Posti Group Oyj Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Posti Group Oyj faces moderate buyer power and low supplier leverage thanks to scale and integrated logistics, while regulatory barriers and capital intensity limit new entrants; digital substitutes and parcel disruptors, however, raise strategic pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Posti Group Oyj’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel and energy dependence

Diesel and electricity costs materially affect Posti’s linehaul and sorting economics; Brent crude averaged about $85/bbl in 2024 and EU industrial electricity prices were near €0.15/kWh, which can shift margins quickly and give fuel suppliers leverage. Hedging reduces volatility but could not fully neutralize 2024 price swings. Transition to EVs and biofuels diversifies fuel sources but increases dependency on charging and biofuel supply infrastructure.

Vehicle and equipment OEMs

Vehicle and equipment OEMs are concentrated: the top three truck OEMs account for roughly 70% of the EU heavy truck market (2023–24), with van markets likewise dominated by a few players. Long lead times of 6–12 months and bespoke specs give suppliers leverage over price and service terms. Multi-sourcing and framework contracts mitigate exposure, but high switching costs and maintenance contracts—often ~10–15% of lifecycle spend—lock in supplier power.

IT, data, and platform vendors

Posti depends on routing, TMS/WMS, cybersecurity and cloud vendors, tying critical operations to a few providers; Posti reported ~€1.7bn revenue in 2023, making vendor outages or license shifts material to margins and service levels. Vendor lock-in and integration complexity raise switching costs and can delay remediation; strategic partnerships and modular architectures have reduced supplier power in logistics by enabling phased migration and alternative suppliers.

Labor and subcontracted carriers

Unionized Posti workforce and a wide subcontractor carrier network are critical supplier inputs; collective wage agreements and driver availability directly affect unit cost and operational flexibility. Tight Finnish labor markets in 2024 have strengthened contractor bargaining power, raising spot rates and limiting rapid capacity scaling. Automation lowers routine labor needs but peak-season volumes still rely heavily on external fleets, keeping supplier leverage high.

- Labor centrality

- Wage agreements drive costs

- Driver scarcity increases supplier power

- Automation reduces but does not eliminate peak reliance

Real estate and infrastructure

Supplier leverage: fuel & power costs and concentrated OEMs ~70%, 6–12m

Suppliers exert high leverage: fuel (Brent ~$85/bbl, EU power ~€0.15/kWh in 2024) and concentrated OEMs (top‑3 trucks ~70% market) drive input cost volatility and switching costs. IT, maintenance (10–15% lifecycle) and scarce urban sites (Greater Helsinki ~1.5M) increase dependency; lead times 6–12 months limit agility. Posti scale (€1.7bn rev 2023) makes vendor disruptions material.

| Input | 2024/2023 |

|---|---|

| Brent crude | $85/bbl (2024) |

| EU electricity | €0.15/kWh (2024) |

| Top‑3 truck OEMs | ~70% EU market |

| Posti revenue | €1.7bn (2023) |

| Lead times | 6–12 months |

What is included in the product

Tailored exclusively for Posti Group Oyj, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, supplier power, and market entry risks affecting postal and logistics operations, while identifying disruptive substitutes and regulatory dynamics that shape pricing, profitability, and strategic positioning.

A clear, one-sheet summary of Posti Group Oyj's five forces—quickly highlights competitive, regulatory and digital-disruption pressures to speed decision-making. Swap in your own data and scenario tabs to test pre/post regulation or new entrants without macros, ideal for board decks.

Customers Bargaining Power

Large e-commerce shippers

Large e-commerce shippers in 2024 negotiate steep volume discounts and leverage dual-sourcing with DHL, PostNord and DB Schenker to extract better rates from Posti. High SLAs on speed and returns raise service-level expectations and operational cost pressure. Performance lapses during peak seasons increase churn risk as major retailers can switch carriers rapidly. This concentration amplifies buyer bargaining power against Posti.

Public sector and enterprise mailers

Government and large billers exert strong price pressure as letter volumes have declined c.10% year-on-year, pushing procurement toward consolidated tenders that squeeze unit rates; Posti’s group revenue was around €1.5bn (2023) highlighting scale but margin sensitivity. Digitalization accelerates substitution away from physical mail, increasing buyer leverage, so Posti must expand value-added services (tracking, hybrid mail, digital archives) to defend margins.

SMBs and long-tail senders

Individually fragmented SMBs and long-tail senders are collectively meaningful—SMBs represent 99.8% of Finnish enterprises (Eurostat). Standard tariff schedules constrain individual bargaining power, while price-comparison tools increase transparency. Aggregators and marketplaces bundle volumes to secure better terms. Simple, predictable pricing helps retain loyalty.

Cross-border customers

Cross-border customers exert strong bargaining power as international sellers shift lanes to global integrators; Posti faces pressure to match global network coverage and pricing. Customs handling and returns complexity let buyers demand bundled end-to-end solutions and service-level credits. Currency volatility and item-level surcharges are explicitly scrutinized in 2024 RFPs, and reliability on cross-border transit times remains a primary leverage point.

- Global integrator switch pressure

- Demand for bundled customs + returns

- 2024 RFPs focus on currency/surcharges

- Transit-time reliability as key lever

End-consumers’ delivery preferences

End-consumers shape Posti indirectly through retailer channel choices: omnichannel merchants increasingly select carriers that meet fast, low-cost and low-emissions delivery goals, squeezing margins on parcel volumes.

Locker and OOH network breadth has become a formal buying criterion for retailers and consumers, with locker share rising notably in Nordic markets and shifting volume away from doorstep delivery.

Poor last-mile experience accelerates negative selection as dissatisfied customers and merchants migrate to competitors, raising churn and cost-to-serve for Posti.

- retailer-driven demand

- margin pressure: speed + price + sustainability

- locker/OOH = procurement criterion

- bad last-mile → customer churn

Shippers, govt contracts raise bargaining power; letters down 10% y/y

Major e-commerce shippers and government contracts wield high bargaining power—letter volumes fell c.10% y/y, while Posti group revenue was ~€1.5bn (2023), amplifying price sensitivity. SMBs (99.8% of Finnish firms) lack individual leverage but aggregate demand; cross-border sellers push for bundled customs/returns and transit-time guarantees, increasing margin pressure.

| Metric | Value | Impact |

|---|---|---|

| Letter volumes | -10% y/y (2024) | Price pressure |

| Revenue | €1.5bn (2023) | Scale vs margin |

| SMB share | 99.8% (Eurostat) | Aggregate demand |

Preview the Actual Deliverable

Posti Group Oyj Porter's Five Forces Analysis

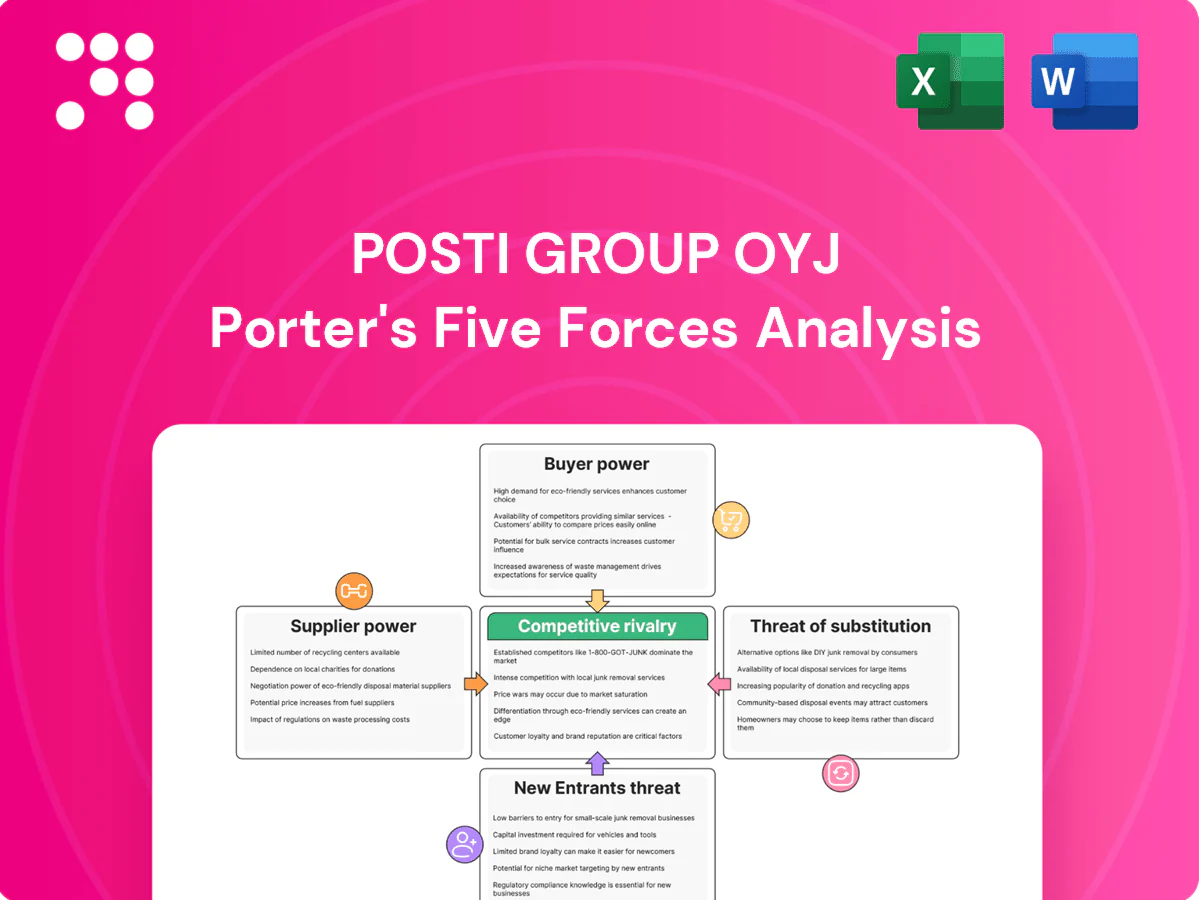

The Porter's Five Forces analysis of Posti Group Oyj evaluates supplier power, buyer power, competitive rivalry, threat of substitutes and new entrants, highlighting logistics regulation, network scale advantages and digital disruption pressures. It identifies strategic implications and mitigation options for Posti’s mail, parcel and logistics segments. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Go Beyond the Preview—Access the Full Strategic Report

Posti Group Oyj faces moderate buyer power and low supplier leverage thanks to scale and integrated logistics, while regulatory barriers and capital intensity limit new entrants; digital substitutes and parcel disruptors, however, raise strategic pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Posti Group Oyj’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel and energy dependence

Diesel and electricity costs materially affect Posti’s linehaul and sorting economics; Brent crude averaged about $85/bbl in 2024 and EU industrial electricity prices were near €0.15/kWh, which can shift margins quickly and give fuel suppliers leverage. Hedging reduces volatility but could not fully neutralize 2024 price swings. Transition to EVs and biofuels diversifies fuel sources but increases dependency on charging and biofuel supply infrastructure.

Vehicle and equipment OEMs

Vehicle and equipment OEMs are concentrated: the top three truck OEMs account for roughly 70% of the EU heavy truck market (2023–24), with van markets likewise dominated by a few players. Long lead times of 6–12 months and bespoke specs give suppliers leverage over price and service terms. Multi-sourcing and framework contracts mitigate exposure, but high switching costs and maintenance contracts—often ~10–15% of lifecycle spend—lock in supplier power.

IT, data, and platform vendors

Posti depends on routing, TMS/WMS, cybersecurity and cloud vendors, tying critical operations to a few providers; Posti reported ~€1.7bn revenue in 2023, making vendor outages or license shifts material to margins and service levels. Vendor lock-in and integration complexity raise switching costs and can delay remediation; strategic partnerships and modular architectures have reduced supplier power in logistics by enabling phased migration and alternative suppliers.

Labor and subcontracted carriers

Unionized Posti workforce and a wide subcontractor carrier network are critical supplier inputs; collective wage agreements and driver availability directly affect unit cost and operational flexibility. Tight Finnish labor markets in 2024 have strengthened contractor bargaining power, raising spot rates and limiting rapid capacity scaling. Automation lowers routine labor needs but peak-season volumes still rely heavily on external fleets, keeping supplier leverage high.

- Labor centrality

- Wage agreements drive costs

- Driver scarcity increases supplier power

- Automation reduces but does not eliminate peak reliance

Real estate and infrastructure

Supplier leverage: fuel & power costs and concentrated OEMs ~70%, 6–12m

Suppliers exert high leverage: fuel (Brent ~$85/bbl, EU power ~€0.15/kWh in 2024) and concentrated OEMs (top‑3 trucks ~70% market) drive input cost volatility and switching costs. IT, maintenance (10–15% lifecycle) and scarce urban sites (Greater Helsinki ~1.5M) increase dependency; lead times 6–12 months limit agility. Posti scale (€1.7bn rev 2023) makes vendor disruptions material.

| Input | 2024/2023 |

|---|---|

| Brent crude | $85/bbl (2024) |

| EU electricity | €0.15/kWh (2024) |

| Top‑3 truck OEMs | ~70% EU market |

| Posti revenue | €1.7bn (2023) |

| Lead times | 6–12 months |

What is included in the product

Tailored exclusively for Posti Group Oyj, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, supplier power, and market entry risks affecting postal and logistics operations, while identifying disruptive substitutes and regulatory dynamics that shape pricing, profitability, and strategic positioning.

A clear, one-sheet summary of Posti Group Oyj's five forces—quickly highlights competitive, regulatory and digital-disruption pressures to speed decision-making. Swap in your own data and scenario tabs to test pre/post regulation or new entrants without macros, ideal for board decks.

Customers Bargaining Power

Large e-commerce shippers

Large e-commerce shippers in 2024 negotiate steep volume discounts and leverage dual-sourcing with DHL, PostNord and DB Schenker to extract better rates from Posti. High SLAs on speed and returns raise service-level expectations and operational cost pressure. Performance lapses during peak seasons increase churn risk as major retailers can switch carriers rapidly. This concentration amplifies buyer bargaining power against Posti.

Public sector and enterprise mailers

Government and large billers exert strong price pressure as letter volumes have declined c.10% year-on-year, pushing procurement toward consolidated tenders that squeeze unit rates; Posti’s group revenue was around €1.5bn (2023) highlighting scale but margin sensitivity. Digitalization accelerates substitution away from physical mail, increasing buyer leverage, so Posti must expand value-added services (tracking, hybrid mail, digital archives) to defend margins.

SMBs and long-tail senders

Individually fragmented SMBs and long-tail senders are collectively meaningful—SMBs represent 99.8% of Finnish enterprises (Eurostat). Standard tariff schedules constrain individual bargaining power, while price-comparison tools increase transparency. Aggregators and marketplaces bundle volumes to secure better terms. Simple, predictable pricing helps retain loyalty.

Cross-border customers

Cross-border customers exert strong bargaining power as international sellers shift lanes to global integrators; Posti faces pressure to match global network coverage and pricing. Customs handling and returns complexity let buyers demand bundled end-to-end solutions and service-level credits. Currency volatility and item-level surcharges are explicitly scrutinized in 2024 RFPs, and reliability on cross-border transit times remains a primary leverage point.

- Global integrator switch pressure

- Demand for bundled customs + returns

- 2024 RFPs focus on currency/surcharges

- Transit-time reliability as key lever

End-consumers’ delivery preferences

End-consumers shape Posti indirectly through retailer channel choices: omnichannel merchants increasingly select carriers that meet fast, low-cost and low-emissions delivery goals, squeezing margins on parcel volumes.

Locker and OOH network breadth has become a formal buying criterion for retailers and consumers, with locker share rising notably in Nordic markets and shifting volume away from doorstep delivery.

Poor last-mile experience accelerates negative selection as dissatisfied customers and merchants migrate to competitors, raising churn and cost-to-serve for Posti.

- retailer-driven demand

- margin pressure: speed + price + sustainability

- locker/OOH = procurement criterion

- bad last-mile → customer churn

Shippers, govt contracts raise bargaining power; letters down 10% y/y

Major e-commerce shippers and government contracts wield high bargaining power—letter volumes fell c.10% y/y, while Posti group revenue was ~€1.5bn (2023), amplifying price sensitivity. SMBs (99.8% of Finnish firms) lack individual leverage but aggregate demand; cross-border sellers push for bundled customs/returns and transit-time guarantees, increasing margin pressure.

| Metric | Value | Impact |

|---|---|---|

| Letter volumes | -10% y/y (2024) | Price pressure |

| Revenue | €1.5bn (2023) | Scale vs margin |

| SMB share | 99.8% (Eurostat) | Aggregate demand |

Preview the Actual Deliverable

Posti Group Oyj Porter's Five Forces Analysis

The Porter's Five Forces analysis of Posti Group Oyj evaluates supplier power, buyer power, competitive rivalry, threat of substitutes and new entrants, highlighting logistics regulation, network scale advantages and digital disruption pressures. It identifies strategic implications and mitigation options for Posti’s mail, parcel and logistics segments. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Posti Group Oyj faces moderate buyer power and low supplier leverage thanks to scale and integrated logistics, while regulatory barriers and capital intensity limit new entrants; digital substitutes and parcel disruptors, however, raise strategic pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Posti Group Oyj’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel and energy dependence

Diesel and electricity costs materially affect Posti’s linehaul and sorting economics; Brent crude averaged about $85/bbl in 2024 and EU industrial electricity prices were near €0.15/kWh, which can shift margins quickly and give fuel suppliers leverage. Hedging reduces volatility but could not fully neutralize 2024 price swings. Transition to EVs and biofuels diversifies fuel sources but increases dependency on charging and biofuel supply infrastructure.

Vehicle and equipment OEMs

Vehicle and equipment OEMs are concentrated: the top three truck OEMs account for roughly 70% of the EU heavy truck market (2023–24), with van markets likewise dominated by a few players. Long lead times of 6–12 months and bespoke specs give suppliers leverage over price and service terms. Multi-sourcing and framework contracts mitigate exposure, but high switching costs and maintenance contracts—often ~10–15% of lifecycle spend—lock in supplier power.

IT, data, and platform vendors

Posti depends on routing, TMS/WMS, cybersecurity and cloud vendors, tying critical operations to a few providers; Posti reported ~€1.7bn revenue in 2023, making vendor outages or license shifts material to margins and service levels. Vendor lock-in and integration complexity raise switching costs and can delay remediation; strategic partnerships and modular architectures have reduced supplier power in logistics by enabling phased migration and alternative suppliers.

Labor and subcontracted carriers

Unionized Posti workforce and a wide subcontractor carrier network are critical supplier inputs; collective wage agreements and driver availability directly affect unit cost and operational flexibility. Tight Finnish labor markets in 2024 have strengthened contractor bargaining power, raising spot rates and limiting rapid capacity scaling. Automation lowers routine labor needs but peak-season volumes still rely heavily on external fleets, keeping supplier leverage high.

- Labor centrality

- Wage agreements drive costs

- Driver scarcity increases supplier power

- Automation reduces but does not eliminate peak reliance

Real estate and infrastructure

Supplier leverage: fuel & power costs and concentrated OEMs ~70%, 6–12m

Suppliers exert high leverage: fuel (Brent ~$85/bbl, EU power ~€0.15/kWh in 2024) and concentrated OEMs (top‑3 trucks ~70% market) drive input cost volatility and switching costs. IT, maintenance (10–15% lifecycle) and scarce urban sites (Greater Helsinki ~1.5M) increase dependency; lead times 6–12 months limit agility. Posti scale (€1.7bn rev 2023) makes vendor disruptions material.

| Input | 2024/2023 |

|---|---|

| Brent crude | $85/bbl (2024) |

| EU electricity | €0.15/kWh (2024) |

| Top‑3 truck OEMs | ~70% EU market |

| Posti revenue | €1.7bn (2023) |

| Lead times | 6–12 months |

What is included in the product

Tailored exclusively for Posti Group Oyj, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, supplier power, and market entry risks affecting postal and logistics operations, while identifying disruptive substitutes and regulatory dynamics that shape pricing, profitability, and strategic positioning.

A clear, one-sheet summary of Posti Group Oyj's five forces—quickly highlights competitive, regulatory and digital-disruption pressures to speed decision-making. Swap in your own data and scenario tabs to test pre/post regulation or new entrants without macros, ideal for board decks.

Customers Bargaining Power

Large e-commerce shippers

Large e-commerce shippers in 2024 negotiate steep volume discounts and leverage dual-sourcing with DHL, PostNord and DB Schenker to extract better rates from Posti. High SLAs on speed and returns raise service-level expectations and operational cost pressure. Performance lapses during peak seasons increase churn risk as major retailers can switch carriers rapidly. This concentration amplifies buyer bargaining power against Posti.

Public sector and enterprise mailers

Government and large billers exert strong price pressure as letter volumes have declined c.10% year-on-year, pushing procurement toward consolidated tenders that squeeze unit rates; Posti’s group revenue was around €1.5bn (2023) highlighting scale but margin sensitivity. Digitalization accelerates substitution away from physical mail, increasing buyer leverage, so Posti must expand value-added services (tracking, hybrid mail, digital archives) to defend margins.

SMBs and long-tail senders

Individually fragmented SMBs and long-tail senders are collectively meaningful—SMBs represent 99.8% of Finnish enterprises (Eurostat). Standard tariff schedules constrain individual bargaining power, while price-comparison tools increase transparency. Aggregators and marketplaces bundle volumes to secure better terms. Simple, predictable pricing helps retain loyalty.

Cross-border customers

Cross-border customers exert strong bargaining power as international sellers shift lanes to global integrators; Posti faces pressure to match global network coverage and pricing. Customs handling and returns complexity let buyers demand bundled end-to-end solutions and service-level credits. Currency volatility and item-level surcharges are explicitly scrutinized in 2024 RFPs, and reliability on cross-border transit times remains a primary leverage point.

- Global integrator switch pressure

- Demand for bundled customs + returns

- 2024 RFPs focus on currency/surcharges

- Transit-time reliability as key lever

End-consumers’ delivery preferences

End-consumers shape Posti indirectly through retailer channel choices: omnichannel merchants increasingly select carriers that meet fast, low-cost and low-emissions delivery goals, squeezing margins on parcel volumes.

Locker and OOH network breadth has become a formal buying criterion for retailers and consumers, with locker share rising notably in Nordic markets and shifting volume away from doorstep delivery.

Poor last-mile experience accelerates negative selection as dissatisfied customers and merchants migrate to competitors, raising churn and cost-to-serve for Posti.

- retailer-driven demand

- margin pressure: speed + price + sustainability

- locker/OOH = procurement criterion

- bad last-mile → customer churn

Shippers, govt contracts raise bargaining power; letters down 10% y/y

Major e-commerce shippers and government contracts wield high bargaining power—letter volumes fell c.10% y/y, while Posti group revenue was ~€1.5bn (2023), amplifying price sensitivity. SMBs (99.8% of Finnish firms) lack individual leverage but aggregate demand; cross-border sellers push for bundled customs/returns and transit-time guarantees, increasing margin pressure.

| Metric | Value | Impact |

|---|---|---|

| Letter volumes | -10% y/y (2024) | Price pressure |

| Revenue | €1.5bn (2023) | Scale vs margin |

| SMB share | 99.8% (Eurostat) | Aggregate demand |

Preview the Actual Deliverable

Posti Group Oyj Porter's Five Forces Analysis

The Porter's Five Forces analysis of Posti Group Oyj evaluates supplier power, buyer power, competitive rivalry, threat of substitutes and new entrants, highlighting logistics regulation, network scale advantages and digital disruption pressures. It identifies strategic implications and mitigation options for Posti’s mail, parcel and logistics segments. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.