Pou Chen Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

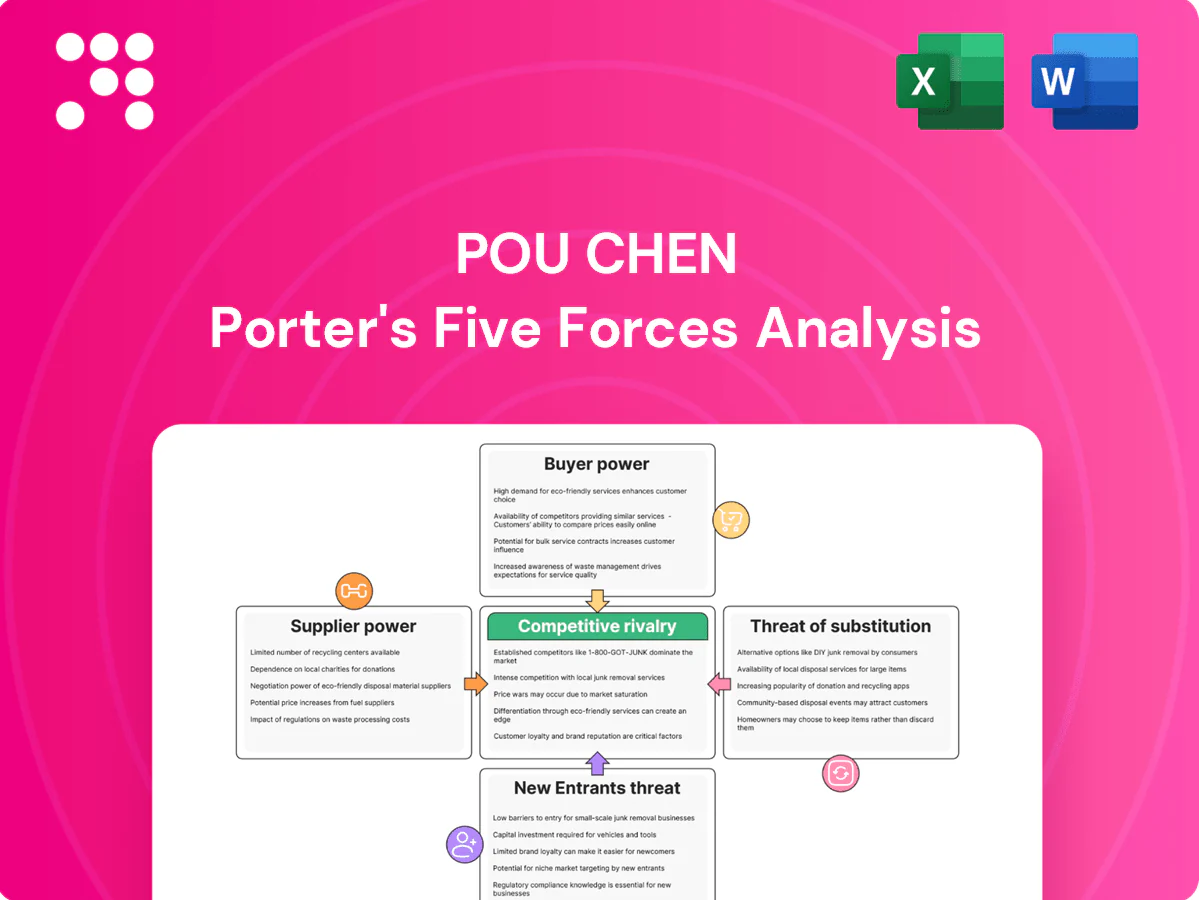

Pou Chen faces moderate supplier leverage, intense buyer pressure from global brands, and niche substitute risks as contract manufacturing evolves, while entry barriers stay elevated by scale and expertise. This snapshot teases strategic tensions and market levers shaping Pou Chen’s competitiveness. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Global raw materials concentration

In 2024 core inputs such as rubber, EVA, PU, technical foams, textiles and adhesives remain sourced from a relatively concentrated set of chemical and material suppliers, increasing supplier bargaining power during shortages or price spikes. Pou Chen’s scale supports multi-sourcing and long-term contracts that mitigate disruption and price exposure. Specialty compounds and certified sustainable inputs continue to command premiums, constraining margin flexibility. Supplier concentration therefore remains a material procurement risk.

Scale-based negotiation leverage

Pou Chen’s unmatched volumes—about 200 million pairs produced and consolidated revenue ~TWD 60bn in 2023—give pricing leverage and priority allocation with major brands like Nike and adidas. Aggregating demand across brands strengthens its position in annual tenders, improving fill rates and contract wins. Vendor-managed inventory and multi-year framework agreements stabilize unit costs and working capital. Leverage eases when global demand spikes or port/logistics bottlenecks tighten.

Compliance and ESG requirements

Brand-mandated ESG, traceability and chemical rules shrink the qualified supplier pool; EU CSRD rollout in 2024 extends sustainability reporting to about 50,000 companies, raising downstream scope 3 expectations. Fewer compliant suppliers can extract better terms and pass through costs. Pou Chen’s long-standing compliance systems and audits reduce switching frictions and broaden eligible partners. Rapidly evolving standards (ISSB/CSRD and tightening PFAS rules) can re-concentrate supplier power.

Geopolitical and logistics exposure

- 5–8% FX volatility (2024 YTD)

- Container rates 40–60% below 2021 peaks (2024)

- Chemicals/resins: persistent chokepoint risk

Process technology and tooling

Advanced molding, automated component feeders and specialized adhesive systems come from a small set of OEMs, giving suppliers leverage in niche tooling and consumables for Pou Chen.

Pou Chen mitigates this by running competitive vendor sourcing and retaining in-house process engineering, but proprietary machinery and fast innovation cycles sustain supplier clout for critical steps.

- Supplier concentration: niche OEMs dominate

- Lock-in: proprietary consumables raise switching costs

- Mitigation: vendor competition + in-house know-how

- Risk: rapid tech cycles keep supplier bargaining power

Supplier power up in 2024: chemical/OEM concentration, premium inputs, resin chokepoints

Supplier power is elevated in 2024 due to concentrated chemical and OEM suppliers, premium sustainable inputs and resin chokepoints despite Pou Chen scale (≈200m pairs, ~TWD60bn revenue 2023). Multi-year contracts, multi-sourcing and in-house engineering mitigate risks, but 5–8% FX swings and volatile logistics keep leverage with key suppliers.

| Metric | 2024 |

|---|---|

| Output | ≈200m pairs |

| Revenue (2023) | ~TWD60bn |

| FX volatility YTD | 5–8% |

| Container rates vs 2021 | -40–60% |

What is included in the product

Comprehensive Porter's Five Forces analysis for Pou Chen that identifies competitive drivers, supplier and buyer power, threat of entrants and substitutes, and strategic levers to defend market share and profitability.

One-sheet Pou Chen Porter's Five Forces that instantly reveals competitive pressure with a clear radar chart and customizable scores for fast, board-ready decisions. No macros, easy swaps for your data, and slide-ready layout to quickly relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated global brand customers

Major global sportswear brands place multi-year orders often worth millions of pairs annually and continuously benchmark suppliers, giving them strong price and term leverage in 2024. Allocation of model award volumes is highly competitive as buyers shift volumes among vendors to optimize cost and lead time. Pou Chen’s scale and breadth across 60+ factories and long-standing relationships with clients like Nike and adidas help it retain wallet share despite pricing pressure.

Switching across OEMs and geographies

Brands use dual-source models and can shift volumes across countries, reducing dependence on any single manufacturer; Pou Chen, as the world’s largest athletic footwear OEM with facilities across China, Vietnam, Indonesia and Cambodia, mitigates this via a multi-country footprint and standardized ramp-up playbooks.

Tooling, quality validation and compliance create switching frictions—certifications and production validation cycles typically take months—so while customers can reallocate volumes, operational and regulatory hurdles make switching time-consuming but not insurmountable.

Design complexity and co-development

Pou Chen’s ODM capabilities and early DFM involvement embed the company deeper into customers’ product cycles, increasing stickiness and enabling value-based pricing; as of 2024 Pou Chen remains the world’s largest footwear manufacturer, operating over 70 plants and roughly 200,000 employees. Advanced specs force tighter SLAs and higher penalties, raising operational risk and margin sensitivity. Co-investment in molds and automation further raises mutual switching costs and locks customers into longer contracts.

Lead time, flexibility, and on-time delivery

Buyers push for shorter cycles, frequent drops and responsive replenishment, making OTIF performance, MOQ flexibility and rapid sample iterations key levers of bargaining power; Pou Chen’s scale, digitalization and near-line automation enhance responsiveness but any OTIF miss risks immediate reallocation to rivals.

- OTIF focus

- MOQ flexibility

- Rapid samples

- Scale + digital automation

- Misses → reallocation

Cost transparency and open-book requests

- Buyer demands: open-book costing and index-linked contracts

- Margin impact: efficiency gains captured by buyers

- Pou Chen defense: process innovation and yield improvement

- Negotiation dynamic: annual price-downs keep buyer power high

Large supplier scale curbs but cannot erase buyer leverage over global footwear contracts

Major brands exert high bargaining power via multi-year, multi-million-pair contracts and annual price-downs; buyers reallocate volumes rapidly to optimize cost and lead time. Pou Chen's >70 plants and ~200,000 employees in 2024, global footprint across China, Vietnam, Indonesia, Cambodia, and ODM capabilities reduce but do not eliminate buyer leverage. OTIF, MOQ flexibility and co-invested tooling raise switching frictions yet misses prompt reallocation.

| Factor | Evidence | 2024 metric |

|---|---|---|

| Scale | Global plants, workforce | >70 plants; ~200,000 employees |

| Order size | Buyer contracts | Multi-million pairs annually |

| Key levers | OTIF, MOQ, tooling | OTIF critical; tooling co-investment |

What You See Is What You Get

Pou Chen Porter's Five Forces Analysis

This preview is the actual Pou Chen Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It contains the full, professionally formatted five‑forces assessment tailored to Pou Chen, ready for download and use. What you see is what you get.

A Must-Have Tool for Decision-Makers

Pou Chen faces moderate supplier leverage, intense buyer pressure from global brands, and niche substitute risks as contract manufacturing evolves, while entry barriers stay elevated by scale and expertise. This snapshot teases strategic tensions and market levers shaping Pou Chen’s competitiveness. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Global raw materials concentration

In 2024 core inputs such as rubber, EVA, PU, technical foams, textiles and adhesives remain sourced from a relatively concentrated set of chemical and material suppliers, increasing supplier bargaining power during shortages or price spikes. Pou Chen’s scale supports multi-sourcing and long-term contracts that mitigate disruption and price exposure. Specialty compounds and certified sustainable inputs continue to command premiums, constraining margin flexibility. Supplier concentration therefore remains a material procurement risk.

Scale-based negotiation leverage

Pou Chen’s unmatched volumes—about 200 million pairs produced and consolidated revenue ~TWD 60bn in 2023—give pricing leverage and priority allocation with major brands like Nike and adidas. Aggregating demand across brands strengthens its position in annual tenders, improving fill rates and contract wins. Vendor-managed inventory and multi-year framework agreements stabilize unit costs and working capital. Leverage eases when global demand spikes or port/logistics bottlenecks tighten.

Compliance and ESG requirements

Brand-mandated ESG, traceability and chemical rules shrink the qualified supplier pool; EU CSRD rollout in 2024 extends sustainability reporting to about 50,000 companies, raising downstream scope 3 expectations. Fewer compliant suppliers can extract better terms and pass through costs. Pou Chen’s long-standing compliance systems and audits reduce switching frictions and broaden eligible partners. Rapidly evolving standards (ISSB/CSRD and tightening PFAS rules) can re-concentrate supplier power.

Geopolitical and logistics exposure

- 5–8% FX volatility (2024 YTD)

- Container rates 40–60% below 2021 peaks (2024)

- Chemicals/resins: persistent chokepoint risk

Process technology and tooling

Advanced molding, automated component feeders and specialized adhesive systems come from a small set of OEMs, giving suppliers leverage in niche tooling and consumables for Pou Chen.

Pou Chen mitigates this by running competitive vendor sourcing and retaining in-house process engineering, but proprietary machinery and fast innovation cycles sustain supplier clout for critical steps.

- Supplier concentration: niche OEMs dominate

- Lock-in: proprietary consumables raise switching costs

- Mitigation: vendor competition + in-house know-how

- Risk: rapid tech cycles keep supplier bargaining power

Supplier power up in 2024: chemical/OEM concentration, premium inputs, resin chokepoints

Supplier power is elevated in 2024 due to concentrated chemical and OEM suppliers, premium sustainable inputs and resin chokepoints despite Pou Chen scale (≈200m pairs, ~TWD60bn revenue 2023). Multi-year contracts, multi-sourcing and in-house engineering mitigate risks, but 5–8% FX swings and volatile logistics keep leverage with key suppliers.

| Metric | 2024 |

|---|---|

| Output | ≈200m pairs |

| Revenue (2023) | ~TWD60bn |

| FX volatility YTD | 5–8% |

| Container rates vs 2021 | -40–60% |

What is included in the product

Comprehensive Porter's Five Forces analysis for Pou Chen that identifies competitive drivers, supplier and buyer power, threat of entrants and substitutes, and strategic levers to defend market share and profitability.

One-sheet Pou Chen Porter's Five Forces that instantly reveals competitive pressure with a clear radar chart and customizable scores for fast, board-ready decisions. No macros, easy swaps for your data, and slide-ready layout to quickly relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated global brand customers

Major global sportswear brands place multi-year orders often worth millions of pairs annually and continuously benchmark suppliers, giving them strong price and term leverage in 2024. Allocation of model award volumes is highly competitive as buyers shift volumes among vendors to optimize cost and lead time. Pou Chen’s scale and breadth across 60+ factories and long-standing relationships with clients like Nike and adidas help it retain wallet share despite pricing pressure.

Switching across OEMs and geographies

Brands use dual-source models and can shift volumes across countries, reducing dependence on any single manufacturer; Pou Chen, as the world’s largest athletic footwear OEM with facilities across China, Vietnam, Indonesia and Cambodia, mitigates this via a multi-country footprint and standardized ramp-up playbooks.

Tooling, quality validation and compliance create switching frictions—certifications and production validation cycles typically take months—so while customers can reallocate volumes, operational and regulatory hurdles make switching time-consuming but not insurmountable.

Design complexity and co-development

Pou Chen’s ODM capabilities and early DFM involvement embed the company deeper into customers’ product cycles, increasing stickiness and enabling value-based pricing; as of 2024 Pou Chen remains the world’s largest footwear manufacturer, operating over 70 plants and roughly 200,000 employees. Advanced specs force tighter SLAs and higher penalties, raising operational risk and margin sensitivity. Co-investment in molds and automation further raises mutual switching costs and locks customers into longer contracts.

Lead time, flexibility, and on-time delivery

Buyers push for shorter cycles, frequent drops and responsive replenishment, making OTIF performance, MOQ flexibility and rapid sample iterations key levers of bargaining power; Pou Chen’s scale, digitalization and near-line automation enhance responsiveness but any OTIF miss risks immediate reallocation to rivals.

- OTIF focus

- MOQ flexibility

- Rapid samples

- Scale + digital automation

- Misses → reallocation

Cost transparency and open-book requests

- Buyer demands: open-book costing and index-linked contracts

- Margin impact: efficiency gains captured by buyers

- Pou Chen defense: process innovation and yield improvement

- Negotiation dynamic: annual price-downs keep buyer power high

Large supplier scale curbs but cannot erase buyer leverage over global footwear contracts

Major brands exert high bargaining power via multi-year, multi-million-pair contracts and annual price-downs; buyers reallocate volumes rapidly to optimize cost and lead time. Pou Chen's >70 plants and ~200,000 employees in 2024, global footprint across China, Vietnam, Indonesia, Cambodia, and ODM capabilities reduce but do not eliminate buyer leverage. OTIF, MOQ flexibility and co-invested tooling raise switching frictions yet misses prompt reallocation.

| Factor | Evidence | 2024 metric |

|---|---|---|

| Scale | Global plants, workforce | >70 plants; ~200,000 employees |

| Order size | Buyer contracts | Multi-million pairs annually |

| Key levers | OTIF, MOQ, tooling | OTIF critical; tooling co-investment |

What You See Is What You Get

Pou Chen Porter's Five Forces Analysis

This preview is the actual Pou Chen Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It contains the full, professionally formatted five‑forces assessment tailored to Pou Chen, ready for download and use. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Pou Chen faces moderate supplier leverage, intense buyer pressure from global brands, and niche substitute risks as contract manufacturing evolves, while entry barriers stay elevated by scale and expertise. This snapshot teases strategic tensions and market levers shaping Pou Chen’s competitiveness. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Global raw materials concentration

In 2024 core inputs such as rubber, EVA, PU, technical foams, textiles and adhesives remain sourced from a relatively concentrated set of chemical and material suppliers, increasing supplier bargaining power during shortages or price spikes. Pou Chen’s scale supports multi-sourcing and long-term contracts that mitigate disruption and price exposure. Specialty compounds and certified sustainable inputs continue to command premiums, constraining margin flexibility. Supplier concentration therefore remains a material procurement risk.

Scale-based negotiation leverage

Pou Chen’s unmatched volumes—about 200 million pairs produced and consolidated revenue ~TWD 60bn in 2023—give pricing leverage and priority allocation with major brands like Nike and adidas. Aggregating demand across brands strengthens its position in annual tenders, improving fill rates and contract wins. Vendor-managed inventory and multi-year framework agreements stabilize unit costs and working capital. Leverage eases when global demand spikes or port/logistics bottlenecks tighten.

Compliance and ESG requirements

Brand-mandated ESG, traceability and chemical rules shrink the qualified supplier pool; EU CSRD rollout in 2024 extends sustainability reporting to about 50,000 companies, raising downstream scope 3 expectations. Fewer compliant suppliers can extract better terms and pass through costs. Pou Chen’s long-standing compliance systems and audits reduce switching frictions and broaden eligible partners. Rapidly evolving standards (ISSB/CSRD and tightening PFAS rules) can re-concentrate supplier power.

Geopolitical and logistics exposure

- 5–8% FX volatility (2024 YTD)

- Container rates 40–60% below 2021 peaks (2024)

- Chemicals/resins: persistent chokepoint risk

Process technology and tooling

Advanced molding, automated component feeders and specialized adhesive systems come from a small set of OEMs, giving suppliers leverage in niche tooling and consumables for Pou Chen.

Pou Chen mitigates this by running competitive vendor sourcing and retaining in-house process engineering, but proprietary machinery and fast innovation cycles sustain supplier clout for critical steps.

- Supplier concentration: niche OEMs dominate

- Lock-in: proprietary consumables raise switching costs

- Mitigation: vendor competition + in-house know-how

- Risk: rapid tech cycles keep supplier bargaining power

Supplier power up in 2024: chemical/OEM concentration, premium inputs, resin chokepoints

Supplier power is elevated in 2024 due to concentrated chemical and OEM suppliers, premium sustainable inputs and resin chokepoints despite Pou Chen scale (≈200m pairs, ~TWD60bn revenue 2023). Multi-year contracts, multi-sourcing and in-house engineering mitigate risks, but 5–8% FX swings and volatile logistics keep leverage with key suppliers.

| Metric | 2024 |

|---|---|

| Output | ≈200m pairs |

| Revenue (2023) | ~TWD60bn |

| FX volatility YTD | 5–8% |

| Container rates vs 2021 | -40–60% |

What is included in the product

Comprehensive Porter's Five Forces analysis for Pou Chen that identifies competitive drivers, supplier and buyer power, threat of entrants and substitutes, and strategic levers to defend market share and profitability.

One-sheet Pou Chen Porter's Five Forces that instantly reveals competitive pressure with a clear radar chart and customizable scores for fast, board-ready decisions. No macros, easy swaps for your data, and slide-ready layout to quickly relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated global brand customers

Major global sportswear brands place multi-year orders often worth millions of pairs annually and continuously benchmark suppliers, giving them strong price and term leverage in 2024. Allocation of model award volumes is highly competitive as buyers shift volumes among vendors to optimize cost and lead time. Pou Chen’s scale and breadth across 60+ factories and long-standing relationships with clients like Nike and adidas help it retain wallet share despite pricing pressure.

Switching across OEMs and geographies

Brands use dual-source models and can shift volumes across countries, reducing dependence on any single manufacturer; Pou Chen, as the world’s largest athletic footwear OEM with facilities across China, Vietnam, Indonesia and Cambodia, mitigates this via a multi-country footprint and standardized ramp-up playbooks.

Tooling, quality validation and compliance create switching frictions—certifications and production validation cycles typically take months—so while customers can reallocate volumes, operational and regulatory hurdles make switching time-consuming but not insurmountable.

Design complexity and co-development

Pou Chen’s ODM capabilities and early DFM involvement embed the company deeper into customers’ product cycles, increasing stickiness and enabling value-based pricing; as of 2024 Pou Chen remains the world’s largest footwear manufacturer, operating over 70 plants and roughly 200,000 employees. Advanced specs force tighter SLAs and higher penalties, raising operational risk and margin sensitivity. Co-investment in molds and automation further raises mutual switching costs and locks customers into longer contracts.

Lead time, flexibility, and on-time delivery

Buyers push for shorter cycles, frequent drops and responsive replenishment, making OTIF performance, MOQ flexibility and rapid sample iterations key levers of bargaining power; Pou Chen’s scale, digitalization and near-line automation enhance responsiveness but any OTIF miss risks immediate reallocation to rivals.

- OTIF focus

- MOQ flexibility

- Rapid samples

- Scale + digital automation

- Misses → reallocation

Cost transparency and open-book requests

- Buyer demands: open-book costing and index-linked contracts

- Margin impact: efficiency gains captured by buyers

- Pou Chen defense: process innovation and yield improvement

- Negotiation dynamic: annual price-downs keep buyer power high

Large supplier scale curbs but cannot erase buyer leverage over global footwear contracts

Major brands exert high bargaining power via multi-year, multi-million-pair contracts and annual price-downs; buyers reallocate volumes rapidly to optimize cost and lead time. Pou Chen's >70 plants and ~200,000 employees in 2024, global footprint across China, Vietnam, Indonesia, Cambodia, and ODM capabilities reduce but do not eliminate buyer leverage. OTIF, MOQ flexibility and co-invested tooling raise switching frictions yet misses prompt reallocation.

| Factor | Evidence | 2024 metric |

|---|---|---|

| Scale | Global plants, workforce | >70 plants; ~200,000 employees |

| Order size | Buyer contracts | Multi-million pairs annually |

| Key levers | OTIF, MOQ, tooling | OTIF critical; tooling co-investment |

What You See Is What You Get

Pou Chen Porter's Five Forces Analysis

This preview is the actual Pou Chen Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It contains the full, professionally formatted five‑forces assessment tailored to Pou Chen, ready for download and use. What you see is what you get.