Primoris Services Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Primoris Services faces moderate buyer power, fragmented supplier dynamics, and niche barriers that shape its competitive stance—our snapshot flags strengths in contract scale but risks from pricing pressure and project cyclicality. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Specialized materials concentration

Primoris depends on specialty inputs like steel pipe, high‑voltage transformers, gas turbines, PV modules, and protective relays from a limited set of qualified vendors, increasing switching costs and lead times. PV module production remained concentrated in China at over 80% of global capacity in 2024, underscoring supplier leverage on price and terms. Dual‑sourcing and framework agreements reduce risk but do not fully remove supplier bargaining power.

Equipment OEMs and rental leverage

Heavy equipment OEMs and major rental fleets exert pricing power in high-utilization periods; North American rental utilization climbed to about 75% in 2024, tightening availability for cranes, HDD rigs and yellow iron. Access to that kit is critical to meeting project schedules, and long-term fleet programs and rentals smooth capex but increase vendor dependence and carry contractual price exposure. Preventive maintenance and mixed-fleet strategies partially offset OEM bargaining strength by improving uptime and bargaining flexibility.

Skilled labor and subcontractor tightness

Union halls, certified welders, linemen and niche subs are often scarce in peak cycles; an AGC 2024 survey found roughly 83% of firms reporting difficulty filling craft positions, driving wage hikes and mobilization premiums. Tight labor markets have pushed skilled hourly pay premiums into the mid‑teens percent range on many projects, elevating supplier power where qualifications and safety records are non‑negotiable. Building workforce development and deepening self‑perform capacity measurably reduces this exposure over time.

Commodity and logistics volatility

Steel, fuel, resin and freight price swings have shifted margin leverage toward upstream suppliers, with long-lead items and port congestion reducing delivery certainty and pressuring spot pricing for Primoris Services. Indexed contracts and hedging can allocate some volatility back to customers but are limited by contract scope and capital requirements. Early-buy strategies and inventory buffers improve certainty but increase working capital and exposure to obsolescence. Supply bottlenecks therefore translate directly into cost pass-through risk and schedule risk for project margins.

- Supply-driven margin pressure

- Delivery uncertainty from ports

- Indexed contracts hedging limits

- Inventory ties up working capital

Qualification and compliance barriers

Qualification and compliance barriers limit vendors to those with utility/DOT, QA/QC and ESG credentials, shrinking the pool and raising supplier leverage; Primoris reported roughly $5.0B revenue in 2024, highlighting buyer dependence on compliant suppliers. Approved-vendor lists entrench incumbents, and expanding rosters requires audits, trials and months of validation.

- Vendor pool narrowed by specialized certifications

- Approved lists raise incumbency and switching costs

- Onboarding new suppliers needs audits, trials, time

PV supplier concentration, heavy-equipment tightness and skilled-labor squeeze risk large EPC scale

Primoris faces elevated supplier bargaining from concentrated PV (China >80% capacity in 2024), long‑lead heavy equipment with NA rental utilization ~75% (2024), and skilled labor shortages (AGC: ~83% firms reporting hiring difficulty in 2024), while company scale (~$5.0B revenue 2024) increases dependence on qualified vendors.

| Supplier Factor | 2024 Metric |

|---|---|

| PV concentration | >80% China capacity |

| Rental utilization | ~75% |

| Labor shortage | 83% firms |

| Primoris revenue | $5.0B |

What is included in the product

Tailored exclusively for Primoris Services, this Porter's Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power, assesses entry barriers and substitutes, and identifies emerging threats and strategic opportunities to protect and grow market share.

A clear, one-sheet Porter's Five Forces summary for Primoris Services that instantly identifies strategic pressures with a spider/radar chart and customizable pressure levels—ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Concentrated, sophisticated customers

Utilities, energy majors and agencies are few, large and procurement‑savvy, running competitive RFPs with strict specs and performance clauses that squeeze margins.

Their scale drives price pressure and rigorous warranty/KPI terms; multi‑year MSAs (typically 3–7 years) mute spot volatility but lock in discounts and service-level KPIs.

Bid-driven pricing and slim margins

Fixed‑price and unit‑rate bidding for Primoris sharply boosts buyer leverage, with industry EBITDA margins compressing to about 3–5% in 2024 as owners push cost and schedule tradeoffs. Buyers routinely solicit multiple contractors to drive down price and tighten schedules, shifting execution risk and change-order exposure onto contractors. To avoid pure price selection, Primoris must emphasize measurable differentiation in safety performance, self‑perform capability and schedule certainty, which the market increasingly rewards.

Moderate switching costs

While projects are rebid frequently, switching vendors requires prequalification, safety vetting and mobilization (mobilization often 3–5% of project value), and for complex high‑risk work incumbency and local crews matter. Primoris carried roughly a $3.1B backlog in 2024, creating moderate switching frictions that soften buyer power, though owners keep vendor panels to preserve options.

Backlog visibility vs volume leverage

Large customers can bundle multi-region work to extract better rates; Primoris’ reported backlog of about $3.3 billion (2024) cushions utilization and lowers dependence on any single award, but large volume commitments typically come with price concessions that compress margins. Diversified end markets across energy, infrastructure and industrial segments help balance buyer influence.

Risk transfer and contractual terms

Primoris (NASDAQ: PRIM) faces buyers pushing liquidated damages, change‑order hurdles and stringent SLAs that shift schedule and cost risk downstream; robust project controls and disciplined bidding are vital to prevent value leakage, and equitable risk‑sharing negotiations improve outcomes but remain buyer‑dependent.

- Liquidated damages: buyer-driven

- Change orders: high approval hurdles

- SLAs: tighten performance risk

- Mitigation: controls, disciplined bids, negotiated risk share

Margins at 3-5% as buyers force fixed-price MSAs; $3.3B backlog cushions

Large, procurement‑savvy utilities and energy majors run competitive RFPs, forcing fixed‑price/unit‑rate bids that compress industry EBITDA to ~3–5% in 2024 and tilt warranty/KPI risk to contractors. Multi‑year MSAs (3–7 years) and bundling raise buyer leverage, though mobilization (3–5% of project value) prequalification and incumbency create moderate switching frictions. Primoris’ ~$3.3B backlog (2024) cushions utilization but volume deals typically demand price concessions.

| Metric | 2024 Value |

|---|---|

| Primoris backlog | $3.3B |

| Industry EBITDA | 3–5% |

| Mobilization | 3–5% of project |

| Typical MSA | 3–7 years |

Preview the Actual Deliverable

Primoris Services Porter's Five Forces Analysis

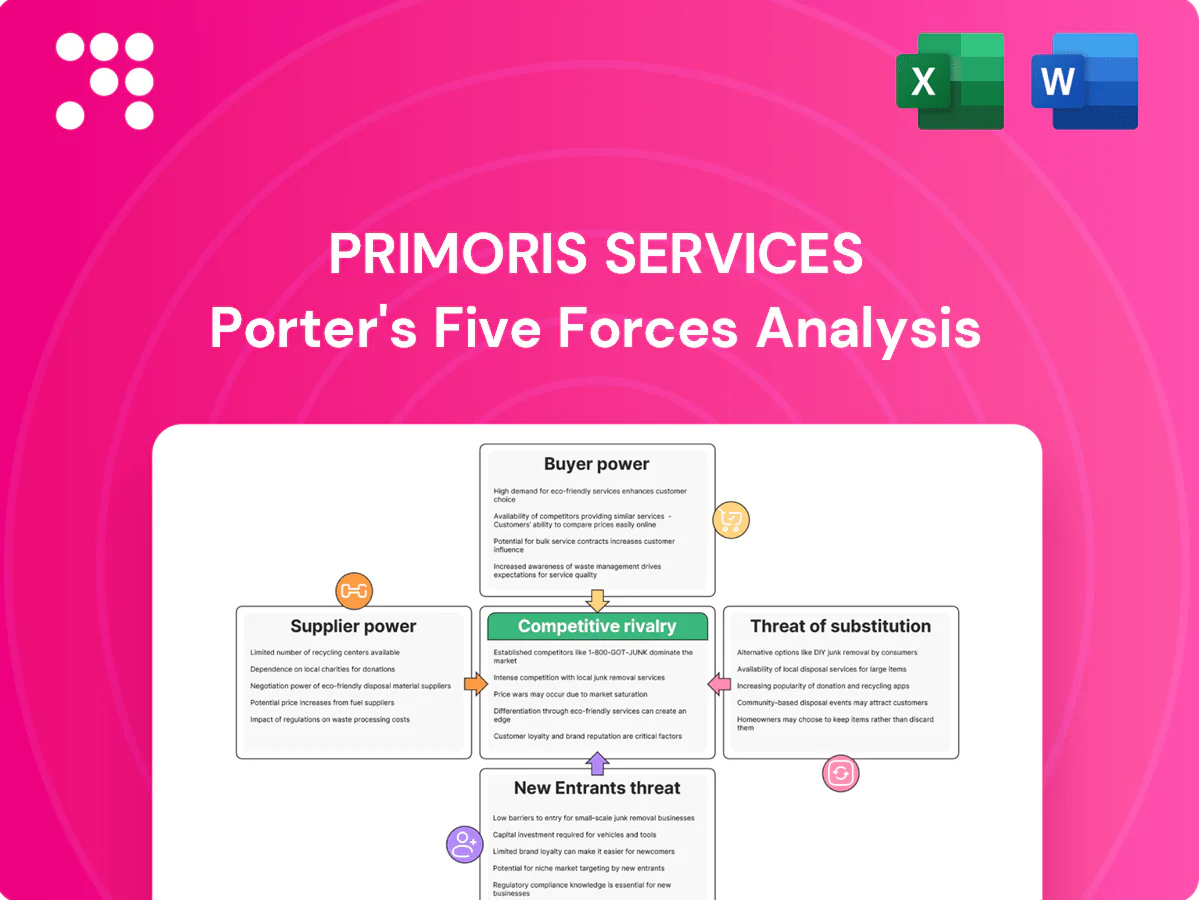

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Primoris Services Porter's Five Forces analysis provides a concise assessment of supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry tailored to the company's civil construction and specialty contracting operations. It is fully formatted and ready for download and use the moment you buy.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Primoris Services faces moderate buyer power, fragmented supplier dynamics, and niche barriers that shape its competitive stance—our snapshot flags strengths in contract scale but risks from pricing pressure and project cyclicality. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Specialized materials concentration

Primoris depends on specialty inputs like steel pipe, high‑voltage transformers, gas turbines, PV modules, and protective relays from a limited set of qualified vendors, increasing switching costs and lead times. PV module production remained concentrated in China at over 80% of global capacity in 2024, underscoring supplier leverage on price and terms. Dual‑sourcing and framework agreements reduce risk but do not fully remove supplier bargaining power.

Equipment OEMs and rental leverage

Heavy equipment OEMs and major rental fleets exert pricing power in high-utilization periods; North American rental utilization climbed to about 75% in 2024, tightening availability for cranes, HDD rigs and yellow iron. Access to that kit is critical to meeting project schedules, and long-term fleet programs and rentals smooth capex but increase vendor dependence and carry contractual price exposure. Preventive maintenance and mixed-fleet strategies partially offset OEM bargaining strength by improving uptime and bargaining flexibility.

Skilled labor and subcontractor tightness

Union halls, certified welders, linemen and niche subs are often scarce in peak cycles; an AGC 2024 survey found roughly 83% of firms reporting difficulty filling craft positions, driving wage hikes and mobilization premiums. Tight labor markets have pushed skilled hourly pay premiums into the mid‑teens percent range on many projects, elevating supplier power where qualifications and safety records are non‑negotiable. Building workforce development and deepening self‑perform capacity measurably reduces this exposure over time.

Commodity and logistics volatility

Steel, fuel, resin and freight price swings have shifted margin leverage toward upstream suppliers, with long-lead items and port congestion reducing delivery certainty and pressuring spot pricing for Primoris Services. Indexed contracts and hedging can allocate some volatility back to customers but are limited by contract scope and capital requirements. Early-buy strategies and inventory buffers improve certainty but increase working capital and exposure to obsolescence. Supply bottlenecks therefore translate directly into cost pass-through risk and schedule risk for project margins.

- Supply-driven margin pressure

- Delivery uncertainty from ports

- Indexed contracts hedging limits

- Inventory ties up working capital

Qualification and compliance barriers

Qualification and compliance barriers limit vendors to those with utility/DOT, QA/QC and ESG credentials, shrinking the pool and raising supplier leverage; Primoris reported roughly $5.0B revenue in 2024, highlighting buyer dependence on compliant suppliers. Approved-vendor lists entrench incumbents, and expanding rosters requires audits, trials and months of validation.

- Vendor pool narrowed by specialized certifications

- Approved lists raise incumbency and switching costs

- Onboarding new suppliers needs audits, trials, time

PV supplier concentration, heavy-equipment tightness and skilled-labor squeeze risk large EPC scale

Primoris faces elevated supplier bargaining from concentrated PV (China >80% capacity in 2024), long‑lead heavy equipment with NA rental utilization ~75% (2024), and skilled labor shortages (AGC: ~83% firms reporting hiring difficulty in 2024), while company scale (~$5.0B revenue 2024) increases dependence on qualified vendors.

| Supplier Factor | 2024 Metric |

|---|---|

| PV concentration | >80% China capacity |

| Rental utilization | ~75% |

| Labor shortage | 83% firms |

| Primoris revenue | $5.0B |

What is included in the product

Tailored exclusively for Primoris Services, this Porter's Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power, assesses entry barriers and substitutes, and identifies emerging threats and strategic opportunities to protect and grow market share.

A clear, one-sheet Porter's Five Forces summary for Primoris Services that instantly identifies strategic pressures with a spider/radar chart and customizable pressure levels—ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Concentrated, sophisticated customers

Utilities, energy majors and agencies are few, large and procurement‑savvy, running competitive RFPs with strict specs and performance clauses that squeeze margins.

Their scale drives price pressure and rigorous warranty/KPI terms; multi‑year MSAs (typically 3–7 years) mute spot volatility but lock in discounts and service-level KPIs.

Bid-driven pricing and slim margins

Fixed‑price and unit‑rate bidding for Primoris sharply boosts buyer leverage, with industry EBITDA margins compressing to about 3–5% in 2024 as owners push cost and schedule tradeoffs. Buyers routinely solicit multiple contractors to drive down price and tighten schedules, shifting execution risk and change-order exposure onto contractors. To avoid pure price selection, Primoris must emphasize measurable differentiation in safety performance, self‑perform capability and schedule certainty, which the market increasingly rewards.

Moderate switching costs

While projects are rebid frequently, switching vendors requires prequalification, safety vetting and mobilization (mobilization often 3–5% of project value), and for complex high‑risk work incumbency and local crews matter. Primoris carried roughly a $3.1B backlog in 2024, creating moderate switching frictions that soften buyer power, though owners keep vendor panels to preserve options.

Backlog visibility vs volume leverage

Large customers can bundle multi-region work to extract better rates; Primoris’ reported backlog of about $3.3 billion (2024) cushions utilization and lowers dependence on any single award, but large volume commitments typically come with price concessions that compress margins. Diversified end markets across energy, infrastructure and industrial segments help balance buyer influence.

Risk transfer and contractual terms

Primoris (NASDAQ: PRIM) faces buyers pushing liquidated damages, change‑order hurdles and stringent SLAs that shift schedule and cost risk downstream; robust project controls and disciplined bidding are vital to prevent value leakage, and equitable risk‑sharing negotiations improve outcomes but remain buyer‑dependent.

- Liquidated damages: buyer-driven

- Change orders: high approval hurdles

- SLAs: tighten performance risk

- Mitigation: controls, disciplined bids, negotiated risk share

Margins at 3-5% as buyers force fixed-price MSAs; $3.3B backlog cushions

Large, procurement‑savvy utilities and energy majors run competitive RFPs, forcing fixed‑price/unit‑rate bids that compress industry EBITDA to ~3–5% in 2024 and tilt warranty/KPI risk to contractors. Multi‑year MSAs (3–7 years) and bundling raise buyer leverage, though mobilization (3–5% of project value) prequalification and incumbency create moderate switching frictions. Primoris’ ~$3.3B backlog (2024) cushions utilization but volume deals typically demand price concessions.

| Metric | 2024 Value |

|---|---|

| Primoris backlog | $3.3B |

| Industry EBITDA | 3–5% |

| Mobilization | 3–5% of project |

| Typical MSA | 3–7 years |

Preview the Actual Deliverable

Primoris Services Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Primoris Services Porter's Five Forces analysis provides a concise assessment of supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry tailored to the company's civil construction and specialty contracting operations. It is fully formatted and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Primoris Services faces moderate buyer power, fragmented supplier dynamics, and niche barriers that shape its competitive stance—our snapshot flags strengths in contract scale but risks from pricing pressure and project cyclicality. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Specialized materials concentration

Primoris depends on specialty inputs like steel pipe, high‑voltage transformers, gas turbines, PV modules, and protective relays from a limited set of qualified vendors, increasing switching costs and lead times. PV module production remained concentrated in China at over 80% of global capacity in 2024, underscoring supplier leverage on price and terms. Dual‑sourcing and framework agreements reduce risk but do not fully remove supplier bargaining power.

Equipment OEMs and rental leverage

Heavy equipment OEMs and major rental fleets exert pricing power in high-utilization periods; North American rental utilization climbed to about 75% in 2024, tightening availability for cranes, HDD rigs and yellow iron. Access to that kit is critical to meeting project schedules, and long-term fleet programs and rentals smooth capex but increase vendor dependence and carry contractual price exposure. Preventive maintenance and mixed-fleet strategies partially offset OEM bargaining strength by improving uptime and bargaining flexibility.

Skilled labor and subcontractor tightness

Union halls, certified welders, linemen and niche subs are often scarce in peak cycles; an AGC 2024 survey found roughly 83% of firms reporting difficulty filling craft positions, driving wage hikes and mobilization premiums. Tight labor markets have pushed skilled hourly pay premiums into the mid‑teens percent range on many projects, elevating supplier power where qualifications and safety records are non‑negotiable. Building workforce development and deepening self‑perform capacity measurably reduces this exposure over time.

Commodity and logistics volatility

Steel, fuel, resin and freight price swings have shifted margin leverage toward upstream suppliers, with long-lead items and port congestion reducing delivery certainty and pressuring spot pricing for Primoris Services. Indexed contracts and hedging can allocate some volatility back to customers but are limited by contract scope and capital requirements. Early-buy strategies and inventory buffers improve certainty but increase working capital and exposure to obsolescence. Supply bottlenecks therefore translate directly into cost pass-through risk and schedule risk for project margins.

- Supply-driven margin pressure

- Delivery uncertainty from ports

- Indexed contracts hedging limits

- Inventory ties up working capital

Qualification and compliance barriers

Qualification and compliance barriers limit vendors to those with utility/DOT, QA/QC and ESG credentials, shrinking the pool and raising supplier leverage; Primoris reported roughly $5.0B revenue in 2024, highlighting buyer dependence on compliant suppliers. Approved-vendor lists entrench incumbents, and expanding rosters requires audits, trials and months of validation.

- Vendor pool narrowed by specialized certifications

- Approved lists raise incumbency and switching costs

- Onboarding new suppliers needs audits, trials, time

PV supplier concentration, heavy-equipment tightness and skilled-labor squeeze risk large EPC scale

Primoris faces elevated supplier bargaining from concentrated PV (China >80% capacity in 2024), long‑lead heavy equipment with NA rental utilization ~75% (2024), and skilled labor shortages (AGC: ~83% firms reporting hiring difficulty in 2024), while company scale (~$5.0B revenue 2024) increases dependence on qualified vendors.

| Supplier Factor | 2024 Metric |

|---|---|

| PV concentration | >80% China capacity |

| Rental utilization | ~75% |

| Labor shortage | 83% firms |

| Primoris revenue | $5.0B |

What is included in the product

Tailored exclusively for Primoris Services, this Porter's Five Forces overview uncovers key drivers of competition, evaluates supplier and buyer power, assesses entry barriers and substitutes, and identifies emerging threats and strategic opportunities to protect and grow market share.

A clear, one-sheet Porter's Five Forces summary for Primoris Services that instantly identifies strategic pressures with a spider/radar chart and customizable pressure levels—ready to drop into pitch decks or Excel dashboards without macros.

Customers Bargaining Power

Concentrated, sophisticated customers

Utilities, energy majors and agencies are few, large and procurement‑savvy, running competitive RFPs with strict specs and performance clauses that squeeze margins.

Their scale drives price pressure and rigorous warranty/KPI terms; multi‑year MSAs (typically 3–7 years) mute spot volatility but lock in discounts and service-level KPIs.

Bid-driven pricing and slim margins

Fixed‑price and unit‑rate bidding for Primoris sharply boosts buyer leverage, with industry EBITDA margins compressing to about 3–5% in 2024 as owners push cost and schedule tradeoffs. Buyers routinely solicit multiple contractors to drive down price and tighten schedules, shifting execution risk and change-order exposure onto contractors. To avoid pure price selection, Primoris must emphasize measurable differentiation in safety performance, self‑perform capability and schedule certainty, which the market increasingly rewards.

Moderate switching costs

While projects are rebid frequently, switching vendors requires prequalification, safety vetting and mobilization (mobilization often 3–5% of project value), and for complex high‑risk work incumbency and local crews matter. Primoris carried roughly a $3.1B backlog in 2024, creating moderate switching frictions that soften buyer power, though owners keep vendor panels to preserve options.

Backlog visibility vs volume leverage

Large customers can bundle multi-region work to extract better rates; Primoris’ reported backlog of about $3.3 billion (2024) cushions utilization and lowers dependence on any single award, but large volume commitments typically come with price concessions that compress margins. Diversified end markets across energy, infrastructure and industrial segments help balance buyer influence.

Risk transfer and contractual terms

Primoris (NASDAQ: PRIM) faces buyers pushing liquidated damages, change‑order hurdles and stringent SLAs that shift schedule and cost risk downstream; robust project controls and disciplined bidding are vital to prevent value leakage, and equitable risk‑sharing negotiations improve outcomes but remain buyer‑dependent.

- Liquidated damages: buyer-driven

- Change orders: high approval hurdles

- SLAs: tighten performance risk

- Mitigation: controls, disciplined bids, negotiated risk share

Margins at 3-5% as buyers force fixed-price MSAs; $3.3B backlog cushions

Large, procurement‑savvy utilities and energy majors run competitive RFPs, forcing fixed‑price/unit‑rate bids that compress industry EBITDA to ~3–5% in 2024 and tilt warranty/KPI risk to contractors. Multi‑year MSAs (3–7 years) and bundling raise buyer leverage, though mobilization (3–5% of project value) prequalification and incumbency create moderate switching frictions. Primoris’ ~$3.3B backlog (2024) cushions utilization but volume deals typically demand price concessions.

| Metric | 2024 Value |

|---|---|

| Primoris backlog | $3.3B |

| Industry EBITDA | 3–5% |

| Mobilization | 3–5% of project |

| Typical MSA | 3–7 years |

Preview the Actual Deliverable

Primoris Services Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The Primoris Services Porter's Five Forces analysis provides a concise assessment of supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry tailored to the company's civil construction and specialty contracting operations. It is fully formatted and ready for download and use the moment you buy.