Österreichische Post AG ( dba Austrian Post) Porter's Five Forces Analysis

From Overview to Strategy Blueprint

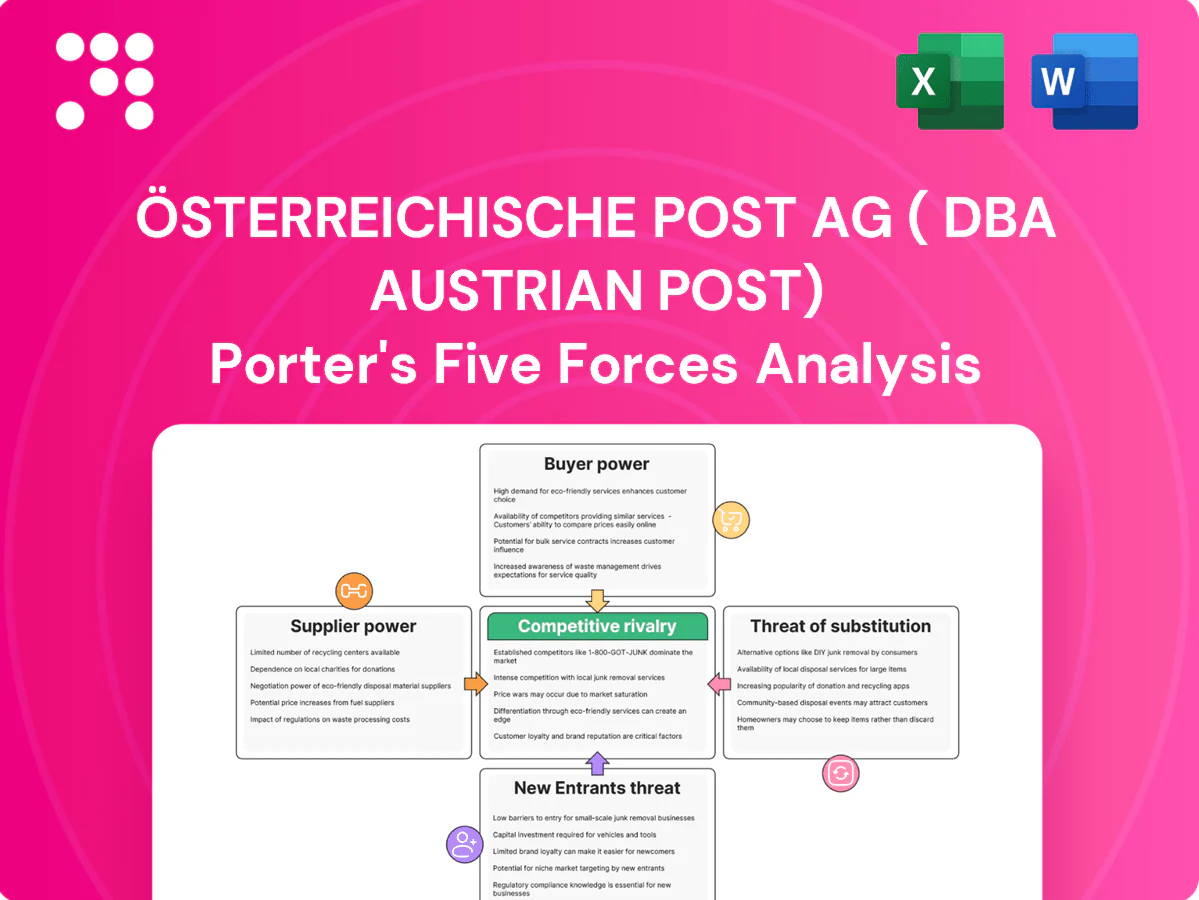

Österreichische Post AG faces moderate buyer power, high regulatory barriers, and rising substitute threats from digital communication and private couriers, while scale and network effects limit new entrants and supplier leverage remains modest; strategic moves on e-commerce logistics are pivotal. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Fuel and energy providers influence costs

Österreichische Post’s cost base is highly sensitive to diesel (~€1.75/l avg 2024) and electricity (~€0.30/kWh avg 2024) and heating price swings; a limited number of regional refiners/utilities and long-term supplier contracts dampen but do not remove volatility. Scaling EV charging and renewable PPAs diversifies sources yet creates dependency on new grid and charging infrastructure. Financial hedges reduce short spikes but cannot fully offset prolonged price shocks.

Fleet, equipment, and spare parts OEMs

Fleet, equipment and spare-parts OEMs are concentrated in Europe among Daimler Truck, Traton (VW Group) and Volvo Group, giving suppliers pricing and lead-time leverage for trucks, vans, e-bikes drivetrains and sorting machines. Österreichische Post can multi-source and standardize parts to reduce dependency, but type-approval, certification and maintenance cycles limit rapid switching. Global supply-chain disruptions since 2020 have intermittently extended delivery times and raised procurement costs.

Air, rail, and linehaul capacity providers

For international mail and parcels Austrian Post relies on bellyhold and dedicated cargo capacity plus rail linehaul as critical inputs, with peak seasons and constrained lanes increasing rates and supplier leverage. Long-term block-space and rail contracts secure volumes and predictability but reduce operational flexibility. Modal shift to rail/road mitigates air dependence, yet customer service-speed requirements limit full substitutability.

IT platforms and parcel locker hardware

Sortation software, last‑mile routing, cybersecurity and locker systems often come from specialized vendors, creating integration complexity and data lock‑in that raise switching costs and strengthen supplier power; proven providers remain critical due to uptime SLAs and security obligations, though open APIs and modular architectures can rebalance negotiation leverage.

- Specialized vendors drive integration and lock‑in

- Switching costs amplified by data and routing complexity

- Open APIs/modularity reduce supplier leverage

- Uptime SLAs and cybersecurity keep dependence high

Labor as a quasi-supplier

Labor functions as a quasi-supplier for Österreichische Post: a large delivery workforce of approximately 23,000 employees (2024) and strong collective agreements shape costs and operational flexibility. Tight labor markets and 2024 wage pressures raise bargaining leverage for unions, while automation and route optimization can reduce labor intensity but require significant capex and change management. Service quality and universal service obligations constrain rapid labour-model changes.

- Workforce: ~23,000 (2024)

- Union/CBAs: high influence on costs

- Wage pressure: elevated in 2024

- Mitigation: automation, route optimization (requires investment)

- Constraint: service mandates limit rapid shifts

Moderate-high supplier power: diesel €1.75/l, electricity €0.30/kWh

Supplier power is moderate–high: energy price exposure (diesel €1.75/l, electricity €0.30/kWh avg 2024) and concentrated OEMs/air-rail carriers give suppliers leverage. Long-term contracts, hedges and multi‑sourcing reduce but do not eliminate risks. Labour (~23,000 in 2024) and specialized IT/maintenance vendors create switching costs and bargaining strength.

| Item | 2024 |

|---|---|

| Diesel | €1.75/l |

| Electricity | €0.30/kWh |

| Workforce | ~23,000 |

What is included in the product

Tailored Porter's Five Forces analysis for Österreichische Post AG (Austrian Post) uncovers competitive intensity, buyer/supplier power, entry barriers and substitution threats, highlighting digital disruption, logistics scale advantages, regulatory protections and pricing pressures to inform strategic, investor, and academic use in editable formats.

A clear one-sheet Porter's Five Forces for Österreichische Post AG that highlights regulatory risk, digital substitution and labor cost pressures—perfect for quick decision-making. Customize pressure levels or swap in your own data to instantly translate strategic pressure into pitch-ready slides.

Customers Bargaining Power

Large e-commerce shippers negotiate hard

In 2024 marketplaces and major retailers remain the primary drivers of Austrian Post parcel volumes, demanding aggressive tariffs and strict SLAs that compress margins. Their ability to multi-home across carriers strengthens bargaining power, forcing frequent rebids as track-and-trace transparency exposes performance gaps. Volume commitments and co-developed solutions can lock customers in but typically at lower unit margins.

SMEs value reliability yet compare prices

SMEs (99.7% of Austrian firms in 2024) are price-aware but prize pickup convenience and local support, making buyer power selective; switching costs are moderate thanks to fast digital onboarding and label tools. Bundled fulfillment, returns and cross-border services lower churn, while loyalty programs and simple pricing tiers further soften customer bargaining power; Austrian Post reported group revenue €2.7bn in 2024.

Households with low switching costs for letters

For addressed mail, end-users have little bargaining power over prices but can increasingly shift to digital alternatives, limiting demand for letters. Price caps and the universal service obligation constrain Austrian Post’s rate flexibility more than direct buyer pressure. Delivery frequency and access-point expectations drive perceived value of postal services. Ongoing declines in mail volumes make customers highly price-sensitive to any tariff changes.

International clients demand cross-border reach

International clients demand predictable transit times, customs handling and returns; exporters/importers benchmark Austrian Post against integrators and EU parcel networks, increasing buyer power. Multi-carrier platforms lower switching costs, while harmonized EU schemes and tracked DDP services can lock share; Austrian Post reported ~200m parcels and €3.1bn revenue in 2024, underscoring commercial pressure.

- Predictability: transit, customs, returns

- Benchmarking vs integrators/EU networks

- Multi-carrier platforms = higher switching

- Harmonized EU + tracked DDP = retention

Returns-heavy fashion and electronics

Retailers and marketplaces dictate low tariffs; high fashion returns drive reverse-logistics pricing

Customers hold significant bargaining power: marketplaces and retailers drive parcel volumes and demand low tariffs and SLAs, while SMEs value convenience over price. International shippers benchmark against integrators, increasing switching. High return rates (fashion 30–40%) push retailers to negotiate reverse-logistics terms and data-driven service pricing.

| Metric | 2024 |

|---|---|

| Parcels | ~200m |

| Revenue | €3.1bn / €2.7bn |

| Fashion returns | 30–40% |

What You See Is What You Get

Österreichische Post AG ( dba Austrian Post) Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Österreichische Post AG you’ll receive—no placeholders. It evaluates competitive rivalry, supplier and buyer power, threat of substitution and entry with tailored insights. Purchase grants instant access to this fully formatted document.

From Overview to Strategy Blueprint

Österreichische Post AG faces moderate buyer power, high regulatory barriers, and rising substitute threats from digital communication and private couriers, while scale and network effects limit new entrants and supplier leverage remains modest; strategic moves on e-commerce logistics are pivotal. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Fuel and energy providers influence costs

Österreichische Post’s cost base is highly sensitive to diesel (~€1.75/l avg 2024) and electricity (~€0.30/kWh avg 2024) and heating price swings; a limited number of regional refiners/utilities and long-term supplier contracts dampen but do not remove volatility. Scaling EV charging and renewable PPAs diversifies sources yet creates dependency on new grid and charging infrastructure. Financial hedges reduce short spikes but cannot fully offset prolonged price shocks.

Fleet, equipment, and spare parts OEMs

Fleet, equipment and spare-parts OEMs are concentrated in Europe among Daimler Truck, Traton (VW Group) and Volvo Group, giving suppliers pricing and lead-time leverage for trucks, vans, e-bikes drivetrains and sorting machines. Österreichische Post can multi-source and standardize parts to reduce dependency, but type-approval, certification and maintenance cycles limit rapid switching. Global supply-chain disruptions since 2020 have intermittently extended delivery times and raised procurement costs.

Air, rail, and linehaul capacity providers

For international mail and parcels Austrian Post relies on bellyhold and dedicated cargo capacity plus rail linehaul as critical inputs, with peak seasons and constrained lanes increasing rates and supplier leverage. Long-term block-space and rail contracts secure volumes and predictability but reduce operational flexibility. Modal shift to rail/road mitigates air dependence, yet customer service-speed requirements limit full substitutability.

IT platforms and parcel locker hardware

Sortation software, last‑mile routing, cybersecurity and locker systems often come from specialized vendors, creating integration complexity and data lock‑in that raise switching costs and strengthen supplier power; proven providers remain critical due to uptime SLAs and security obligations, though open APIs and modular architectures can rebalance negotiation leverage.

- Specialized vendors drive integration and lock‑in

- Switching costs amplified by data and routing complexity

- Open APIs/modularity reduce supplier leverage

- Uptime SLAs and cybersecurity keep dependence high

Labor as a quasi-supplier

Labor functions as a quasi-supplier for Österreichische Post: a large delivery workforce of approximately 23,000 employees (2024) and strong collective agreements shape costs and operational flexibility. Tight labor markets and 2024 wage pressures raise bargaining leverage for unions, while automation and route optimization can reduce labor intensity but require significant capex and change management. Service quality and universal service obligations constrain rapid labour-model changes.

- Workforce: ~23,000 (2024)

- Union/CBAs: high influence on costs

- Wage pressure: elevated in 2024

- Mitigation: automation, route optimization (requires investment)

- Constraint: service mandates limit rapid shifts

Moderate-high supplier power: diesel €1.75/l, electricity €0.30/kWh

Supplier power is moderate–high: energy price exposure (diesel €1.75/l, electricity €0.30/kWh avg 2024) and concentrated OEMs/air-rail carriers give suppliers leverage. Long-term contracts, hedges and multi‑sourcing reduce but do not eliminate risks. Labour (~23,000 in 2024) and specialized IT/maintenance vendors create switching costs and bargaining strength.

| Item | 2024 |

|---|---|

| Diesel | €1.75/l |

| Electricity | €0.30/kWh |

| Workforce | ~23,000 |

What is included in the product

Tailored Porter's Five Forces analysis for Österreichische Post AG (Austrian Post) uncovers competitive intensity, buyer/supplier power, entry barriers and substitution threats, highlighting digital disruption, logistics scale advantages, regulatory protections and pricing pressures to inform strategic, investor, and academic use in editable formats.

A clear one-sheet Porter's Five Forces for Österreichische Post AG that highlights regulatory risk, digital substitution and labor cost pressures—perfect for quick decision-making. Customize pressure levels or swap in your own data to instantly translate strategic pressure into pitch-ready slides.

Customers Bargaining Power

Large e-commerce shippers negotiate hard

In 2024 marketplaces and major retailers remain the primary drivers of Austrian Post parcel volumes, demanding aggressive tariffs and strict SLAs that compress margins. Their ability to multi-home across carriers strengthens bargaining power, forcing frequent rebids as track-and-trace transparency exposes performance gaps. Volume commitments and co-developed solutions can lock customers in but typically at lower unit margins.

SMEs value reliability yet compare prices

SMEs (99.7% of Austrian firms in 2024) are price-aware but prize pickup convenience and local support, making buyer power selective; switching costs are moderate thanks to fast digital onboarding and label tools. Bundled fulfillment, returns and cross-border services lower churn, while loyalty programs and simple pricing tiers further soften customer bargaining power; Austrian Post reported group revenue €2.7bn in 2024.

Households with low switching costs for letters

For addressed mail, end-users have little bargaining power over prices but can increasingly shift to digital alternatives, limiting demand for letters. Price caps and the universal service obligation constrain Austrian Post’s rate flexibility more than direct buyer pressure. Delivery frequency and access-point expectations drive perceived value of postal services. Ongoing declines in mail volumes make customers highly price-sensitive to any tariff changes.

International clients demand cross-border reach

International clients demand predictable transit times, customs handling and returns; exporters/importers benchmark Austrian Post against integrators and EU parcel networks, increasing buyer power. Multi-carrier platforms lower switching costs, while harmonized EU schemes and tracked DDP services can lock share; Austrian Post reported ~200m parcels and €3.1bn revenue in 2024, underscoring commercial pressure.

- Predictability: transit, customs, returns

- Benchmarking vs integrators/EU networks

- Multi-carrier platforms = higher switching

- Harmonized EU + tracked DDP = retention

Returns-heavy fashion and electronics

Retailers and marketplaces dictate low tariffs; high fashion returns drive reverse-logistics pricing

Customers hold significant bargaining power: marketplaces and retailers drive parcel volumes and demand low tariffs and SLAs, while SMEs value convenience over price. International shippers benchmark against integrators, increasing switching. High return rates (fashion 30–40%) push retailers to negotiate reverse-logistics terms and data-driven service pricing.

| Metric | 2024 |

|---|---|

| Parcels | ~200m |

| Revenue | €3.1bn / €2.7bn |

| Fashion returns | 30–40% |

What You See Is What You Get

Österreichische Post AG ( dba Austrian Post) Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Österreichische Post AG you’ll receive—no placeholders. It evaluates competitive rivalry, supplier and buyer power, threat of substitution and entry with tailored insights. Purchase grants instant access to this fully formatted document.

Description

From Overview to Strategy Blueprint

Österreichische Post AG faces moderate buyer power, high regulatory barriers, and rising substitute threats from digital communication and private couriers, while scale and network effects limit new entrants and supplier leverage remains modest; strategic moves on e-commerce logistics are pivotal. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Fuel and energy providers influence costs

Österreichische Post’s cost base is highly sensitive to diesel (~€1.75/l avg 2024) and electricity (~€0.30/kWh avg 2024) and heating price swings; a limited number of regional refiners/utilities and long-term supplier contracts dampen but do not remove volatility. Scaling EV charging and renewable PPAs diversifies sources yet creates dependency on new grid and charging infrastructure. Financial hedges reduce short spikes but cannot fully offset prolonged price shocks.

Fleet, equipment, and spare parts OEMs

Fleet, equipment and spare-parts OEMs are concentrated in Europe among Daimler Truck, Traton (VW Group) and Volvo Group, giving suppliers pricing and lead-time leverage for trucks, vans, e-bikes drivetrains and sorting machines. Österreichische Post can multi-source and standardize parts to reduce dependency, but type-approval, certification and maintenance cycles limit rapid switching. Global supply-chain disruptions since 2020 have intermittently extended delivery times and raised procurement costs.

Air, rail, and linehaul capacity providers

For international mail and parcels Austrian Post relies on bellyhold and dedicated cargo capacity plus rail linehaul as critical inputs, with peak seasons and constrained lanes increasing rates and supplier leverage. Long-term block-space and rail contracts secure volumes and predictability but reduce operational flexibility. Modal shift to rail/road mitigates air dependence, yet customer service-speed requirements limit full substitutability.

IT platforms and parcel locker hardware

Sortation software, last‑mile routing, cybersecurity and locker systems often come from specialized vendors, creating integration complexity and data lock‑in that raise switching costs and strengthen supplier power; proven providers remain critical due to uptime SLAs and security obligations, though open APIs and modular architectures can rebalance negotiation leverage.

- Specialized vendors drive integration and lock‑in

- Switching costs amplified by data and routing complexity

- Open APIs/modularity reduce supplier leverage

- Uptime SLAs and cybersecurity keep dependence high

Labor as a quasi-supplier

Labor functions as a quasi-supplier for Österreichische Post: a large delivery workforce of approximately 23,000 employees (2024) and strong collective agreements shape costs and operational flexibility. Tight labor markets and 2024 wage pressures raise bargaining leverage for unions, while automation and route optimization can reduce labor intensity but require significant capex and change management. Service quality and universal service obligations constrain rapid labour-model changes.

- Workforce: ~23,000 (2024)

- Union/CBAs: high influence on costs

- Wage pressure: elevated in 2024

- Mitigation: automation, route optimization (requires investment)

- Constraint: service mandates limit rapid shifts

Moderate-high supplier power: diesel €1.75/l, electricity €0.30/kWh

Supplier power is moderate–high: energy price exposure (diesel €1.75/l, electricity €0.30/kWh avg 2024) and concentrated OEMs/air-rail carriers give suppliers leverage. Long-term contracts, hedges and multi‑sourcing reduce but do not eliminate risks. Labour (~23,000 in 2024) and specialized IT/maintenance vendors create switching costs and bargaining strength.

| Item | 2024 |

|---|---|

| Diesel | €1.75/l |

| Electricity | €0.30/kWh |

| Workforce | ~23,000 |

What is included in the product

Tailored Porter's Five Forces analysis for Österreichische Post AG (Austrian Post) uncovers competitive intensity, buyer/supplier power, entry barriers and substitution threats, highlighting digital disruption, logistics scale advantages, regulatory protections and pricing pressures to inform strategic, investor, and academic use in editable formats.

A clear one-sheet Porter's Five Forces for Österreichische Post AG that highlights regulatory risk, digital substitution and labor cost pressures—perfect for quick decision-making. Customize pressure levels or swap in your own data to instantly translate strategic pressure into pitch-ready slides.

Customers Bargaining Power

Large e-commerce shippers negotiate hard

In 2024 marketplaces and major retailers remain the primary drivers of Austrian Post parcel volumes, demanding aggressive tariffs and strict SLAs that compress margins. Their ability to multi-home across carriers strengthens bargaining power, forcing frequent rebids as track-and-trace transparency exposes performance gaps. Volume commitments and co-developed solutions can lock customers in but typically at lower unit margins.

SMEs value reliability yet compare prices

SMEs (99.7% of Austrian firms in 2024) are price-aware but prize pickup convenience and local support, making buyer power selective; switching costs are moderate thanks to fast digital onboarding and label tools. Bundled fulfillment, returns and cross-border services lower churn, while loyalty programs and simple pricing tiers further soften customer bargaining power; Austrian Post reported group revenue €2.7bn in 2024.

Households with low switching costs for letters

For addressed mail, end-users have little bargaining power over prices but can increasingly shift to digital alternatives, limiting demand for letters. Price caps and the universal service obligation constrain Austrian Post’s rate flexibility more than direct buyer pressure. Delivery frequency and access-point expectations drive perceived value of postal services. Ongoing declines in mail volumes make customers highly price-sensitive to any tariff changes.

International clients demand cross-border reach

International clients demand predictable transit times, customs handling and returns; exporters/importers benchmark Austrian Post against integrators and EU parcel networks, increasing buyer power. Multi-carrier platforms lower switching costs, while harmonized EU schemes and tracked DDP services can lock share; Austrian Post reported ~200m parcels and €3.1bn revenue in 2024, underscoring commercial pressure.

- Predictability: transit, customs, returns

- Benchmarking vs integrators/EU networks

- Multi-carrier platforms = higher switching

- Harmonized EU + tracked DDP = retention

Returns-heavy fashion and electronics

Retailers and marketplaces dictate low tariffs; high fashion returns drive reverse-logistics pricing

Customers hold significant bargaining power: marketplaces and retailers drive parcel volumes and demand low tariffs and SLAs, while SMEs value convenience over price. International shippers benchmark against integrators, increasing switching. High return rates (fashion 30–40%) push retailers to negotiate reverse-logistics terms and data-driven service pricing.

| Metric | 2024 |

|---|---|

| Parcels | ~200m |

| Revenue | €3.1bn / €2.7bn |

| Fashion returns | 30–40% |

What You See Is What You Get

Österreichische Post AG ( dba Austrian Post) Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Österreichische Post AG you’ll receive—no placeholders. It evaluates competitive rivalry, supplier and buyer power, threat of substitution and entry with tailored insights. Purchase grants instant access to this fully formatted document.