Primoris Services PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

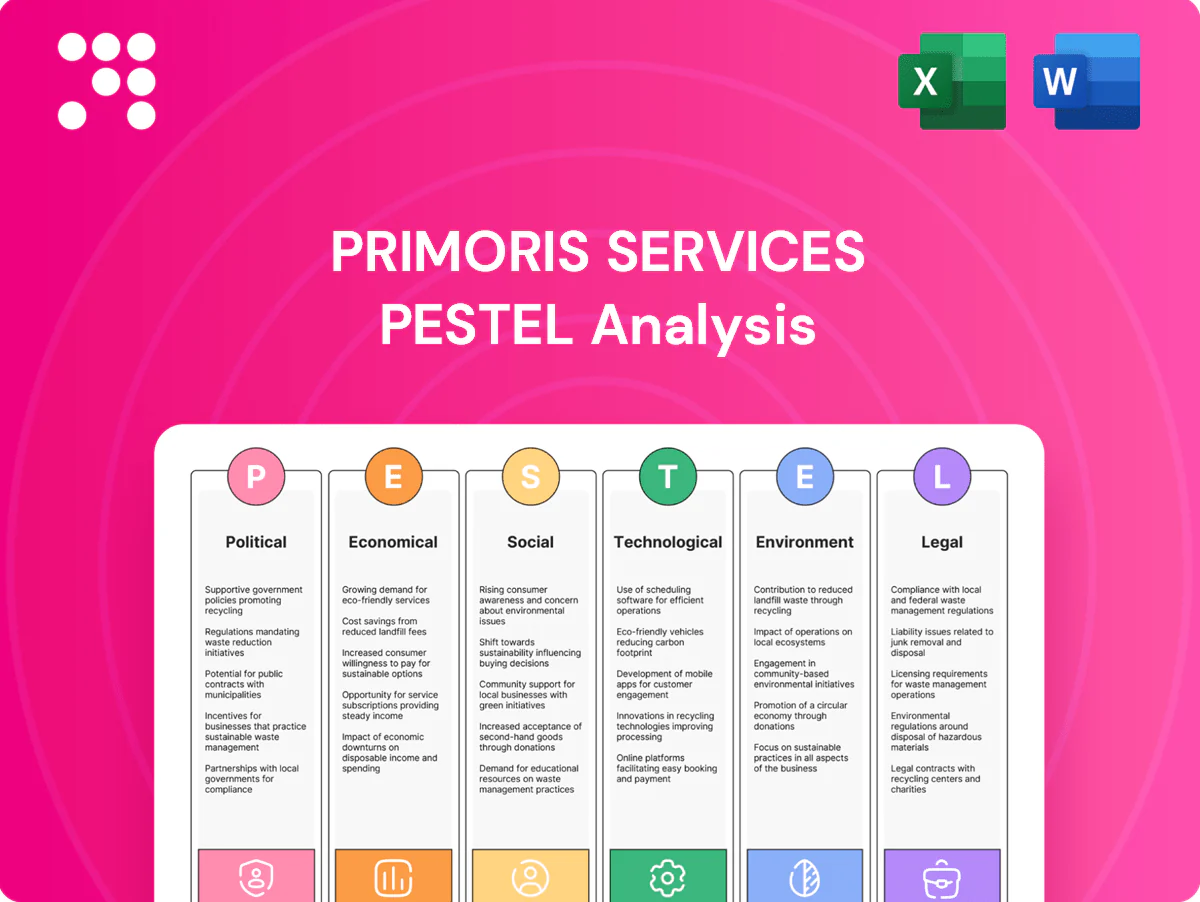

Gain a strategic edge with our PESTLE analysis of Primoris Services—concise insights on political, economic, social, technological, legal and environmental forces shaping its outlook. Ideal for investors, advisors and execs, it highlights regulatory risks, market drivers and growth pockets. Purchase the full report for detailed, editable intelligence you can act on immediately.

Political factors

Federal and state infrastructure funding

Shifts in U.S. and Canadian infrastructure bills directly drive Primoris’s bid pipeline; the IIJA commits $1.2 trillion (about $550 billion new) while BEAD allocates $42.45 billion for broadband and the IRA mobilized roughly $369 billion for energy and climate—more funding for grid hardening, broadband, and roads expands addressable markets, while delays or cuts defer starts and revenue; monitoring DOT, DOE, and provincial budgets is critical.

Permitting and energy policy direction

Permitting reform or tighter environmental reviews lengthen Primoris project timelines for pipelines, transmission and generation, raising carrying costs and bid risk. Federal direction—notably the Inflation Reduction Act’s roughly 369 billion in energy and climate spending—shifts work toward renewables and grid upgrades. Over 30 states’ RPS and clean-energy mandates boost EPC demand for renewables. Election-driven policy reversals create backlog volatility and stop-start scheduling.

Public–private partnerships and procurement

Evolving PPP frameworks and greater adoption of design‑build shift risk to private partners and can compress or expand Primoris margins depending on contract terms; the US Bipartisan Infrastructure Law commits roughly 550 billion in new federal infrastructure funding, increasing PPP opportunities. Changes in procurement rules at utilities and agencies favor integrated contractors, concentrating scope. Clear, transparent pipelines from agencies reduce bid costs and raise win rates amid local policy-driven shifts in bidding intensity.

Trade and Buy America provisions

Trade and Buy America provisions — tariffs, supply-chain localization, and Buy America rules — shape material availability and pricing. 25% steel and 10% aluminum tariffs under Section 232 and the IIJA's $550 billion of new infrastructure funding increase domestic demand, raising costs and extending lead times while protecting domestic contractors. Waivers and exemptions on large EPC packages and clearer federal policy improve schedule certainty and estimating.

- Tariffs: 25% steel, 10% aluminum (Section 232)

- Demand: IIJA adds $550 billion new infrastructure funding

- Impact: longer lead times vs domestic protection; waivers aid schedule certainty

Labor and immigration policy

Prevailing-wage rules (Davis-Bacon threshold $2,000) and apprenticeship mandates on federal projects raise field labor costs; US construction employment ~7.8M with a construction unionization rate ~12.4% that affects labor relations. H-2B visa cap 66,000 constrains seasonal staffing; CHIPS/clean-energy funding ties to apprenticeship use, so regulatory certainty aids multi-year resource planning.

- Prevailing wage: Davis-Bacon > $2,000

- Union rate (construction): ~12.4%

- Construction employment: ~7.8M

- H-2B cap: 66,000

Federal infrastructure boosts construction pipeline but raises political, cost and labor risks

Federal infrastructure packages (IIJA ~$1.2T with ~$550B new, BEAD $42.45B, IRA ~$369B) expand Primoris’s addressable market but create dependency on appropriations and election cycles. Permitting reforms, Davis‑Bacon and apprenticeship rules, and PPP shifts alter timelines, costs and margin risk. Tariffs/Buy America (steel 25%, aluminum 10%) and H-2B caps (66,000) tighten supply and labor availability.

| Policy | Key figure | Impact |

|---|---|---|

| IIJA | $1.2T (≈$550B new) | ↑Bid pipeline |

| IRA | ≈$369B | Shift to clean energy |

| BEAD | $42.45B | Broadband projects |

| Tariffs | Steel 25% / Al 10% | ↑Materials cost |

| Labor | Construction 7.8M; union 12.4%; H-2B 66k | Staffing & wage pressure |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Primoris Services, with data-driven trends and forward-looking insights to identify risks, opportunities, and strategic responses for executives, investors, and advisors.

A concise, visually segmented PESTLE summary of Primoris Services that can be dropped into presentations or shared across teams, enabling quick alignment on regulatory, economic and environmental risks while allowing space for custom notes by region or business line.

Economic factors

Interest rates and capital spending cycles

Higher interest rates (US fed funds ~5.25–5.50% in mid‑2025) raise utility and energy WACC and can defer Primoris‑relevant capex. Lower rates unlock transmission, renewables and industrial builds—US Inflation Reduction Act includes about 65 billion USD for grid/transmission. Project NPV sensitivity materially shifts award timing, while financing access drives change‑order resolution and timing of progress payments.

Inflation and input cost volatility

Steel, concrete, fuel and equipment price swings—historic volatility up to ±25% across 2021–24 and U.S. diesel averaging about $3.90/gal in 2024—strain fixed‑price Primoris contracts; escalation clauses and material hedges have limited margin erosion. Supply‑chain normalization in 2024–25 can restore bid aggressiveness, while strict procurement discipline preserves backlog quality and protects margins.

Energy price dynamics

WTI crude averaged about $80/bbl in 2024 and Henry Hub natural gas roughly $3/MMBtu, driving midstream and downstream maintenance and expansion spending. Wholesale power prices and PPA economics — often $40–60/MWh in many U.S. markets in 2024—shape renewable project starts. Price volatility both triggers outages/turnarounds during spikes and causes deferrals during slumps. Primoris diversification across end-markets helps smooth these cycles.

Labor market tightness

Labor market tightness forces Primoris to contend with skilled craft shortages that pressure wages and productivity; an AGC 2024 workforce survey found about 82% of contractors reporting difficulty filling craft positions. Training, retention, and subcontractor strategies become key differentiators as tight markets support pricing but squeeze execution timelines; regional labor mobility and multi-state crews help mitigate localized bottlenecks.

- 82% AGC 2024: difficulty filling craft roles

- Higher wages vs. productivity squeeze margins

- Training/retention/subcontracting = competitive edge

- Regional mobility reduces local shortages

Macroeconomic growth and recession risk

Slower macro growth (IMF 2025 world growth 3.0%, US real GDP ~2.5% in 2024) can delay discretionary industrial and commercial projects, but counter-cyclical utility maintenance keeps revenue steadier; Primoris reported roughly $3.6bn backlog in 2024, giving visible work into downturns while cash discipline preserves bonding capacity and bid eligibility.

- IMF 2025 world growth 3.0%

- US 2024 GDP ~2.5%

- Primoris backlog ~3.6bn (2024)

- Cash discipline sustains bonding/bids

Federal infrastructure boosts construction pipeline but raises political, cost and labor risks

Higher rates (Fed funds ~5.25–5.50% mid‑2025) raise WACC and can defer capex; IRA ~65bn USD supports grid builds. Commodity prices (WTI ~$80/bbl, diesel ~$3.90/gal) and ±25% material swings strain fixed‑price margins. Labor tightness (AGC 82% difficulty) lifts wages; Primoris backlog ~$3.6bn cushions demand swings.

| Metric | 2024/25 |

|---|---|

| Fed funds | 5.25–5.50% |

| IRA for grid | $65bn |

| WTI | $80/bbl |

| Diesel | $3.90/gal |

| AGC craft difficulty | 82% |

| Primoris backlog | $3.6bn |

Preview Before You Purchase

Primoris Services PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains a complete PESTLE analysis of Primoris Services with the same content, structure, and professional layout as the downloadable file. No placeholders or teasers—after checkout you’ll instantly get this final, ready-to-use document.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our PESTLE analysis of Primoris Services—concise insights on political, economic, social, technological, legal and environmental forces shaping its outlook. Ideal for investors, advisors and execs, it highlights regulatory risks, market drivers and growth pockets. Purchase the full report for detailed, editable intelligence you can act on immediately.

Political factors

Federal and state infrastructure funding

Shifts in U.S. and Canadian infrastructure bills directly drive Primoris’s bid pipeline; the IIJA commits $1.2 trillion (about $550 billion new) while BEAD allocates $42.45 billion for broadband and the IRA mobilized roughly $369 billion for energy and climate—more funding for grid hardening, broadband, and roads expands addressable markets, while delays or cuts defer starts and revenue; monitoring DOT, DOE, and provincial budgets is critical.

Permitting and energy policy direction

Permitting reform or tighter environmental reviews lengthen Primoris project timelines for pipelines, transmission and generation, raising carrying costs and bid risk. Federal direction—notably the Inflation Reduction Act’s roughly 369 billion in energy and climate spending—shifts work toward renewables and grid upgrades. Over 30 states’ RPS and clean-energy mandates boost EPC demand for renewables. Election-driven policy reversals create backlog volatility and stop-start scheduling.

Public–private partnerships and procurement

Evolving PPP frameworks and greater adoption of design‑build shift risk to private partners and can compress or expand Primoris margins depending on contract terms; the US Bipartisan Infrastructure Law commits roughly 550 billion in new federal infrastructure funding, increasing PPP opportunities. Changes in procurement rules at utilities and agencies favor integrated contractors, concentrating scope. Clear, transparent pipelines from agencies reduce bid costs and raise win rates amid local policy-driven shifts in bidding intensity.

Trade and Buy America provisions

Trade and Buy America provisions — tariffs, supply-chain localization, and Buy America rules — shape material availability and pricing. 25% steel and 10% aluminum tariffs under Section 232 and the IIJA's $550 billion of new infrastructure funding increase domestic demand, raising costs and extending lead times while protecting domestic contractors. Waivers and exemptions on large EPC packages and clearer federal policy improve schedule certainty and estimating.

- Tariffs: 25% steel, 10% aluminum (Section 232)

- Demand: IIJA adds $550 billion new infrastructure funding

- Impact: longer lead times vs domestic protection; waivers aid schedule certainty

Labor and immigration policy

Prevailing-wage rules (Davis-Bacon threshold $2,000) and apprenticeship mandates on federal projects raise field labor costs; US construction employment ~7.8M with a construction unionization rate ~12.4% that affects labor relations. H-2B visa cap 66,000 constrains seasonal staffing; CHIPS/clean-energy funding ties to apprenticeship use, so regulatory certainty aids multi-year resource planning.

- Prevailing wage: Davis-Bacon > $2,000

- Union rate (construction): ~12.4%

- Construction employment: ~7.8M

- H-2B cap: 66,000

Federal infrastructure boosts construction pipeline but raises political, cost and labor risks

Federal infrastructure packages (IIJA ~$1.2T with ~$550B new, BEAD $42.45B, IRA ~$369B) expand Primoris’s addressable market but create dependency on appropriations and election cycles. Permitting reforms, Davis‑Bacon and apprenticeship rules, and PPP shifts alter timelines, costs and margin risk. Tariffs/Buy America (steel 25%, aluminum 10%) and H-2B caps (66,000) tighten supply and labor availability.

| Policy | Key figure | Impact |

|---|---|---|

| IIJA | $1.2T (≈$550B new) | ↑Bid pipeline |

| IRA | ≈$369B | Shift to clean energy |

| BEAD | $42.45B | Broadband projects |

| Tariffs | Steel 25% / Al 10% | ↑Materials cost |

| Labor | Construction 7.8M; union 12.4%; H-2B 66k | Staffing & wage pressure |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Primoris Services, with data-driven trends and forward-looking insights to identify risks, opportunities, and strategic responses for executives, investors, and advisors.

A concise, visually segmented PESTLE summary of Primoris Services that can be dropped into presentations or shared across teams, enabling quick alignment on regulatory, economic and environmental risks while allowing space for custom notes by region or business line.

Economic factors

Interest rates and capital spending cycles

Higher interest rates (US fed funds ~5.25–5.50% in mid‑2025) raise utility and energy WACC and can defer Primoris‑relevant capex. Lower rates unlock transmission, renewables and industrial builds—US Inflation Reduction Act includes about 65 billion USD for grid/transmission. Project NPV sensitivity materially shifts award timing, while financing access drives change‑order resolution and timing of progress payments.

Inflation and input cost volatility

Steel, concrete, fuel and equipment price swings—historic volatility up to ±25% across 2021–24 and U.S. diesel averaging about $3.90/gal in 2024—strain fixed‑price Primoris contracts; escalation clauses and material hedges have limited margin erosion. Supply‑chain normalization in 2024–25 can restore bid aggressiveness, while strict procurement discipline preserves backlog quality and protects margins.

Energy price dynamics

WTI crude averaged about $80/bbl in 2024 and Henry Hub natural gas roughly $3/MMBtu, driving midstream and downstream maintenance and expansion spending. Wholesale power prices and PPA economics — often $40–60/MWh in many U.S. markets in 2024—shape renewable project starts. Price volatility both triggers outages/turnarounds during spikes and causes deferrals during slumps. Primoris diversification across end-markets helps smooth these cycles.

Labor market tightness

Labor market tightness forces Primoris to contend with skilled craft shortages that pressure wages and productivity; an AGC 2024 workforce survey found about 82% of contractors reporting difficulty filling craft positions. Training, retention, and subcontractor strategies become key differentiators as tight markets support pricing but squeeze execution timelines; regional labor mobility and multi-state crews help mitigate localized bottlenecks.

- 82% AGC 2024: difficulty filling craft roles

- Higher wages vs. productivity squeeze margins

- Training/retention/subcontracting = competitive edge

- Regional mobility reduces local shortages

Macroeconomic growth and recession risk

Slower macro growth (IMF 2025 world growth 3.0%, US real GDP ~2.5% in 2024) can delay discretionary industrial and commercial projects, but counter-cyclical utility maintenance keeps revenue steadier; Primoris reported roughly $3.6bn backlog in 2024, giving visible work into downturns while cash discipline preserves bonding capacity and bid eligibility.

- IMF 2025 world growth 3.0%

- US 2024 GDP ~2.5%

- Primoris backlog ~3.6bn (2024)

- Cash discipline sustains bonding/bids

Federal infrastructure boosts construction pipeline but raises political, cost and labor risks

Higher rates (Fed funds ~5.25–5.50% mid‑2025) raise WACC and can defer capex; IRA ~65bn USD supports grid builds. Commodity prices (WTI ~$80/bbl, diesel ~$3.90/gal) and ±25% material swings strain fixed‑price margins. Labor tightness (AGC 82% difficulty) lifts wages; Primoris backlog ~$3.6bn cushions demand swings.

| Metric | 2024/25 |

|---|---|

| Fed funds | 5.25–5.50% |

| IRA for grid | $65bn |

| WTI | $80/bbl |

| Diesel | $3.90/gal |

| AGC craft difficulty | 82% |

| Primoris backlog | $3.6bn |

Preview Before You Purchase

Primoris Services PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains a complete PESTLE analysis of Primoris Services with the same content, structure, and professional layout as the downloadable file. No placeholders or teasers—after checkout you’ll instantly get this final, ready-to-use document.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a strategic edge with our PESTLE analysis of Primoris Services—concise insights on political, economic, social, technological, legal and environmental forces shaping its outlook. Ideal for investors, advisors and execs, it highlights regulatory risks, market drivers and growth pockets. Purchase the full report for detailed, editable intelligence you can act on immediately.

Political factors

Federal and state infrastructure funding

Shifts in U.S. and Canadian infrastructure bills directly drive Primoris’s bid pipeline; the IIJA commits $1.2 trillion (about $550 billion new) while BEAD allocates $42.45 billion for broadband and the IRA mobilized roughly $369 billion for energy and climate—more funding for grid hardening, broadband, and roads expands addressable markets, while delays or cuts defer starts and revenue; monitoring DOT, DOE, and provincial budgets is critical.

Permitting and energy policy direction

Permitting reform or tighter environmental reviews lengthen Primoris project timelines for pipelines, transmission and generation, raising carrying costs and bid risk. Federal direction—notably the Inflation Reduction Act’s roughly 369 billion in energy and climate spending—shifts work toward renewables and grid upgrades. Over 30 states’ RPS and clean-energy mandates boost EPC demand for renewables. Election-driven policy reversals create backlog volatility and stop-start scheduling.

Public–private partnerships and procurement

Evolving PPP frameworks and greater adoption of design‑build shift risk to private partners and can compress or expand Primoris margins depending on contract terms; the US Bipartisan Infrastructure Law commits roughly 550 billion in new federal infrastructure funding, increasing PPP opportunities. Changes in procurement rules at utilities and agencies favor integrated contractors, concentrating scope. Clear, transparent pipelines from agencies reduce bid costs and raise win rates amid local policy-driven shifts in bidding intensity.

Trade and Buy America provisions

Trade and Buy America provisions — tariffs, supply-chain localization, and Buy America rules — shape material availability and pricing. 25% steel and 10% aluminum tariffs under Section 232 and the IIJA's $550 billion of new infrastructure funding increase domestic demand, raising costs and extending lead times while protecting domestic contractors. Waivers and exemptions on large EPC packages and clearer federal policy improve schedule certainty and estimating.

- Tariffs: 25% steel, 10% aluminum (Section 232)

- Demand: IIJA adds $550 billion new infrastructure funding

- Impact: longer lead times vs domestic protection; waivers aid schedule certainty

Labor and immigration policy

Prevailing-wage rules (Davis-Bacon threshold $2,000) and apprenticeship mandates on federal projects raise field labor costs; US construction employment ~7.8M with a construction unionization rate ~12.4% that affects labor relations. H-2B visa cap 66,000 constrains seasonal staffing; CHIPS/clean-energy funding ties to apprenticeship use, so regulatory certainty aids multi-year resource planning.

- Prevailing wage: Davis-Bacon > $2,000

- Union rate (construction): ~12.4%

- Construction employment: ~7.8M

- H-2B cap: 66,000

Federal infrastructure boosts construction pipeline but raises political, cost and labor risks

Federal infrastructure packages (IIJA ~$1.2T with ~$550B new, BEAD $42.45B, IRA ~$369B) expand Primoris’s addressable market but create dependency on appropriations and election cycles. Permitting reforms, Davis‑Bacon and apprenticeship rules, and PPP shifts alter timelines, costs and margin risk. Tariffs/Buy America (steel 25%, aluminum 10%) and H-2B caps (66,000) tighten supply and labor availability.

| Policy | Key figure | Impact |

|---|---|---|

| IIJA | $1.2T (≈$550B new) | ↑Bid pipeline |

| IRA | ≈$369B | Shift to clean energy |

| BEAD | $42.45B | Broadband projects |

| Tariffs | Steel 25% / Al 10% | ↑Materials cost |

| Labor | Construction 7.8M; union 12.4%; H-2B 66k | Staffing & wage pressure |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Primoris Services, with data-driven trends and forward-looking insights to identify risks, opportunities, and strategic responses for executives, investors, and advisors.

A concise, visually segmented PESTLE summary of Primoris Services that can be dropped into presentations or shared across teams, enabling quick alignment on regulatory, economic and environmental risks while allowing space for custom notes by region or business line.

Economic factors

Interest rates and capital spending cycles

Higher interest rates (US fed funds ~5.25–5.50% in mid‑2025) raise utility and energy WACC and can defer Primoris‑relevant capex. Lower rates unlock transmission, renewables and industrial builds—US Inflation Reduction Act includes about 65 billion USD for grid/transmission. Project NPV sensitivity materially shifts award timing, while financing access drives change‑order resolution and timing of progress payments.

Inflation and input cost volatility

Steel, concrete, fuel and equipment price swings—historic volatility up to ±25% across 2021–24 and U.S. diesel averaging about $3.90/gal in 2024—strain fixed‑price Primoris contracts; escalation clauses and material hedges have limited margin erosion. Supply‑chain normalization in 2024–25 can restore bid aggressiveness, while strict procurement discipline preserves backlog quality and protects margins.

Energy price dynamics

WTI crude averaged about $80/bbl in 2024 and Henry Hub natural gas roughly $3/MMBtu, driving midstream and downstream maintenance and expansion spending. Wholesale power prices and PPA economics — often $40–60/MWh in many U.S. markets in 2024—shape renewable project starts. Price volatility both triggers outages/turnarounds during spikes and causes deferrals during slumps. Primoris diversification across end-markets helps smooth these cycles.

Labor market tightness

Labor market tightness forces Primoris to contend with skilled craft shortages that pressure wages and productivity; an AGC 2024 workforce survey found about 82% of contractors reporting difficulty filling craft positions. Training, retention, and subcontractor strategies become key differentiators as tight markets support pricing but squeeze execution timelines; regional labor mobility and multi-state crews help mitigate localized bottlenecks.

- 82% AGC 2024: difficulty filling craft roles

- Higher wages vs. productivity squeeze margins

- Training/retention/subcontracting = competitive edge

- Regional mobility reduces local shortages

Macroeconomic growth and recession risk

Slower macro growth (IMF 2025 world growth 3.0%, US real GDP ~2.5% in 2024) can delay discretionary industrial and commercial projects, but counter-cyclical utility maintenance keeps revenue steadier; Primoris reported roughly $3.6bn backlog in 2024, giving visible work into downturns while cash discipline preserves bonding capacity and bid eligibility.

- IMF 2025 world growth 3.0%

- US 2024 GDP ~2.5%

- Primoris backlog ~3.6bn (2024)

- Cash discipline sustains bonding/bids

Federal infrastructure boosts construction pipeline but raises political, cost and labor risks

Higher rates (Fed funds ~5.25–5.50% mid‑2025) raise WACC and can defer capex; IRA ~65bn USD supports grid builds. Commodity prices (WTI ~$80/bbl, diesel ~$3.90/gal) and ±25% material swings strain fixed‑price margins. Labor tightness (AGC 82% difficulty) lifts wages; Primoris backlog ~$3.6bn cushions demand swings.

| Metric | 2024/25 |

|---|---|

| Fed funds | 5.25–5.50% |

| IRA for grid | $65bn |

| WTI | $80/bbl |

| Diesel | $3.90/gal |

| AGC craft difficulty | 82% |

| Primoris backlog | $3.6bn |

Preview Before You Purchase

Primoris Services PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains a complete PESTLE analysis of Primoris Services with the same content, structure, and professional layout as the downloadable file. No placeholders or teasers—after checkout you’ll instantly get this final, ready-to-use document.