Popular PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of Popular—concise, evidence-based insights into political, economic, social, technological, legal, and environmental forces shaping the company. Ideal for investors, consultants, and planners, it highlights risks and opportunities you can act on. Purchase the full report for the complete, downloadable analysis and immediately applicable recommendations.

Political factors

Puerto Rico fiscal oversight

PROMESA, enacted in 2016, created the Fiscal Oversight and Management Board which controls public spending, pensions and government contracting cycles; Puerto Rico carried roughly $70 billion of public debt pre-restructuring. Popular, the island's largest bank, ties performance to local fiscal reforms and economic health—Puerto Rico GDP was about $104 billion in 2023. Budget austerity or restructurings can cut loan demand and government deposits; policy stability improves credit conditions and investor confidence.

U.S. federal policy dependency

As a U.S.-regulated bank, Popular is highly sensitive to Federal Reserve policy (federal funds 5.25–5.50% in 2024–25) and FDIC rules (deposit insurance cap $250,000), which affect funding costs and deposit flows. Federal stimulus, disaster aid and Medicaid funding for Puerto Rico (population ~3.2M) materially sway island liquidity and loan performance. Shifts in federal priorities can quickly alter credit quality and fee income, and cross-territory operations must align with U.S. national policy changes.

Disaster relief and resilience funding

Hurricane recovery and the Bipartisan Infrastructure Law (approximately 1.2 trillion USD) boost construction and mortgage activity, spurring rebuild and resiliency projects. Popular can capture loan demand from public-private rebuild programs and housing recovery funds totaling tens of billions. Aid delays or cuts can slow growth and raise NPLs; active advocacy and program participation are strategic levers.

Territorial status and political uncertainty

Debate over Puerto Rico’s status (2020 plebiscite: 52.34% for statehood) creates regulatory and tax uncertainty; shifts could alter federal benefit access, Medicaid funding (territories receive capped grants vs state FMAP), labor rules and investor treatment. With ~3.2M residents and pre-PROMESA debt near $70B, Popular must scenario-plan for compliance and capital structure changes; policy clarity would lower risk premia.

- 2020 plebiscite: 52.34% pro-statehood

- Population ≈3.2M (2023 est)

- Pre-PROMESA debt ≈$70B — potential capital flow impacts

Government banking relationships

Government banking relationships with Puerto Rico, the USVI and municipal entities drive deposit stability and fee pipelines for Popular, affecting liquidity and service revenues.

Procurement rules, transparency standards and political turnover can reallocate mandates; strong governance and competitive pricing are critical to retain public-sector business and limit churn.

- Deposit stability tied to public-sector mandates

- Procurement/transparency can shift accounts

- Governance and pricing secure renewals

- Scandal risk requires strict ethics controls

Oversight board, $70B debt and capped federal aid squeeze PR credit

PROMESA (2016) and the Fiscal Oversight Board still govern spending and pensions after ~ $70B pre-restructuring debt; Puerto Rico GDP ≈ $104B (2023) and population ≈3.2M. Federal policy (fed funds 5.25–5.50% in 2024–25) and capped Medicaid/federal aid drive liquidity and credit; 2020 plebiscite: 52.34% pro-statehood increases regulatory uncertainty.

| Metric | Value |

|---|---|

| Pre-PROMESA debt | $70B |

| GDP (2023) | $104B |

| Population (2023) | 3.2M |

| Fed funds (2024–25) | 5.25–5.50% |

What is included in the product

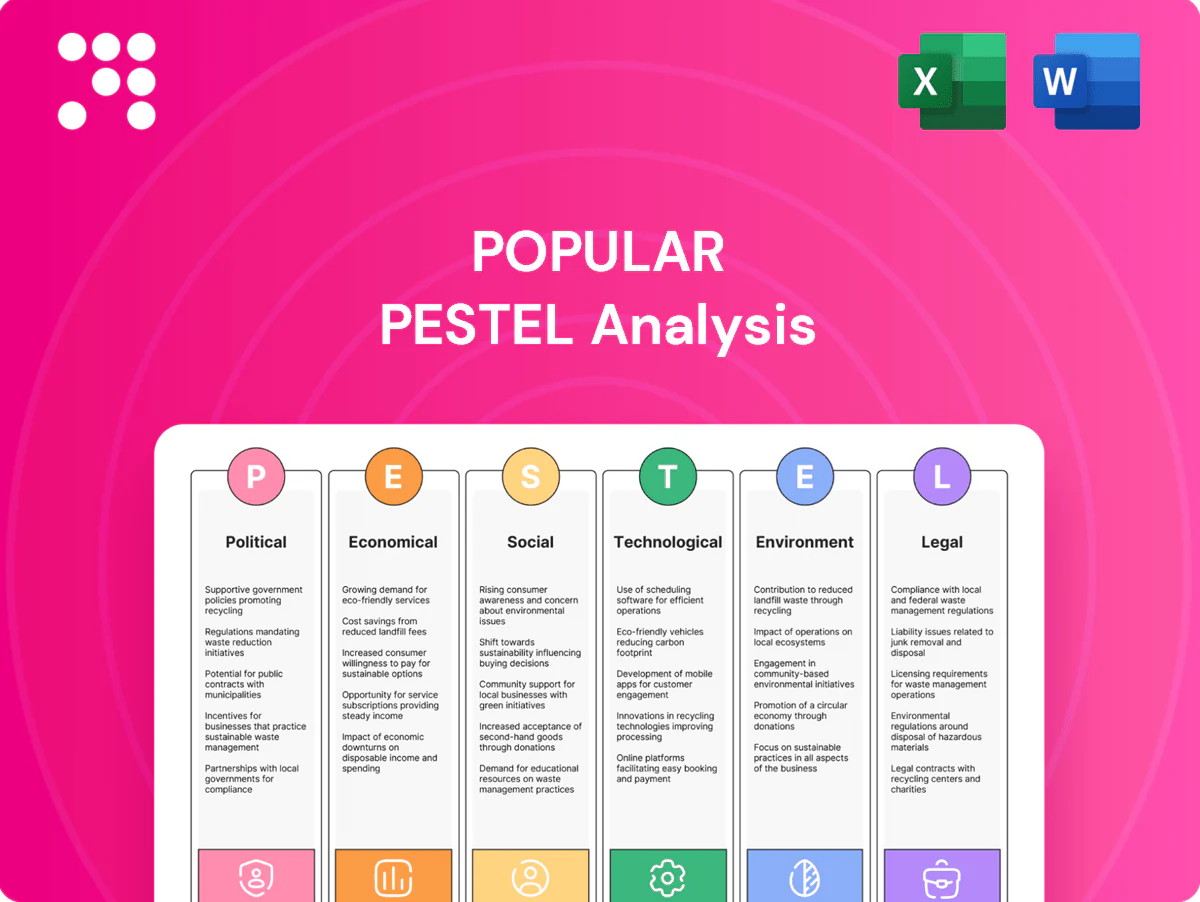

Explores how external macro-environmental factors uniquely affect the Popular across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities and support strategic planning for executives, investors, and entrepreneurs.

A concise, visually segmented PESTLE summary that teams can edit, share, and drop into presentations to streamline external risk discussions and quickly align stakeholders across functions.

Economic factors

Interest rate cycle sensitivity

Net interest income at Popular is highly sensitive to the Fed rate cycle—after the Fed peaked at 5.25–5.50% in 2023, ALM must trade off margin versus liquidity as funding mix and local deposit betas shift. Rapid rate cuts compress asset‑liability spreads and NII, while rapid hikes lift funding costs and stress liquidity. A move toward noninterest‑bearing deposits materially supports margin by lowering funding expense.

Puerto Rico macro recovery

Puerto Rico GDP growth hinges on reconstruction, manufacturing export expansion, tourism recovery (visitor levels near 2019 by 2024) and federal recovery/transfers (roughly $60B committed after Hurricane Maria and subsequent programs).

Labor force participation remains low after long-term outmigration (population fell 11.8% 2010–2020), constraining loan demand and pressuring credit quality.

A sustained upswing would lift consumer lending and SME credit, while a recession would raise delinquencies, notably in unsecured portfolios.

Mainland U.S. diversification

Popular Bank provides geographic and sectoral diversification across the mainland U.S., where deeper funding markets and fee pools reduce concentration risk; the Fed funds target stood at 5.25–5.50% as of July 2025. U.S. credit cycles and commercial real estate trends can either offset or amplify Puerto Rico swings. Funding depth and fee opportunities are broader stateside. However, CRE stress could elevate provisions.

Inflation and cost dynamics

Inflation raises operating costs and dents borrower affordability—US CPI averaged 3.4% in 2024, lifting input prices. Wage growth near 4% in 2024 and rising tech spend (global IT spend ~$5.4T in 2024, Gartner) squeeze efficiency ratios. Higher prices supported nominal loan growth in several markets while amplifying credit strain, so pricing discipline and tight cost control are vital.

- CPI 2024: US 3.4%

- Wage growth ~4% (2024)

- Global IT spend ~$5.4T (Gartner 2024)

Tourism and remittances

Tourism in Puerto Rico (≈4.2M visitors, ~$7B in receipts in 2023) and the USVI (~1.1M visitors in 2023) drives seasonal deposits and merchant fees; travel shocks (pandemics, hurricanes) quickly cut small-business cash flows. Remittances to Puerto Rico (~$8.6B in 2023) support household liquidity and sustain transaction revenues. Diversifying revenue mixes reduces this cyclicality.

- Seasonal arrivals: Puerto Rico ~4.2M (2023)

- Tourism receipts ~7B (PR, 2023)

- Remittances ~8.6B (PR, 2023)

- Diversification lowers cash-flow volatility

Oversight board, $70B debt and capped federal aid squeeze PR credit

Popular's NII is highly tied to the Fed cycle (target 5.25–5.50% Jul 2025), forcing ALM tradeoffs between margin and liquidity; rapid cuts compress spreads while hikes raise funding costs. Puerto Rico recovery (≈$60B federal recovery, tourism ~4.2M visitors, receipts ~$7B, remittances ~$8.6B) and low labor participation constrain loan growth and credit quality. Diversification to US markets reduces deposit concentration but CRE stress and inflation (US CPI 3.4% 2024; wage growth ~4% 2024) pressure costs and provisions.

| Metric | Value |

|---|---|

| Fed target Jul 2025 | 5.25–5.50% |

| US CPI 2024 | 3.4% |

| Wage growth 2024 | ~4% |

| PR visitors 2023 | ~4.2M |

| PR tourism receipts 2023 | ~$7B |

| PR remittances 2023 | ~$8.6B |

| Federal recovery | ~$60B |

What You See Is What You Get

Popular PESTLE Analysis

The preview shown here is the exact Popular PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content, layout, and structure are identical to the downloadable file. After checkout you’ll instantly get this same professional, ready-to-use PESTLE Analysis.

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of Popular—concise, evidence-based insights into political, economic, social, technological, legal, and environmental forces shaping the company. Ideal for investors, consultants, and planners, it highlights risks and opportunities you can act on. Purchase the full report for the complete, downloadable analysis and immediately applicable recommendations.

Political factors

Puerto Rico fiscal oversight

PROMESA, enacted in 2016, created the Fiscal Oversight and Management Board which controls public spending, pensions and government contracting cycles; Puerto Rico carried roughly $70 billion of public debt pre-restructuring. Popular, the island's largest bank, ties performance to local fiscal reforms and economic health—Puerto Rico GDP was about $104 billion in 2023. Budget austerity or restructurings can cut loan demand and government deposits; policy stability improves credit conditions and investor confidence.

U.S. federal policy dependency

As a U.S.-regulated bank, Popular is highly sensitive to Federal Reserve policy (federal funds 5.25–5.50% in 2024–25) and FDIC rules (deposit insurance cap $250,000), which affect funding costs and deposit flows. Federal stimulus, disaster aid and Medicaid funding for Puerto Rico (population ~3.2M) materially sway island liquidity and loan performance. Shifts in federal priorities can quickly alter credit quality and fee income, and cross-territory operations must align with U.S. national policy changes.

Disaster relief and resilience funding

Hurricane recovery and the Bipartisan Infrastructure Law (approximately 1.2 trillion USD) boost construction and mortgage activity, spurring rebuild and resiliency projects. Popular can capture loan demand from public-private rebuild programs and housing recovery funds totaling tens of billions. Aid delays or cuts can slow growth and raise NPLs; active advocacy and program participation are strategic levers.

Territorial status and political uncertainty

Debate over Puerto Rico’s status (2020 plebiscite: 52.34% for statehood) creates regulatory and tax uncertainty; shifts could alter federal benefit access, Medicaid funding (territories receive capped grants vs state FMAP), labor rules and investor treatment. With ~3.2M residents and pre-PROMESA debt near $70B, Popular must scenario-plan for compliance and capital structure changes; policy clarity would lower risk premia.

- 2020 plebiscite: 52.34% pro-statehood

- Population ≈3.2M (2023 est)

- Pre-PROMESA debt ≈$70B — potential capital flow impacts

Government banking relationships

Government banking relationships with Puerto Rico, the USVI and municipal entities drive deposit stability and fee pipelines for Popular, affecting liquidity and service revenues.

Procurement rules, transparency standards and political turnover can reallocate mandates; strong governance and competitive pricing are critical to retain public-sector business and limit churn.

- Deposit stability tied to public-sector mandates

- Procurement/transparency can shift accounts

- Governance and pricing secure renewals

- Scandal risk requires strict ethics controls

Oversight board, $70B debt and capped federal aid squeeze PR credit

PROMESA (2016) and the Fiscal Oversight Board still govern spending and pensions after ~ $70B pre-restructuring debt; Puerto Rico GDP ≈ $104B (2023) and population ≈3.2M. Federal policy (fed funds 5.25–5.50% in 2024–25) and capped Medicaid/federal aid drive liquidity and credit; 2020 plebiscite: 52.34% pro-statehood increases regulatory uncertainty.

| Metric | Value |

|---|---|

| Pre-PROMESA debt | $70B |

| GDP (2023) | $104B |

| Population (2023) | 3.2M |

| Fed funds (2024–25) | 5.25–5.50% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Popular across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities and support strategic planning for executives, investors, and entrepreneurs.

A concise, visually segmented PESTLE summary that teams can edit, share, and drop into presentations to streamline external risk discussions and quickly align stakeholders across functions.

Economic factors

Interest rate cycle sensitivity

Net interest income at Popular is highly sensitive to the Fed rate cycle—after the Fed peaked at 5.25–5.50% in 2023, ALM must trade off margin versus liquidity as funding mix and local deposit betas shift. Rapid rate cuts compress asset‑liability spreads and NII, while rapid hikes lift funding costs and stress liquidity. A move toward noninterest‑bearing deposits materially supports margin by lowering funding expense.

Puerto Rico macro recovery

Puerto Rico GDP growth hinges on reconstruction, manufacturing export expansion, tourism recovery (visitor levels near 2019 by 2024) and federal recovery/transfers (roughly $60B committed after Hurricane Maria and subsequent programs).

Labor force participation remains low after long-term outmigration (population fell 11.8% 2010–2020), constraining loan demand and pressuring credit quality.

A sustained upswing would lift consumer lending and SME credit, while a recession would raise delinquencies, notably in unsecured portfolios.

Mainland U.S. diversification

Popular Bank provides geographic and sectoral diversification across the mainland U.S., where deeper funding markets and fee pools reduce concentration risk; the Fed funds target stood at 5.25–5.50% as of July 2025. U.S. credit cycles and commercial real estate trends can either offset or amplify Puerto Rico swings. Funding depth and fee opportunities are broader stateside. However, CRE stress could elevate provisions.

Inflation and cost dynamics

Inflation raises operating costs and dents borrower affordability—US CPI averaged 3.4% in 2024, lifting input prices. Wage growth near 4% in 2024 and rising tech spend (global IT spend ~$5.4T in 2024, Gartner) squeeze efficiency ratios. Higher prices supported nominal loan growth in several markets while amplifying credit strain, so pricing discipline and tight cost control are vital.

- CPI 2024: US 3.4%

- Wage growth ~4% (2024)

- Global IT spend ~$5.4T (Gartner 2024)

Tourism and remittances

Tourism in Puerto Rico (≈4.2M visitors, ~$7B in receipts in 2023) and the USVI (~1.1M visitors in 2023) drives seasonal deposits and merchant fees; travel shocks (pandemics, hurricanes) quickly cut small-business cash flows. Remittances to Puerto Rico (~$8.6B in 2023) support household liquidity and sustain transaction revenues. Diversifying revenue mixes reduces this cyclicality.

- Seasonal arrivals: Puerto Rico ~4.2M (2023)

- Tourism receipts ~7B (PR, 2023)

- Remittances ~8.6B (PR, 2023)

- Diversification lowers cash-flow volatility

Oversight board, $70B debt and capped federal aid squeeze PR credit

Popular's NII is highly tied to the Fed cycle (target 5.25–5.50% Jul 2025), forcing ALM tradeoffs between margin and liquidity; rapid cuts compress spreads while hikes raise funding costs. Puerto Rico recovery (≈$60B federal recovery, tourism ~4.2M visitors, receipts ~$7B, remittances ~$8.6B) and low labor participation constrain loan growth and credit quality. Diversification to US markets reduces deposit concentration but CRE stress and inflation (US CPI 3.4% 2024; wage growth ~4% 2024) pressure costs and provisions.

| Metric | Value |

|---|---|

| Fed target Jul 2025 | 5.25–5.50% |

| US CPI 2024 | 3.4% |

| Wage growth 2024 | ~4% |

| PR visitors 2023 | ~4.2M |

| PR tourism receipts 2023 | ~$7B |

| PR remittances 2023 | ~$8.6B |

| Federal recovery | ~$60B |

What You See Is What You Get

Popular PESTLE Analysis

The preview shown here is the exact Popular PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content, layout, and structure are identical to the downloadable file. After checkout you’ll instantly get this same professional, ready-to-use PESTLE Analysis.

Description

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of Popular—concise, evidence-based insights into political, economic, social, technological, legal, and environmental forces shaping the company. Ideal for investors, consultants, and planners, it highlights risks and opportunities you can act on. Purchase the full report for the complete, downloadable analysis and immediately applicable recommendations.

Political factors

Puerto Rico fiscal oversight

PROMESA, enacted in 2016, created the Fiscal Oversight and Management Board which controls public spending, pensions and government contracting cycles; Puerto Rico carried roughly $70 billion of public debt pre-restructuring. Popular, the island's largest bank, ties performance to local fiscal reforms and economic health—Puerto Rico GDP was about $104 billion in 2023. Budget austerity or restructurings can cut loan demand and government deposits; policy stability improves credit conditions and investor confidence.

U.S. federal policy dependency

As a U.S.-regulated bank, Popular is highly sensitive to Federal Reserve policy (federal funds 5.25–5.50% in 2024–25) and FDIC rules (deposit insurance cap $250,000), which affect funding costs and deposit flows. Federal stimulus, disaster aid and Medicaid funding for Puerto Rico (population ~3.2M) materially sway island liquidity and loan performance. Shifts in federal priorities can quickly alter credit quality and fee income, and cross-territory operations must align with U.S. national policy changes.

Disaster relief and resilience funding

Hurricane recovery and the Bipartisan Infrastructure Law (approximately 1.2 trillion USD) boost construction and mortgage activity, spurring rebuild and resiliency projects. Popular can capture loan demand from public-private rebuild programs and housing recovery funds totaling tens of billions. Aid delays or cuts can slow growth and raise NPLs; active advocacy and program participation are strategic levers.

Territorial status and political uncertainty

Debate over Puerto Rico’s status (2020 plebiscite: 52.34% for statehood) creates regulatory and tax uncertainty; shifts could alter federal benefit access, Medicaid funding (territories receive capped grants vs state FMAP), labor rules and investor treatment. With ~3.2M residents and pre-PROMESA debt near $70B, Popular must scenario-plan for compliance and capital structure changes; policy clarity would lower risk premia.

- 2020 plebiscite: 52.34% pro-statehood

- Population ≈3.2M (2023 est)

- Pre-PROMESA debt ≈$70B — potential capital flow impacts

Government banking relationships

Government banking relationships with Puerto Rico, the USVI and municipal entities drive deposit stability and fee pipelines for Popular, affecting liquidity and service revenues.

Procurement rules, transparency standards and political turnover can reallocate mandates; strong governance and competitive pricing are critical to retain public-sector business and limit churn.

- Deposit stability tied to public-sector mandates

- Procurement/transparency can shift accounts

- Governance and pricing secure renewals

- Scandal risk requires strict ethics controls

Oversight board, $70B debt and capped federal aid squeeze PR credit

PROMESA (2016) and the Fiscal Oversight Board still govern spending and pensions after ~ $70B pre-restructuring debt; Puerto Rico GDP ≈ $104B (2023) and population ≈3.2M. Federal policy (fed funds 5.25–5.50% in 2024–25) and capped Medicaid/federal aid drive liquidity and credit; 2020 plebiscite: 52.34% pro-statehood increases regulatory uncertainty.

| Metric | Value |

|---|---|

| Pre-PROMESA debt | $70B |

| GDP (2023) | $104B |

| Population (2023) | 3.2M |

| Fed funds (2024–25) | 5.25–5.50% |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Popular across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities and support strategic planning for executives, investors, and entrepreneurs.

A concise, visually segmented PESTLE summary that teams can edit, share, and drop into presentations to streamline external risk discussions and quickly align stakeholders across functions.

Economic factors

Interest rate cycle sensitivity

Net interest income at Popular is highly sensitive to the Fed rate cycle—after the Fed peaked at 5.25–5.50% in 2023, ALM must trade off margin versus liquidity as funding mix and local deposit betas shift. Rapid rate cuts compress asset‑liability spreads and NII, while rapid hikes lift funding costs and stress liquidity. A move toward noninterest‑bearing deposits materially supports margin by lowering funding expense.

Puerto Rico macro recovery

Puerto Rico GDP growth hinges on reconstruction, manufacturing export expansion, tourism recovery (visitor levels near 2019 by 2024) and federal recovery/transfers (roughly $60B committed after Hurricane Maria and subsequent programs).

Labor force participation remains low after long-term outmigration (population fell 11.8% 2010–2020), constraining loan demand and pressuring credit quality.

A sustained upswing would lift consumer lending and SME credit, while a recession would raise delinquencies, notably in unsecured portfolios.

Mainland U.S. diversification

Popular Bank provides geographic and sectoral diversification across the mainland U.S., where deeper funding markets and fee pools reduce concentration risk; the Fed funds target stood at 5.25–5.50% as of July 2025. U.S. credit cycles and commercial real estate trends can either offset or amplify Puerto Rico swings. Funding depth and fee opportunities are broader stateside. However, CRE stress could elevate provisions.

Inflation and cost dynamics

Inflation raises operating costs and dents borrower affordability—US CPI averaged 3.4% in 2024, lifting input prices. Wage growth near 4% in 2024 and rising tech spend (global IT spend ~$5.4T in 2024, Gartner) squeeze efficiency ratios. Higher prices supported nominal loan growth in several markets while amplifying credit strain, so pricing discipline and tight cost control are vital.

- CPI 2024: US 3.4%

- Wage growth ~4% (2024)

- Global IT spend ~$5.4T (Gartner 2024)

Tourism and remittances

Tourism in Puerto Rico (≈4.2M visitors, ~$7B in receipts in 2023) and the USVI (~1.1M visitors in 2023) drives seasonal deposits and merchant fees; travel shocks (pandemics, hurricanes) quickly cut small-business cash flows. Remittances to Puerto Rico (~$8.6B in 2023) support household liquidity and sustain transaction revenues. Diversifying revenue mixes reduces this cyclicality.

- Seasonal arrivals: Puerto Rico ~4.2M (2023)

- Tourism receipts ~7B (PR, 2023)

- Remittances ~8.6B (PR, 2023)

- Diversification lowers cash-flow volatility

Oversight board, $70B debt and capped federal aid squeeze PR credit

Popular's NII is highly tied to the Fed cycle (target 5.25–5.50% Jul 2025), forcing ALM tradeoffs between margin and liquidity; rapid cuts compress spreads while hikes raise funding costs. Puerto Rico recovery (≈$60B federal recovery, tourism ~4.2M visitors, receipts ~$7B, remittances ~$8.6B) and low labor participation constrain loan growth and credit quality. Diversification to US markets reduces deposit concentration but CRE stress and inflation (US CPI 3.4% 2024; wage growth ~4% 2024) pressure costs and provisions.

| Metric | Value |

|---|---|

| Fed target Jul 2025 | 5.25–5.50% |

| US CPI 2024 | 3.4% |

| Wage growth 2024 | ~4% |

| PR visitors 2023 | ~4.2M |

| PR tourism receipts 2023 | ~$7B |

| PR remittances 2023 | ~$8.6B |

| Federal recovery | ~$60B |

What You See Is What You Get

Popular PESTLE Analysis

The preview shown here is the exact Popular PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content, layout, and structure are identical to the downloadable file. After checkout you’ll instantly get this same professional, ready-to-use PESTLE Analysis.