PPHC PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

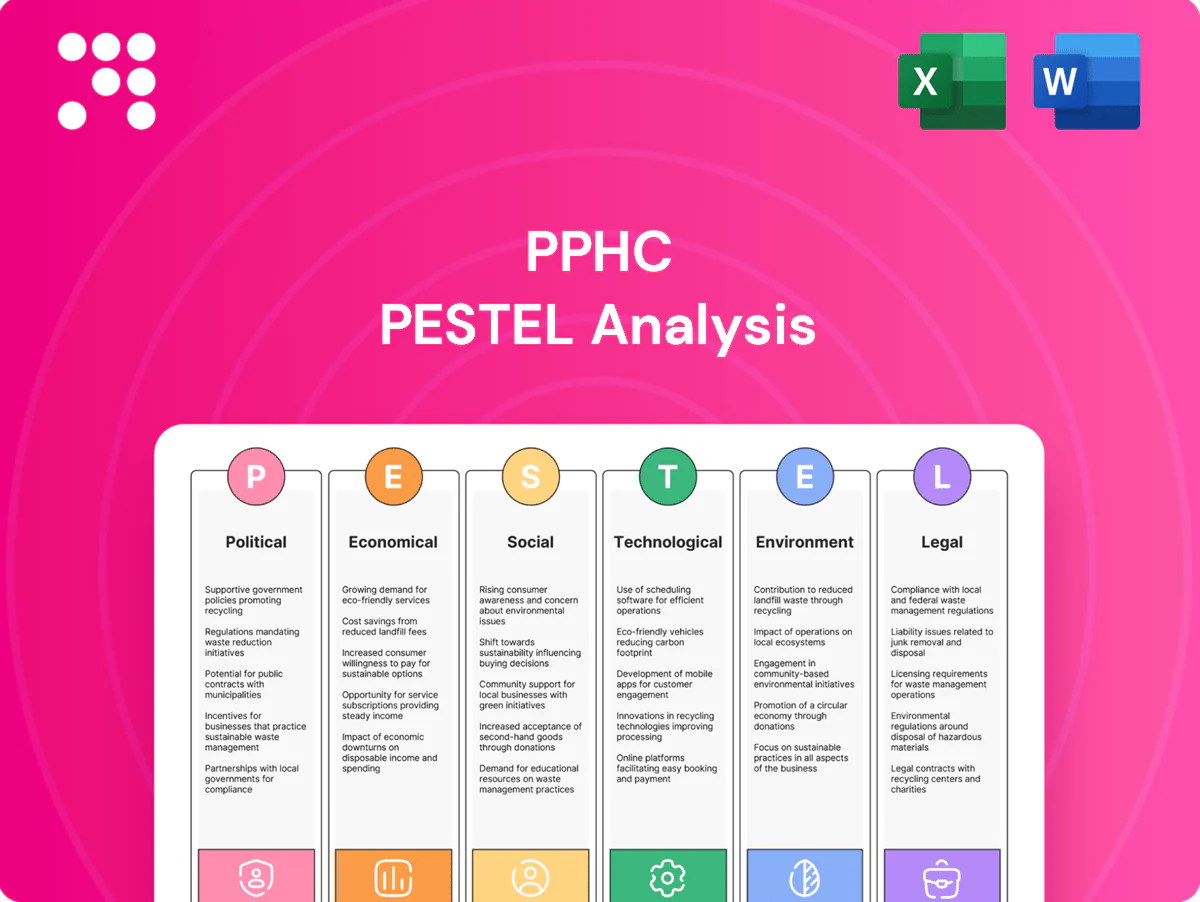

Gain a strategic edge with our PPHC PESTLE Analysis—concise, expert-reviewed insight into political, economic, social, technological, legal and environmental forces shaping PPHC. Use these findings to anticipate risks, spot growth opportunities and refine your investment or strategic plan. Purchase the full analysis to download the complete, editable report and actionable intelligence instantly.

Political factors

Policy volatility and partisanship

Polarized legislatures drive rapid swings in policy priorities that increase client exposure and PPHC workload, as partisan agendas accelerate agenda changes across federal and state levels. Gridlock slows legislative wins but heightens demand for defensive advocacy and rapid regulatory workarounds. Shifts in roughly 36 standing committee chairs across Congress reset access maps and messaging. Scenario planning across party-control outcomes becomes a core service.

Election cycle sensitivity

Elections reallocate power, staff, and agendas, creating measurable spikes in demand before and after votes, notably following the Nov 5, 2024 US elections. Transition periods require rapid relationship mapping and onboarding of roughly 1,200 presidentially appointed, Senate-confirmed decision‑makers. Campaign narratives from 2024 reshape client perceptions of regulatory risk. PPHC must time advocacy to pre‑rulemaking windows and lame‑duck sessions.

Federal–state interplay

When federal action stalls, policy increasingly advances at state and municipal levels, with about 50 states and roughly 19,000 local governments shaping regulation and raising multi-jurisdiction coordination complexity and spend. Preemption battles across states alter compliance burdens for national clients and can force duplicate reporting systems. PPHC benefits from a federated footprint and localized stakeholder networks that reduce rollout time and regulatory risk.

Geopolitics and national security lens

Administrative rulemaking dynamics

Executive agencies drive policy via guidance, rules, and enforcement priorities; OMB review can last up to 90 days and public comment periods typically run 30–60 days, making those windows critical influence points. Litigation risk regularly forces narrower rule language and delayed implementation. PPHC’s early intelligence and coalition submissions increase visibility and influence during rule drafting and OMB review.

- OMB review: up to 90 days

- Comment windows: 30–60 days

- Agencies issue thousands of guidance documents yearly

- Early submissions raise agency responsiveness

Polarized Congress, post-2024 churn: 36 chair shifts, 1,200 PAS, $52B CHIPS

Polarized Congress and post-2024 transitions surge demand for advocacy; ~36 committee chair changes and ~1,200 PAS nominees reset access. State/local rulemaking (50 states, ~19k local govts) raises compliance costs. Geopolitics and CHIPS $52B plus OMB/agency windows (OMB ≤90d; comments 30–60d) force rapid, localized engagement.

| Metric | Value |

|---|---|

| Committee shifts | ~36 |

| PAS nominees | ~1,200 |

| Local govts | ~19,000 |

| CHIPS / OMB | $52B / ≤90d |

What is included in the product

Explores how macro-environmental factors uniquely affect PPHC across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, region- and industry-specific insights to inform executives, investors and strategists, highlight risks/opportunities, and support scenario planning and pitch-ready reporting.

Condenses PPHC’s full PESTLE into a clear, visually segmented summary for quick meetings or presentations, and includes editable notes so teams can localize risks, opportunities, and action items for rapid alignment.

Economic factors

Budget cycles and client spend

Corporate and association advocacy budgets track revenue cycles and cost pressures—US lobbying spend was about $3.9B in 2023 (OpenSecrets) while FY2024 federal discretionary appropriations totaled roughly $1.7T, shaping grant-linked advocacy. Fiscal tightening pushes clients to high-ROI, targeted campaigns; PPHC must flex delivery and pricing to preserve utilization during downturns.

Interest rates and investment flows

Interest rate levels steer capital toward or away from regulated sectors; with global FDI at $1.02 trillion in 2023 (UNCTAD), higher costs of capital raise scrutiny on policy-dependent projects and shift advocacy needs. Infrastructure and industrial policy can offset private pullbacks by crowding in finance. PPHC maps policy wins to client financing milestones to preserve deal viability.

Sector mix and regulatory intensity

Heavily regulated industries like healthcare and energy drive recurring retainer work and stable cashflows, while emerging sectors seek foundational policy frameworks that create new advisory demand. Shifts in healthcare, tech, energy and fintech cycles rebalance PPHC’s portfolio as clean energy investment rose to about 1.7 trillion USD in 2023. PPHC hedges risk through cross-sector diversification to smooth cyclical exposure.

M&A and consolidation

Consolidation often reduces client counts while enlarging mandates as buyers rationalize vendor rosters; Refinitiv reported global M&A deal value of about $2.8 trillion in 2024, underscoring scale opportunities for larger mandates. Integration periods heighten demand for unified policy narratives and change-management advisory. Rising antitrust scrutiny from US and EU authorities increases need for specialized regulatory advisory, enabling PPHC to cross-sell services across combined entities.

- Consolidation: fewer clients, larger mandates

- 2024 global M&A ~2.8 trillion (Refinitiv)

- Integration: unified policy narratives needed

- Antitrust: higher demand for regulatory advisory

- Opportunity: cross-selling across merged entities

Pricing power and utilization

Outcome visibility and strategic depth supported premium fees, with many advisory firms commanding 15–20% higher rates in 2024–25; blended teams and tech leverage improved gross margins by about 2–3 percentage points. Fixed-fee projects require tight scope control to protect profitability, and PPHC aligns staffing to peak legislative calendars to lift utilization roughly 8–10% seasonally.

- Premium fees: 15–20%

- Margin uplift: +2–3 ppt

- Fixed-fee risk: scope control critical

- Utilization boost: +8–10% at peak

Polarized Congress, post-2024 churn: 36 chair shifts, 1,200 PAS, $52B CHIPS

Economic pressures—tight fiscal envelopes, higher rates and shifting FDI flows—force PPHC to prioritize high-ROI, targeted advocacy while flexing pricing and delivery to protect utilization. Sector regulation and consolidation drive steady retainers and larger mandates, with 2024 M&A ~2.8T supporting cross-sell opportunities and antitrust advisory. Premium fees (15–20%) and margin uplifts (+2–3 ppt) reward outcome-led work and tight scope control.

| Metric | Value |

|---|---|

| US lobbying (2023) | ~3.9B |

| FY2024 discretionary | ~1.7T |

| Global FDI (2023) | ~1.02T |

| Clean energy invest (2023) | ~1.7T |

| Global M&A (2024) | ~2.8T |

| Advisory premium (24–25) | 15–20% |

Same Document Delivered

PPHC PESTLE Analysis

The PPHC PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal, and environmental factors affecting PPHC, highlighting key risks and strategic opportunities. The content and structure shown in the preview is the same document you’ll download after payment. It’s fully formatted and ready to use for strategic planning or investor briefings.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our PPHC PESTLE Analysis—concise, expert-reviewed insight into political, economic, social, technological, legal and environmental forces shaping PPHC. Use these findings to anticipate risks, spot growth opportunities and refine your investment or strategic plan. Purchase the full analysis to download the complete, editable report and actionable intelligence instantly.

Political factors

Policy volatility and partisanship

Polarized legislatures drive rapid swings in policy priorities that increase client exposure and PPHC workload, as partisan agendas accelerate agenda changes across federal and state levels. Gridlock slows legislative wins but heightens demand for defensive advocacy and rapid regulatory workarounds. Shifts in roughly 36 standing committee chairs across Congress reset access maps and messaging. Scenario planning across party-control outcomes becomes a core service.

Election cycle sensitivity

Elections reallocate power, staff, and agendas, creating measurable spikes in demand before and after votes, notably following the Nov 5, 2024 US elections. Transition periods require rapid relationship mapping and onboarding of roughly 1,200 presidentially appointed, Senate-confirmed decision‑makers. Campaign narratives from 2024 reshape client perceptions of regulatory risk. PPHC must time advocacy to pre‑rulemaking windows and lame‑duck sessions.

Federal–state interplay

When federal action stalls, policy increasingly advances at state and municipal levels, with about 50 states and roughly 19,000 local governments shaping regulation and raising multi-jurisdiction coordination complexity and spend. Preemption battles across states alter compliance burdens for national clients and can force duplicate reporting systems. PPHC benefits from a federated footprint and localized stakeholder networks that reduce rollout time and regulatory risk.

Geopolitics and national security lens

Administrative rulemaking dynamics

Executive agencies drive policy via guidance, rules, and enforcement priorities; OMB review can last up to 90 days and public comment periods typically run 30–60 days, making those windows critical influence points. Litigation risk regularly forces narrower rule language and delayed implementation. PPHC’s early intelligence and coalition submissions increase visibility and influence during rule drafting and OMB review.

- OMB review: up to 90 days

- Comment windows: 30–60 days

- Agencies issue thousands of guidance documents yearly

- Early submissions raise agency responsiveness

Polarized Congress, post-2024 churn: 36 chair shifts, 1,200 PAS, $52B CHIPS

Polarized Congress and post-2024 transitions surge demand for advocacy; ~36 committee chair changes and ~1,200 PAS nominees reset access. State/local rulemaking (50 states, ~19k local govts) raises compliance costs. Geopolitics and CHIPS $52B plus OMB/agency windows (OMB ≤90d; comments 30–60d) force rapid, localized engagement.

| Metric | Value |

|---|---|

| Committee shifts | ~36 |

| PAS nominees | ~1,200 |

| Local govts | ~19,000 |

| CHIPS / OMB | $52B / ≤90d |

What is included in the product

Explores how macro-environmental factors uniquely affect PPHC across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, region- and industry-specific insights to inform executives, investors and strategists, highlight risks/opportunities, and support scenario planning and pitch-ready reporting.

Condenses PPHC’s full PESTLE into a clear, visually segmented summary for quick meetings or presentations, and includes editable notes so teams can localize risks, opportunities, and action items for rapid alignment.

Economic factors

Budget cycles and client spend

Corporate and association advocacy budgets track revenue cycles and cost pressures—US lobbying spend was about $3.9B in 2023 (OpenSecrets) while FY2024 federal discretionary appropriations totaled roughly $1.7T, shaping grant-linked advocacy. Fiscal tightening pushes clients to high-ROI, targeted campaigns; PPHC must flex delivery and pricing to preserve utilization during downturns.

Interest rates and investment flows

Interest rate levels steer capital toward or away from regulated sectors; with global FDI at $1.02 trillion in 2023 (UNCTAD), higher costs of capital raise scrutiny on policy-dependent projects and shift advocacy needs. Infrastructure and industrial policy can offset private pullbacks by crowding in finance. PPHC maps policy wins to client financing milestones to preserve deal viability.

Sector mix and regulatory intensity

Heavily regulated industries like healthcare and energy drive recurring retainer work and stable cashflows, while emerging sectors seek foundational policy frameworks that create new advisory demand. Shifts in healthcare, tech, energy and fintech cycles rebalance PPHC’s portfolio as clean energy investment rose to about 1.7 trillion USD in 2023. PPHC hedges risk through cross-sector diversification to smooth cyclical exposure.

M&A and consolidation

Consolidation often reduces client counts while enlarging mandates as buyers rationalize vendor rosters; Refinitiv reported global M&A deal value of about $2.8 trillion in 2024, underscoring scale opportunities for larger mandates. Integration periods heighten demand for unified policy narratives and change-management advisory. Rising antitrust scrutiny from US and EU authorities increases need for specialized regulatory advisory, enabling PPHC to cross-sell services across combined entities.

- Consolidation: fewer clients, larger mandates

- 2024 global M&A ~2.8 trillion (Refinitiv)

- Integration: unified policy narratives needed

- Antitrust: higher demand for regulatory advisory

- Opportunity: cross-selling across merged entities

Pricing power and utilization

Outcome visibility and strategic depth supported premium fees, with many advisory firms commanding 15–20% higher rates in 2024–25; blended teams and tech leverage improved gross margins by about 2–3 percentage points. Fixed-fee projects require tight scope control to protect profitability, and PPHC aligns staffing to peak legislative calendars to lift utilization roughly 8–10% seasonally.

- Premium fees: 15–20%

- Margin uplift: +2–3 ppt

- Fixed-fee risk: scope control critical

- Utilization boost: +8–10% at peak

Polarized Congress, post-2024 churn: 36 chair shifts, 1,200 PAS, $52B CHIPS

Economic pressures—tight fiscal envelopes, higher rates and shifting FDI flows—force PPHC to prioritize high-ROI, targeted advocacy while flexing pricing and delivery to protect utilization. Sector regulation and consolidation drive steady retainers and larger mandates, with 2024 M&A ~2.8T supporting cross-sell opportunities and antitrust advisory. Premium fees (15–20%) and margin uplifts (+2–3 ppt) reward outcome-led work and tight scope control.

| Metric | Value |

|---|---|

| US lobbying (2023) | ~3.9B |

| FY2024 discretionary | ~1.7T |

| Global FDI (2023) | ~1.02T |

| Clean energy invest (2023) | ~1.7T |

| Global M&A (2024) | ~2.8T |

| Advisory premium (24–25) | 15–20% |

Same Document Delivered

PPHC PESTLE Analysis

The PPHC PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal, and environmental factors affecting PPHC, highlighting key risks and strategic opportunities. The content and structure shown in the preview is the same document you’ll download after payment. It’s fully formatted and ready to use for strategic planning or investor briefings.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our PPHC PESTLE Analysis—concise, expert-reviewed insight into political, economic, social, technological, legal and environmental forces shaping PPHC. Use these findings to anticipate risks, spot growth opportunities and refine your investment or strategic plan. Purchase the full analysis to download the complete, editable report and actionable intelligence instantly.

Political factors

Policy volatility and partisanship

Polarized legislatures drive rapid swings in policy priorities that increase client exposure and PPHC workload, as partisan agendas accelerate agenda changes across federal and state levels. Gridlock slows legislative wins but heightens demand for defensive advocacy and rapid regulatory workarounds. Shifts in roughly 36 standing committee chairs across Congress reset access maps and messaging. Scenario planning across party-control outcomes becomes a core service.

Election cycle sensitivity

Elections reallocate power, staff, and agendas, creating measurable spikes in demand before and after votes, notably following the Nov 5, 2024 US elections. Transition periods require rapid relationship mapping and onboarding of roughly 1,200 presidentially appointed, Senate-confirmed decision‑makers. Campaign narratives from 2024 reshape client perceptions of regulatory risk. PPHC must time advocacy to pre‑rulemaking windows and lame‑duck sessions.

Federal–state interplay

When federal action stalls, policy increasingly advances at state and municipal levels, with about 50 states and roughly 19,000 local governments shaping regulation and raising multi-jurisdiction coordination complexity and spend. Preemption battles across states alter compliance burdens for national clients and can force duplicate reporting systems. PPHC benefits from a federated footprint and localized stakeholder networks that reduce rollout time and regulatory risk.

Geopolitics and national security lens

Administrative rulemaking dynamics

Executive agencies drive policy via guidance, rules, and enforcement priorities; OMB review can last up to 90 days and public comment periods typically run 30–60 days, making those windows critical influence points. Litigation risk regularly forces narrower rule language and delayed implementation. PPHC’s early intelligence and coalition submissions increase visibility and influence during rule drafting and OMB review.

- OMB review: up to 90 days

- Comment windows: 30–60 days

- Agencies issue thousands of guidance documents yearly

- Early submissions raise agency responsiveness

Polarized Congress, post-2024 churn: 36 chair shifts, 1,200 PAS, $52B CHIPS

Polarized Congress and post-2024 transitions surge demand for advocacy; ~36 committee chair changes and ~1,200 PAS nominees reset access. State/local rulemaking (50 states, ~19k local govts) raises compliance costs. Geopolitics and CHIPS $52B plus OMB/agency windows (OMB ≤90d; comments 30–60d) force rapid, localized engagement.

| Metric | Value |

|---|---|

| Committee shifts | ~36 |

| PAS nominees | ~1,200 |

| Local govts | ~19,000 |

| CHIPS / OMB | $52B / ≤90d |

What is included in the product

Explores how macro-environmental factors uniquely affect PPHC across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, region- and industry-specific insights to inform executives, investors and strategists, highlight risks/opportunities, and support scenario planning and pitch-ready reporting.

Condenses PPHC’s full PESTLE into a clear, visually segmented summary for quick meetings or presentations, and includes editable notes so teams can localize risks, opportunities, and action items for rapid alignment.

Economic factors

Budget cycles and client spend

Corporate and association advocacy budgets track revenue cycles and cost pressures—US lobbying spend was about $3.9B in 2023 (OpenSecrets) while FY2024 federal discretionary appropriations totaled roughly $1.7T, shaping grant-linked advocacy. Fiscal tightening pushes clients to high-ROI, targeted campaigns; PPHC must flex delivery and pricing to preserve utilization during downturns.

Interest rates and investment flows

Interest rate levels steer capital toward or away from regulated sectors; with global FDI at $1.02 trillion in 2023 (UNCTAD), higher costs of capital raise scrutiny on policy-dependent projects and shift advocacy needs. Infrastructure and industrial policy can offset private pullbacks by crowding in finance. PPHC maps policy wins to client financing milestones to preserve deal viability.

Sector mix and regulatory intensity

Heavily regulated industries like healthcare and energy drive recurring retainer work and stable cashflows, while emerging sectors seek foundational policy frameworks that create new advisory demand. Shifts in healthcare, tech, energy and fintech cycles rebalance PPHC’s portfolio as clean energy investment rose to about 1.7 trillion USD in 2023. PPHC hedges risk through cross-sector diversification to smooth cyclical exposure.

M&A and consolidation

Consolidation often reduces client counts while enlarging mandates as buyers rationalize vendor rosters; Refinitiv reported global M&A deal value of about $2.8 trillion in 2024, underscoring scale opportunities for larger mandates. Integration periods heighten demand for unified policy narratives and change-management advisory. Rising antitrust scrutiny from US and EU authorities increases need for specialized regulatory advisory, enabling PPHC to cross-sell services across combined entities.

- Consolidation: fewer clients, larger mandates

- 2024 global M&A ~2.8 trillion (Refinitiv)

- Integration: unified policy narratives needed

- Antitrust: higher demand for regulatory advisory

- Opportunity: cross-selling across merged entities

Pricing power and utilization

Outcome visibility and strategic depth supported premium fees, with many advisory firms commanding 15–20% higher rates in 2024–25; blended teams and tech leverage improved gross margins by about 2–3 percentage points. Fixed-fee projects require tight scope control to protect profitability, and PPHC aligns staffing to peak legislative calendars to lift utilization roughly 8–10% seasonally.

- Premium fees: 15–20%

- Margin uplift: +2–3 ppt

- Fixed-fee risk: scope control critical

- Utilization boost: +8–10% at peak

Polarized Congress, post-2024 churn: 36 chair shifts, 1,200 PAS, $52B CHIPS

Economic pressures—tight fiscal envelopes, higher rates and shifting FDI flows—force PPHC to prioritize high-ROI, targeted advocacy while flexing pricing and delivery to protect utilization. Sector regulation and consolidation drive steady retainers and larger mandates, with 2024 M&A ~2.8T supporting cross-sell opportunities and antitrust advisory. Premium fees (15–20%) and margin uplifts (+2–3 ppt) reward outcome-led work and tight scope control.

| Metric | Value |

|---|---|

| US lobbying (2023) | ~3.9B |

| FY2024 discretionary | ~1.7T |

| Global FDI (2023) | ~1.02T |

| Clean energy invest (2023) | ~1.7T |

| Global M&A (2024) | ~2.8T |

| Advisory premium (24–25) | 15–20% |

Same Document Delivered

PPHC PESTLE Analysis

The PPHC PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal, and environmental factors affecting PPHC, highlighting key risks and strategic opportunities. The content and structure shown in the preview is the same document you’ll download after payment. It’s fully formatted and ready to use for strategic planning or investor briefings.