PREIT Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

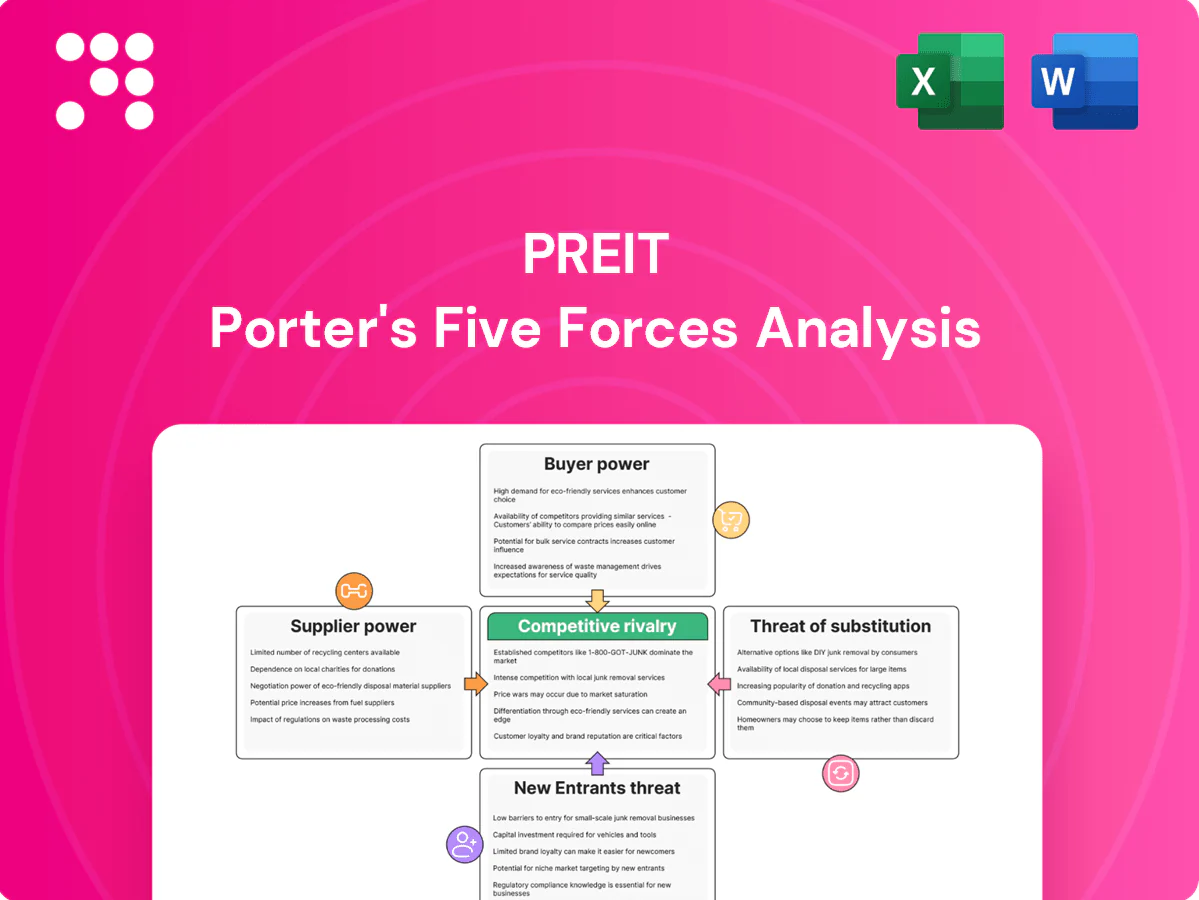

PREIT faces intense retail headwinds, shifting tenant mixes, and evolving consumer preferences that reshape mall profitability and leasing power. Competitive rivalry and buyer leverage remain high while barriers to new experiential retail entrants are moderate. Operational execution and property diversification are critical for resilience. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore PREIT’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated contractors

PREIT depends on specialized construction, renovation and maintenance firms that are regionally concentrated, with its mall portfolio of about 17 properties amplifying demand for limited qualified vendors.

When only a handful of contractors can execute large mall overhauls, bids and timelines rise — reports show regional contractors captured roughly 60% of major retail redevelopment projects in 2024, increasing costs and schedule risk.

That concentration raises switching costs and gives suppliers leverage during peak redevelopment cycles, though PREIT’s use of multiyear framework agreements and volume commitments in 2024 helped cap price escalation and secure capacity.

Utility dependence

Enclosed malls are energy-intensive, leaving PREIT dependent on local utility monopolies with few alternatives for electricity, water, and HVAC; demand charges, which often represent 20–40% of commercial bills, and 2024 regional rate hikes directly pressure operating margins. Efficiency projects reduce consumption but need significant upfront capital and coordination with utility providers for demand management and incentives.

Anchor tenant leverage

Anchor tenants act as quasi-suppliers for PREIT by driving the foot traffic that sustains in-line tenants; their departures in 2024 triggered co-tenancy clauses and materially reduced rent-roll stability, amplifying anchor negotiating power. PREIT has responded with rent concessions and capital allowances to retain or replace anchors. The scarcity of modern, experiential anchors further increases this leverage and raises repositioning costs.

Municipal gatekeepers

Local governments control entitlements, permits and tax incentives critical to repositioning malls; PREIT held 19 operating malls in 2024, making municipal decisions material to portfolio value. Lengthy approvals and community pushback can delay projects by months to years, effectively raising supplier power. PILOT agreements and zoning flexibility can alter project economics by millions annually; strong public-sector relationships reduce but do not eliminate this risk.

- Municipal control: entitlements, permits

- Delays: months–years, higher costs

- PILOT/zoning: millions impact

- Mitigation: public-sector relationships

Proptech and service vendors

Proptech and service vendors (leasing systems, foot-traffic analytics, security tech) became critical to PREIT by 2024, with a few specialist platforms commanding premium pricing and creating data lock-in that raises switching costs. Integration and customization typically require multi-month projects and significant IT spend, slowing vendor changes and affecting leasing velocity and operational efficiency.

- Data lock-in

- Six-figure integration costs

- Impacts leasing velocity

Suppliers wield elevated 2024 leverage amid contractor concentration and utility-driven costs

Suppliers hold elevated leverage over PREIT in 2024 due to concentrated regional contractors (≈60% share of major redevelopments), local utility monopolies driving demand charges (20–40% of bills), and scarce experiential anchor tenants increasing repositioning costs. PREIT’s multiyear frameworks and public-sector relationships partially mitigate price and schedule risk but do not eliminate supplier power.

| Metric | 2024 Value |

|---|---|

| Regional contractor share | ≈60% |

| Demand charges of commercial bills | 20–40% |

| Operating malls | 19 |

What is included in the product

Concise Porter's Five Forces analysis for PREIT that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its mall-focused portfolio.

A clear one-sheet PREIT Porter's Five Forces summary—perfect for quick mall-asset decisions; customizable pressure levels reflect rent trends, foot traffic, and retailer health. Includes an instant spider/radar chart and clean layout ready for decks or Excel dashboards.

Customers Bargaining Power

National tenant clout

National tenants, particularly large chains and creditworthy retailers, extract leverage with favorable base rents and TI packages, using brand draw and covenant quality to press PREIT (NYSE: PEI) for concessions in 2024. In key markets they secure below-market initial yields as PREIT prioritizes marquee names to drive traffic. Portfolio-level relationships allow PREIT to trade off higher rents for occupancy stability and renewal predictability.

Limited tenant pool

Retail consolidation and store rationalizations have shrunk the pool of viable tenants, with national mall vacancy rates near 10% in 2024, intensifying competition among landlords to fill space.

Fewer prospects raise tenant bargaining power as landlords bid down rents or offer TI and free-rent; specialty retailers increasingly secure concessions or shorter terms to limit exposure.

These pressures are amplified in secondary and tertiary trade areas where foot traffic and creditworthy tenants are scarcer.

Co-tenancy and kick-out rights

Lease co-tenancy and kick-out rights let tenants reduce rent or exit leases if anchors close or occupancy falls, sharply increasing customer bargaining power during disruptions. These clauses force PREIT to manage cascading effects from a single anchor failure, raising vacancy and revenue risk. Proactive backfilling, shorter-term leases, and mixed-use conversions can reduce activation of these clauses and stabilize cash flow.

Alternative location options

Tenants can relocate from PREIT malls to open-air centers, outlet districts or street retail with lower occupancy costs, increasing their leverage; PREIT’s Mid-Atlantic regional mall focus in 2024 intensifies this pressure. To retain tenants PREIT may match market concessions and flexible lease terms, while differentiated merchandising and upgraded amenities reduce direct comparability and weaken tenant bargaining power.

- Tenant options: open-air, outlets, street retail

- Leverage: higher with more location choice

- PREIT response: concessions, flexible leases

- Mitigation: unique merchandising, amenities

Price sensitivity and ROI focus

10% mall vacancy boosts tenant leverage, forcing rent concessions and TI

National, creditworthy tenants hold high leverage in 2024, extracting below-market base rents and TI to secure mall anchors, pressuring PREIT (PEI) for concessions. National mall vacancy ~10% in 2024 (ICSC), implying PREIT occupancy near 90–91% and stronger tenant negotiating power. Rent-to-sales targets ≈10% and demand for POS/footfall transparency amplify tenant bargaining.

| Metric | 2024 Value |

|---|---|

| National mall vacancy | ~10% |

| PREIT occupancy | ~90–91% |

| Retail rent-to-sales target | ~10% |

Preview Before You Purchase

PREIT Porter's Five Forces Analysis

This preview shows the exact PREIT Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted and ready for download and use. You’ll get instant access to this same professional, actionable assessment as the final deliverable.

A Must-Have Tool for Decision-Makers

PREIT faces intense retail headwinds, shifting tenant mixes, and evolving consumer preferences that reshape mall profitability and leasing power. Competitive rivalry and buyer leverage remain high while barriers to new experiential retail entrants are moderate. Operational execution and property diversification are critical for resilience. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore PREIT’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated contractors

PREIT depends on specialized construction, renovation and maintenance firms that are regionally concentrated, with its mall portfolio of about 17 properties amplifying demand for limited qualified vendors.

When only a handful of contractors can execute large mall overhauls, bids and timelines rise — reports show regional contractors captured roughly 60% of major retail redevelopment projects in 2024, increasing costs and schedule risk.

That concentration raises switching costs and gives suppliers leverage during peak redevelopment cycles, though PREIT’s use of multiyear framework agreements and volume commitments in 2024 helped cap price escalation and secure capacity.

Utility dependence

Enclosed malls are energy-intensive, leaving PREIT dependent on local utility monopolies with few alternatives for electricity, water, and HVAC; demand charges, which often represent 20–40% of commercial bills, and 2024 regional rate hikes directly pressure operating margins. Efficiency projects reduce consumption but need significant upfront capital and coordination with utility providers for demand management and incentives.

Anchor tenant leverage

Anchor tenants act as quasi-suppliers for PREIT by driving the foot traffic that sustains in-line tenants; their departures in 2024 triggered co-tenancy clauses and materially reduced rent-roll stability, amplifying anchor negotiating power. PREIT has responded with rent concessions and capital allowances to retain or replace anchors. The scarcity of modern, experiential anchors further increases this leverage and raises repositioning costs.

Municipal gatekeepers

Local governments control entitlements, permits and tax incentives critical to repositioning malls; PREIT held 19 operating malls in 2024, making municipal decisions material to portfolio value. Lengthy approvals and community pushback can delay projects by months to years, effectively raising supplier power. PILOT agreements and zoning flexibility can alter project economics by millions annually; strong public-sector relationships reduce but do not eliminate this risk.

- Municipal control: entitlements, permits

- Delays: months–years, higher costs

- PILOT/zoning: millions impact

- Mitigation: public-sector relationships

Proptech and service vendors

Proptech and service vendors (leasing systems, foot-traffic analytics, security tech) became critical to PREIT by 2024, with a few specialist platforms commanding premium pricing and creating data lock-in that raises switching costs. Integration and customization typically require multi-month projects and significant IT spend, slowing vendor changes and affecting leasing velocity and operational efficiency.

- Data lock-in

- Six-figure integration costs

- Impacts leasing velocity

Suppliers wield elevated 2024 leverage amid contractor concentration and utility-driven costs

Suppliers hold elevated leverage over PREIT in 2024 due to concentrated regional contractors (≈60% share of major redevelopments), local utility monopolies driving demand charges (20–40% of bills), and scarce experiential anchor tenants increasing repositioning costs. PREIT’s multiyear frameworks and public-sector relationships partially mitigate price and schedule risk but do not eliminate supplier power.

| Metric | 2024 Value |

|---|---|

| Regional contractor share | ≈60% |

| Demand charges of commercial bills | 20–40% |

| Operating malls | 19 |

What is included in the product

Concise Porter's Five Forces analysis for PREIT that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its mall-focused portfolio.

A clear one-sheet PREIT Porter's Five Forces summary—perfect for quick mall-asset decisions; customizable pressure levels reflect rent trends, foot traffic, and retailer health. Includes an instant spider/radar chart and clean layout ready for decks or Excel dashboards.

Customers Bargaining Power

National tenant clout

National tenants, particularly large chains and creditworthy retailers, extract leverage with favorable base rents and TI packages, using brand draw and covenant quality to press PREIT (NYSE: PEI) for concessions in 2024. In key markets they secure below-market initial yields as PREIT prioritizes marquee names to drive traffic. Portfolio-level relationships allow PREIT to trade off higher rents for occupancy stability and renewal predictability.

Limited tenant pool

Retail consolidation and store rationalizations have shrunk the pool of viable tenants, with national mall vacancy rates near 10% in 2024, intensifying competition among landlords to fill space.

Fewer prospects raise tenant bargaining power as landlords bid down rents or offer TI and free-rent; specialty retailers increasingly secure concessions or shorter terms to limit exposure.

These pressures are amplified in secondary and tertiary trade areas where foot traffic and creditworthy tenants are scarcer.

Co-tenancy and kick-out rights

Lease co-tenancy and kick-out rights let tenants reduce rent or exit leases if anchors close or occupancy falls, sharply increasing customer bargaining power during disruptions. These clauses force PREIT to manage cascading effects from a single anchor failure, raising vacancy and revenue risk. Proactive backfilling, shorter-term leases, and mixed-use conversions can reduce activation of these clauses and stabilize cash flow.

Alternative location options

Tenants can relocate from PREIT malls to open-air centers, outlet districts or street retail with lower occupancy costs, increasing their leverage; PREIT’s Mid-Atlantic regional mall focus in 2024 intensifies this pressure. To retain tenants PREIT may match market concessions and flexible lease terms, while differentiated merchandising and upgraded amenities reduce direct comparability and weaken tenant bargaining power.

- Tenant options: open-air, outlets, street retail

- Leverage: higher with more location choice

- PREIT response: concessions, flexible leases

- Mitigation: unique merchandising, amenities

Price sensitivity and ROI focus

10% mall vacancy boosts tenant leverage, forcing rent concessions and TI

National, creditworthy tenants hold high leverage in 2024, extracting below-market base rents and TI to secure mall anchors, pressuring PREIT (PEI) for concessions. National mall vacancy ~10% in 2024 (ICSC), implying PREIT occupancy near 90–91% and stronger tenant negotiating power. Rent-to-sales targets ≈10% and demand for POS/footfall transparency amplify tenant bargaining.

| Metric | 2024 Value |

|---|---|

| National mall vacancy | ~10% |

| PREIT occupancy | ~90–91% |

| Retail rent-to-sales target | ~10% |

Preview Before You Purchase

PREIT Porter's Five Forces Analysis

This preview shows the exact PREIT Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted and ready for download and use. You’ll get instant access to this same professional, actionable assessment as the final deliverable.

Description

A Must-Have Tool for Decision-Makers

PREIT faces intense retail headwinds, shifting tenant mixes, and evolving consumer preferences that reshape mall profitability and leasing power. Competitive rivalry and buyer leverage remain high while barriers to new experiential retail entrants are moderate. Operational execution and property diversification are critical for resilience. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore PREIT’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated contractors

PREIT depends on specialized construction, renovation and maintenance firms that are regionally concentrated, with its mall portfolio of about 17 properties amplifying demand for limited qualified vendors.

When only a handful of contractors can execute large mall overhauls, bids and timelines rise — reports show regional contractors captured roughly 60% of major retail redevelopment projects in 2024, increasing costs and schedule risk.

That concentration raises switching costs and gives suppliers leverage during peak redevelopment cycles, though PREIT’s use of multiyear framework agreements and volume commitments in 2024 helped cap price escalation and secure capacity.

Utility dependence

Enclosed malls are energy-intensive, leaving PREIT dependent on local utility monopolies with few alternatives for electricity, water, and HVAC; demand charges, which often represent 20–40% of commercial bills, and 2024 regional rate hikes directly pressure operating margins. Efficiency projects reduce consumption but need significant upfront capital and coordination with utility providers for demand management and incentives.

Anchor tenant leverage

Anchor tenants act as quasi-suppliers for PREIT by driving the foot traffic that sustains in-line tenants; their departures in 2024 triggered co-tenancy clauses and materially reduced rent-roll stability, amplifying anchor negotiating power. PREIT has responded with rent concessions and capital allowances to retain or replace anchors. The scarcity of modern, experiential anchors further increases this leverage and raises repositioning costs.

Municipal gatekeepers

Local governments control entitlements, permits and tax incentives critical to repositioning malls; PREIT held 19 operating malls in 2024, making municipal decisions material to portfolio value. Lengthy approvals and community pushback can delay projects by months to years, effectively raising supplier power. PILOT agreements and zoning flexibility can alter project economics by millions annually; strong public-sector relationships reduce but do not eliminate this risk.

- Municipal control: entitlements, permits

- Delays: months–years, higher costs

- PILOT/zoning: millions impact

- Mitigation: public-sector relationships

Proptech and service vendors

Proptech and service vendors (leasing systems, foot-traffic analytics, security tech) became critical to PREIT by 2024, with a few specialist platforms commanding premium pricing and creating data lock-in that raises switching costs. Integration and customization typically require multi-month projects and significant IT spend, slowing vendor changes and affecting leasing velocity and operational efficiency.

- Data lock-in

- Six-figure integration costs

- Impacts leasing velocity

Suppliers wield elevated 2024 leverage amid contractor concentration and utility-driven costs

Suppliers hold elevated leverage over PREIT in 2024 due to concentrated regional contractors (≈60% share of major redevelopments), local utility monopolies driving demand charges (20–40% of bills), and scarce experiential anchor tenants increasing repositioning costs. PREIT’s multiyear frameworks and public-sector relationships partially mitigate price and schedule risk but do not eliminate supplier power.

| Metric | 2024 Value |

|---|---|

| Regional contractor share | ≈60% |

| Demand charges of commercial bills | 20–40% |

| Operating malls | 19 |

What is included in the product

Concise Porter's Five Forces analysis for PREIT that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its mall-focused portfolio.

A clear one-sheet PREIT Porter's Five Forces summary—perfect for quick mall-asset decisions; customizable pressure levels reflect rent trends, foot traffic, and retailer health. Includes an instant spider/radar chart and clean layout ready for decks or Excel dashboards.

Customers Bargaining Power

National tenant clout

National tenants, particularly large chains and creditworthy retailers, extract leverage with favorable base rents and TI packages, using brand draw and covenant quality to press PREIT (NYSE: PEI) for concessions in 2024. In key markets they secure below-market initial yields as PREIT prioritizes marquee names to drive traffic. Portfolio-level relationships allow PREIT to trade off higher rents for occupancy stability and renewal predictability.

Limited tenant pool

Retail consolidation and store rationalizations have shrunk the pool of viable tenants, with national mall vacancy rates near 10% in 2024, intensifying competition among landlords to fill space.

Fewer prospects raise tenant bargaining power as landlords bid down rents or offer TI and free-rent; specialty retailers increasingly secure concessions or shorter terms to limit exposure.

These pressures are amplified in secondary and tertiary trade areas where foot traffic and creditworthy tenants are scarcer.

Co-tenancy and kick-out rights

Lease co-tenancy and kick-out rights let tenants reduce rent or exit leases if anchors close or occupancy falls, sharply increasing customer bargaining power during disruptions. These clauses force PREIT to manage cascading effects from a single anchor failure, raising vacancy and revenue risk. Proactive backfilling, shorter-term leases, and mixed-use conversions can reduce activation of these clauses and stabilize cash flow.

Alternative location options

Tenants can relocate from PREIT malls to open-air centers, outlet districts or street retail with lower occupancy costs, increasing their leverage; PREIT’s Mid-Atlantic regional mall focus in 2024 intensifies this pressure. To retain tenants PREIT may match market concessions and flexible lease terms, while differentiated merchandising and upgraded amenities reduce direct comparability and weaken tenant bargaining power.

- Tenant options: open-air, outlets, street retail

- Leverage: higher with more location choice

- PREIT response: concessions, flexible leases

- Mitigation: unique merchandising, amenities

Price sensitivity and ROI focus

10% mall vacancy boosts tenant leverage, forcing rent concessions and TI

National, creditworthy tenants hold high leverage in 2024, extracting below-market base rents and TI to secure mall anchors, pressuring PREIT (PEI) for concessions. National mall vacancy ~10% in 2024 (ICSC), implying PREIT occupancy near 90–91% and stronger tenant negotiating power. Rent-to-sales targets ≈10% and demand for POS/footfall transparency amplify tenant bargaining.

| Metric | 2024 Value |

|---|---|

| National mall vacancy | ~10% |

| PREIT occupancy | ~90–91% |

| Retail rent-to-sales target | ~10% |

Preview Before You Purchase

PREIT Porter's Five Forces Analysis

This preview shows the exact PREIT Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted and ready for download and use. You’ll get instant access to this same professional, actionable assessment as the final deliverable.