Plug Power Porter's Five Forces Analysis

From Overview to Strategy Blueprint

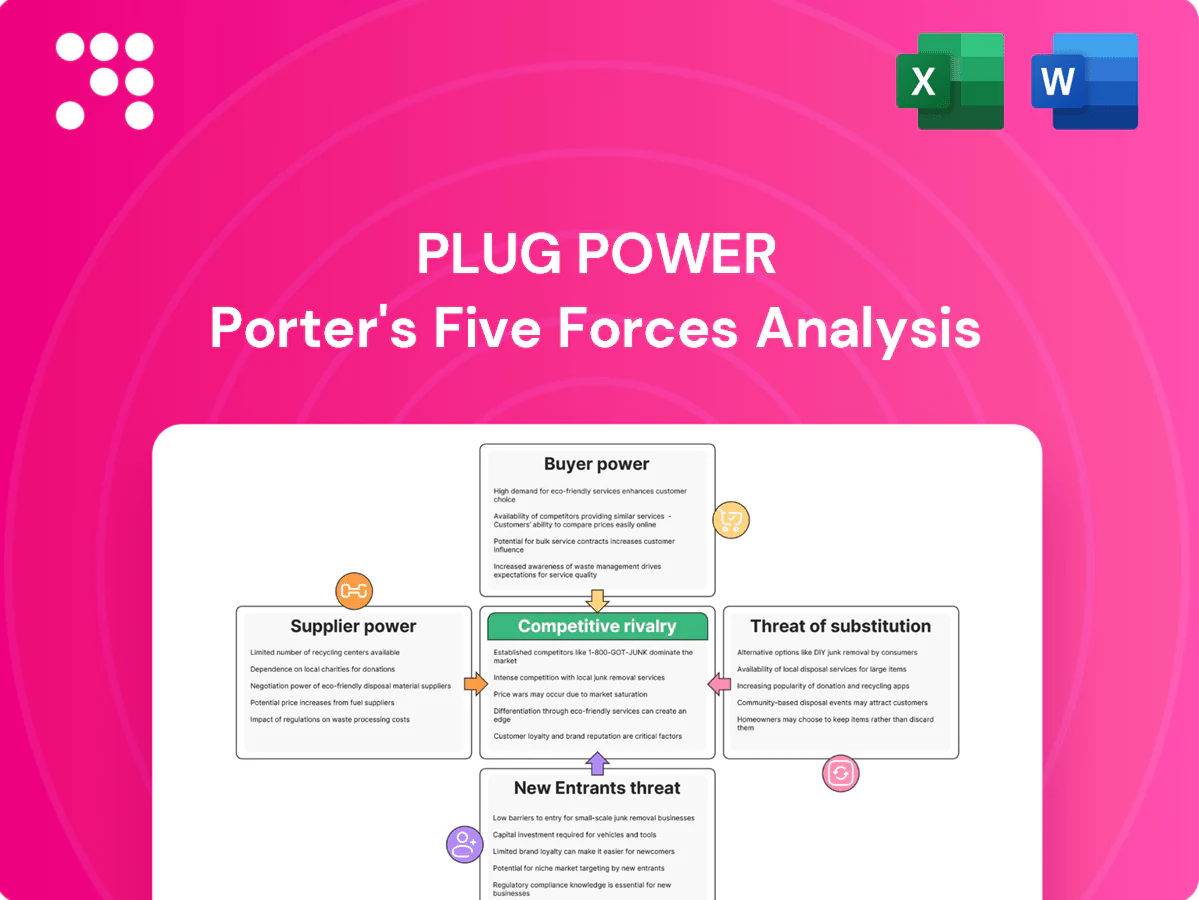

Plug Power faces intense supplier and buyer dynamics, emerging substitute risks from alternative clean-energy tech, and high capital barriers shaping competitive rivalry; this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Plug Power’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized PEM materials

Specialized PEM membranes, bipolar plates and gaskets are often sourced from fewer than 5 qualified vendors, concentrating pricing and lead‑time leverage in suppliers.

Qualification cycles commonly take 6–18 months and stack performance ties to supplier materials raise switching costs and barriers to rapid change.

Any supplier disruption can ripple through stack output and SLAs, while targeted multi‑sourcing and selective in‑house development partially offset this concentration risk.

PGM catalyst volatility

PGM catalyst volatility raises stack costs and squeezes margins as platinum group metals, with South Africa supplying ~70% of platinum, saw price swings often exceeding 20% YoY in recent cycles; long-term hedges (3–5 year contracts) dampen but do not remove short-term shocks. Reducing catalyst loading is strategic yet requires multi-year redesigns, while recycling programs can recover up to ~90% of PGMs over product lifecycles to ease supply dependence.

Electrolyzer and balance-of-plant

Compressors, power electronics and cryogenic systems are concentrated among a few global OEMs, with the announced electrolyzer pipeline topping ~200 GW by end-2024, amplifying supplier leverage. Long-lead items (often 6–24 months) create scheduling risk for hydrogen plants and elevate costs when demand spikes across projects. Supplier bargaining power surged in 2024 during procurement waves; strategic partnerships and frame agreements have materially improved availability and pricing terms.

Renewable power for green H2

PPAs and grid access largely set green H2 costs and uptime; average US solar PPA prices fell toward ~$25–35/MWh in 2024, but interconnection queue backlogs exceeding 1,000 GW give utilities and IPPs leverage over timing and pricing. Congestion and curtailment risks compress Plug Power’s negotiating power, while co-location and behind-the-meter PPAs can cut exposure and stabilize offtake economics.

- PPAs ~25–35/MWh (US, 2024)

- Interconnection backlog >1,000 GW (2024)

- Co-location reduces curtailment/uplink risk

Hydrogen logistics and storage

Liquid hydrogen equipment, trailers and storage tanks require certified vendors and stringent permitting, concentrating supplier power and limiting choices; in 2024 lead times for cryogenic trailers extended to roughly 12–18 months, elevating costs and delaying deployments. Building proprietary logistics reduces reliance but raises capital intensity and operational cash needs, pressuring margins and rollout speed.

- Certified vendors concentrated

- 12–18 month lead times (2024)

- Higher capex for proprietary logistics

- Permitting limits supplier pool

Supplier leverage spikes: PGM volatility (South Africa ~70%), >1,000 GW backlog, 12-18m cryo lead

Supplier power is high: critical PEM/plate/gasket vendors <5, long qualification (6–18m) and limited OEMs for compressors/electrolyzers concentrate leverage. PGM volatility (South Africa ~70% supply) and 20%+ YoY swings raise stack costs despite 3–5y hedges and recycling. Grid/PPAs (US solar ~25–35/MWh) and >1,000 GW interconnection backlog plus 12–18m cryo lead times amplify supplier negotiation risk.

| Metric | 2024 | Impact |

|---|---|---|

| PGM supply (SA) | ~70% | Price volatility |

| Interconnection backlog | >1,000 GW | Timing leverage |

| Cryo trailer lead time | 12–18 months | Deployment delays |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks tailored exclusively for Plug Power, identifying disruptive substitutes, emerging threats, and strategic levers that affect pricing, profitability, and market share.

One-sheet Plug Power Porter's Five Forces—quickly pinpoint hydrogen fuel cell competitive pressures and priority actions for management and investors.

Customers Bargaining Power

Concentrated anchor customers

Concentrated anchor customers in material handling and mobility extract steep discounts and custom commercial terms, using scale to pressure pricing across Plug Power’s portfolio. Their renewal negotiations are frequent flashpoints that can shift margins and delivery priorities. Reference value to new buyers is high, but the potential churn from a lost anchor customer poses a material revenue and growth risk.

TCO-driven procurement

Buyers benchmark fuel cells vs Li-ion and diesel on TCO and uptime, using 2023–24 BNEF battery pack benchmarks (~132 USD/kWh in 2023) and diesel retail around ~3.8 USD/gal (2024) to model costs. Fuel price, incentives and maintenance assumptions swing procurement; green hydrogen spot costs often exceed 5 USD/kg in 2024, so buyers demand price concessions. Performance guarantees shift uptime and replacement risk back to Plug.

Multi-sourcing and trials

Customers pilot multiple hydrogen and fuel-cell technologies before scaling, which raises their likelihood to switch and strengthens bargaining leverage. Standardized interfaces and fuel formats lower technical switching costs, making replacements operationally easier. Vendor stickiness usually only materializes after full site integration and fleet-wide rollout, when switching costs and downtime risks rise.

Backward integration options

Large logistics and energy players can build or procure hydrogen assets in-house, reducing dependence on a single OEM and increasing customers bargaining power; buyers increasingly unbundle equipment, fuel and service contracts, forcing Plug Power to defend margins by selling bundled value.

To retain pricing power Plug must emphasize integrated solutions, long-term fuel contracts and service guarantees, as unbundling enables customers to mix suppliers and squeeze OEM margins.

- Backward integration risk: customers can internalize hydrogen supply

- Unbundling trend: separates equipment, fuel, service

- Defensive move: bundled solutions, long-term contracts, guaranteed uptime

Policy-linked demand

Policy-linked demand makes buyers sensitive to incentive shifts; the IRS 45V hydrogen tax credit guidance in 2024 (up to 3 per kg for qualifying H2) means when credits weaken customers often renegotiate or delay purchases, using timing as leverage to extract better terms or defer capex. Firm offtake and floor-price structures reduce that leverage by stabilizing revenue expectations for suppliers like Plug Power.

- 45V: up to 3 per kg (IRS guidance 2024)

- Buyers renegotiate/delay when credits wane

- Timing = bargaining chip

- Offtake + floor prices stabilize deals

Anchor buyers force discounts: green H2 >5 USD/kg, Li-ion 132 USD/kWh, 45V shifts leverage

Concentrated anchor buyers extract steep discounts and can pivot procurement, risking churn and margin pressure. Buyers benchmark fuel cells vs Li-ion (~132 USD/kWh in 2023) and diesel (~3.8 USD/gal in 2024); green H2 spot often >5 USD/kg (2024), prompting price concessions. IRS 45V guidance (up to 3 USD/kg, 2024) makes incentives a bargaining chip; offtake/floor prices reduce leverage.

| Metric | Value (year) |

|---|---|

| Battery pack | ~132 USD/kWh (2023) |

| Diesel retail | ~3.8 USD/gal (2024) |

| Green H2 spot | >5 USD/kg (2024) |

| IRS 45V credit | up to 3 USD/kg (2024) |

Preview Before You Purchase

Plug Power Porter's Five Forces Analysis

This preview shows the exact Plug Power Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy. You're viewing the final deliverable.

From Overview to Strategy Blueprint

Plug Power faces intense supplier and buyer dynamics, emerging substitute risks from alternative clean-energy tech, and high capital barriers shaping competitive rivalry; this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Plug Power’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized PEM materials

Specialized PEM membranes, bipolar plates and gaskets are often sourced from fewer than 5 qualified vendors, concentrating pricing and lead‑time leverage in suppliers.

Qualification cycles commonly take 6–18 months and stack performance ties to supplier materials raise switching costs and barriers to rapid change.

Any supplier disruption can ripple through stack output and SLAs, while targeted multi‑sourcing and selective in‑house development partially offset this concentration risk.

PGM catalyst volatility

PGM catalyst volatility raises stack costs and squeezes margins as platinum group metals, with South Africa supplying ~70% of platinum, saw price swings often exceeding 20% YoY in recent cycles; long-term hedges (3–5 year contracts) dampen but do not remove short-term shocks. Reducing catalyst loading is strategic yet requires multi-year redesigns, while recycling programs can recover up to ~90% of PGMs over product lifecycles to ease supply dependence.

Electrolyzer and balance-of-plant

Compressors, power electronics and cryogenic systems are concentrated among a few global OEMs, with the announced electrolyzer pipeline topping ~200 GW by end-2024, amplifying supplier leverage. Long-lead items (often 6–24 months) create scheduling risk for hydrogen plants and elevate costs when demand spikes across projects. Supplier bargaining power surged in 2024 during procurement waves; strategic partnerships and frame agreements have materially improved availability and pricing terms.

Renewable power for green H2

PPAs and grid access largely set green H2 costs and uptime; average US solar PPA prices fell toward ~$25–35/MWh in 2024, but interconnection queue backlogs exceeding 1,000 GW give utilities and IPPs leverage over timing and pricing. Congestion and curtailment risks compress Plug Power’s negotiating power, while co-location and behind-the-meter PPAs can cut exposure and stabilize offtake economics.

- PPAs ~25–35/MWh (US, 2024)

- Interconnection backlog >1,000 GW (2024)

- Co-location reduces curtailment/uplink risk

Hydrogen logistics and storage

Liquid hydrogen equipment, trailers and storage tanks require certified vendors and stringent permitting, concentrating supplier power and limiting choices; in 2024 lead times for cryogenic trailers extended to roughly 12–18 months, elevating costs and delaying deployments. Building proprietary logistics reduces reliance but raises capital intensity and operational cash needs, pressuring margins and rollout speed.

- Certified vendors concentrated

- 12–18 month lead times (2024)

- Higher capex for proprietary logistics

- Permitting limits supplier pool

Supplier leverage spikes: PGM volatility (South Africa ~70%), >1,000 GW backlog, 12-18m cryo lead

Supplier power is high: critical PEM/plate/gasket vendors <5, long qualification (6–18m) and limited OEMs for compressors/electrolyzers concentrate leverage. PGM volatility (South Africa ~70% supply) and 20%+ YoY swings raise stack costs despite 3–5y hedges and recycling. Grid/PPAs (US solar ~25–35/MWh) and >1,000 GW interconnection backlog plus 12–18m cryo lead times amplify supplier negotiation risk.

| Metric | 2024 | Impact |

|---|---|---|

| PGM supply (SA) | ~70% | Price volatility |

| Interconnection backlog | >1,000 GW | Timing leverage |

| Cryo trailer lead time | 12–18 months | Deployment delays |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks tailored exclusively for Plug Power, identifying disruptive substitutes, emerging threats, and strategic levers that affect pricing, profitability, and market share.

One-sheet Plug Power Porter's Five Forces—quickly pinpoint hydrogen fuel cell competitive pressures and priority actions for management and investors.

Customers Bargaining Power

Concentrated anchor customers

Concentrated anchor customers in material handling and mobility extract steep discounts and custom commercial terms, using scale to pressure pricing across Plug Power’s portfolio. Their renewal negotiations are frequent flashpoints that can shift margins and delivery priorities. Reference value to new buyers is high, but the potential churn from a lost anchor customer poses a material revenue and growth risk.

TCO-driven procurement

Buyers benchmark fuel cells vs Li-ion and diesel on TCO and uptime, using 2023–24 BNEF battery pack benchmarks (~132 USD/kWh in 2023) and diesel retail around ~3.8 USD/gal (2024) to model costs. Fuel price, incentives and maintenance assumptions swing procurement; green hydrogen spot costs often exceed 5 USD/kg in 2024, so buyers demand price concessions. Performance guarantees shift uptime and replacement risk back to Plug.

Multi-sourcing and trials

Customers pilot multiple hydrogen and fuel-cell technologies before scaling, which raises their likelihood to switch and strengthens bargaining leverage. Standardized interfaces and fuel formats lower technical switching costs, making replacements operationally easier. Vendor stickiness usually only materializes after full site integration and fleet-wide rollout, when switching costs and downtime risks rise.

Backward integration options

Large logistics and energy players can build or procure hydrogen assets in-house, reducing dependence on a single OEM and increasing customers bargaining power; buyers increasingly unbundle equipment, fuel and service contracts, forcing Plug Power to defend margins by selling bundled value.

To retain pricing power Plug must emphasize integrated solutions, long-term fuel contracts and service guarantees, as unbundling enables customers to mix suppliers and squeeze OEM margins.

- Backward integration risk: customers can internalize hydrogen supply

- Unbundling trend: separates equipment, fuel, service

- Defensive move: bundled solutions, long-term contracts, guaranteed uptime

Policy-linked demand

Policy-linked demand makes buyers sensitive to incentive shifts; the IRS 45V hydrogen tax credit guidance in 2024 (up to 3 per kg for qualifying H2) means when credits weaken customers often renegotiate or delay purchases, using timing as leverage to extract better terms or defer capex. Firm offtake and floor-price structures reduce that leverage by stabilizing revenue expectations for suppliers like Plug Power.

- 45V: up to 3 per kg (IRS guidance 2024)

- Buyers renegotiate/delay when credits wane

- Timing = bargaining chip

- Offtake + floor prices stabilize deals

Anchor buyers force discounts: green H2 >5 USD/kg, Li-ion 132 USD/kWh, 45V shifts leverage

Concentrated anchor buyers extract steep discounts and can pivot procurement, risking churn and margin pressure. Buyers benchmark fuel cells vs Li-ion (~132 USD/kWh in 2023) and diesel (~3.8 USD/gal in 2024); green H2 spot often >5 USD/kg (2024), prompting price concessions. IRS 45V guidance (up to 3 USD/kg, 2024) makes incentives a bargaining chip; offtake/floor prices reduce leverage.

| Metric | Value (year) |

|---|---|

| Battery pack | ~132 USD/kWh (2023) |

| Diesel retail | ~3.8 USD/gal (2024) |

| Green H2 spot | >5 USD/kg (2024) |

| IRS 45V credit | up to 3 USD/kg (2024) |

Preview Before You Purchase

Plug Power Porter's Five Forces Analysis

This preview shows the exact Plug Power Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy. You're viewing the final deliverable.

Description

From Overview to Strategy Blueprint

Plug Power faces intense supplier and buyer dynamics, emerging substitute risks from alternative clean-energy tech, and high capital barriers shaping competitive rivalry; this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Plug Power’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized PEM materials

Specialized PEM membranes, bipolar plates and gaskets are often sourced from fewer than 5 qualified vendors, concentrating pricing and lead‑time leverage in suppliers.

Qualification cycles commonly take 6–18 months and stack performance ties to supplier materials raise switching costs and barriers to rapid change.

Any supplier disruption can ripple through stack output and SLAs, while targeted multi‑sourcing and selective in‑house development partially offset this concentration risk.

PGM catalyst volatility

PGM catalyst volatility raises stack costs and squeezes margins as platinum group metals, with South Africa supplying ~70% of platinum, saw price swings often exceeding 20% YoY in recent cycles; long-term hedges (3–5 year contracts) dampen but do not remove short-term shocks. Reducing catalyst loading is strategic yet requires multi-year redesigns, while recycling programs can recover up to ~90% of PGMs over product lifecycles to ease supply dependence.

Electrolyzer and balance-of-plant

Compressors, power electronics and cryogenic systems are concentrated among a few global OEMs, with the announced electrolyzer pipeline topping ~200 GW by end-2024, amplifying supplier leverage. Long-lead items (often 6–24 months) create scheduling risk for hydrogen plants and elevate costs when demand spikes across projects. Supplier bargaining power surged in 2024 during procurement waves; strategic partnerships and frame agreements have materially improved availability and pricing terms.

Renewable power for green H2

PPAs and grid access largely set green H2 costs and uptime; average US solar PPA prices fell toward ~$25–35/MWh in 2024, but interconnection queue backlogs exceeding 1,000 GW give utilities and IPPs leverage over timing and pricing. Congestion and curtailment risks compress Plug Power’s negotiating power, while co-location and behind-the-meter PPAs can cut exposure and stabilize offtake economics.

- PPAs ~25–35/MWh (US, 2024)

- Interconnection backlog >1,000 GW (2024)

- Co-location reduces curtailment/uplink risk

Hydrogen logistics and storage

Liquid hydrogen equipment, trailers and storage tanks require certified vendors and stringent permitting, concentrating supplier power and limiting choices; in 2024 lead times for cryogenic trailers extended to roughly 12–18 months, elevating costs and delaying deployments. Building proprietary logistics reduces reliance but raises capital intensity and operational cash needs, pressuring margins and rollout speed.

- Certified vendors concentrated

- 12–18 month lead times (2024)

- Higher capex for proprietary logistics

- Permitting limits supplier pool

Supplier leverage spikes: PGM volatility (South Africa ~70%), >1,000 GW backlog, 12-18m cryo lead

Supplier power is high: critical PEM/plate/gasket vendors <5, long qualification (6–18m) and limited OEMs for compressors/electrolyzers concentrate leverage. PGM volatility (South Africa ~70% supply) and 20%+ YoY swings raise stack costs despite 3–5y hedges and recycling. Grid/PPAs (US solar ~25–35/MWh) and >1,000 GW interconnection backlog plus 12–18m cryo lead times amplify supplier negotiation risk.

| Metric | 2024 | Impact |

|---|---|---|

| PGM supply (SA) | ~70% | Price volatility |

| Interconnection backlog | >1,000 GW | Timing leverage |

| Cryo trailer lead time | 12–18 months | Deployment delays |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and market entry risks tailored exclusively for Plug Power, identifying disruptive substitutes, emerging threats, and strategic levers that affect pricing, profitability, and market share.

One-sheet Plug Power Porter's Five Forces—quickly pinpoint hydrogen fuel cell competitive pressures and priority actions for management and investors.

Customers Bargaining Power

Concentrated anchor customers

Concentrated anchor customers in material handling and mobility extract steep discounts and custom commercial terms, using scale to pressure pricing across Plug Power’s portfolio. Their renewal negotiations are frequent flashpoints that can shift margins and delivery priorities. Reference value to new buyers is high, but the potential churn from a lost anchor customer poses a material revenue and growth risk.

TCO-driven procurement

Buyers benchmark fuel cells vs Li-ion and diesel on TCO and uptime, using 2023–24 BNEF battery pack benchmarks (~132 USD/kWh in 2023) and diesel retail around ~3.8 USD/gal (2024) to model costs. Fuel price, incentives and maintenance assumptions swing procurement; green hydrogen spot costs often exceed 5 USD/kg in 2024, so buyers demand price concessions. Performance guarantees shift uptime and replacement risk back to Plug.

Multi-sourcing and trials

Customers pilot multiple hydrogen and fuel-cell technologies before scaling, which raises their likelihood to switch and strengthens bargaining leverage. Standardized interfaces and fuel formats lower technical switching costs, making replacements operationally easier. Vendor stickiness usually only materializes after full site integration and fleet-wide rollout, when switching costs and downtime risks rise.

Backward integration options

Large logistics and energy players can build or procure hydrogen assets in-house, reducing dependence on a single OEM and increasing customers bargaining power; buyers increasingly unbundle equipment, fuel and service contracts, forcing Plug Power to defend margins by selling bundled value.

To retain pricing power Plug must emphasize integrated solutions, long-term fuel contracts and service guarantees, as unbundling enables customers to mix suppliers and squeeze OEM margins.

- Backward integration risk: customers can internalize hydrogen supply

- Unbundling trend: separates equipment, fuel, service

- Defensive move: bundled solutions, long-term contracts, guaranteed uptime

Policy-linked demand

Policy-linked demand makes buyers sensitive to incentive shifts; the IRS 45V hydrogen tax credit guidance in 2024 (up to 3 per kg for qualifying H2) means when credits weaken customers often renegotiate or delay purchases, using timing as leverage to extract better terms or defer capex. Firm offtake and floor-price structures reduce that leverage by stabilizing revenue expectations for suppliers like Plug Power.

- 45V: up to 3 per kg (IRS guidance 2024)

- Buyers renegotiate/delay when credits wane

- Timing = bargaining chip

- Offtake + floor prices stabilize deals

Anchor buyers force discounts: green H2 >5 USD/kg, Li-ion 132 USD/kWh, 45V shifts leverage

Concentrated anchor buyers extract steep discounts and can pivot procurement, risking churn and margin pressure. Buyers benchmark fuel cells vs Li-ion (~132 USD/kWh in 2023) and diesel (~3.8 USD/gal in 2024); green H2 spot often >5 USD/kg (2024), prompting price concessions. IRS 45V guidance (up to 3 USD/kg, 2024) makes incentives a bargaining chip; offtake/floor prices reduce leverage.

| Metric | Value (year) |

|---|---|

| Battery pack | ~132 USD/kWh (2023) |

| Diesel retail | ~3.8 USD/gal (2024) |

| Green H2 spot | >5 USD/kg (2024) |

| IRS 45V credit | up to 3 USD/kg (2024) |

Preview Before You Purchase

Plug Power Porter's Five Forces Analysis

This preview shows the exact Plug Power Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy. You're viewing the final deliverable.