Premier Investments PESTLE Analysis

Your Shortcut to Market Insight Starts Here

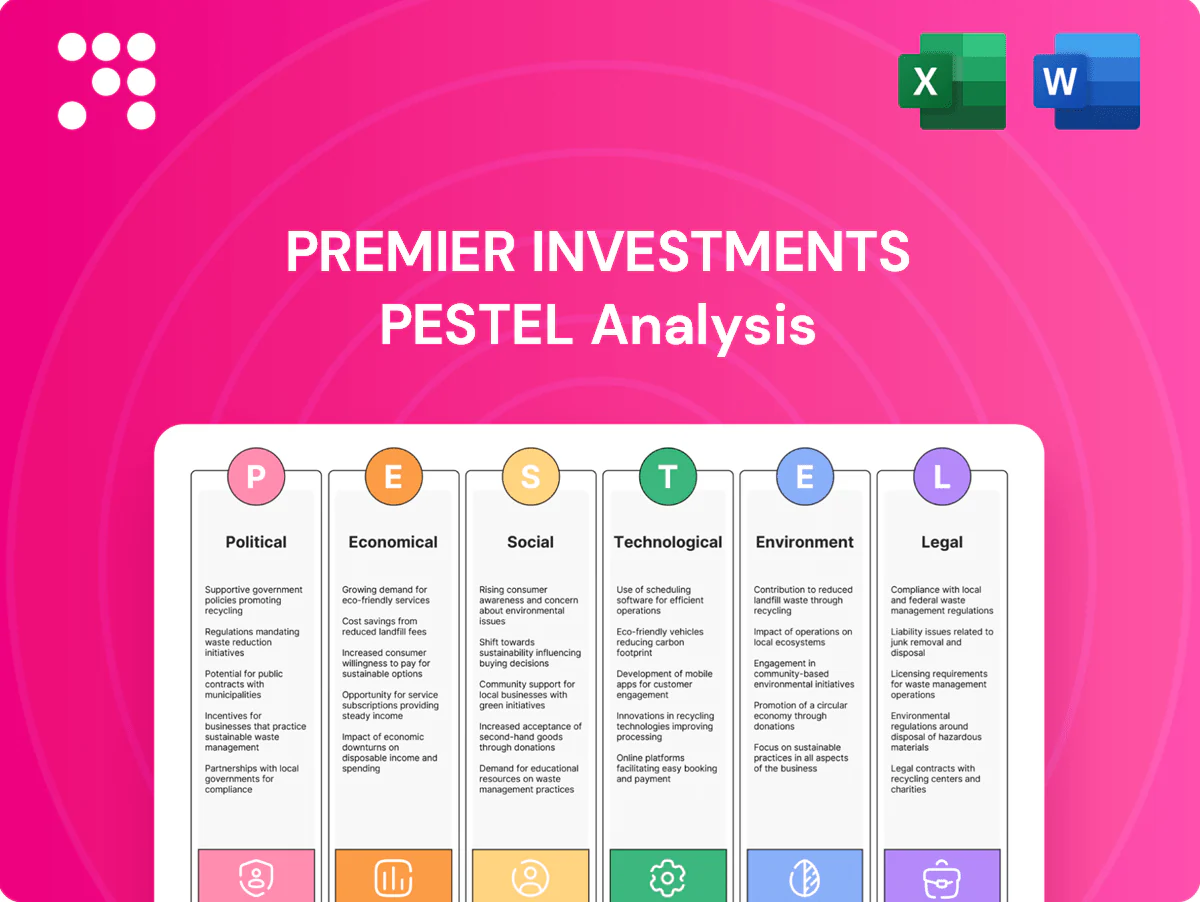

Unlock how political, economic, social, technological, legal and environmental forces shape Premier Investments' prospects in our concise PESTLE overview—perfect for investors and strategists. Buy the full analysis to access detailed risk assessments, growth opportunities and ready-to-use insights for smarter decisions.

Political factors

Trade policy and tariffs

Operating across Australia, NZ, Asia and Europe exposes Premier to shifting tariffs, FTAs and customs rules that directly affect apparel landed costs; RCEP, in force since 2022, covers about 30% of world GDP and shifts regional tariff dynamics for Asian sourcing hubs. Changes to Australia’s FTAs with Asian partners can alter duty outcomes and margins. EU apparel MFN tariffs commonly sit around 10–12% and complex rules-of-origin can complicate Smiggle and apparel flows. Proactive sourcing diversification and tariff engineering mitigate volatility in landed costs and help stabilize gross margin.

Geopolitical tensions and supply chain security

US–China and regional tensions threaten Asian manufacturing and logistics lanes used by fashion and accessories, with export controls expanded since 2022 and episodic port congestions adding weeks to transit in past disruption cycles.

Retail sector policy and fiscal settings

Government stimulus and payroll subsidies (eg JobKeeper ended 2021) shape retail demand and labor costs; GST in Australia is 10% and in New Zealand 15%, while UK VAT is 20%, all affecting pricing and margin for Premier Investments. Budget shifts in Australia and NZ alter disposable income and sentiment; UK/EU business rates and local council levies materially impact store profitability. Aligning promotions and capex with fiscal calendars is essential.

Industrial relations and minimum wage policy

Changes to minimum wages—Fair Work raised the national minimum to $882.90/week ($23.23/hr) from 1 July 2024—increase Premier Investments store labour costs across Australia and similar adjustments in NZ/UK affect margins; political support for penalty rates and rostering rules shifts economics of extended hours. Rising union activity and compliance audits boost administrative burden and potential remediation costs, while roster optimisation and productivity tools can cut labour hours by ~5%, partially offsetting wage inflation.

- Minimum wage: $882.90/wk (from 1 Jul 2024)

- Roster optimisation: ~5% labour hours saved

- Higher compliance/admin costs from audits/unions

Foreign investment and governance expectations

As an ASX-listed group (ASX:PMV) with a material exposure to Breville, Premier Investments faces heightened scrutiny over governance and cross-border investment decisions; political shifts in foreign investment rules can reallocate capital flows and affect strategic stakes. Government emphasis on corporate tax (Australia headline rate 30%) and transparency increases disclosure obligations, while robust governance reduces policy risk and supports valuation.

- ASX listing: ASX:PMV

- Corporate tax: 30% Australia

- Exposure to Breville influences investor scrutiny

- Strong governance = lower policy risk

Tariff, wage & tax shifts squeeze apparel margins — RCEP ~30%, EU 10–12%, AU $882.90/wk

Premier faces tariff/FTA shifts (RCEP in force 2022, ~30% world GDP) that affect apparel landed costs; EU MFN tariffs ~10–12%. Minimum wage Australia $882.90/wk (from 1 Jul 2024) raises store labour costs; GST AU 10%, NZ 15%, UK VAT 20%. ASX:PMV listing and 30% Australian corporate tax increase governance scrutiny.

| Item | Value |

|---|---|

| RCEP | ~30% GDP |

| EU MFN tariff | 10–12% |

| Min wage AU | $882.90/wk |

| GST/VAT | AU10%/NZ15%/UK20% |

| ASX | PMV |

| Corp tax AU | 30% |

What is included in the product

Explores how macro-environmental factors uniquely affect Premier Investments across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven points and current trends; designed for executives and investors to identify risks, opportunities and forward-looking scenarios ready for reports and strategy use.

A concise, visually segmented PESTLE summary for Premier Investments that’s easily dropped into presentations, shared across teams, and annotated for local context—streamlining risk discussion and strategic planning.

Economic factors

Consumer spending cycles and confidence

Retail apparel and gifting (Smiggle, Peter Alexander) are highly cyclical; Premier Investments reported group sales ~AU$2.6bn and NPAT ~AU$266m in FY24, exposing earnings to consumer sentiment swings. Weak confidence or rising unemployment compresses discretionary baskets and ticket sizes, driving promotional intensity in downturns and pressuring margins. Agile pricing, targeted promos and disciplined inventory buys are therefore critical to protect EBIT.

Inflation, FX, and cost of goods

Input costs priced in USD and local supplier currencies expose Premier Investments to FX risk for imported apparel and goods; AUD averaged about 0.67 USD in 2024, directly influencing landed cost from Asia.

Freight, cotton and energy inflation — which spiked globally in 2021–23 and remained elevated into 2024 — can compress gross margin if not hedged or passed through to consumers.

Hedging FX and dynamic sourcing across suppliers and regions balances price and quality, while AUD volatility also affects reported A$ results and sourcing economics.

Interest rates and household budgets

High mortgage and rent burdens have squeezed discretionary spend among core demographics, with Australian households facing record housing costs—housing payments consumed roughly one-third of disposable income for many families in 2024. Rate cuts from a mid‑2025 cash rate near 4.35% can release demand for apparel and gifting. BNPL penetration (~15% of online apparel spend in 2024) smooths baskets but raises fees and credit risk. Calibrating promotions to rate cycles supports comp sales.

Omnichannel growth and channel mix

- Online reach: 13% (2023 ABS) / ~14% (2024 Statista)

- Higher marketing & fulfillment costs vs improved inventory turns

- Click-and-collect & ship-from-store raise sell-through

- Optimal channel mix stabilises margins & working capital

Property costs and footprint optimization

Retail rents and lease terms directly drive store-level profitability for Premier Investments; ABS data shows online retailing accounted for about 12.3% of Australian retail turnover in 2023–24, increasing the need to optimize high-cost footprints.

Negotiating turnover rents and shorter leases boosts flexibility in volatile markets and allows faster store closures where performance lags, reallocating capital to digital channels.

Data-led network planning and targeted closures improve store-level ROIC by concentrating investment in higher-performing sites and omnichannel fulfilment nodes.

- Retail rents pressure: prioritize turnover rents

- Shorter leases: increase agility

- Closures → redirect capex to digital

- Data-led planning: lift ROIC

Tariff, wage & tax shifts squeeze apparel margins — RCEP ~30%, EU 10–12%, AU $882.90/wk

Premier Investments (FY24 group sales AU$2.6bn; NPAT AU$266m) is highly cyclical—consumer confidence, unemployment and housing costs (housing ≈33% disposable income in 2024) drive discretionary spend and margin pressure. FX (AUD≈0.67 USD in 2024), freight, cotton and BNPL penetration (~15% online apparel spend 2024) raise input and operating costs. Omnichannel (online ≈14% 2024) and agile sourcing/hedging are essential to defend EBIT.

| Metric | 2024/2025 |

|---|---|

| Group sales (FY24) | AU$2.6bn |

| NPAT (FY24) | AU$266m |

| AUD/USD (avg 2024) | ≈0.67 |

| Online retail AU (2024) | ≈14% |

| BNPL share (apparel 2024) | ≈15% |

| Housing cost share (2024) | ≈33% |

| Cash rate (mid‑2025) | ≈4.35% |

What You See Is What You Get

Premier Investments PESTLE Analysis

The preview of the Premier Investments PESTLE Analysis is the exact document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. No placeholders or teasers; the content and layout shown are delivered exactly as displayed. After payment you’ll instantly download this final, print-ready file.

Your Shortcut to Market Insight Starts Here

Unlock how political, economic, social, technological, legal and environmental forces shape Premier Investments' prospects in our concise PESTLE overview—perfect for investors and strategists. Buy the full analysis to access detailed risk assessments, growth opportunities and ready-to-use insights for smarter decisions.

Political factors

Trade policy and tariffs

Operating across Australia, NZ, Asia and Europe exposes Premier to shifting tariffs, FTAs and customs rules that directly affect apparel landed costs; RCEP, in force since 2022, covers about 30% of world GDP and shifts regional tariff dynamics for Asian sourcing hubs. Changes to Australia’s FTAs with Asian partners can alter duty outcomes and margins. EU apparel MFN tariffs commonly sit around 10–12% and complex rules-of-origin can complicate Smiggle and apparel flows. Proactive sourcing diversification and tariff engineering mitigate volatility in landed costs and help stabilize gross margin.

Geopolitical tensions and supply chain security

US–China and regional tensions threaten Asian manufacturing and logistics lanes used by fashion and accessories, with export controls expanded since 2022 and episodic port congestions adding weeks to transit in past disruption cycles.

Retail sector policy and fiscal settings

Government stimulus and payroll subsidies (eg JobKeeper ended 2021) shape retail demand and labor costs; GST in Australia is 10% and in New Zealand 15%, while UK VAT is 20%, all affecting pricing and margin for Premier Investments. Budget shifts in Australia and NZ alter disposable income and sentiment; UK/EU business rates and local council levies materially impact store profitability. Aligning promotions and capex with fiscal calendars is essential.

Industrial relations and minimum wage policy

Changes to minimum wages—Fair Work raised the national minimum to $882.90/week ($23.23/hr) from 1 July 2024—increase Premier Investments store labour costs across Australia and similar adjustments in NZ/UK affect margins; political support for penalty rates and rostering rules shifts economics of extended hours. Rising union activity and compliance audits boost administrative burden and potential remediation costs, while roster optimisation and productivity tools can cut labour hours by ~5%, partially offsetting wage inflation.

- Minimum wage: $882.90/wk (from 1 Jul 2024)

- Roster optimisation: ~5% labour hours saved

- Higher compliance/admin costs from audits/unions

Foreign investment and governance expectations

As an ASX-listed group (ASX:PMV) with a material exposure to Breville, Premier Investments faces heightened scrutiny over governance and cross-border investment decisions; political shifts in foreign investment rules can reallocate capital flows and affect strategic stakes. Government emphasis on corporate tax (Australia headline rate 30%) and transparency increases disclosure obligations, while robust governance reduces policy risk and supports valuation.

- ASX listing: ASX:PMV

- Corporate tax: 30% Australia

- Exposure to Breville influences investor scrutiny

- Strong governance = lower policy risk

Tariff, wage & tax shifts squeeze apparel margins — RCEP ~30%, EU 10–12%, AU $882.90/wk

Premier faces tariff/FTA shifts (RCEP in force 2022, ~30% world GDP) that affect apparel landed costs; EU MFN tariffs ~10–12%. Minimum wage Australia $882.90/wk (from 1 Jul 2024) raises store labour costs; GST AU 10%, NZ 15%, UK VAT 20%. ASX:PMV listing and 30% Australian corporate tax increase governance scrutiny.

| Item | Value |

|---|---|

| RCEP | ~30% GDP |

| EU MFN tariff | 10–12% |

| Min wage AU | $882.90/wk |

| GST/VAT | AU10%/NZ15%/UK20% |

| ASX | PMV |

| Corp tax AU | 30% |

What is included in the product

Explores how macro-environmental factors uniquely affect Premier Investments across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven points and current trends; designed for executives and investors to identify risks, opportunities and forward-looking scenarios ready for reports and strategy use.

A concise, visually segmented PESTLE summary for Premier Investments that’s easily dropped into presentations, shared across teams, and annotated for local context—streamlining risk discussion and strategic planning.

Economic factors

Consumer spending cycles and confidence

Retail apparel and gifting (Smiggle, Peter Alexander) are highly cyclical; Premier Investments reported group sales ~AU$2.6bn and NPAT ~AU$266m in FY24, exposing earnings to consumer sentiment swings. Weak confidence or rising unemployment compresses discretionary baskets and ticket sizes, driving promotional intensity in downturns and pressuring margins. Agile pricing, targeted promos and disciplined inventory buys are therefore critical to protect EBIT.

Inflation, FX, and cost of goods

Input costs priced in USD and local supplier currencies expose Premier Investments to FX risk for imported apparel and goods; AUD averaged about 0.67 USD in 2024, directly influencing landed cost from Asia.

Freight, cotton and energy inflation — which spiked globally in 2021–23 and remained elevated into 2024 — can compress gross margin if not hedged or passed through to consumers.

Hedging FX and dynamic sourcing across suppliers and regions balances price and quality, while AUD volatility also affects reported A$ results and sourcing economics.

Interest rates and household budgets

High mortgage and rent burdens have squeezed discretionary spend among core demographics, with Australian households facing record housing costs—housing payments consumed roughly one-third of disposable income for many families in 2024. Rate cuts from a mid‑2025 cash rate near 4.35% can release demand for apparel and gifting. BNPL penetration (~15% of online apparel spend in 2024) smooths baskets but raises fees and credit risk. Calibrating promotions to rate cycles supports comp sales.

Omnichannel growth and channel mix

- Online reach: 13% (2023 ABS) / ~14% (2024 Statista)

- Higher marketing & fulfillment costs vs improved inventory turns

- Click-and-collect & ship-from-store raise sell-through

- Optimal channel mix stabilises margins & working capital

Property costs and footprint optimization

Retail rents and lease terms directly drive store-level profitability for Premier Investments; ABS data shows online retailing accounted for about 12.3% of Australian retail turnover in 2023–24, increasing the need to optimize high-cost footprints.

Negotiating turnover rents and shorter leases boosts flexibility in volatile markets and allows faster store closures where performance lags, reallocating capital to digital channels.

Data-led network planning and targeted closures improve store-level ROIC by concentrating investment in higher-performing sites and omnichannel fulfilment nodes.

- Retail rents pressure: prioritize turnover rents

- Shorter leases: increase agility

- Closures → redirect capex to digital

- Data-led planning: lift ROIC

Tariff, wage & tax shifts squeeze apparel margins — RCEP ~30%, EU 10–12%, AU $882.90/wk

Premier Investments (FY24 group sales AU$2.6bn; NPAT AU$266m) is highly cyclical—consumer confidence, unemployment and housing costs (housing ≈33% disposable income in 2024) drive discretionary spend and margin pressure. FX (AUD≈0.67 USD in 2024), freight, cotton and BNPL penetration (~15% online apparel spend 2024) raise input and operating costs. Omnichannel (online ≈14% 2024) and agile sourcing/hedging are essential to defend EBIT.

| Metric | 2024/2025 |

|---|---|

| Group sales (FY24) | AU$2.6bn |

| NPAT (FY24) | AU$266m |

| AUD/USD (avg 2024) | ≈0.67 |

| Online retail AU (2024) | ≈14% |

| BNPL share (apparel 2024) | ≈15% |

| Housing cost share (2024) | ≈33% |

| Cash rate (mid‑2025) | ≈4.35% |

What You See Is What You Get

Premier Investments PESTLE Analysis

The preview of the Premier Investments PESTLE Analysis is the exact document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. No placeholders or teasers; the content and layout shown are delivered exactly as displayed. After payment you’ll instantly download this final, print-ready file.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock how political, economic, social, technological, legal and environmental forces shape Premier Investments' prospects in our concise PESTLE overview—perfect for investors and strategists. Buy the full analysis to access detailed risk assessments, growth opportunities and ready-to-use insights for smarter decisions.

Political factors

Trade policy and tariffs

Operating across Australia, NZ, Asia and Europe exposes Premier to shifting tariffs, FTAs and customs rules that directly affect apparel landed costs; RCEP, in force since 2022, covers about 30% of world GDP and shifts regional tariff dynamics for Asian sourcing hubs. Changes to Australia’s FTAs with Asian partners can alter duty outcomes and margins. EU apparel MFN tariffs commonly sit around 10–12% and complex rules-of-origin can complicate Smiggle and apparel flows. Proactive sourcing diversification and tariff engineering mitigate volatility in landed costs and help stabilize gross margin.

Geopolitical tensions and supply chain security

US–China and regional tensions threaten Asian manufacturing and logistics lanes used by fashion and accessories, with export controls expanded since 2022 and episodic port congestions adding weeks to transit in past disruption cycles.

Retail sector policy and fiscal settings

Government stimulus and payroll subsidies (eg JobKeeper ended 2021) shape retail demand and labor costs; GST in Australia is 10% and in New Zealand 15%, while UK VAT is 20%, all affecting pricing and margin for Premier Investments. Budget shifts in Australia and NZ alter disposable income and sentiment; UK/EU business rates and local council levies materially impact store profitability. Aligning promotions and capex with fiscal calendars is essential.

Industrial relations and minimum wage policy

Changes to minimum wages—Fair Work raised the national minimum to $882.90/week ($23.23/hr) from 1 July 2024—increase Premier Investments store labour costs across Australia and similar adjustments in NZ/UK affect margins; political support for penalty rates and rostering rules shifts economics of extended hours. Rising union activity and compliance audits boost administrative burden and potential remediation costs, while roster optimisation and productivity tools can cut labour hours by ~5%, partially offsetting wage inflation.

- Minimum wage: $882.90/wk (from 1 Jul 2024)

- Roster optimisation: ~5% labour hours saved

- Higher compliance/admin costs from audits/unions

Foreign investment and governance expectations

As an ASX-listed group (ASX:PMV) with a material exposure to Breville, Premier Investments faces heightened scrutiny over governance and cross-border investment decisions; political shifts in foreign investment rules can reallocate capital flows and affect strategic stakes. Government emphasis on corporate tax (Australia headline rate 30%) and transparency increases disclosure obligations, while robust governance reduces policy risk and supports valuation.

- ASX listing: ASX:PMV

- Corporate tax: 30% Australia

- Exposure to Breville influences investor scrutiny

- Strong governance = lower policy risk

Tariff, wage & tax shifts squeeze apparel margins — RCEP ~30%, EU 10–12%, AU $882.90/wk

Premier faces tariff/FTA shifts (RCEP in force 2022, ~30% world GDP) that affect apparel landed costs; EU MFN tariffs ~10–12%. Minimum wage Australia $882.90/wk (from 1 Jul 2024) raises store labour costs; GST AU 10%, NZ 15%, UK VAT 20%. ASX:PMV listing and 30% Australian corporate tax increase governance scrutiny.

| Item | Value |

|---|---|

| RCEP | ~30% GDP |

| EU MFN tariff | 10–12% |

| Min wage AU | $882.90/wk |

| GST/VAT | AU10%/NZ15%/UK20% |

| ASX | PMV |

| Corp tax AU | 30% |

What is included in the product

Explores how macro-environmental factors uniquely affect Premier Investments across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven points and current trends; designed for executives and investors to identify risks, opportunities and forward-looking scenarios ready for reports and strategy use.

A concise, visually segmented PESTLE summary for Premier Investments that’s easily dropped into presentations, shared across teams, and annotated for local context—streamlining risk discussion and strategic planning.

Economic factors

Consumer spending cycles and confidence

Retail apparel and gifting (Smiggle, Peter Alexander) are highly cyclical; Premier Investments reported group sales ~AU$2.6bn and NPAT ~AU$266m in FY24, exposing earnings to consumer sentiment swings. Weak confidence or rising unemployment compresses discretionary baskets and ticket sizes, driving promotional intensity in downturns and pressuring margins. Agile pricing, targeted promos and disciplined inventory buys are therefore critical to protect EBIT.

Inflation, FX, and cost of goods

Input costs priced in USD and local supplier currencies expose Premier Investments to FX risk for imported apparel and goods; AUD averaged about 0.67 USD in 2024, directly influencing landed cost from Asia.

Freight, cotton and energy inflation — which spiked globally in 2021–23 and remained elevated into 2024 — can compress gross margin if not hedged or passed through to consumers.

Hedging FX and dynamic sourcing across suppliers and regions balances price and quality, while AUD volatility also affects reported A$ results and sourcing economics.

Interest rates and household budgets

High mortgage and rent burdens have squeezed discretionary spend among core demographics, with Australian households facing record housing costs—housing payments consumed roughly one-third of disposable income for many families in 2024. Rate cuts from a mid‑2025 cash rate near 4.35% can release demand for apparel and gifting. BNPL penetration (~15% of online apparel spend in 2024) smooths baskets but raises fees and credit risk. Calibrating promotions to rate cycles supports comp sales.

Omnichannel growth and channel mix

- Online reach: 13% (2023 ABS) / ~14% (2024 Statista)

- Higher marketing & fulfillment costs vs improved inventory turns

- Click-and-collect & ship-from-store raise sell-through

- Optimal channel mix stabilises margins & working capital

Property costs and footprint optimization

Retail rents and lease terms directly drive store-level profitability for Premier Investments; ABS data shows online retailing accounted for about 12.3% of Australian retail turnover in 2023–24, increasing the need to optimize high-cost footprints.

Negotiating turnover rents and shorter leases boosts flexibility in volatile markets and allows faster store closures where performance lags, reallocating capital to digital channels.

Data-led network planning and targeted closures improve store-level ROIC by concentrating investment in higher-performing sites and omnichannel fulfilment nodes.

- Retail rents pressure: prioritize turnover rents

- Shorter leases: increase agility

- Closures → redirect capex to digital

- Data-led planning: lift ROIC

Tariff, wage & tax shifts squeeze apparel margins — RCEP ~30%, EU 10–12%, AU $882.90/wk

Premier Investments (FY24 group sales AU$2.6bn; NPAT AU$266m) is highly cyclical—consumer confidence, unemployment and housing costs (housing ≈33% disposable income in 2024) drive discretionary spend and margin pressure. FX (AUD≈0.67 USD in 2024), freight, cotton and BNPL penetration (~15% online apparel spend 2024) raise input and operating costs. Omnichannel (online ≈14% 2024) and agile sourcing/hedging are essential to defend EBIT.

| Metric | 2024/2025 |

|---|---|

| Group sales (FY24) | AU$2.6bn |

| NPAT (FY24) | AU$266m |

| AUD/USD (avg 2024) | ≈0.67 |

| Online retail AU (2024) | ≈14% |

| BNPL share (apparel 2024) | ≈15% |

| Housing cost share (2024) | ≈33% |

| Cash rate (mid‑2025) | ≈4.35% |

What You See Is What You Get

Premier Investments PESTLE Analysis

The preview of the Premier Investments PESTLE Analysis is the exact document you’ll receive after purchase — fully formatted, professionally structured, and ready to use. No placeholders or teasers; the content and layout shown are delivered exactly as displayed. After payment you’ll instantly download this final, print-ready file.