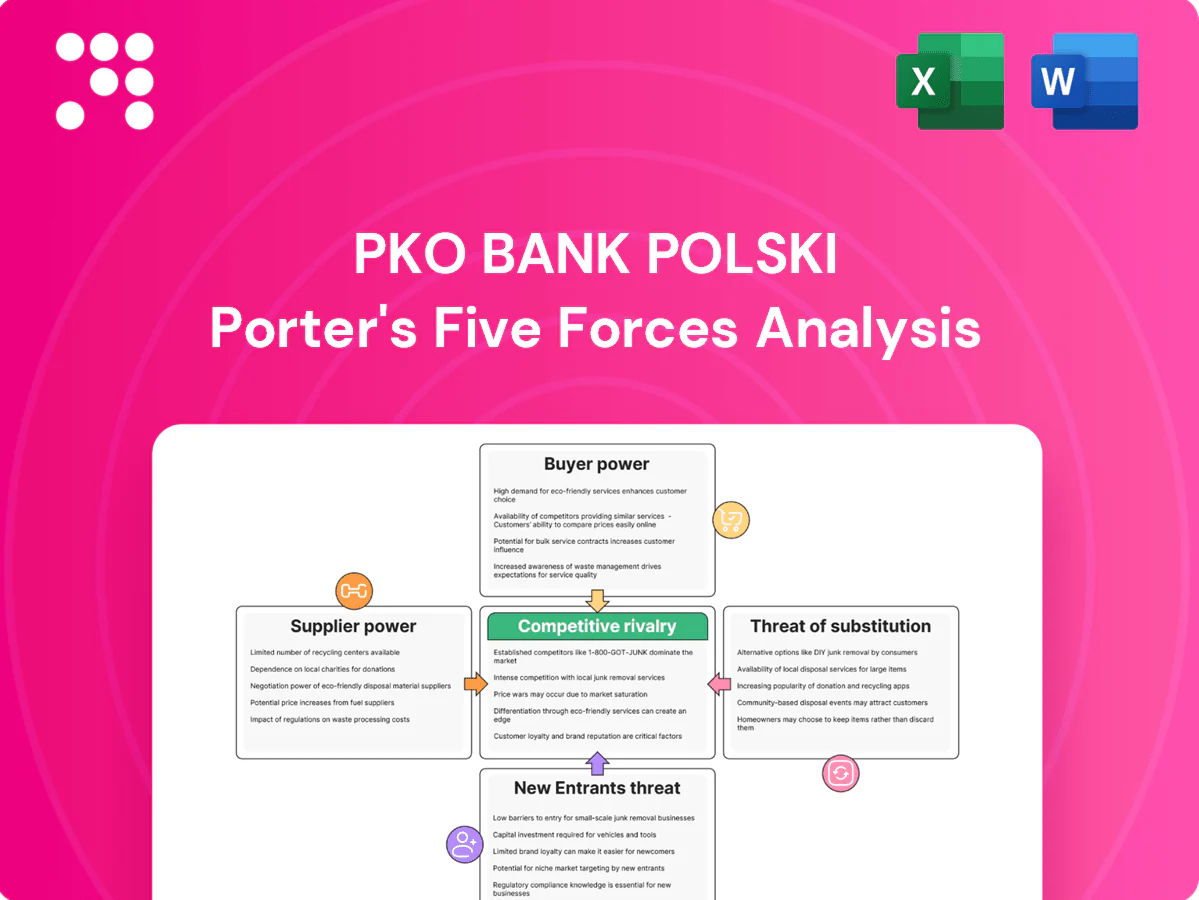

Uncovers key drivers of competition, customer influence, and market entry risks tailored to PKO Bank Polski; evaluates supplier and buyer power, substitutes, rivalry and barriers to entry, identifying disruptive threats and strategic protections for the bank’s market position.

One-sheet Porter's Five Forces for PKO Bank Polski—instantly visualizes competitive pressure with a spider chart and editable stress levels, so teams can customize threats, copy into decks, and make fast, board-ready strategic decisions.

Customers Bargaining Power

Price-sensitive retail customers

Retail customers increasingly compare rates and fees via digital channels, raising transparency and price sensitivity for PKO Bank Polski.

Improved account portability has lowered switching costs, though PKO remains Poland's largest bank by assets, serving over 9 million retail customers in 2024, which mitigates churn.

Its broad product suite and loyalty ecosystem (multi-product penetration above industry averages) reduce buyer power.

Strong brand trust and ~1,000 branches continue to temper customer leverage in key segments.

Large corporates and institutions

Large corporates negotiate bespoke pricing and SLAs, leveraging transaction volumes and multi-banking to exert strong bargaining power against PKO Bank Polski, Poland's largest bank by assets with about 20% market share in 2024.

They pressure margins on cash management, trade finance and lending packages, where PKO competes intensively.

Deep relationships and cross-sell of treasury, FX and lending products help PKO defend spreads and retain strategic corporate clients.

Digital adoption and UX expectations

Customers demand seamless mobile onboarding, instant payments and 24/7 service, with Polish mobile banking adoption exceeding 70% in 2024; poor UX leads to rapid switching to nimble fintechs. PKO’s IKO and iPKO platforms—IKO reporting over 8 million users in 2024—help meet expectations and retain volumes as digital transactions surpass 70% of retail activity. Continuous feature rollout and faster onboarding are needed to curb growing buyer leverage.

Access to alternatives

Fintech wallets, BNPL, brokers and neo-banks deliver lower-cost point solutions, expanding choice and raising customers' negotiation leverage; BNPL/neo-bank users in Poland rose ~30% YoY to ~6m users by 2024, intensifying price pressure on incumbents.

PKO mitigates this via integrated retail and corporate bundles, cross-sell (serving ~10m clients, ~18% market share in 2024) and trust-based full-service relationships for complex credit and corporate needs.

- Fintechs: lower cost, point solutions

- BNPL/neo-banks: ~6m Polish users (2024)

- PKO: ~10m clients, ~18% market share (2024)

- Advantage: trust, integrated full-service bundles

Information transparency

Aggregators and comparison sites reveal pricing and performance instantly, increasing switching by informed customers. Reviews and social media amplify service issues, forcing PKO Bank Polski — serving about 8.6 million clients and holding roughly 31% of Polish banking assets in 2023–24 — to maintain consistent quality to avoid discount pressure. Clear communication and financial education can shift buyer focus from price to value.

- Instant transparency drives price sensitivity

- Reputation risk amplified by social media

- PKO must prioritize service consistency (8.6m clients, ~31% market share)

- Education reduces churn

>70% mobile shifts power to price-sensitive Polish retail banking

Customers are more price-sensitive due to digital comparison and >70% mobile banking adoption in Poland (2024), raising retail bargaining power.

PKO’s scale—~10m clients and ~18% market share in 2024—and IKO’s ~8m users limit churn via cross-sell and trust.

Fintechs/BNPL (~6m users in 2024) and corporate multi-banking pressure fees on transaction and lending margins.

| Metric | 2024 |

|---|---|

| PKO clients | ~10m |

| Market share | ~18% |

| IKO users | ~8m |

| Mobile adoption (PL) | >70% |

| BNPL/neo-bank users | ~6m |

What You See Is What You Get

PKO Bank Polski Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of PKO Bank Polski you'll receive after purchase—no placeholders or samples. The document assesses competitive rivalry, buyer and supplier power, and the threats of entry and substitutes with clear strategic implications. It's the final, fully formatted file ready for immediate download and use.

Don't Miss the Bigger Picture

PKO Bank Polski faces moderate competitive intensity with regulatory constraints and rising fintech substitution. This snapshot flags key pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for detailed metrics, strategic implications, and charts. Purchase the complete report to inform investment or strategy.

Suppliers Bargaining Power

Concentrated tech vendors

In 2024 PKO Bank Polski, Poland's largest bank by assets, relies on a handful of core banking, cloud and cybersecurity providers, creating switching costs and supplier leverage. Contract renewals can pressure pricing and service levels, but PKO’s scale supports multi-vendor strategies and tougher negotiations. Ongoing KNF and EBA operational resilience scrutiny further disciplines suppliers.

Wholesale funding providers

Wholesale funding—interbank lines, capital markets, and covered bonds—supplements deposits, but in stressed markets spreads can widen and covenants tighten, increasing supplier power. PKO Bank Polski, Poland’s largest bank by assets, mitigates this through a strong brand, deep collateral pools and a robust balance sheet. Diversified maturities and instruments reduce concentration risk and reliance on any single provider.

Payment schemes and processors

Card networks and payment rails set fees and technical standards—Visa processed about $14.9tn TPV in FY2023—giving them leverage, particularly on interchange and compliance mandates. EU interchange caps (0.2% debit, 0.3% credit) limit fees but do not eliminate scheme rule power. PKO mitigates through scale, co‑brand deals and routing to domestic switches. Rising instant payments (growing adoption in 2023–24) may rebalance dynamics.

Talent and specialist skills

- Talent pool: c.500,000 IT specialists (2024)

- PKO scale: c.25,000 employees

- Mitigants: training, automation, nearshoring

Data and credit bureaus

External data, ratings and credit bureau inputs (notably BIK and BIG InfoMonitor) materially shape PKO Bank Polski underwriting and compliance, creating supplier leverage where niche datasets have limited alternatives and can raise costs and lock-in. PKO can blend rich internal customer data with PSD2 open-banking feeds to reduce dependence, while EU and Polish regulatory open-data initiatives from 2018 onward may further weaken supplier clout.

- BIK, BIG InfoMonitor: primary bureau providers

- PSD2 (2018): enables open-banking data aggregation

- Internal data + open banking: lowers bureau reliance

Polish bank balances vendor leverage, funding stress and IT talent squeeze

PKO faces supplier leverage from core IT, cloud and cybersecurity vendors and card schemes, but its scale and multi-vendor approach strengthen negotiating power. Wholesale funding lines and capital markets raise supplier risk in stress, partially offset by deep collateral and diversified maturities. Talent scarcity (c.500,000 IT specialists in Poland) and bureau reliance raise costs, mitigated by PKO’s c.25,000 staff, training and automation.

| Item | 2024 figure | Impact |

|---|---|---|

| PKO employees | c.25,000 | negotiation scale |

| Poland IT pool | c.500,000 | talent pressure |

| Visa TPV | $14.9tn (FY2023) | scheme leverage |

| Interchange caps | 0.2% debit / 0.3% credit | fee limits |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to PKO Bank Polski; evaluates supplier and buyer power, substitutes, rivalry and barriers to entry, identifying disruptive threats and strategic protections for the bank’s market position.

One-sheet Porter's Five Forces for PKO Bank Polski—instantly visualizes competitive pressure with a spider chart and editable stress levels, so teams can customize threats, copy into decks, and make fast, board-ready strategic decisions.

Customers Bargaining Power

Price-sensitive retail customers

Retail customers increasingly compare rates and fees via digital channels, raising transparency and price sensitivity for PKO Bank Polski.

Improved account portability has lowered switching costs, though PKO remains Poland's largest bank by assets, serving over 9 million retail customers in 2024, which mitigates churn.

Its broad product suite and loyalty ecosystem (multi-product penetration above industry averages) reduce buyer power.

Strong brand trust and ~1,000 branches continue to temper customer leverage in key segments.

Large corporates and institutions

Large corporates negotiate bespoke pricing and SLAs, leveraging transaction volumes and multi-banking to exert strong bargaining power against PKO Bank Polski, Poland's largest bank by assets with about 20% market share in 2024.

They pressure margins on cash management, trade finance and lending packages, where PKO competes intensively.

Deep relationships and cross-sell of treasury, FX and lending products help PKO defend spreads and retain strategic corporate clients.

Digital adoption and UX expectations

Customers demand seamless mobile onboarding, instant payments and 24/7 service, with Polish mobile banking adoption exceeding 70% in 2024; poor UX leads to rapid switching to nimble fintechs. PKO’s IKO and iPKO platforms—IKO reporting over 8 million users in 2024—help meet expectations and retain volumes as digital transactions surpass 70% of retail activity. Continuous feature rollout and faster onboarding are needed to curb growing buyer leverage.

Access to alternatives

Fintech wallets, BNPL, brokers and neo-banks deliver lower-cost point solutions, expanding choice and raising customers' negotiation leverage; BNPL/neo-bank users in Poland rose ~30% YoY to ~6m users by 2024, intensifying price pressure on incumbents.

PKO mitigates this via integrated retail and corporate bundles, cross-sell (serving ~10m clients, ~18% market share in 2024) and trust-based full-service relationships for complex credit and corporate needs.

- Fintechs: lower cost, point solutions

- BNPL/neo-banks: ~6m Polish users (2024)

- PKO: ~10m clients, ~18% market share (2024)

- Advantage: trust, integrated full-service bundles

Information transparency

Aggregators and comparison sites reveal pricing and performance instantly, increasing switching by informed customers. Reviews and social media amplify service issues, forcing PKO Bank Polski — serving about 8.6 million clients and holding roughly 31% of Polish banking assets in 2023–24 — to maintain consistent quality to avoid discount pressure. Clear communication and financial education can shift buyer focus from price to value.

- Instant transparency drives price sensitivity

- Reputation risk amplified by social media

- PKO must prioritize service consistency (8.6m clients, ~31% market share)

- Education reduces churn

>70% mobile shifts power to price-sensitive Polish retail banking

Customers are more price-sensitive due to digital comparison and >70% mobile banking adoption in Poland (2024), raising retail bargaining power.

PKO’s scale—~10m clients and ~18% market share in 2024—and IKO’s ~8m users limit churn via cross-sell and trust.

Fintechs/BNPL (~6m users in 2024) and corporate multi-banking pressure fees on transaction and lending margins.

| Metric | 2024 |

|---|---|

| PKO clients | ~10m |

| Market share | ~18% |

| IKO users | ~8m |

| Mobile adoption (PL) | >70% |

| BNPL/neo-bank users | ~6m |

What You See Is What You Get

PKO Bank Polski Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of PKO Bank Polski you'll receive after purchase—no placeholders or samples. The document assesses competitive rivalry, buyer and supplier power, and the threats of entry and substitutes with clear strategic implications. It's the final, fully formatted file ready for immediate download and use.

Description

Don't Miss the Bigger Picture

PKO Bank Polski faces moderate competitive intensity with regulatory constraints and rising fintech substitution. This snapshot flags key pressures but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for detailed metrics, strategic implications, and charts. Purchase the complete report to inform investment or strategy.

Suppliers Bargaining Power

Concentrated tech vendors

In 2024 PKO Bank Polski, Poland's largest bank by assets, relies on a handful of core banking, cloud and cybersecurity providers, creating switching costs and supplier leverage. Contract renewals can pressure pricing and service levels, but PKO’s scale supports multi-vendor strategies and tougher negotiations. Ongoing KNF and EBA operational resilience scrutiny further disciplines suppliers.

Wholesale funding providers

Wholesale funding—interbank lines, capital markets, and covered bonds—supplements deposits, but in stressed markets spreads can widen and covenants tighten, increasing supplier power. PKO Bank Polski, Poland’s largest bank by assets, mitigates this through a strong brand, deep collateral pools and a robust balance sheet. Diversified maturities and instruments reduce concentration risk and reliance on any single provider.

Payment schemes and processors

Card networks and payment rails set fees and technical standards—Visa processed about $14.9tn TPV in FY2023—giving them leverage, particularly on interchange and compliance mandates. EU interchange caps (0.2% debit, 0.3% credit) limit fees but do not eliminate scheme rule power. PKO mitigates through scale, co‑brand deals and routing to domestic switches. Rising instant payments (growing adoption in 2023–24) may rebalance dynamics.

Talent and specialist skills

- Talent pool: c.500,000 IT specialists (2024)

- PKO scale: c.25,000 employees

- Mitigants: training, automation, nearshoring

Data and credit bureaus

External data, ratings and credit bureau inputs (notably BIK and BIG InfoMonitor) materially shape PKO Bank Polski underwriting and compliance, creating supplier leverage where niche datasets have limited alternatives and can raise costs and lock-in. PKO can blend rich internal customer data with PSD2 open-banking feeds to reduce dependence, while EU and Polish regulatory open-data initiatives from 2018 onward may further weaken supplier clout.

- BIK, BIG InfoMonitor: primary bureau providers

- PSD2 (2018): enables open-banking data aggregation

- Internal data + open banking: lowers bureau reliance

Polish bank balances vendor leverage, funding stress and IT talent squeeze

PKO faces supplier leverage from core IT, cloud and cybersecurity vendors and card schemes, but its scale and multi-vendor approach strengthen negotiating power. Wholesale funding lines and capital markets raise supplier risk in stress, partially offset by deep collateral and diversified maturities. Talent scarcity (c.500,000 IT specialists in Poland) and bureau reliance raise costs, mitigated by PKO’s c.25,000 staff, training and automation.

| Item | 2024 figure | Impact |

|---|---|---|

| PKO employees | c.25,000 | negotiation scale |

| Poland IT pool | c.500,000 | talent pressure |

| Visa TPV | $14.9tn (FY2023) | scheme leverage |

| Interchange caps | 0.2% debit / 0.3% credit | fee limits |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to PKO Bank Polski; evaluates supplier and buyer power, substitutes, rivalry and barriers to entry, identifying disruptive threats and strategic protections for the bank’s market position.

One-sheet Porter's Five Forces for PKO Bank Polski—instantly visualizes competitive pressure with a spider chart and editable stress levels, so teams can customize threats, copy into decks, and make fast, board-ready strategic decisions.

Customers Bargaining Power

Price-sensitive retail customers

Retail customers increasingly compare rates and fees via digital channels, raising transparency and price sensitivity for PKO Bank Polski.

Improved account portability has lowered switching costs, though PKO remains Poland's largest bank by assets, serving over 9 million retail customers in 2024, which mitigates churn.

Its broad product suite and loyalty ecosystem (multi-product penetration above industry averages) reduce buyer power.

Strong brand trust and ~1,000 branches continue to temper customer leverage in key segments.

Large corporates and institutions

Large corporates negotiate bespoke pricing and SLAs, leveraging transaction volumes and multi-banking to exert strong bargaining power against PKO Bank Polski, Poland's largest bank by assets with about 20% market share in 2024.

They pressure margins on cash management, trade finance and lending packages, where PKO competes intensively.

Deep relationships and cross-sell of treasury, FX and lending products help PKO defend spreads and retain strategic corporate clients.

Digital adoption and UX expectations

Customers demand seamless mobile onboarding, instant payments and 24/7 service, with Polish mobile banking adoption exceeding 70% in 2024; poor UX leads to rapid switching to nimble fintechs. PKO’s IKO and iPKO platforms—IKO reporting over 8 million users in 2024—help meet expectations and retain volumes as digital transactions surpass 70% of retail activity. Continuous feature rollout and faster onboarding are needed to curb growing buyer leverage.

Access to alternatives

Fintech wallets, BNPL, brokers and neo-banks deliver lower-cost point solutions, expanding choice and raising customers' negotiation leverage; BNPL/neo-bank users in Poland rose ~30% YoY to ~6m users by 2024, intensifying price pressure on incumbents.

PKO mitigates this via integrated retail and corporate bundles, cross-sell (serving ~10m clients, ~18% market share in 2024) and trust-based full-service relationships for complex credit and corporate needs.

- Fintechs: lower cost, point solutions

- BNPL/neo-banks: ~6m Polish users (2024)

- PKO: ~10m clients, ~18% market share (2024)

- Advantage: trust, integrated full-service bundles

Information transparency

Aggregators and comparison sites reveal pricing and performance instantly, increasing switching by informed customers. Reviews and social media amplify service issues, forcing PKO Bank Polski — serving about 8.6 million clients and holding roughly 31% of Polish banking assets in 2023–24 — to maintain consistent quality to avoid discount pressure. Clear communication and financial education can shift buyer focus from price to value.

- Instant transparency drives price sensitivity

- Reputation risk amplified by social media

- PKO must prioritize service consistency (8.6m clients, ~31% market share)

- Education reduces churn

>70% mobile shifts power to price-sensitive Polish retail banking

Customers are more price-sensitive due to digital comparison and >70% mobile banking adoption in Poland (2024), raising retail bargaining power.

PKO’s scale—~10m clients and ~18% market share in 2024—and IKO’s ~8m users limit churn via cross-sell and trust.

Fintechs/BNPL (~6m users in 2024) and corporate multi-banking pressure fees on transaction and lending margins.

| Metric | 2024 |

|---|---|

| PKO clients | ~10m |

| Market share | ~18% |

| IKO users | ~8m |

| Mobile adoption (PL) | >70% |

| BNPL/neo-bank users | ~6m |

What You See Is What You Get

PKO Bank Polski Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of PKO Bank Polski you'll receive after purchase—no placeholders or samples. The document assesses competitive rivalry, buyer and supplier power, and the threats of entry and substitutes with clear strategic implications. It's the final, fully formatted file ready for immediate download and use.