Powell SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Explore Powell's strategic position with our concise SWOT snapshot — uncover core strengths, competitive risks, and untapped growth levers in three clear sections. Want the full story and actionable recommendations? Purchase the complete SWOT analysis for a research-backed, editable Word and Excel package designed for investors, strategists, and advisors. Make informed decisions with a professional, ready-to-use report.

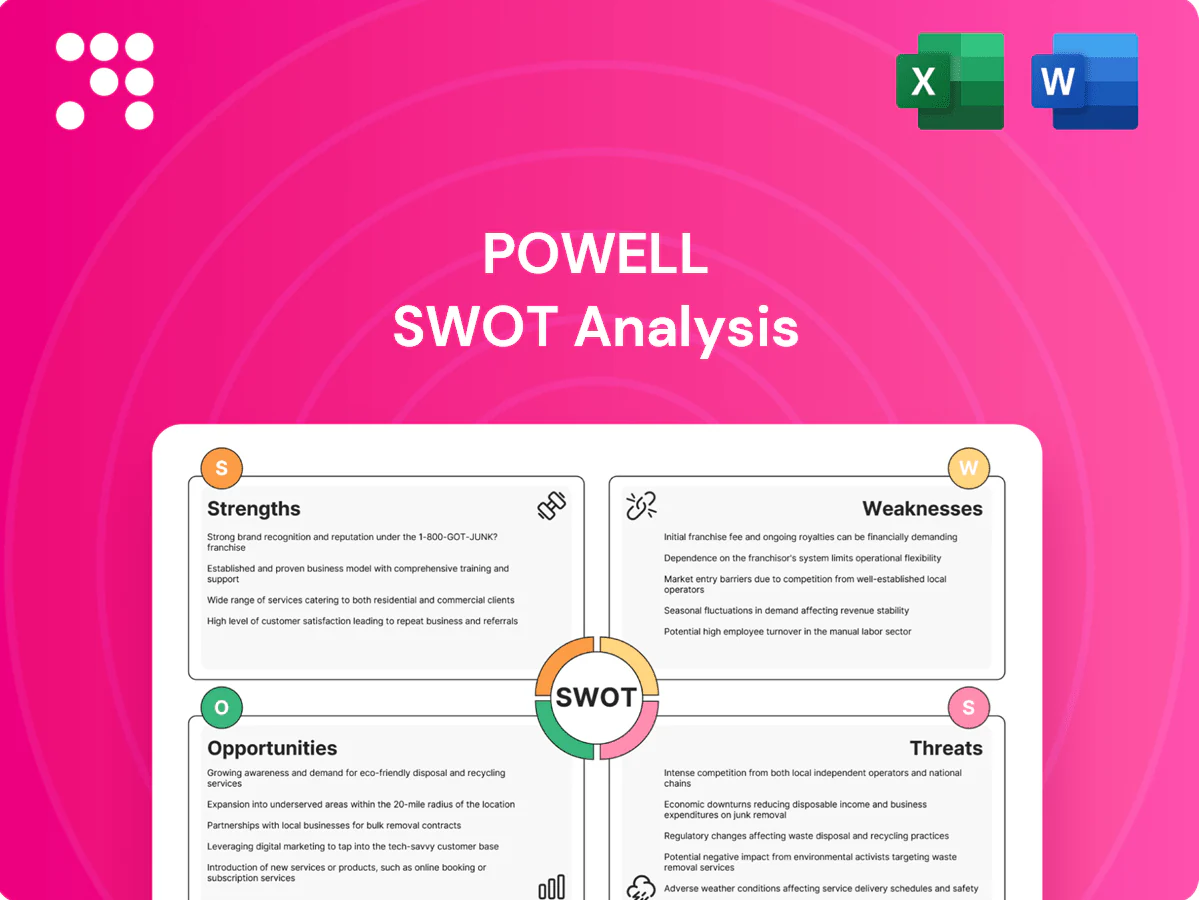

Strengths

Custom-engineered power solutions

Powell Industries (POWL) specializes in tailor-made electrical equipment for complex, mission-critical environments, leveraging engineering depth to differentiate from standard catalog offerings. This specialization supports premium pricing—historically capturing roughly a 15–20% margin advantage—and tight customer integration, contributing to Powell’s FY2024 revenue of about $446 million. Customized solutions raise switching costs and strengthen client retention.

Diversified heavy-industry customer base

Serving oil and gas, refining, petrochemical, power generation, and transportation spreads demand across multiple verticals, reducing reliance on a single end market and stabilizing revenue streams.

Integrated portfolio from substations to breakers

Offering substations, switchgear, circuit breakers and monitoring systems creates a one-stop solution that simplifies vendor management and centralizes system-level accountability. Integrated product lines improve interoperability and operational reliability across assets. This vertical scope positions Powell to capture larger EPC project packages and increase share-of-wallet on grid modernization contracts.

Critical safety and reliability positioning

Powell’s products are essential to safe, continuous operations in harsh industrial settings, positioning the company as mission-critical and elevating perceived value and demand resilience.

Strong compliance and reliability track records—demonstrated through certifications and long-serving client relationships—build trust and support durable contracts and aftermarket revenue.

This safety-first reputation sustains long-term relationships, driving repeat business and higher customer retention rates.

- mission-critical positioning

- high trust from compliance/reliability

- repeat business and retention

Lifecycle services and support

Lifecycle services and support extend engagement beyond initial capex by delivering recurring service, maintenance, and upgrade contracts that stabilize revenue and improve margin mix; field service work shifts spend from one-time sales to higher-margin aftermarket income. Field data from the installed base feeds product improvements and firmware updates, embedding operational know-how that raises switching costs and strengthens barriers to entry.

Engineering-led switchgear yields premium pricing, 15-20% margin edge and ~$446M FY2024 revenue

Powell Industries’ engineering-led, customized switchgear and substation solutions enable premium pricing and strong retention—supporting a roughly 15–20% margin advantage and FY2024 revenue near $446 million—across diversified end markets (oil & gas, refining, petrochemical, power, transportation). Certifications, lifecycle services and installed-base telemetry drive recurring aftermarket revenue and high switching costs.

| Metric | Value |

|---|---|

| FY2024 revenue | ~$446M |

| Margin advantage | 15–20% |

| Core end markets | Oil & gas, refining, petrochemical, power, transportation |

What is included in the product

Provides a concise SWOT analysis of Powell, outlining internal strengths and weaknesses alongside external opportunities and threats to assess its strategic position and future risks.

Powell SWOT Analysis delivers a concise, visual matrix that speeds strategic alignment and eases stakeholder communication for rapid decision-making.

Weaknesses

Exposure to capex cycles

Demand is tightly linked to industrial capital spending, making revenue sensitive to cyclical swings; oil and gas or heavy-industry downturns commonly delay or cancel large projects, narrowing revenue visibility in weak macro conditions and increasing forecasting and capacity-planning risk.

Project complexity and execution risk

Project-based, custom work exposes Powell to schedule, scope and cost overrun risks—industry studies show about 70% of large engineering projects face delays and median cost overruns near 30% as of 2024. Late-stage design changes can compress margins materially, with unit margins shrinking by double-digit percentage points on disrupted projects. Warranty and performance guarantees create added liability pools that can hit cash flow in year 1–2 post-delivery. Robust project controls and change management are required to preserve profitability and limit exposure.

Supply chain and lead-time sensitivity

Custom builds rely on specialized components with lead times often ranging 12–52 weeks; disruptions in switchgear, breakers, steel or semiconductors have pushed delivery slippage rates above 20% in recent project cycles. Expediting freight and premium sourcing can raise procurement costs by 5–15%, squeezing margins, while customer liquidated damages commonly apply (typically 1–3% of contract value per missed milestone).

Limited scale versus global conglomerates

Compared with very large OEMs, Powell Industries (NASDAQ: POWL) operates at far smaller scale—2024 revenue about $520M versus Siemens' ~€67B—weakening purchasing power and R&D breadth. Limited global service footprint yields thinner after-sales coverage in regions where mega-projects require 24/7 support. This scale gap can constrain competitive bidding on billion-dollar infrastructure contracts.

- Smaller revenue base vs global rivals

- Weaker procurement leverage

- Narrower R&D investment

- Thinner global service coverage

Geographic concentration risk

Geographic concentration leaves Powell vulnerable: if revenues are concentrated in North America, regional downturns can heavily reduce top-line performance. A limited international footprint constrains diversification and growth channels. Local regulatory shifts can have outsized operational and compliance costs, while currency upside is muted without broader global exposure.

- Concentration: North America dependency

- Diversification: limited international reach

- Regulatory: outsized local impact

- FX: reduced currency benefits

Cyclical capex, project overruns and North America concentration reduce revenue visibility

Demand is cyclical and tied to industrial capex, reducing revenue visibility in downturns. Project-based work exposes Powell to schedule/scope overruns—about 70% of large projects face delays and median cost overruns ~30% (2024). Limited scale and North America concentration (2024 revenue ~$520M) weakens procurement, R&D and global service reach.

| Metric | Value (2024) |

|---|---|

| Revenue | $520M |

| Project delay rate | ~70% |

| Median cost overrun | ~30% |

What You See Is What You Get

Powell SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You're viewing a live preview of the real, editable file and the complete document becomes available after checkout.

Dive Deeper Into the Company’s Strategic Blueprint

Explore Powell's strategic position with our concise SWOT snapshot — uncover core strengths, competitive risks, and untapped growth levers in three clear sections. Want the full story and actionable recommendations? Purchase the complete SWOT analysis for a research-backed, editable Word and Excel package designed for investors, strategists, and advisors. Make informed decisions with a professional, ready-to-use report.

Strengths

Custom-engineered power solutions

Powell Industries (POWL) specializes in tailor-made electrical equipment for complex, mission-critical environments, leveraging engineering depth to differentiate from standard catalog offerings. This specialization supports premium pricing—historically capturing roughly a 15–20% margin advantage—and tight customer integration, contributing to Powell’s FY2024 revenue of about $446 million. Customized solutions raise switching costs and strengthen client retention.

Diversified heavy-industry customer base

Serving oil and gas, refining, petrochemical, power generation, and transportation spreads demand across multiple verticals, reducing reliance on a single end market and stabilizing revenue streams.

Integrated portfolio from substations to breakers

Offering substations, switchgear, circuit breakers and monitoring systems creates a one-stop solution that simplifies vendor management and centralizes system-level accountability. Integrated product lines improve interoperability and operational reliability across assets. This vertical scope positions Powell to capture larger EPC project packages and increase share-of-wallet on grid modernization contracts.

Critical safety and reliability positioning

Powell’s products are essential to safe, continuous operations in harsh industrial settings, positioning the company as mission-critical and elevating perceived value and demand resilience.

Strong compliance and reliability track records—demonstrated through certifications and long-serving client relationships—build trust and support durable contracts and aftermarket revenue.

This safety-first reputation sustains long-term relationships, driving repeat business and higher customer retention rates.

- mission-critical positioning

- high trust from compliance/reliability

- repeat business and retention

Lifecycle services and support

Lifecycle services and support extend engagement beyond initial capex by delivering recurring service, maintenance, and upgrade contracts that stabilize revenue and improve margin mix; field service work shifts spend from one-time sales to higher-margin aftermarket income. Field data from the installed base feeds product improvements and firmware updates, embedding operational know-how that raises switching costs and strengthens barriers to entry.

Engineering-led switchgear yields premium pricing, 15-20% margin edge and ~$446M FY2024 revenue

Powell Industries’ engineering-led, customized switchgear and substation solutions enable premium pricing and strong retention—supporting a roughly 15–20% margin advantage and FY2024 revenue near $446 million—across diversified end markets (oil & gas, refining, petrochemical, power, transportation). Certifications, lifecycle services and installed-base telemetry drive recurring aftermarket revenue and high switching costs.

| Metric | Value |

|---|---|

| FY2024 revenue | ~$446M |

| Margin advantage | 15–20% |

| Core end markets | Oil & gas, refining, petrochemical, power, transportation |

What is included in the product

Provides a concise SWOT analysis of Powell, outlining internal strengths and weaknesses alongside external opportunities and threats to assess its strategic position and future risks.

Powell SWOT Analysis delivers a concise, visual matrix that speeds strategic alignment and eases stakeholder communication for rapid decision-making.

Weaknesses

Exposure to capex cycles

Demand is tightly linked to industrial capital spending, making revenue sensitive to cyclical swings; oil and gas or heavy-industry downturns commonly delay or cancel large projects, narrowing revenue visibility in weak macro conditions and increasing forecasting and capacity-planning risk.

Project complexity and execution risk

Project-based, custom work exposes Powell to schedule, scope and cost overrun risks—industry studies show about 70% of large engineering projects face delays and median cost overruns near 30% as of 2024. Late-stage design changes can compress margins materially, with unit margins shrinking by double-digit percentage points on disrupted projects. Warranty and performance guarantees create added liability pools that can hit cash flow in year 1–2 post-delivery. Robust project controls and change management are required to preserve profitability and limit exposure.

Supply chain and lead-time sensitivity

Custom builds rely on specialized components with lead times often ranging 12–52 weeks; disruptions in switchgear, breakers, steel or semiconductors have pushed delivery slippage rates above 20% in recent project cycles. Expediting freight and premium sourcing can raise procurement costs by 5–15%, squeezing margins, while customer liquidated damages commonly apply (typically 1–3% of contract value per missed milestone).

Limited scale versus global conglomerates

Compared with very large OEMs, Powell Industries (NASDAQ: POWL) operates at far smaller scale—2024 revenue about $520M versus Siemens' ~€67B—weakening purchasing power and R&D breadth. Limited global service footprint yields thinner after-sales coverage in regions where mega-projects require 24/7 support. This scale gap can constrain competitive bidding on billion-dollar infrastructure contracts.

- Smaller revenue base vs global rivals

- Weaker procurement leverage

- Narrower R&D investment

- Thinner global service coverage

Geographic concentration risk

Geographic concentration leaves Powell vulnerable: if revenues are concentrated in North America, regional downturns can heavily reduce top-line performance. A limited international footprint constrains diversification and growth channels. Local regulatory shifts can have outsized operational and compliance costs, while currency upside is muted without broader global exposure.

- Concentration: North America dependency

- Diversification: limited international reach

- Regulatory: outsized local impact

- FX: reduced currency benefits

Cyclical capex, project overruns and North America concentration reduce revenue visibility

Demand is cyclical and tied to industrial capex, reducing revenue visibility in downturns. Project-based work exposes Powell to schedule/scope overruns—about 70% of large projects face delays and median cost overruns ~30% (2024). Limited scale and North America concentration (2024 revenue ~$520M) weakens procurement, R&D and global service reach.

| Metric | Value (2024) |

|---|---|

| Revenue | $520M |

| Project delay rate | ~70% |

| Median cost overrun | ~30% |

What You See Is What You Get

Powell SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You're viewing a live preview of the real, editable file and the complete document becomes available after checkout.

Description

Dive Deeper Into the Company’s Strategic Blueprint

Explore Powell's strategic position with our concise SWOT snapshot — uncover core strengths, competitive risks, and untapped growth levers in three clear sections. Want the full story and actionable recommendations? Purchase the complete SWOT analysis for a research-backed, editable Word and Excel package designed for investors, strategists, and advisors. Make informed decisions with a professional, ready-to-use report.

Strengths

Custom-engineered power solutions

Powell Industries (POWL) specializes in tailor-made electrical equipment for complex, mission-critical environments, leveraging engineering depth to differentiate from standard catalog offerings. This specialization supports premium pricing—historically capturing roughly a 15–20% margin advantage—and tight customer integration, contributing to Powell’s FY2024 revenue of about $446 million. Customized solutions raise switching costs and strengthen client retention.

Diversified heavy-industry customer base

Serving oil and gas, refining, petrochemical, power generation, and transportation spreads demand across multiple verticals, reducing reliance on a single end market and stabilizing revenue streams.

Integrated portfolio from substations to breakers

Offering substations, switchgear, circuit breakers and monitoring systems creates a one-stop solution that simplifies vendor management and centralizes system-level accountability. Integrated product lines improve interoperability and operational reliability across assets. This vertical scope positions Powell to capture larger EPC project packages and increase share-of-wallet on grid modernization contracts.

Critical safety and reliability positioning

Powell’s products are essential to safe, continuous operations in harsh industrial settings, positioning the company as mission-critical and elevating perceived value and demand resilience.

Strong compliance and reliability track records—demonstrated through certifications and long-serving client relationships—build trust and support durable contracts and aftermarket revenue.

This safety-first reputation sustains long-term relationships, driving repeat business and higher customer retention rates.

- mission-critical positioning

- high trust from compliance/reliability

- repeat business and retention

Lifecycle services and support

Lifecycle services and support extend engagement beyond initial capex by delivering recurring service, maintenance, and upgrade contracts that stabilize revenue and improve margin mix; field service work shifts spend from one-time sales to higher-margin aftermarket income. Field data from the installed base feeds product improvements and firmware updates, embedding operational know-how that raises switching costs and strengthens barriers to entry.

Engineering-led switchgear yields premium pricing, 15-20% margin edge and ~$446M FY2024 revenue

Powell Industries’ engineering-led, customized switchgear and substation solutions enable premium pricing and strong retention—supporting a roughly 15–20% margin advantage and FY2024 revenue near $446 million—across diversified end markets (oil & gas, refining, petrochemical, power, transportation). Certifications, lifecycle services and installed-base telemetry drive recurring aftermarket revenue and high switching costs.

| Metric | Value |

|---|---|

| FY2024 revenue | ~$446M |

| Margin advantage | 15–20% |

| Core end markets | Oil & gas, refining, petrochemical, power, transportation |

What is included in the product

Provides a concise SWOT analysis of Powell, outlining internal strengths and weaknesses alongside external opportunities and threats to assess its strategic position and future risks.

Powell SWOT Analysis delivers a concise, visual matrix that speeds strategic alignment and eases stakeholder communication for rapid decision-making.

Weaknesses

Exposure to capex cycles

Demand is tightly linked to industrial capital spending, making revenue sensitive to cyclical swings; oil and gas or heavy-industry downturns commonly delay or cancel large projects, narrowing revenue visibility in weak macro conditions and increasing forecasting and capacity-planning risk.

Project complexity and execution risk

Project-based, custom work exposes Powell to schedule, scope and cost overrun risks—industry studies show about 70% of large engineering projects face delays and median cost overruns near 30% as of 2024. Late-stage design changes can compress margins materially, with unit margins shrinking by double-digit percentage points on disrupted projects. Warranty and performance guarantees create added liability pools that can hit cash flow in year 1–2 post-delivery. Robust project controls and change management are required to preserve profitability and limit exposure.

Supply chain and lead-time sensitivity

Custom builds rely on specialized components with lead times often ranging 12–52 weeks; disruptions in switchgear, breakers, steel or semiconductors have pushed delivery slippage rates above 20% in recent project cycles. Expediting freight and premium sourcing can raise procurement costs by 5–15%, squeezing margins, while customer liquidated damages commonly apply (typically 1–3% of contract value per missed milestone).

Limited scale versus global conglomerates

Compared with very large OEMs, Powell Industries (NASDAQ: POWL) operates at far smaller scale—2024 revenue about $520M versus Siemens' ~€67B—weakening purchasing power and R&D breadth. Limited global service footprint yields thinner after-sales coverage in regions where mega-projects require 24/7 support. This scale gap can constrain competitive bidding on billion-dollar infrastructure contracts.

- Smaller revenue base vs global rivals

- Weaker procurement leverage

- Narrower R&D investment

- Thinner global service coverage

Geographic concentration risk

Geographic concentration leaves Powell vulnerable: if revenues are concentrated in North America, regional downturns can heavily reduce top-line performance. A limited international footprint constrains diversification and growth channels. Local regulatory shifts can have outsized operational and compliance costs, while currency upside is muted without broader global exposure.

- Concentration: North America dependency

- Diversification: limited international reach

- Regulatory: outsized local impact

- FX: reduced currency benefits

Cyclical capex, project overruns and North America concentration reduce revenue visibility

Demand is cyclical and tied to industrial capex, reducing revenue visibility in downturns. Project-based work exposes Powell to schedule/scope overruns—about 70% of large projects face delays and median cost overruns ~30% (2024). Limited scale and North America concentration (2024 revenue ~$520M) weakens procurement, R&D and global service reach.

| Metric | Value (2024) |

|---|---|

| Revenue | $520M |

| Project delay rate | ~70% |

| Median cost overrun | ~30% |

What You See Is What You Get

Powell SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You're viewing a live preview of the real, editable file and the complete document becomes available after checkout.