Plug Power PESTLE Analysis

Skip the Research. Get the Strategy.

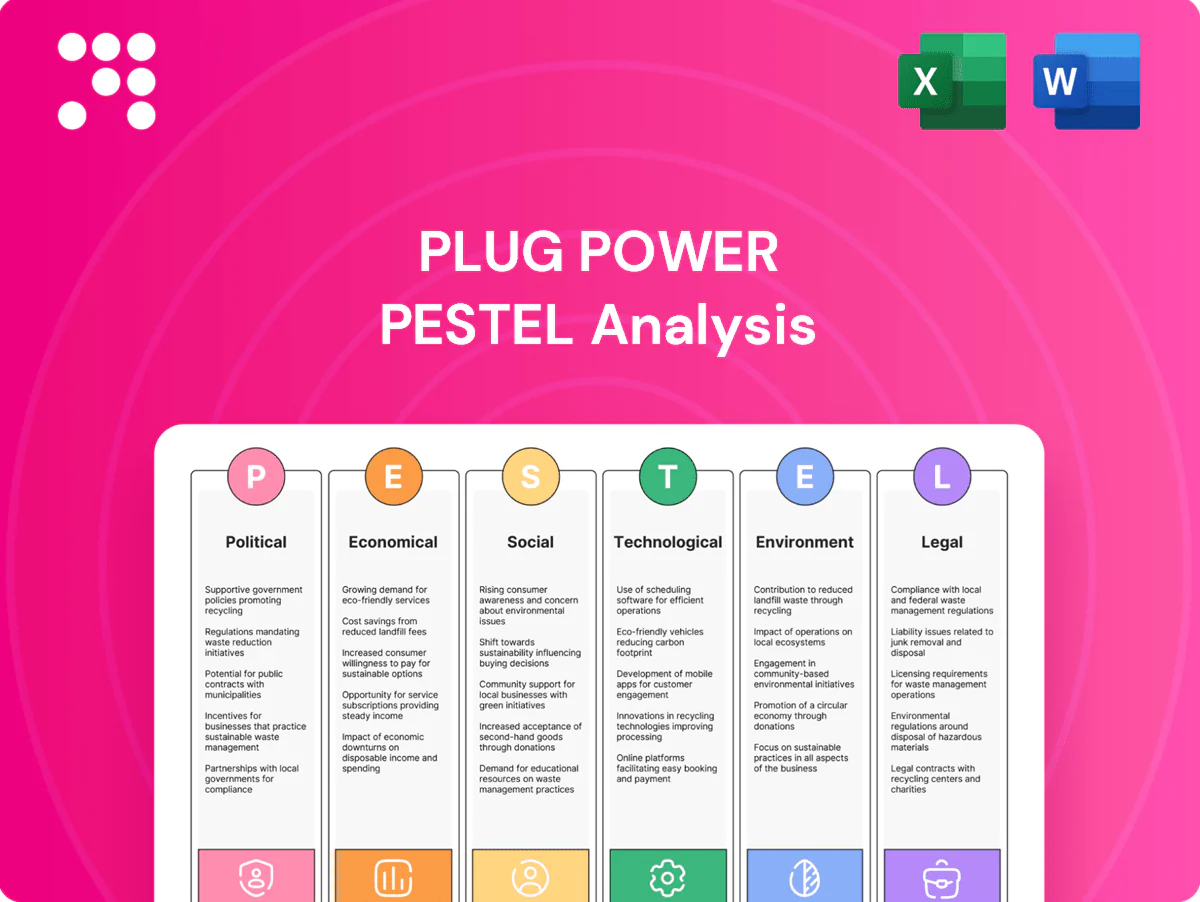

Unlock strategic clarity with our PESTLE Analysis of Plug Power—concise, data-driven insight into political, economic, social, technological, legal and environmental forces shaping its prospects. Ideal for investors and strategists, it's ready to use and editable. Purchase the full report for the complete breakdown and actionable recommendations.

Political factors

Hydrogen subsidies

U.S. IRA 45V clean hydrogen credit—worth up to $3 per kg for ultra-low carbon H2—and EU hydrogen incentives including the EU Hydrogen Bank (estimated €3–5 billion initial support) materially improve green hydrogen project IRRs; Plug Power’s electrolyzer and fuel cell rollouts hinge on the clarity, value and multi-year duration of these supports, while policy revisions, claw-backs or disbursement delays can push investment timelines and alter site selection, making government advocacy and policy alignment core strategic priorities.

Permitting and siting

Hydrogen plants require multi-jurisdictional permits across generation, storage, safety and transportation, and DOE’s $8 billion Hydrogen Hubs program (first 7 hubs selected in 2023) shows federal-state coordination matters. Streamlined approvals can accelerate Plug Power’s build-out; fragmented or slow processes raise capex and O&M risk. Community engagement and state cooperation are decisive, so permitting risk must be priced into project pipelines.

Energy security agendas

Energy security agendas push governments to prioritize domestic clean supply chains, driven by policies like the Inflation Reduction Act's roughly 369 billion USD in climate incentives and DOE funding of seven hydrogen hubs ~7 billion USD, creating localization incentives and PPP opportunities for Plug Power. Policy-driven procurement (federal ZEV targets to 2035) can catalyze demand, but national content rules may raise costs or restrict sourcing, squeezing margins against Plug Power's ~588 million USD 2023 revenue.

Trade and tariffs

Tariffs on metals (US Section 232: 25% steel, 10% aluminum) and restrictions on renewables components raise Plug Power’s BOM costs and squeeze margins. Export controls and customs delays add weeks to cross-border electrolyzer deployments, complicating project timelines. Plug must diversify suppliers, use hedges and localize sourcing since trade-policy shifts can change global competitiveness overnight.

- Tariffs: 25% steel, 10% aluminum

- Delays: weeks added to deployments

- Mitigation: supplier diversification, sourcing local

Public funding competition

Grants, loan guarantees and the DOE's $7 billion hydrogen hubs program plus the IRA's clean hydrogen PTC (up to $3/kg) have drawn many competitors, making selection outcomes crucial to Plug Power's market access and regional footprint; awards determine capacity build-outs and offtake visibility. Co-funding rules and milestone-based payments improve execution discipline but raise compliance and cash-flow demands, so balancing participation across programs reduces concentration risk.

- Grants/LOAN: DOE $7B hubs

- PTC: up to $3/kg

- Impact: awards drive regional access

- Risk: co-funding/compliance burden

- Mitigation: diversify across programs

IRA H2 credit up to $3/kg and $8B DOE hubs lift IRRs; tariffs raise capex, localize supply

IRA clean hydrogen credit up to $3/kg and DOE $8B Hydrogen Hubs (first 7 in 2023) materially lift project IRRs; policy clarity and multi-year duration are critical. Permitting delays and tariffs (25% steel, 10% aluminum) raise capex and timelines. Plug Power (2023 revenue 588M USD) must localize supply and secure awards to de-risk pipelines.

| Policy | Value/Size | Impact |

|---|---|---|

| IRA H2 PTC | up to 3 USD/kg | Improves IRR |

| DOE Hubs | 8 B USD | Regional access |

| Tariffs | 25% steel/10% Al | Raises BOM cost |

What is included in the product

Explores how macro-environmental factors uniquely affect Plug Power across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific examples; designed for executives and investors to identify risks, opportunities and actionable, forward-looking strategic insights.

Condenses Plug Power's PESTLE into a clean, editable summary that highlights regulatory, market and technological risks and opportunities for quick inclusion in presentations or team briefings.

Economic factors

Capital intensity

Building green hydrogen plants, logistics and refueling networks is highly capex‑intensive; project economics are driven by 2024 US policy and markets, including the Inflation Reduction Act H2 tax credit of up to 3 USD/kg and a Federal Funds rate near 5.25–5.50% that raises financing costs. Plug’s access to tax equity, project finance and offtake‑backed debt determines WACC and viability, while scale reduces unit costs but increases execution and delivery risk.

Hydrogen price volatility

Levelized cost of hydrogen is driven mainly by electricity, capacity factor and electrolyzer efficiency: modern PEM/alkaline electrolysis typically requires ~45–55 kWh/kg H2, so at $40–60/MWh (typical wholesale ranges in 2023–24) electricity alone can add roughly $1.8–$3.3/kg. Wholesale price volatility therefore compresses margins; long-term PPAs and hedges (commonly used across the industry) stabilize economics. Plug Power’s integrated model aims to capture spreads across production, storage and offtake to mitigate this volatility.

Demand ramp and adoption

Material handling, mobility and industrial adoption for Plug Power scale unevenly across regions, with North America and Europe leading deployments while APAC lags; Plug Power reported 2024 revenue of $1.34B and points to regional concentration of orders. Fleet conversions and heavy‑duty transport contracts trigger step‑change volumes when offtakes convert, creating lumpy demand. Cyclicality in logistics and manufacturing shifts order timing quarter‑to‑quarter. Plug must balance inventory, service capacity and pipeline health to avoid margin pressure.

Supply chain constraints

Supply-chain constraints for Plug Power center on PGMs, membranes, power electronics and compressors, which can bottleneck system output and delay deployments.

Localization of manufacturing lowers freight and tariff exposure but requires sizable upfront capital and facility lead times; strategic sourcing and dual-sourcing mitigate single-point failures.

Commodity price swings in PGMs and polymers pass through to product pricing and long-term contracts, increasing margin volatility and requiring indexed pricing clauses.

- PGMs: critical single-source risk

- Localization: reduces logistics/tariff risk but ups CAPEX

- Dual-sourcing: lowers disruption probability

- Commodity swings: feed-through to pricing/contracts

Currency and global exposure

Plug Power's revenues and costs span USD, EUR and other currencies as the company expanded European deployments in 2024; full-year 2024 revenue was about $1.02 billion, exposing reported results to FX translation effects. FX movements have materially affected quarterly EPS and project ROIs, while natural hedges from Euro-denominated sales vs. Euro costs reduce but do not eliminate exposure. The company uses financial hedges and considers country risk premiums when pricing bids into Europe and Latin America.

- USD/EUR exposure: material post-2024 European growth

- Hedging: natural hedges + financial instruments used

- Country risk premiums: affect bid competitiveness and ROI

IRA H2 credit up to $3/kg and $8B DOE hubs lift IRRs; tariffs raise capex, localize supply

Capex‑heavy green H2 projects depend on IRA H2 credit up to 3 USD/kg, Fed Funds ~5.25–5.50% raising WACC, and Plug Power 2024 revenue ~1.02B USD—access to tax equity and offtake finance is decisive. LCoH driven by 45–55 kWh/kg and $40–60/MWh power (~1.8–3.3 USD/kg electricity); PPAs/hedges stabilize margins. PGMs, membranes and compressors remain supply bottlenecks.

| Metric | Value (2024) |

|---|---|

| Revenue | 1.02B USD |

| IRA H2 credit | up to 3 USD/kg |

| Electricity | 40–60 USD/MWh |

| Electrolyzer use | 45–55 kWh/kg |

Preview the Actual Deliverable

Plug Power PESTLE Analysis

The preview shown here is the exact Plug Power PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and insights visible are the final file with no placeholders. You’ll be able to download this exact document immediately after checkout.

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Plug Power—concise, data-driven insight into political, economic, social, technological, legal and environmental forces shaping its prospects. Ideal for investors and strategists, it's ready to use and editable. Purchase the full report for the complete breakdown and actionable recommendations.

Political factors

Hydrogen subsidies

U.S. IRA 45V clean hydrogen credit—worth up to $3 per kg for ultra-low carbon H2—and EU hydrogen incentives including the EU Hydrogen Bank (estimated €3–5 billion initial support) materially improve green hydrogen project IRRs; Plug Power’s electrolyzer and fuel cell rollouts hinge on the clarity, value and multi-year duration of these supports, while policy revisions, claw-backs or disbursement delays can push investment timelines and alter site selection, making government advocacy and policy alignment core strategic priorities.

Permitting and siting

Hydrogen plants require multi-jurisdictional permits across generation, storage, safety and transportation, and DOE’s $8 billion Hydrogen Hubs program (first 7 hubs selected in 2023) shows federal-state coordination matters. Streamlined approvals can accelerate Plug Power’s build-out; fragmented or slow processes raise capex and O&M risk. Community engagement and state cooperation are decisive, so permitting risk must be priced into project pipelines.

Energy security agendas

Energy security agendas push governments to prioritize domestic clean supply chains, driven by policies like the Inflation Reduction Act's roughly 369 billion USD in climate incentives and DOE funding of seven hydrogen hubs ~7 billion USD, creating localization incentives and PPP opportunities for Plug Power. Policy-driven procurement (federal ZEV targets to 2035) can catalyze demand, but national content rules may raise costs or restrict sourcing, squeezing margins against Plug Power's ~588 million USD 2023 revenue.

Trade and tariffs

Tariffs on metals (US Section 232: 25% steel, 10% aluminum) and restrictions on renewables components raise Plug Power’s BOM costs and squeeze margins. Export controls and customs delays add weeks to cross-border electrolyzer deployments, complicating project timelines. Plug must diversify suppliers, use hedges and localize sourcing since trade-policy shifts can change global competitiveness overnight.

- Tariffs: 25% steel, 10% aluminum

- Delays: weeks added to deployments

- Mitigation: supplier diversification, sourcing local

Public funding competition

Grants, loan guarantees and the DOE's $7 billion hydrogen hubs program plus the IRA's clean hydrogen PTC (up to $3/kg) have drawn many competitors, making selection outcomes crucial to Plug Power's market access and regional footprint; awards determine capacity build-outs and offtake visibility. Co-funding rules and milestone-based payments improve execution discipline but raise compliance and cash-flow demands, so balancing participation across programs reduces concentration risk.

- Grants/LOAN: DOE $7B hubs

- PTC: up to $3/kg

- Impact: awards drive regional access

- Risk: co-funding/compliance burden

- Mitigation: diversify across programs

IRA H2 credit up to $3/kg and $8B DOE hubs lift IRRs; tariffs raise capex, localize supply

IRA clean hydrogen credit up to $3/kg and DOE $8B Hydrogen Hubs (first 7 in 2023) materially lift project IRRs; policy clarity and multi-year duration are critical. Permitting delays and tariffs (25% steel, 10% aluminum) raise capex and timelines. Plug Power (2023 revenue 588M USD) must localize supply and secure awards to de-risk pipelines.

| Policy | Value/Size | Impact |

|---|---|---|

| IRA H2 PTC | up to 3 USD/kg | Improves IRR |

| DOE Hubs | 8 B USD | Regional access |

| Tariffs | 25% steel/10% Al | Raises BOM cost |

What is included in the product

Explores how macro-environmental factors uniquely affect Plug Power across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific examples; designed for executives and investors to identify risks, opportunities and actionable, forward-looking strategic insights.

Condenses Plug Power's PESTLE into a clean, editable summary that highlights regulatory, market and technological risks and opportunities for quick inclusion in presentations or team briefings.

Economic factors

Capital intensity

Building green hydrogen plants, logistics and refueling networks is highly capex‑intensive; project economics are driven by 2024 US policy and markets, including the Inflation Reduction Act H2 tax credit of up to 3 USD/kg and a Federal Funds rate near 5.25–5.50% that raises financing costs. Plug’s access to tax equity, project finance and offtake‑backed debt determines WACC and viability, while scale reduces unit costs but increases execution and delivery risk.

Hydrogen price volatility

Levelized cost of hydrogen is driven mainly by electricity, capacity factor and electrolyzer efficiency: modern PEM/alkaline electrolysis typically requires ~45–55 kWh/kg H2, so at $40–60/MWh (typical wholesale ranges in 2023–24) electricity alone can add roughly $1.8–$3.3/kg. Wholesale price volatility therefore compresses margins; long-term PPAs and hedges (commonly used across the industry) stabilize economics. Plug Power’s integrated model aims to capture spreads across production, storage and offtake to mitigate this volatility.

Demand ramp and adoption

Material handling, mobility and industrial adoption for Plug Power scale unevenly across regions, with North America and Europe leading deployments while APAC lags; Plug Power reported 2024 revenue of $1.34B and points to regional concentration of orders. Fleet conversions and heavy‑duty transport contracts trigger step‑change volumes when offtakes convert, creating lumpy demand. Cyclicality in logistics and manufacturing shifts order timing quarter‑to‑quarter. Plug must balance inventory, service capacity and pipeline health to avoid margin pressure.

Supply chain constraints

Supply-chain constraints for Plug Power center on PGMs, membranes, power electronics and compressors, which can bottleneck system output and delay deployments.

Localization of manufacturing lowers freight and tariff exposure but requires sizable upfront capital and facility lead times; strategic sourcing and dual-sourcing mitigate single-point failures.

Commodity price swings in PGMs and polymers pass through to product pricing and long-term contracts, increasing margin volatility and requiring indexed pricing clauses.

- PGMs: critical single-source risk

- Localization: reduces logistics/tariff risk but ups CAPEX

- Dual-sourcing: lowers disruption probability

- Commodity swings: feed-through to pricing/contracts

Currency and global exposure

Plug Power's revenues and costs span USD, EUR and other currencies as the company expanded European deployments in 2024; full-year 2024 revenue was about $1.02 billion, exposing reported results to FX translation effects. FX movements have materially affected quarterly EPS and project ROIs, while natural hedges from Euro-denominated sales vs. Euro costs reduce but do not eliminate exposure. The company uses financial hedges and considers country risk premiums when pricing bids into Europe and Latin America.

- USD/EUR exposure: material post-2024 European growth

- Hedging: natural hedges + financial instruments used

- Country risk premiums: affect bid competitiveness and ROI

IRA H2 credit up to $3/kg and $8B DOE hubs lift IRRs; tariffs raise capex, localize supply

Capex‑heavy green H2 projects depend on IRA H2 credit up to 3 USD/kg, Fed Funds ~5.25–5.50% raising WACC, and Plug Power 2024 revenue ~1.02B USD—access to tax equity and offtake finance is decisive. LCoH driven by 45–55 kWh/kg and $40–60/MWh power (~1.8–3.3 USD/kg electricity); PPAs/hedges stabilize margins. PGMs, membranes and compressors remain supply bottlenecks.

| Metric | Value (2024) |

|---|---|

| Revenue | 1.02B USD |

| IRA H2 credit | up to 3 USD/kg |

| Electricity | 40–60 USD/MWh |

| Electrolyzer use | 45–55 kWh/kg |

Preview the Actual Deliverable

Plug Power PESTLE Analysis

The preview shown here is the exact Plug Power PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and insights visible are the final file with no placeholders. You’ll be able to download this exact document immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of Plug Power—concise, data-driven insight into political, economic, social, technological, legal and environmental forces shaping its prospects. Ideal for investors and strategists, it's ready to use and editable. Purchase the full report for the complete breakdown and actionable recommendations.

Political factors

Hydrogen subsidies

U.S. IRA 45V clean hydrogen credit—worth up to $3 per kg for ultra-low carbon H2—and EU hydrogen incentives including the EU Hydrogen Bank (estimated €3–5 billion initial support) materially improve green hydrogen project IRRs; Plug Power’s electrolyzer and fuel cell rollouts hinge on the clarity, value and multi-year duration of these supports, while policy revisions, claw-backs or disbursement delays can push investment timelines and alter site selection, making government advocacy and policy alignment core strategic priorities.

Permitting and siting

Hydrogen plants require multi-jurisdictional permits across generation, storage, safety and transportation, and DOE’s $8 billion Hydrogen Hubs program (first 7 hubs selected in 2023) shows federal-state coordination matters. Streamlined approvals can accelerate Plug Power’s build-out; fragmented or slow processes raise capex and O&M risk. Community engagement and state cooperation are decisive, so permitting risk must be priced into project pipelines.

Energy security agendas

Energy security agendas push governments to prioritize domestic clean supply chains, driven by policies like the Inflation Reduction Act's roughly 369 billion USD in climate incentives and DOE funding of seven hydrogen hubs ~7 billion USD, creating localization incentives and PPP opportunities for Plug Power. Policy-driven procurement (federal ZEV targets to 2035) can catalyze demand, but national content rules may raise costs or restrict sourcing, squeezing margins against Plug Power's ~588 million USD 2023 revenue.

Trade and tariffs

Tariffs on metals (US Section 232: 25% steel, 10% aluminum) and restrictions on renewables components raise Plug Power’s BOM costs and squeeze margins. Export controls and customs delays add weeks to cross-border electrolyzer deployments, complicating project timelines. Plug must diversify suppliers, use hedges and localize sourcing since trade-policy shifts can change global competitiveness overnight.

- Tariffs: 25% steel, 10% aluminum

- Delays: weeks added to deployments

- Mitigation: supplier diversification, sourcing local

Public funding competition

Grants, loan guarantees and the DOE's $7 billion hydrogen hubs program plus the IRA's clean hydrogen PTC (up to $3/kg) have drawn many competitors, making selection outcomes crucial to Plug Power's market access and regional footprint; awards determine capacity build-outs and offtake visibility. Co-funding rules and milestone-based payments improve execution discipline but raise compliance and cash-flow demands, so balancing participation across programs reduces concentration risk.

- Grants/LOAN: DOE $7B hubs

- PTC: up to $3/kg

- Impact: awards drive regional access

- Risk: co-funding/compliance burden

- Mitigation: diversify across programs

IRA H2 credit up to $3/kg and $8B DOE hubs lift IRRs; tariffs raise capex, localize supply

IRA clean hydrogen credit up to $3/kg and DOE $8B Hydrogen Hubs (first 7 in 2023) materially lift project IRRs; policy clarity and multi-year duration are critical. Permitting delays and tariffs (25% steel, 10% aluminum) raise capex and timelines. Plug Power (2023 revenue 588M USD) must localize supply and secure awards to de-risk pipelines.

| Policy | Value/Size | Impact |

|---|---|---|

| IRA H2 PTC | up to 3 USD/kg | Improves IRR |

| DOE Hubs | 8 B USD | Regional access |

| Tariffs | 25% steel/10% Al | Raises BOM cost |

What is included in the product

Explores how macro-environmental factors uniquely affect Plug Power across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and region-specific examples; designed for executives and investors to identify risks, opportunities and actionable, forward-looking strategic insights.

Condenses Plug Power's PESTLE into a clean, editable summary that highlights regulatory, market and technological risks and opportunities for quick inclusion in presentations or team briefings.

Economic factors

Capital intensity

Building green hydrogen plants, logistics and refueling networks is highly capex‑intensive; project economics are driven by 2024 US policy and markets, including the Inflation Reduction Act H2 tax credit of up to 3 USD/kg and a Federal Funds rate near 5.25–5.50% that raises financing costs. Plug’s access to tax equity, project finance and offtake‑backed debt determines WACC and viability, while scale reduces unit costs but increases execution and delivery risk.

Hydrogen price volatility

Levelized cost of hydrogen is driven mainly by electricity, capacity factor and electrolyzer efficiency: modern PEM/alkaline electrolysis typically requires ~45–55 kWh/kg H2, so at $40–60/MWh (typical wholesale ranges in 2023–24) electricity alone can add roughly $1.8–$3.3/kg. Wholesale price volatility therefore compresses margins; long-term PPAs and hedges (commonly used across the industry) stabilize economics. Plug Power’s integrated model aims to capture spreads across production, storage and offtake to mitigate this volatility.

Demand ramp and adoption

Material handling, mobility and industrial adoption for Plug Power scale unevenly across regions, with North America and Europe leading deployments while APAC lags; Plug Power reported 2024 revenue of $1.34B and points to regional concentration of orders. Fleet conversions and heavy‑duty transport contracts trigger step‑change volumes when offtakes convert, creating lumpy demand. Cyclicality in logistics and manufacturing shifts order timing quarter‑to‑quarter. Plug must balance inventory, service capacity and pipeline health to avoid margin pressure.

Supply chain constraints

Supply-chain constraints for Plug Power center on PGMs, membranes, power electronics and compressors, which can bottleneck system output and delay deployments.

Localization of manufacturing lowers freight and tariff exposure but requires sizable upfront capital and facility lead times; strategic sourcing and dual-sourcing mitigate single-point failures.

Commodity price swings in PGMs and polymers pass through to product pricing and long-term contracts, increasing margin volatility and requiring indexed pricing clauses.

- PGMs: critical single-source risk

- Localization: reduces logistics/tariff risk but ups CAPEX

- Dual-sourcing: lowers disruption probability

- Commodity swings: feed-through to pricing/contracts

Currency and global exposure

Plug Power's revenues and costs span USD, EUR and other currencies as the company expanded European deployments in 2024; full-year 2024 revenue was about $1.02 billion, exposing reported results to FX translation effects. FX movements have materially affected quarterly EPS and project ROIs, while natural hedges from Euro-denominated sales vs. Euro costs reduce but do not eliminate exposure. The company uses financial hedges and considers country risk premiums when pricing bids into Europe and Latin America.

- USD/EUR exposure: material post-2024 European growth

- Hedging: natural hedges + financial instruments used

- Country risk premiums: affect bid competitiveness and ROI

IRA H2 credit up to $3/kg and $8B DOE hubs lift IRRs; tariffs raise capex, localize supply

Capex‑heavy green H2 projects depend on IRA H2 credit up to 3 USD/kg, Fed Funds ~5.25–5.50% raising WACC, and Plug Power 2024 revenue ~1.02B USD—access to tax equity and offtake finance is decisive. LCoH driven by 45–55 kWh/kg and $40–60/MWh power (~1.8–3.3 USD/kg electricity); PPAs/hedges stabilize margins. PGMs, membranes and compressors remain supply bottlenecks.

| Metric | Value (2024) |

|---|---|

| Revenue | 1.02B USD |

| IRA H2 credit | up to 3 USD/kg |

| Electricity | 40–60 USD/MWh |

| Electrolyzer use | 45–55 kWh/kg |

Preview the Actual Deliverable

Plug Power PESTLE Analysis

The preview shown here is the exact Plug Power PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and insights visible are the final file with no placeholders. You’ll be able to download this exact document immediately after checkout.