Popular Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Popular's competitive landscape is driven by supplier leverage, buyer bargaining, new-entrant threats, substitute risks, and industry rivalry—each shaping margins and growth prospects. This snapshot flags the main tensions but skips granular ratings and scenario analysis. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy recommendations tailored to Popular.

Suppliers Bargaining Power

Concentrated core tech vendors

Popular relies on a small set of core banking and payments vendors, giving suppliers leverage over pricing and contract terms. Switching core systems is costly and risky—industry implementations typically take 18–36 months and cost tens to hundreds of millions—heightening lock-in. Scale and multi‑year deals can secure better pricing, while strategic vendor management and modular architectures reduce dependence.

Wholesale funding counterparties

Wholesale funding counterparties — brokered deposits, FHLB advances and interbank lines — can tighten sharply in stress or rate spikes, forcing higher funding costs and margin compression. These suppliers gain bargaining power during liquidity shocks when access or pricing is restricted. Popular’s relatively strong core deposit franchise moderates reliance on such sources, but robust contingency funding plans remain critical. Diversifying counterparties and instruments reduces concentration and execution risk.

Payment networks and card processors

Visa and Mastercard dominate ~80% of global card volumes in 2024, allowing them and major processors (Fiserv, FIS, Global Payments) to set interchange and network rules with few alternatives; merchants typically pay ~1.5–2.0% per transaction. Popular’s scale gives limited bargaining leverage, while co-brand and interchange splits shape economics. Multi-network routing and tokenization/EMV upgrades can trim costs by up to ~10–20 bps.

Talent and specialized services

Skilled bankers and risk, compliance, and tech talent remain scarce in regulated markets like Puerto Rico and the US, with US unemployment ~3.7% in 2024 (BLS) tightening supply; wage inflation and poaching raise supplier power and drive salary premiums. Outsourcing specialized functions reduces hiring pressure but adds vendor and concentration risk; strong employer brand and training lower churn and bargaining leverage.

- Scarcity: high

- Wage inflation: increases power

- Outsourcing: shifts vendor risk

- Mitigation: branding & training

Regulatory and compliance infrastructure

Regulators are not suppliers, but licenses, deposit insurance (FDIC cap $250,000), and access to payment rails function as essential, non-negotiable inputs that set hard terms; changes in compliance have pushed banks' operating timelines and costs higher, with major banks reporting average CET1 ratios near 14% in 2024 reflecting capital and compliance buffers. Maintaining strong risk management preserves access and reduces implicit supplier pressure, while regulatory clarity improves planning.

- Licenses as inputs

- FDIC cap $250,000

- CET1 ~14% (2024)

Supplier power, card networks ~80%: diversify vendors and funding

Suppliers wield high power: core banking vendors (implementations 18–36 months, $10s–$100sM) create lock‑in; card networks control ~80% of volumes with merchant fees ~1.5–2.0%; wholesale funding tightens in stress; skilled talent scarce (US unemployment ~3.7% in 2024). Diversification, vendor management and contingency funding reduce risk.

| Item | 2024 |

|---|---|

| Card share | ~80% |

| Interchange | 1.5–2.0% |

| Unemployment | 3.7% |

| CET1 | ~14% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Popular, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats with strategic insights and an editable Word format for easy customization.

A compact Porter's Five Forces template that translates complex competitive dynamics into clear, actionable insights, speeding decision-making and helping teams prioritize strategic responses to reduce market risk and analysis time.

Customers Bargaining Power

Rate-sensitive depositors

With the fed funds rate near 5.25–5.50% in 2024, rate-sensitive depositors pushed for higher yields, lifting Popular’s funding costs; digital account portability and widespread mobile banking adoption (over 80% of US adults in 2024) eased switching and strengthened buyer power. Popular can mitigate outflows by segmenting pricing, offering tiered yields and value-added services, and bundling relationships to reduce churn.

Corporate and government clients

Larger corporate and government clients in Puerto Rico and the U.S. exert strong fee and collateral negotiation power due to big-ticket sizes and alternative lenders, with Puerto Rico deposit concentration led by the top five banks at roughly 65% (2023 OCIF/FDIC trends) reinforcing their leverage into 2024. Tailored lending, treasury and cash-management solutions help defend margins. Cross-selling multiple products increases client stickiness and raises switching costs.

SME borrowers with multiple options

SMEs can shop across banks, credit unions and fintech lenders, with transparent pricing and faster decisions driving switching; World Bank 2024 notes SMEs comprise about 90% of firms and over 50% of employment globally. Popular’s local market knowledge and faster underwriting help offset pure price competition, while advisory-led cross-sell (cash management, FX, payroll) deepens ties and boosts retention.

Retail customers’ switching costs

Digital onboarding and account-transfer tools have reduced switching friction—by 2024 about 76% of retail bank customers used mobile apps for routine banking—yet trust, branch access and integrated mortgage/wealth services still anchor many users. Superior mobile UX and strict SLAs raise retention; loyalty programs and fee waivers add measurable exit friction.

- Digital adoption: 76% mobile use (2024)

- Trust/branches: still key

- UX/SLA retain users

- Loyalty/fee waivers add friction

Investment and insurance clients

- Fees: 0.5%+ pressure

- Transparency: robo-AUM 1T USD (2024)

- Differentiation: holistic planning, local insights

- Defense: bundled pricing, cross-sell

Depositors demand yields: Fed funds 5.25-5.50%, mobile 76%

Customer bargaining power is elevated in 2024 with fed funds ~5.25–5.50% and digital switching; depositors seek higher yields. Large corporates wield strong fee/Collateral leverage amid top-five banks holding ~65% PR deposits (2023). Mobile adoption ~76% and robo-AUM ~1T USD raise price transparency; Popular mitigates via tiered pricing, UX and cross-sell.

| Metric | 2024/2023 |

|---|---|

| Fed funds | 5.25–5.50% |

| Mobile use | 76% |

| Robo AUM | 1T USD |

| PR top-5 deposit share | ~65% (2023) |

Preview Before You Purchase

Popular Porter's Five Forces Analysis

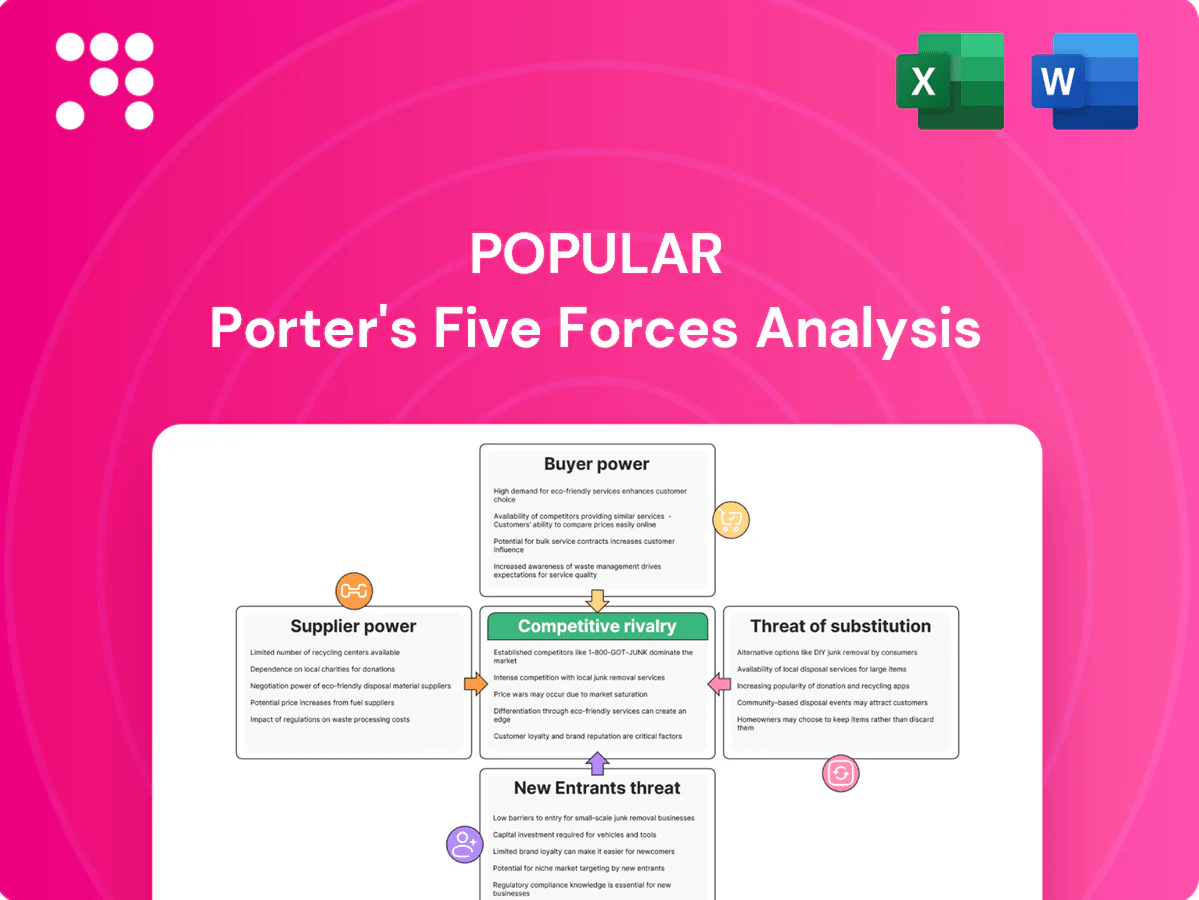

Porter's Five Forces analysis evaluates industry rivalry, threat of new entrants, bargaining power of buyers and suppliers, and substitute threats to illuminate competitive dynamics and strategic levers. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is professionally formatted and ready for download and immediate use in strategy or valuation work.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Popular's competitive landscape is driven by supplier leverage, buyer bargaining, new-entrant threats, substitute risks, and industry rivalry—each shaping margins and growth prospects. This snapshot flags the main tensions but skips granular ratings and scenario analysis. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy recommendations tailored to Popular.

Suppliers Bargaining Power

Concentrated core tech vendors

Popular relies on a small set of core banking and payments vendors, giving suppliers leverage over pricing and contract terms. Switching core systems is costly and risky—industry implementations typically take 18–36 months and cost tens to hundreds of millions—heightening lock-in. Scale and multi‑year deals can secure better pricing, while strategic vendor management and modular architectures reduce dependence.

Wholesale funding counterparties

Wholesale funding counterparties — brokered deposits, FHLB advances and interbank lines — can tighten sharply in stress or rate spikes, forcing higher funding costs and margin compression. These suppliers gain bargaining power during liquidity shocks when access or pricing is restricted. Popular’s relatively strong core deposit franchise moderates reliance on such sources, but robust contingency funding plans remain critical. Diversifying counterparties and instruments reduces concentration and execution risk.

Payment networks and card processors

Visa and Mastercard dominate ~80% of global card volumes in 2024, allowing them and major processors (Fiserv, FIS, Global Payments) to set interchange and network rules with few alternatives; merchants typically pay ~1.5–2.0% per transaction. Popular’s scale gives limited bargaining leverage, while co-brand and interchange splits shape economics. Multi-network routing and tokenization/EMV upgrades can trim costs by up to ~10–20 bps.

Talent and specialized services

Skilled bankers and risk, compliance, and tech talent remain scarce in regulated markets like Puerto Rico and the US, with US unemployment ~3.7% in 2024 (BLS) tightening supply; wage inflation and poaching raise supplier power and drive salary premiums. Outsourcing specialized functions reduces hiring pressure but adds vendor and concentration risk; strong employer brand and training lower churn and bargaining leverage.

- Scarcity: high

- Wage inflation: increases power

- Outsourcing: shifts vendor risk

- Mitigation: branding & training

Regulatory and compliance infrastructure

Regulators are not suppliers, but licenses, deposit insurance (FDIC cap $250,000), and access to payment rails function as essential, non-negotiable inputs that set hard terms; changes in compliance have pushed banks' operating timelines and costs higher, with major banks reporting average CET1 ratios near 14% in 2024 reflecting capital and compliance buffers. Maintaining strong risk management preserves access and reduces implicit supplier pressure, while regulatory clarity improves planning.

- Licenses as inputs

- FDIC cap $250,000

- CET1 ~14% (2024)

Supplier power, card networks ~80%: diversify vendors and funding

Suppliers wield high power: core banking vendors (implementations 18–36 months, $10s–$100sM) create lock‑in; card networks control ~80% of volumes with merchant fees ~1.5–2.0%; wholesale funding tightens in stress; skilled talent scarce (US unemployment ~3.7% in 2024). Diversification, vendor management and contingency funding reduce risk.

| Item | 2024 |

|---|---|

| Card share | ~80% |

| Interchange | 1.5–2.0% |

| Unemployment | 3.7% |

| CET1 | ~14% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Popular, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats with strategic insights and an editable Word format for easy customization.

A compact Porter's Five Forces template that translates complex competitive dynamics into clear, actionable insights, speeding decision-making and helping teams prioritize strategic responses to reduce market risk and analysis time.

Customers Bargaining Power

Rate-sensitive depositors

With the fed funds rate near 5.25–5.50% in 2024, rate-sensitive depositors pushed for higher yields, lifting Popular’s funding costs; digital account portability and widespread mobile banking adoption (over 80% of US adults in 2024) eased switching and strengthened buyer power. Popular can mitigate outflows by segmenting pricing, offering tiered yields and value-added services, and bundling relationships to reduce churn.

Corporate and government clients

Larger corporate and government clients in Puerto Rico and the U.S. exert strong fee and collateral negotiation power due to big-ticket sizes and alternative lenders, with Puerto Rico deposit concentration led by the top five banks at roughly 65% (2023 OCIF/FDIC trends) reinforcing their leverage into 2024. Tailored lending, treasury and cash-management solutions help defend margins. Cross-selling multiple products increases client stickiness and raises switching costs.

SME borrowers with multiple options

SMEs can shop across banks, credit unions and fintech lenders, with transparent pricing and faster decisions driving switching; World Bank 2024 notes SMEs comprise about 90% of firms and over 50% of employment globally. Popular’s local market knowledge and faster underwriting help offset pure price competition, while advisory-led cross-sell (cash management, FX, payroll) deepens ties and boosts retention.

Retail customers’ switching costs

Digital onboarding and account-transfer tools have reduced switching friction—by 2024 about 76% of retail bank customers used mobile apps for routine banking—yet trust, branch access and integrated mortgage/wealth services still anchor many users. Superior mobile UX and strict SLAs raise retention; loyalty programs and fee waivers add measurable exit friction.

- Digital adoption: 76% mobile use (2024)

- Trust/branches: still key

- UX/SLA retain users

- Loyalty/fee waivers add friction

Investment and insurance clients

- Fees: 0.5%+ pressure

- Transparency: robo-AUM 1T USD (2024)

- Differentiation: holistic planning, local insights

- Defense: bundled pricing, cross-sell

Depositors demand yields: Fed funds 5.25-5.50%, mobile 76%

Customer bargaining power is elevated in 2024 with fed funds ~5.25–5.50% and digital switching; depositors seek higher yields. Large corporates wield strong fee/Collateral leverage amid top-five banks holding ~65% PR deposits (2023). Mobile adoption ~76% and robo-AUM ~1T USD raise price transparency; Popular mitigates via tiered pricing, UX and cross-sell.

| Metric | 2024/2023 |

|---|---|

| Fed funds | 5.25–5.50% |

| Mobile use | 76% |

| Robo AUM | 1T USD |

| PR top-5 deposit share | ~65% (2023) |

Preview Before You Purchase

Popular Porter's Five Forces Analysis

Porter's Five Forces analysis evaluates industry rivalry, threat of new entrants, bargaining power of buyers and suppliers, and substitute threats to illuminate competitive dynamics and strategic levers. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is professionally formatted and ready for download and immediate use in strategy or valuation work.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Popular's competitive landscape is driven by supplier leverage, buyer bargaining, new-entrant threats, substitute risks, and industry rivalry—each shaping margins and growth prospects. This snapshot flags the main tensions but skips granular ratings and scenario analysis. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy recommendations tailored to Popular.

Suppliers Bargaining Power

Concentrated core tech vendors

Popular relies on a small set of core banking and payments vendors, giving suppliers leverage over pricing and contract terms. Switching core systems is costly and risky—industry implementations typically take 18–36 months and cost tens to hundreds of millions—heightening lock-in. Scale and multi‑year deals can secure better pricing, while strategic vendor management and modular architectures reduce dependence.

Wholesale funding counterparties

Wholesale funding counterparties — brokered deposits, FHLB advances and interbank lines — can tighten sharply in stress or rate spikes, forcing higher funding costs and margin compression. These suppliers gain bargaining power during liquidity shocks when access or pricing is restricted. Popular’s relatively strong core deposit franchise moderates reliance on such sources, but robust contingency funding plans remain critical. Diversifying counterparties and instruments reduces concentration and execution risk.

Payment networks and card processors

Visa and Mastercard dominate ~80% of global card volumes in 2024, allowing them and major processors (Fiserv, FIS, Global Payments) to set interchange and network rules with few alternatives; merchants typically pay ~1.5–2.0% per transaction. Popular’s scale gives limited bargaining leverage, while co-brand and interchange splits shape economics. Multi-network routing and tokenization/EMV upgrades can trim costs by up to ~10–20 bps.

Talent and specialized services

Skilled bankers and risk, compliance, and tech talent remain scarce in regulated markets like Puerto Rico and the US, with US unemployment ~3.7% in 2024 (BLS) tightening supply; wage inflation and poaching raise supplier power and drive salary premiums. Outsourcing specialized functions reduces hiring pressure but adds vendor and concentration risk; strong employer brand and training lower churn and bargaining leverage.

- Scarcity: high

- Wage inflation: increases power

- Outsourcing: shifts vendor risk

- Mitigation: branding & training

Regulatory and compliance infrastructure

Regulators are not suppliers, but licenses, deposit insurance (FDIC cap $250,000), and access to payment rails function as essential, non-negotiable inputs that set hard terms; changes in compliance have pushed banks' operating timelines and costs higher, with major banks reporting average CET1 ratios near 14% in 2024 reflecting capital and compliance buffers. Maintaining strong risk management preserves access and reduces implicit supplier pressure, while regulatory clarity improves planning.

- Licenses as inputs

- FDIC cap $250,000

- CET1 ~14% (2024)

Supplier power, card networks ~80%: diversify vendors and funding

Suppliers wield high power: core banking vendors (implementations 18–36 months, $10s–$100sM) create lock‑in; card networks control ~80% of volumes with merchant fees ~1.5–2.0%; wholesale funding tightens in stress; skilled talent scarce (US unemployment ~3.7% in 2024). Diversification, vendor management and contingency funding reduce risk.

| Item | 2024 |

|---|---|

| Card share | ~80% |

| Interchange | 1.5–2.0% |

| Unemployment | 3.7% |

| CET1 | ~14% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for Popular, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats with strategic insights and an editable Word format for easy customization.

A compact Porter's Five Forces template that translates complex competitive dynamics into clear, actionable insights, speeding decision-making and helping teams prioritize strategic responses to reduce market risk and analysis time.

Customers Bargaining Power

Rate-sensitive depositors

With the fed funds rate near 5.25–5.50% in 2024, rate-sensitive depositors pushed for higher yields, lifting Popular’s funding costs; digital account portability and widespread mobile banking adoption (over 80% of US adults in 2024) eased switching and strengthened buyer power. Popular can mitigate outflows by segmenting pricing, offering tiered yields and value-added services, and bundling relationships to reduce churn.

Corporate and government clients

Larger corporate and government clients in Puerto Rico and the U.S. exert strong fee and collateral negotiation power due to big-ticket sizes and alternative lenders, with Puerto Rico deposit concentration led by the top five banks at roughly 65% (2023 OCIF/FDIC trends) reinforcing their leverage into 2024. Tailored lending, treasury and cash-management solutions help defend margins. Cross-selling multiple products increases client stickiness and raises switching costs.

SME borrowers with multiple options

SMEs can shop across banks, credit unions and fintech lenders, with transparent pricing and faster decisions driving switching; World Bank 2024 notes SMEs comprise about 90% of firms and over 50% of employment globally. Popular’s local market knowledge and faster underwriting help offset pure price competition, while advisory-led cross-sell (cash management, FX, payroll) deepens ties and boosts retention.

Retail customers’ switching costs

Digital onboarding and account-transfer tools have reduced switching friction—by 2024 about 76% of retail bank customers used mobile apps for routine banking—yet trust, branch access and integrated mortgage/wealth services still anchor many users. Superior mobile UX and strict SLAs raise retention; loyalty programs and fee waivers add measurable exit friction.

- Digital adoption: 76% mobile use (2024)

- Trust/branches: still key

- UX/SLA retain users

- Loyalty/fee waivers add friction

Investment and insurance clients

- Fees: 0.5%+ pressure

- Transparency: robo-AUM 1T USD (2024)

- Differentiation: holistic planning, local insights

- Defense: bundled pricing, cross-sell

Depositors demand yields: Fed funds 5.25-5.50%, mobile 76%

Customer bargaining power is elevated in 2024 with fed funds ~5.25–5.50% and digital switching; depositors seek higher yields. Large corporates wield strong fee/Collateral leverage amid top-five banks holding ~65% PR deposits (2023). Mobile adoption ~76% and robo-AUM ~1T USD raise price transparency; Popular mitigates via tiered pricing, UX and cross-sell.

| Metric | 2024/2023 |

|---|---|

| Fed funds | 5.25–5.50% |

| Mobile use | 76% |

| Robo AUM | 1T USD |

| PR top-5 deposit share | ~65% (2023) |

Preview Before You Purchase

Popular Porter's Five Forces Analysis

Porter's Five Forces analysis evaluates industry rivalry, threat of new entrants, bargaining power of buyers and suppliers, and substitute threats to illuminate competitive dynamics and strategic levers. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is professionally formatted and ready for download and immediate use in strategy or valuation work.