Popular Business Model Canvas

Unlock a leading bank business model blueprint for investors, entrepreneurs, and analysts

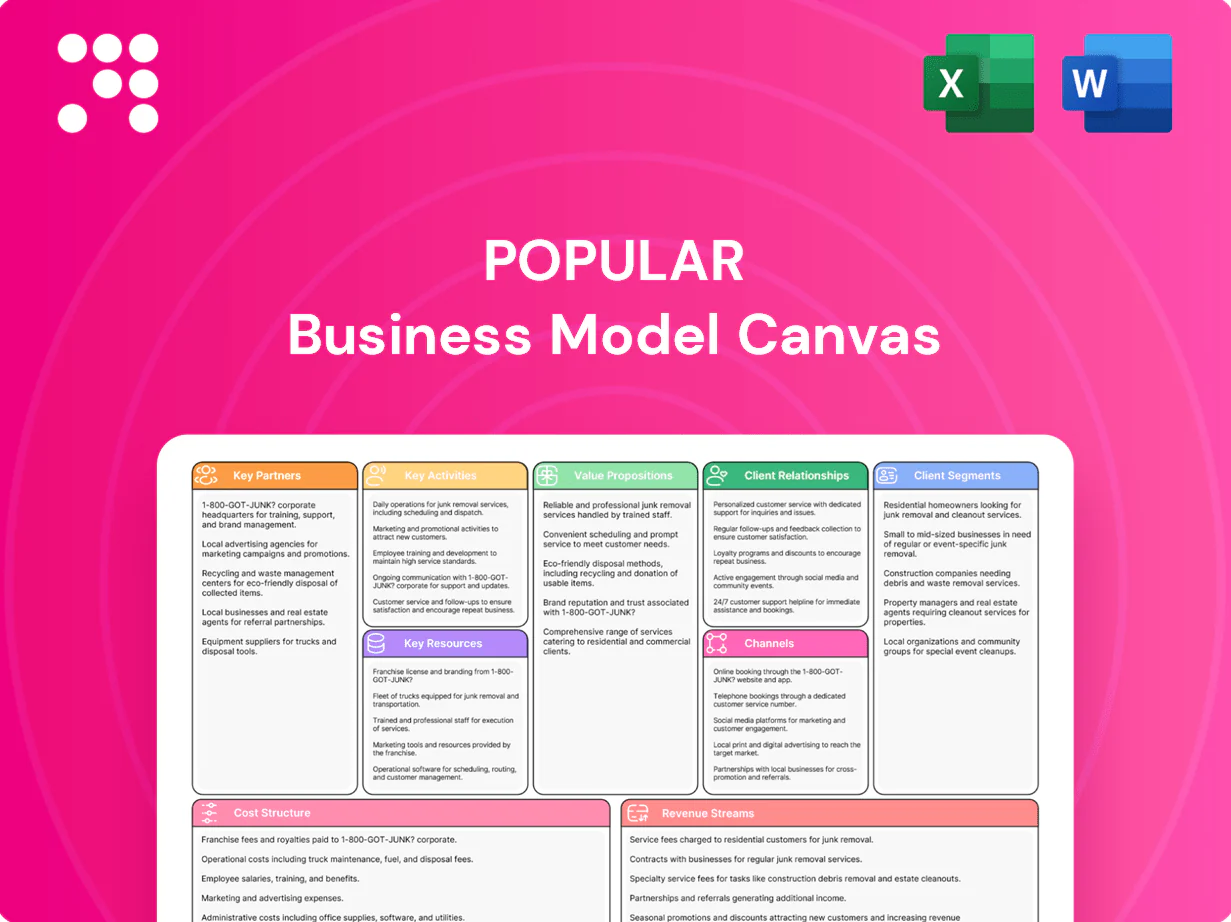

Unlock the full strategic blueprint behind Popular’s business model with our in-depth Business Model Canvas—showing how Popular creates value, scales revenue, and sustains competitive advantage. Ideal for entrepreneurs, analysts, and investors seeking actionable insights; download the complete, editable canvas in Word and Excel to benchmark, plan, and execute with confidence.

Partnerships

Payment networks and card issuers

Partnerships with Visa, Mastercard and processors enable seamless credit/debit issuance and acceptance; together their networks handled over $20 trillion in annual payments by 2023–24, providing broad interchange connectivity and real-time authorization rails. They supply advanced fraud and tokenization tools that reduce chargebacks and regulatory risk. Scale drives down per-transaction processing costs and speeds approvals, while co-brand and affinity programs—often boosting card spend and acquisition—expand reach.

Fintech and core banking providers

Alliances with core system vendors and fintechs accelerate digital features; over 26,000 fintech firms operated globally in 2024, expanding partner options. Open APIs enable seamless payments, P2P and onboarding integrations, reducing integration friction and IT risk. These partners shorten time-to-market, while joint pilots allow rapid testing of new services.

Capital markets and correspondent banks

Relationships with major broker-dealers and correspondent banks support liquidity and funding, enabling underwriting, syndication and market-making capacity; Popular leverages a correspondent network across 80+ markets to facilitate cross-border settlement and FX. These partnerships strengthen treasury and investment banking offerings, driving access to wholesale funding lines and syndication platforms that in 2024 handled billions in placement activity.

Insurance and brokerage partners

Insurance carriers and broker platforms enable bancassurance and wealth products by integrating underwriting and distribution, with bancassurance contributing an estimated 30–40% of life-policy sales in key markets in 2024.

White-label solutions broaden product shelves and speed time-to-market, while revenue-sharing models (commonly 10–40%) align incentives across partners.

Dedicated compliance teams and shared controls ensure regulatory alignment across jurisdictions, reducing breach risk and remediation costs.

- 30–40%: bancassurance share (key markets, 2024)

- 10–40%: typical revenue-share ranges

- White-label: faster product rollout

- Compliance: shared controls across jurisdictions

Government and development agencies

Partnerships with Puerto Rico, US federal entities and multilateral development banks channel SBA, FHA and disaster-recovery financing into local markets, unlocking capital for reconstruction and SME growth. Public-private initiatives broaden SME credit access through targeted lending programs and technical assistance. Government guarantees and blended finance structures lower portfolio credit risk and deepen measurable community impact.

- Channels: SBA, FHA, disaster loans

- Partners: Puerto Rico + US federal agencies + development banks

- Impact: expanded SME credit access via public-private programs

- Risk mitigation: government guarantees reduce default exposure

Payments alliances cut costs, speed issuance, boost FX liquidity and bancassurance

Strategic partnerships with Visa/Mastercard and processors (networks >$20T annual payments in 2023–24) enable seamless issuance, fraud tools and lower per-transaction costs. Alliances with 26,000+ fintechs (2024) and core vendors speed digital rollout via open APIs. Correspondent banks in 80+ markets and MDBs provide liquidity, FX and disaster financing. Bancassurance (30–40% life sales, 2024) and 10–40% revenue-share models expand product distribution.

| Partner Type | Key Metric (2024) |

|---|---|

| Card Networks | >$20T payments |

| Fintechs/Core Vendors | 26,000+ firms |

| Correspondents/MDBs | 80+ markets |

| Bancassurance | 30–40% life sales |

| Revenue-share | 10–40% |

What is included in the product

A polished, ready-to-use Business Model Canvas aligned with the company’s strategy, detailing nine BMC blocks—customer segments, value propositions, channels, revenue, costs, key partners, resources, activities, and customer relations—with SWOT-linked insights to support presentations, funding discussions, and validated decision-making.

Condenses complex business strategy into a single editable canvas, eliminating hours of formatting and scattered notes; perfect for fast decision-making, team alignment, and comparing models side-by-side.

Activities

Deposit gathering and liquidity management

Acquire and retain low-cost retail and commercial deposits to fund lending while targeting low-cost deposit share above 60% of total funding; optimize pricing and product mix to stabilize net interest margin around industry averages of roughly 2.5–3.5% in 2024. Manage liquidity buffers and interest-rate risk through diversified cash, HQLA and hedges while keeping Liquidity Coverage Ratio and Net Stable Funding Ratio above the Basel III minimums of 100%. Ensure regulatory liquidity ratios remain strong via monthly stress testing and contingency funding plans.

Lending, underwriting, and portfolio management

Originate consumer, mortgage, SME and commercial loans across channels while applying risk-based pricing and credit models targeting risk-adjusted yields (spreads commonly 200–600 bps); monitor portfolios for delinquency and provisioning with US bank nonperforming loan ratio near 0.9% in 2024; actively manage concentrations and collateral to limit sectoral exposure and loss given default.

Payments and cards operations

Issue and service credit/debit cards and merchant acquiring to drive spend, interchange, and fee income, with cards representing a core revenue stream. Operate real-time fraud detection and dispute resolution to cut chargebacks and protect margins. Enhance digital wallets and contactless capabilities as contactless adoption exceeded 60% of in-person card transactions in 2024. Focus on merchant acceptance to boost acquiring volumes.

Wealth, brokerage, and insurance distribution

Wealth, brokerage, and insurance distribution delivers advisory, brokerage execution, and bancassurance, curating shelves across funds, annuities and protection while enforcing suitability and fiduciary standards; global wealth AUM was about $110 trillion in 2024, underscoring scale and demand. Cross-selling deepens share of wallet and lifts client LTV.

- Advisory + execution

- Bancassurance distribution

- Product shelves: funds, annuities, protection

- Suitability & fiduciary compliance

- Cross-sell to grow share of wallet

Digital innovation and compliance

Build mobile, online and API-led services while maintaining cybersecurity, KYC/AML and regulatory reporting; IBM reported average breach cost of 4.45 million USD in 2024, underscoring compliance spend. Automate onboarding and servicing to cut time by up to 90% and continuously improve UX and operational resilience to reduce downtime and fraud losses.

- APIs-first: faster product rollouts

- KYC/AML: market ~10B USD (2024)

- Automation: onboarding ≤ minutes

Acquire low-cost deposits >60%, NIM 2.5–3.5%, NPL ≈0.9%

Acquire/retain low‑cost deposits (>60% funding) to support lending; target NIM ~2.5–3.5% (2024). Originate consumer/mortgage/SME loans with risk‑based pricing (spreads 200–600bps) and keep NPL ≈0.9% (2024). Drive card/acquiring revenue (contactless >60% in‑store, 2024) and scale wealth/bancassurance (AUM $110T, 2024) while enforcing cybersecurity (breach cost $4.45M, 2024).

| Metric | 2024 |

|---|---|

| Low‑cost deposit share | >60% |

| NIM | 2.5–3.5% |

| NPL | ≈0.9% |

| Card contactless | >60% |

| Wealth AUM | $110T |

| Breach cost | $4.45M |

Preview Before You Purchase

Business Model Canvas

The document previewed here is the actual Business Model Canvas you'll receive—no mockups or samples. When you purchase, you’ll get this same fully editable file, formatted and complete, ready for presentation and editing. What you see is exactly what you’ll download.

Unlock a leading bank business model blueprint for investors, entrepreneurs, and analysts

Unlock the full strategic blueprint behind Popular’s business model with our in-depth Business Model Canvas—showing how Popular creates value, scales revenue, and sustains competitive advantage. Ideal for entrepreneurs, analysts, and investors seeking actionable insights; download the complete, editable canvas in Word and Excel to benchmark, plan, and execute with confidence.

Partnerships

Payment networks and card issuers

Partnerships with Visa, Mastercard and processors enable seamless credit/debit issuance and acceptance; together their networks handled over $20 trillion in annual payments by 2023–24, providing broad interchange connectivity and real-time authorization rails. They supply advanced fraud and tokenization tools that reduce chargebacks and regulatory risk. Scale drives down per-transaction processing costs and speeds approvals, while co-brand and affinity programs—often boosting card spend and acquisition—expand reach.

Fintech and core banking providers

Alliances with core system vendors and fintechs accelerate digital features; over 26,000 fintech firms operated globally in 2024, expanding partner options. Open APIs enable seamless payments, P2P and onboarding integrations, reducing integration friction and IT risk. These partners shorten time-to-market, while joint pilots allow rapid testing of new services.

Capital markets and correspondent banks

Relationships with major broker-dealers and correspondent banks support liquidity and funding, enabling underwriting, syndication and market-making capacity; Popular leverages a correspondent network across 80+ markets to facilitate cross-border settlement and FX. These partnerships strengthen treasury and investment banking offerings, driving access to wholesale funding lines and syndication platforms that in 2024 handled billions in placement activity.

Insurance and brokerage partners

Insurance carriers and broker platforms enable bancassurance and wealth products by integrating underwriting and distribution, with bancassurance contributing an estimated 30–40% of life-policy sales in key markets in 2024.

White-label solutions broaden product shelves and speed time-to-market, while revenue-sharing models (commonly 10–40%) align incentives across partners.

Dedicated compliance teams and shared controls ensure regulatory alignment across jurisdictions, reducing breach risk and remediation costs.

- 30–40%: bancassurance share (key markets, 2024)

- 10–40%: typical revenue-share ranges

- White-label: faster product rollout

- Compliance: shared controls across jurisdictions

Government and development agencies

Partnerships with Puerto Rico, US federal entities and multilateral development banks channel SBA, FHA and disaster-recovery financing into local markets, unlocking capital for reconstruction and SME growth. Public-private initiatives broaden SME credit access through targeted lending programs and technical assistance. Government guarantees and blended finance structures lower portfolio credit risk and deepen measurable community impact.

- Channels: SBA, FHA, disaster loans

- Partners: Puerto Rico + US federal agencies + development banks

- Impact: expanded SME credit access via public-private programs

- Risk mitigation: government guarantees reduce default exposure

Payments alliances cut costs, speed issuance, boost FX liquidity and bancassurance

Strategic partnerships with Visa/Mastercard and processors (networks >$20T annual payments in 2023–24) enable seamless issuance, fraud tools and lower per-transaction costs. Alliances with 26,000+ fintechs (2024) and core vendors speed digital rollout via open APIs. Correspondent banks in 80+ markets and MDBs provide liquidity, FX and disaster financing. Bancassurance (30–40% life sales, 2024) and 10–40% revenue-share models expand product distribution.

| Partner Type | Key Metric (2024) |

|---|---|

| Card Networks | >$20T payments |

| Fintechs/Core Vendors | 26,000+ firms |

| Correspondents/MDBs | 80+ markets |

| Bancassurance | 30–40% life sales |

| Revenue-share | 10–40% |

What is included in the product

A polished, ready-to-use Business Model Canvas aligned with the company’s strategy, detailing nine BMC blocks—customer segments, value propositions, channels, revenue, costs, key partners, resources, activities, and customer relations—with SWOT-linked insights to support presentations, funding discussions, and validated decision-making.

Condenses complex business strategy into a single editable canvas, eliminating hours of formatting and scattered notes; perfect for fast decision-making, team alignment, and comparing models side-by-side.

Activities

Deposit gathering and liquidity management

Acquire and retain low-cost retail and commercial deposits to fund lending while targeting low-cost deposit share above 60% of total funding; optimize pricing and product mix to stabilize net interest margin around industry averages of roughly 2.5–3.5% in 2024. Manage liquidity buffers and interest-rate risk through diversified cash, HQLA and hedges while keeping Liquidity Coverage Ratio and Net Stable Funding Ratio above the Basel III minimums of 100%. Ensure regulatory liquidity ratios remain strong via monthly stress testing and contingency funding plans.

Lending, underwriting, and portfolio management

Originate consumer, mortgage, SME and commercial loans across channels while applying risk-based pricing and credit models targeting risk-adjusted yields (spreads commonly 200–600 bps); monitor portfolios for delinquency and provisioning with US bank nonperforming loan ratio near 0.9% in 2024; actively manage concentrations and collateral to limit sectoral exposure and loss given default.

Payments and cards operations

Issue and service credit/debit cards and merchant acquiring to drive spend, interchange, and fee income, with cards representing a core revenue stream. Operate real-time fraud detection and dispute resolution to cut chargebacks and protect margins. Enhance digital wallets and contactless capabilities as contactless adoption exceeded 60% of in-person card transactions in 2024. Focus on merchant acceptance to boost acquiring volumes.

Wealth, brokerage, and insurance distribution

Wealth, brokerage, and insurance distribution delivers advisory, brokerage execution, and bancassurance, curating shelves across funds, annuities and protection while enforcing suitability and fiduciary standards; global wealth AUM was about $110 trillion in 2024, underscoring scale and demand. Cross-selling deepens share of wallet and lifts client LTV.

- Advisory + execution

- Bancassurance distribution

- Product shelves: funds, annuities, protection

- Suitability & fiduciary compliance

- Cross-sell to grow share of wallet

Digital innovation and compliance

Build mobile, online and API-led services while maintaining cybersecurity, KYC/AML and regulatory reporting; IBM reported average breach cost of 4.45 million USD in 2024, underscoring compliance spend. Automate onboarding and servicing to cut time by up to 90% and continuously improve UX and operational resilience to reduce downtime and fraud losses.

- APIs-first: faster product rollouts

- KYC/AML: market ~10B USD (2024)

- Automation: onboarding ≤ minutes

Acquire low-cost deposits >60%, NIM 2.5–3.5%, NPL ≈0.9%

Acquire/retain low‑cost deposits (>60% funding) to support lending; target NIM ~2.5–3.5% (2024). Originate consumer/mortgage/SME loans with risk‑based pricing (spreads 200–600bps) and keep NPL ≈0.9% (2024). Drive card/acquiring revenue (contactless >60% in‑store, 2024) and scale wealth/bancassurance (AUM $110T, 2024) while enforcing cybersecurity (breach cost $4.45M, 2024).

| Metric | 2024 |

|---|---|

| Low‑cost deposit share | >60% |

| NIM | 2.5–3.5% |

| NPL | ≈0.9% |

| Card contactless | >60% |

| Wealth AUM | $110T |

| Breach cost | $4.45M |

Preview Before You Purchase

Business Model Canvas

The document previewed here is the actual Business Model Canvas you'll receive—no mockups or samples. When you purchase, you’ll get this same fully editable file, formatted and complete, ready for presentation and editing. What you see is exactly what you’ll download.

Description

Unlock a leading bank business model blueprint for investors, entrepreneurs, and analysts

Unlock the full strategic blueprint behind Popular’s business model with our in-depth Business Model Canvas—showing how Popular creates value, scales revenue, and sustains competitive advantage. Ideal for entrepreneurs, analysts, and investors seeking actionable insights; download the complete, editable canvas in Word and Excel to benchmark, plan, and execute with confidence.

Partnerships

Payment networks and card issuers

Partnerships with Visa, Mastercard and processors enable seamless credit/debit issuance and acceptance; together their networks handled over $20 trillion in annual payments by 2023–24, providing broad interchange connectivity and real-time authorization rails. They supply advanced fraud and tokenization tools that reduce chargebacks and regulatory risk. Scale drives down per-transaction processing costs and speeds approvals, while co-brand and affinity programs—often boosting card spend and acquisition—expand reach.

Fintech and core banking providers

Alliances with core system vendors and fintechs accelerate digital features; over 26,000 fintech firms operated globally in 2024, expanding partner options. Open APIs enable seamless payments, P2P and onboarding integrations, reducing integration friction and IT risk. These partners shorten time-to-market, while joint pilots allow rapid testing of new services.

Capital markets and correspondent banks

Relationships with major broker-dealers and correspondent banks support liquidity and funding, enabling underwriting, syndication and market-making capacity; Popular leverages a correspondent network across 80+ markets to facilitate cross-border settlement and FX. These partnerships strengthen treasury and investment banking offerings, driving access to wholesale funding lines and syndication platforms that in 2024 handled billions in placement activity.

Insurance and brokerage partners

Insurance carriers and broker platforms enable bancassurance and wealth products by integrating underwriting and distribution, with bancassurance contributing an estimated 30–40% of life-policy sales in key markets in 2024.

White-label solutions broaden product shelves and speed time-to-market, while revenue-sharing models (commonly 10–40%) align incentives across partners.

Dedicated compliance teams and shared controls ensure regulatory alignment across jurisdictions, reducing breach risk and remediation costs.

- 30–40%: bancassurance share (key markets, 2024)

- 10–40%: typical revenue-share ranges

- White-label: faster product rollout

- Compliance: shared controls across jurisdictions

Government and development agencies

Partnerships with Puerto Rico, US federal entities and multilateral development banks channel SBA, FHA and disaster-recovery financing into local markets, unlocking capital for reconstruction and SME growth. Public-private initiatives broaden SME credit access through targeted lending programs and technical assistance. Government guarantees and blended finance structures lower portfolio credit risk and deepen measurable community impact.

- Channels: SBA, FHA, disaster loans

- Partners: Puerto Rico + US federal agencies + development banks

- Impact: expanded SME credit access via public-private programs

- Risk mitigation: government guarantees reduce default exposure

Payments alliances cut costs, speed issuance, boost FX liquidity and bancassurance

Strategic partnerships with Visa/Mastercard and processors (networks >$20T annual payments in 2023–24) enable seamless issuance, fraud tools and lower per-transaction costs. Alliances with 26,000+ fintechs (2024) and core vendors speed digital rollout via open APIs. Correspondent banks in 80+ markets and MDBs provide liquidity, FX and disaster financing. Bancassurance (30–40% life sales, 2024) and 10–40% revenue-share models expand product distribution.

| Partner Type | Key Metric (2024) |

|---|---|

| Card Networks | >$20T payments |

| Fintechs/Core Vendors | 26,000+ firms |

| Correspondents/MDBs | 80+ markets |

| Bancassurance | 30–40% life sales |

| Revenue-share | 10–40% |

What is included in the product

A polished, ready-to-use Business Model Canvas aligned with the company’s strategy, detailing nine BMC blocks—customer segments, value propositions, channels, revenue, costs, key partners, resources, activities, and customer relations—with SWOT-linked insights to support presentations, funding discussions, and validated decision-making.

Condenses complex business strategy into a single editable canvas, eliminating hours of formatting and scattered notes; perfect for fast decision-making, team alignment, and comparing models side-by-side.

Activities

Deposit gathering and liquidity management

Acquire and retain low-cost retail and commercial deposits to fund lending while targeting low-cost deposit share above 60% of total funding; optimize pricing and product mix to stabilize net interest margin around industry averages of roughly 2.5–3.5% in 2024. Manage liquidity buffers and interest-rate risk through diversified cash, HQLA and hedges while keeping Liquidity Coverage Ratio and Net Stable Funding Ratio above the Basel III minimums of 100%. Ensure regulatory liquidity ratios remain strong via monthly stress testing and contingency funding plans.

Lending, underwriting, and portfolio management

Originate consumer, mortgage, SME and commercial loans across channels while applying risk-based pricing and credit models targeting risk-adjusted yields (spreads commonly 200–600 bps); monitor portfolios for delinquency and provisioning with US bank nonperforming loan ratio near 0.9% in 2024; actively manage concentrations and collateral to limit sectoral exposure and loss given default.

Payments and cards operations

Issue and service credit/debit cards and merchant acquiring to drive spend, interchange, and fee income, with cards representing a core revenue stream. Operate real-time fraud detection and dispute resolution to cut chargebacks and protect margins. Enhance digital wallets and contactless capabilities as contactless adoption exceeded 60% of in-person card transactions in 2024. Focus on merchant acceptance to boost acquiring volumes.

Wealth, brokerage, and insurance distribution

Wealth, brokerage, and insurance distribution delivers advisory, brokerage execution, and bancassurance, curating shelves across funds, annuities and protection while enforcing suitability and fiduciary standards; global wealth AUM was about $110 trillion in 2024, underscoring scale and demand. Cross-selling deepens share of wallet and lifts client LTV.

- Advisory + execution

- Bancassurance distribution

- Product shelves: funds, annuities, protection

- Suitability & fiduciary compliance

- Cross-sell to grow share of wallet

Digital innovation and compliance

Build mobile, online and API-led services while maintaining cybersecurity, KYC/AML and regulatory reporting; IBM reported average breach cost of 4.45 million USD in 2024, underscoring compliance spend. Automate onboarding and servicing to cut time by up to 90% and continuously improve UX and operational resilience to reduce downtime and fraud losses.

- APIs-first: faster product rollouts

- KYC/AML: market ~10B USD (2024)

- Automation: onboarding ≤ minutes

Acquire low-cost deposits >60%, NIM 2.5–3.5%, NPL ≈0.9%

Acquire/retain low‑cost deposits (>60% funding) to support lending; target NIM ~2.5–3.5% (2024). Originate consumer/mortgage/SME loans with risk‑based pricing (spreads 200–600bps) and keep NPL ≈0.9% (2024). Drive card/acquiring revenue (contactless >60% in‑store, 2024) and scale wealth/bancassurance (AUM $110T, 2024) while enforcing cybersecurity (breach cost $4.45M, 2024).

| Metric | 2024 |

|---|---|

| Low‑cost deposit share | >60% |

| NIM | 2.5–3.5% |

| NPL | ≈0.9% |

| Card contactless | >60% |

| Wealth AUM | $110T |

| Breach cost | $4.45M |

Preview Before You Purchase

Business Model Canvas

The document previewed here is the actual Business Model Canvas you'll receive—no mockups or samples. When you purchase, you’ll get this same fully editable file, formatted and complete, ready for presentation and editing. What you see is exactly what you’ll download.