Popular SWOT Analysis

Make Insightful Decisions Backed by Expert Research

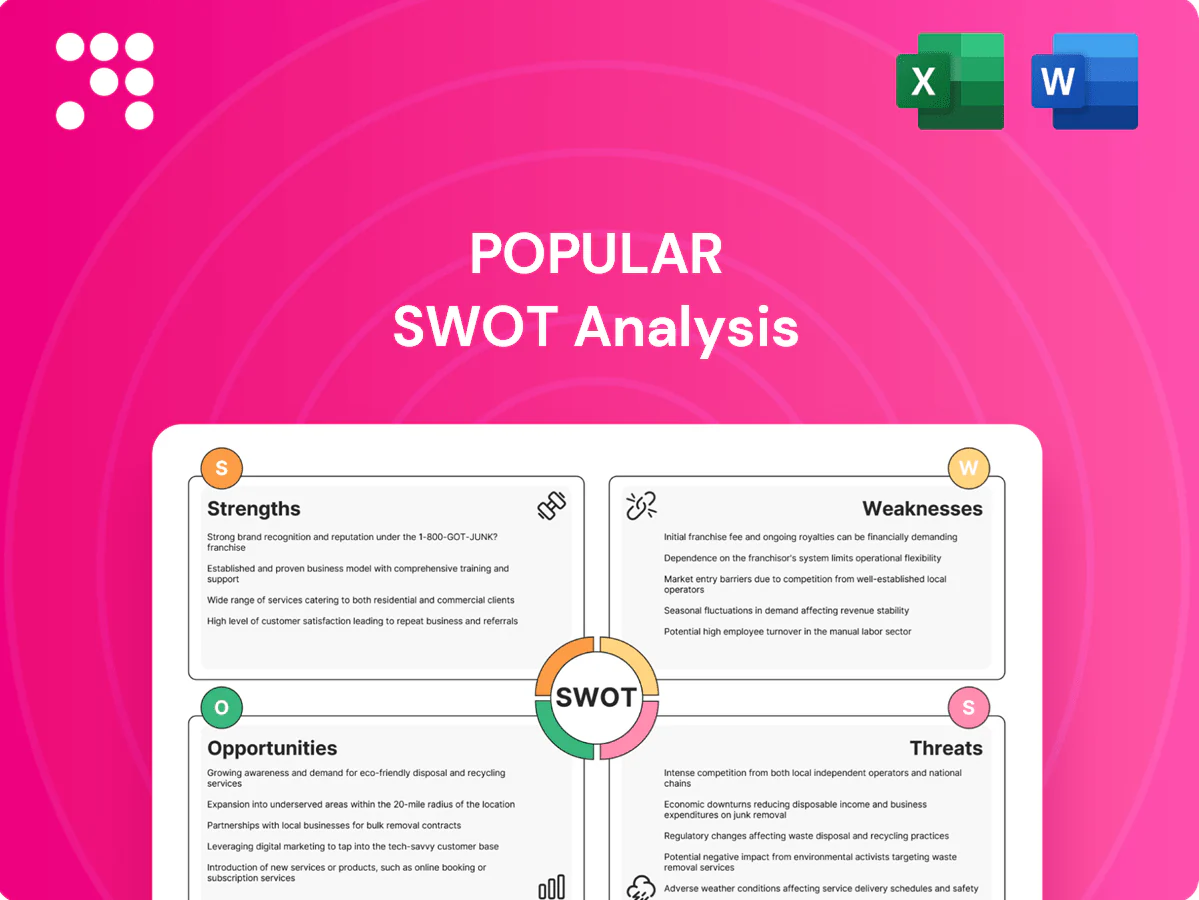

Explore a compelling snapshot of the company’s strengths, weaknesses, opportunities, and threats with our Popular SWOT Analysis—designed to clarify strategic priorities and competitive positioning. This concise review highlights key risks and growth levers for investors, advisors, and entrepreneurs. For actionable recommendations, editable templates, and financial context, purchase the full SWOT analysis and turn insight into strategy.

Strengths

Dominant PR franchise

Popular commands roughly 35% deposit market share in Puerto Rico and a comparable lending footprint, giving scale that drives brand recognition, low-cost funding and pricing power. Deep relationships with consumers, SMEs, corporates and government generate stable fee income and support resilient earnings through cycles.

Diverse revenue streams

The group spans retail, commercial, cards, investment banking, brokerage and insurance, with fee income from payments, wealth and insurance materially balancing spread income; multiple product lines enable cross-sell and higher customer lifetime value, while this diversification reduces reliance on any single revenue stream.

Stable, low-cost deposits

Core retail deposit funding lowers Popular’s interest expense, with strong CASA balances supporting net interest margins through volatile rate cycles. Relationship banking in Puerto Rico anchors sticky deposits and bolsters liquidity. This low-cost, stable funding profile enhances balance-sheet resilience and provides a durable buffer for credit and market stress.

Risk management discipline

Seasoned underwriting across Popular's consumer and commercial portfolios supports resilient credit quality, with diversified exposure across core geographies and sectors reducing concentration risk. Conservative reserve practices and healthy capital buffers help mitigate downturns, while robust compliance and credit controls sustain franchise trust and credit discipline.

- Underwriting depth across segments

- Geographic and sector diversification

- Conservative reserves + capital buffers

- Strong compliance and credit controls

Omnichannel capabilities

Popular's omnichannel capabilities combine digital banking, ATMs, and a branch network to provide broad access. Mobile and online tools deepen engagement while lowering unit costs through automation and self-service. Tech investments have improved onboarding, payments, and servicing, and the hybrid model supports retention and cross-sell.

- Digital + branch reach

- Mobile/online reduce unit costs

- Faster onboarding & payments

- Hybrid model boosts cross-sell

Puerto Rico bank with 35% deposits, six-line franchise, strong CASA funding

Popular holds roughly 35% deposit market share in Puerto Rico, giving scale for brand recognition, low-cost funding and pricing power.

Multi-line franchise spans retail, commercial, cards, investment banking, brokerage and insurance, diversifying fee income and enabling cross-sell.

Strong CASA-funded funding profile and seasoned underwriting support resilient margins, credit quality and liquidity through cycles.

| Metric | Value |

|---|---|

| Deposit market share (PR) | ~35% |

| Business lines | 6 (retail, commercial, cards, IB, brokerage, insurance) |

What is included in the product

Delivers a concise SWOT analysis of Popular, outlining its core strengths and weaknesses and the external opportunities and threats shaping its competitive position and strategic outlook.

Delivers a focused SWOT dashboard that highlights priority actions to reduce analysis paralysis and accelerate strategic decision-making across teams.

Weaknesses

Geographic concentration

Earnings are heavily tied to Puerto Rico’s economic cycle: over 50% of Popular’s loan portfolio is located in Puerto Rico per Popular, Inc.’s 2023 Form 10-K, making revenue sensitive to local GDP and employment swings. Local shocks can disproportionately reduce credit demand and deteriorate asset quality, as seen in past hurricane and fiscal stress episodes. Limited diversification versus nationwide peers heightens earnings volatility, while US mainland operations remain smaller and provide limited offset.

Scale disadvantages

Compared with megabanks, Popular carries higher per-dollar costs for technology and compliance given a smaller scale, with total assets under $100 billion as of 2024. Its smaller balance sheet limits underwriting capacity for very large syndicated deals, reducing fee income opportunities. Pricing power in competitive US markets is constrained, which can compress margins. During investment cycles this dynamic can pressure efficiency ratios and ROE.

Rate sensitivity

Asset-liability mismatches leave net interest margin highly exposed to rapid rate shifts; US banks experienced pronounced NIM swings during the 2022–23 tightening cycle.

Deposit betas climbed into roughly 40–80% in 2022–23, lifting funding costs and squeezing margins across retail-heavy franchises.

Repricing lags on loans compress spreads while hedging can blunt but not eliminate earnings volatility when rates move quickly.

Legacy systems burden

Concentration in disaster-prone areas

Operations concentrated in Puerto Rico and the USVI face acute hurricane and outage risks; Hurricane Maria (2017) caused about 90 billion dollars in damage in Puerto Rico and left many customers without power for up to 11 months, amplifying credit losses and operating costs. Business interruptions raise provisioning needs while insurance recoveries often lag by months to years, and recurring storms increase local demand and strain.

- NOAA 1991–2020 average: 14 named storms/yr — elevated exposure

- Maria: ~$90B economic damage; prolonged outages → higher credit losses

- Insurance payouts frequently delayed months–years, stressing liquidity

Puerto Rico loan concentration and volatile margins amplify credit and operational risk

Over 50% of loans are in Puerto Rico (Popular Inc. 2023 10-K), concentrating credit and revenue risk; total assets remained under $100B in 2024, limiting scale benefits. NIM and deposit betas swung sharply in 2022–23 (deposit beta ~40–80%), and Hurricane Maria caused ~$90B damage, amplifying operational and credit stress.

| Metric | Value | Source |

|---|---|---|

| PR loan share | >50% | Popular 2023 10-K |

| Total assets | <$100B (2024) | Company filings |

| Deposit beta (2022–23) | 40–80% | Industry data |

| Hurricane Maria damage | ~$90B | FEMA/estimates |

What You See Is What You Get

Popular SWOT Analysis

This is the actual Popular SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after checkout. You’re viewing a live excerpt of the real file; buy now to unlock the entire, detailed analysis.

Make Insightful Decisions Backed by Expert Research

Explore a compelling snapshot of the company’s strengths, weaknesses, opportunities, and threats with our Popular SWOT Analysis—designed to clarify strategic priorities and competitive positioning. This concise review highlights key risks and growth levers for investors, advisors, and entrepreneurs. For actionable recommendations, editable templates, and financial context, purchase the full SWOT analysis and turn insight into strategy.

Strengths

Dominant PR franchise

Popular commands roughly 35% deposit market share in Puerto Rico and a comparable lending footprint, giving scale that drives brand recognition, low-cost funding and pricing power. Deep relationships with consumers, SMEs, corporates and government generate stable fee income and support resilient earnings through cycles.

Diverse revenue streams

The group spans retail, commercial, cards, investment banking, brokerage and insurance, with fee income from payments, wealth and insurance materially balancing spread income; multiple product lines enable cross-sell and higher customer lifetime value, while this diversification reduces reliance on any single revenue stream.

Stable, low-cost deposits

Core retail deposit funding lowers Popular’s interest expense, with strong CASA balances supporting net interest margins through volatile rate cycles. Relationship banking in Puerto Rico anchors sticky deposits and bolsters liquidity. This low-cost, stable funding profile enhances balance-sheet resilience and provides a durable buffer for credit and market stress.

Risk management discipline

Seasoned underwriting across Popular's consumer and commercial portfolios supports resilient credit quality, with diversified exposure across core geographies and sectors reducing concentration risk. Conservative reserve practices and healthy capital buffers help mitigate downturns, while robust compliance and credit controls sustain franchise trust and credit discipline.

- Underwriting depth across segments

- Geographic and sector diversification

- Conservative reserves + capital buffers

- Strong compliance and credit controls

Omnichannel capabilities

Popular's omnichannel capabilities combine digital banking, ATMs, and a branch network to provide broad access. Mobile and online tools deepen engagement while lowering unit costs through automation and self-service. Tech investments have improved onboarding, payments, and servicing, and the hybrid model supports retention and cross-sell.

- Digital + branch reach

- Mobile/online reduce unit costs

- Faster onboarding & payments

- Hybrid model boosts cross-sell

Puerto Rico bank with 35% deposits, six-line franchise, strong CASA funding

Popular holds roughly 35% deposit market share in Puerto Rico, giving scale for brand recognition, low-cost funding and pricing power.

Multi-line franchise spans retail, commercial, cards, investment banking, brokerage and insurance, diversifying fee income and enabling cross-sell.

Strong CASA-funded funding profile and seasoned underwriting support resilient margins, credit quality and liquidity through cycles.

| Metric | Value |

|---|---|

| Deposit market share (PR) | ~35% |

| Business lines | 6 (retail, commercial, cards, IB, brokerage, insurance) |

What is included in the product

Delivers a concise SWOT analysis of Popular, outlining its core strengths and weaknesses and the external opportunities and threats shaping its competitive position and strategic outlook.

Delivers a focused SWOT dashboard that highlights priority actions to reduce analysis paralysis and accelerate strategic decision-making across teams.

Weaknesses

Geographic concentration

Earnings are heavily tied to Puerto Rico’s economic cycle: over 50% of Popular’s loan portfolio is located in Puerto Rico per Popular, Inc.’s 2023 Form 10-K, making revenue sensitive to local GDP and employment swings. Local shocks can disproportionately reduce credit demand and deteriorate asset quality, as seen in past hurricane and fiscal stress episodes. Limited diversification versus nationwide peers heightens earnings volatility, while US mainland operations remain smaller and provide limited offset.

Scale disadvantages

Compared with megabanks, Popular carries higher per-dollar costs for technology and compliance given a smaller scale, with total assets under $100 billion as of 2024. Its smaller balance sheet limits underwriting capacity for very large syndicated deals, reducing fee income opportunities. Pricing power in competitive US markets is constrained, which can compress margins. During investment cycles this dynamic can pressure efficiency ratios and ROE.

Rate sensitivity

Asset-liability mismatches leave net interest margin highly exposed to rapid rate shifts; US banks experienced pronounced NIM swings during the 2022–23 tightening cycle.

Deposit betas climbed into roughly 40–80% in 2022–23, lifting funding costs and squeezing margins across retail-heavy franchises.

Repricing lags on loans compress spreads while hedging can blunt but not eliminate earnings volatility when rates move quickly.

Legacy systems burden

Concentration in disaster-prone areas

Operations concentrated in Puerto Rico and the USVI face acute hurricane and outage risks; Hurricane Maria (2017) caused about 90 billion dollars in damage in Puerto Rico and left many customers without power for up to 11 months, amplifying credit losses and operating costs. Business interruptions raise provisioning needs while insurance recoveries often lag by months to years, and recurring storms increase local demand and strain.

- NOAA 1991–2020 average: 14 named storms/yr — elevated exposure

- Maria: ~$90B economic damage; prolonged outages → higher credit losses

- Insurance payouts frequently delayed months–years, stressing liquidity

Puerto Rico loan concentration and volatile margins amplify credit and operational risk

Over 50% of loans are in Puerto Rico (Popular Inc. 2023 10-K), concentrating credit and revenue risk; total assets remained under $100B in 2024, limiting scale benefits. NIM and deposit betas swung sharply in 2022–23 (deposit beta ~40–80%), and Hurricane Maria caused ~$90B damage, amplifying operational and credit stress.

| Metric | Value | Source |

|---|---|---|

| PR loan share | >50% | Popular 2023 10-K |

| Total assets | <$100B (2024) | Company filings |

| Deposit beta (2022–23) | 40–80% | Industry data |

| Hurricane Maria damage | ~$90B | FEMA/estimates |

What You See Is What You Get

Popular SWOT Analysis

This is the actual Popular SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after checkout. You’re viewing a live excerpt of the real file; buy now to unlock the entire, detailed analysis.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Explore a compelling snapshot of the company’s strengths, weaknesses, opportunities, and threats with our Popular SWOT Analysis—designed to clarify strategic priorities and competitive positioning. This concise review highlights key risks and growth levers for investors, advisors, and entrepreneurs. For actionable recommendations, editable templates, and financial context, purchase the full SWOT analysis and turn insight into strategy.

Strengths

Dominant PR franchise

Popular commands roughly 35% deposit market share in Puerto Rico and a comparable lending footprint, giving scale that drives brand recognition, low-cost funding and pricing power. Deep relationships with consumers, SMEs, corporates and government generate stable fee income and support resilient earnings through cycles.

Diverse revenue streams

The group spans retail, commercial, cards, investment banking, brokerage and insurance, with fee income from payments, wealth and insurance materially balancing spread income; multiple product lines enable cross-sell and higher customer lifetime value, while this diversification reduces reliance on any single revenue stream.

Stable, low-cost deposits

Core retail deposit funding lowers Popular’s interest expense, with strong CASA balances supporting net interest margins through volatile rate cycles. Relationship banking in Puerto Rico anchors sticky deposits and bolsters liquidity. This low-cost, stable funding profile enhances balance-sheet resilience and provides a durable buffer for credit and market stress.

Risk management discipline

Seasoned underwriting across Popular's consumer and commercial portfolios supports resilient credit quality, with diversified exposure across core geographies and sectors reducing concentration risk. Conservative reserve practices and healthy capital buffers help mitigate downturns, while robust compliance and credit controls sustain franchise trust and credit discipline.

- Underwriting depth across segments

- Geographic and sector diversification

- Conservative reserves + capital buffers

- Strong compliance and credit controls

Omnichannel capabilities

Popular's omnichannel capabilities combine digital banking, ATMs, and a branch network to provide broad access. Mobile and online tools deepen engagement while lowering unit costs through automation and self-service. Tech investments have improved onboarding, payments, and servicing, and the hybrid model supports retention and cross-sell.

- Digital + branch reach

- Mobile/online reduce unit costs

- Faster onboarding & payments

- Hybrid model boosts cross-sell

Puerto Rico bank with 35% deposits, six-line franchise, strong CASA funding

Popular holds roughly 35% deposit market share in Puerto Rico, giving scale for brand recognition, low-cost funding and pricing power.

Multi-line franchise spans retail, commercial, cards, investment banking, brokerage and insurance, diversifying fee income and enabling cross-sell.

Strong CASA-funded funding profile and seasoned underwriting support resilient margins, credit quality and liquidity through cycles.

| Metric | Value |

|---|---|

| Deposit market share (PR) | ~35% |

| Business lines | 6 (retail, commercial, cards, IB, brokerage, insurance) |

What is included in the product

Delivers a concise SWOT analysis of Popular, outlining its core strengths and weaknesses and the external opportunities and threats shaping its competitive position and strategic outlook.

Delivers a focused SWOT dashboard that highlights priority actions to reduce analysis paralysis and accelerate strategic decision-making across teams.

Weaknesses

Geographic concentration

Earnings are heavily tied to Puerto Rico’s economic cycle: over 50% of Popular’s loan portfolio is located in Puerto Rico per Popular, Inc.’s 2023 Form 10-K, making revenue sensitive to local GDP and employment swings. Local shocks can disproportionately reduce credit demand and deteriorate asset quality, as seen in past hurricane and fiscal stress episodes. Limited diversification versus nationwide peers heightens earnings volatility, while US mainland operations remain smaller and provide limited offset.

Scale disadvantages

Compared with megabanks, Popular carries higher per-dollar costs for technology and compliance given a smaller scale, with total assets under $100 billion as of 2024. Its smaller balance sheet limits underwriting capacity for very large syndicated deals, reducing fee income opportunities. Pricing power in competitive US markets is constrained, which can compress margins. During investment cycles this dynamic can pressure efficiency ratios and ROE.

Rate sensitivity

Asset-liability mismatches leave net interest margin highly exposed to rapid rate shifts; US banks experienced pronounced NIM swings during the 2022–23 tightening cycle.

Deposit betas climbed into roughly 40–80% in 2022–23, lifting funding costs and squeezing margins across retail-heavy franchises.

Repricing lags on loans compress spreads while hedging can blunt but not eliminate earnings volatility when rates move quickly.

Legacy systems burden

Concentration in disaster-prone areas

Operations concentrated in Puerto Rico and the USVI face acute hurricane and outage risks; Hurricane Maria (2017) caused about 90 billion dollars in damage in Puerto Rico and left many customers without power for up to 11 months, amplifying credit losses and operating costs. Business interruptions raise provisioning needs while insurance recoveries often lag by months to years, and recurring storms increase local demand and strain.

- NOAA 1991–2020 average: 14 named storms/yr — elevated exposure

- Maria: ~$90B economic damage; prolonged outages → higher credit losses

- Insurance payouts frequently delayed months–years, stressing liquidity

Puerto Rico loan concentration and volatile margins amplify credit and operational risk

Over 50% of loans are in Puerto Rico (Popular Inc. 2023 10-K), concentrating credit and revenue risk; total assets remained under $100B in 2024, limiting scale benefits. NIM and deposit betas swung sharply in 2022–23 (deposit beta ~40–80%), and Hurricane Maria caused ~$90B damage, amplifying operational and credit stress.

| Metric | Value | Source |

|---|---|---|

| PR loan share | >50% | Popular 2023 10-K |

| Total assets | <$100B (2024) | Company filings |

| Deposit beta (2022–23) | 40–80% | Industry data |

| Hurricane Maria damage | ~$90B | FEMA/estimates |

What You See Is What You Get

Popular SWOT Analysis

This is the actual Popular SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after checkout. You’re viewing a live excerpt of the real file; buy now to unlock the entire, detailed analysis.