Principal Financial Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

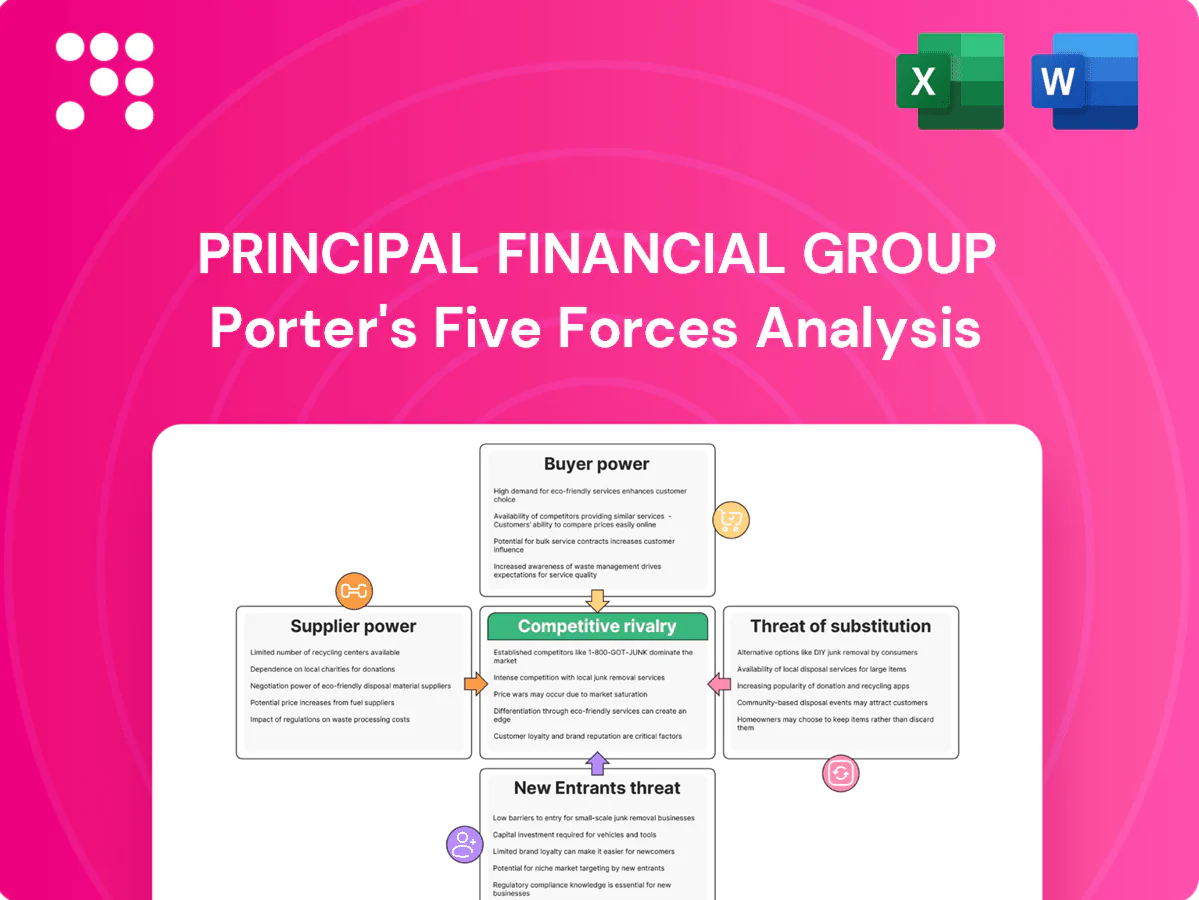

Principal Financial Group faces nuanced competitive pressures from large insurers, rising fintech substitutes, and regulatory shifts that shape margins and growth prospects. This snapshot highlights buyer bargaining, supplier constraints, and entry barriers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategy insights tailored to Principal Financial Group.

Suppliers Bargaining Power

Critical data and tech vendors

Principal depends on market data, custodial platforms, and cloud providers to run investment and admin systems; Bloomberg had about 325,000 terminals in 2024 and global cloud infra market share was roughly AWS 31%, Microsoft 24%, Google 11% (Synergy). Vendor concentration in core systems raises switching costs and outage risk, but multivendor strategies and in-house tooling reduce supplier leverage, while contracting scale secures volume discounts and enforceable SLAs.

Third-party asset managers

Third-party subadvisors supply niche strategies that can command pricing power when performance is scarce; Principal reported roughly $713 billion in AUM in 2024, but relies on external managers to fill specialized sleeves. Principal mitigates supplier power through multi-manager lineups and robust internal teams. Strong track records and capacity constraints among top subadvisors still drive premium fees and tighter terms.

Distribution intermediaries

Broker-dealers, recordkeepers and benefits consultants gate access to plan sponsors and retail flows, with shelf space and preferred lists extracting higher revenue sharing or marketing support often in the range of 10–50 bps. Principal’s own recordkeeping footprint — supporting millions of retirement participants and contributing to its $744 billion in assets under management and administration in 2024 — reduces channel dependence. Fiduciary and transparency rules have curtailed opaque economics but keep placement and shelf access strategically valuable.

Reinsurers and capital providers

Life and annuity operations rely on reinsurance and capital markets to manage risk and solvency; 2023–24 reinsurance cycles hardened with double-digit price increases and tighter terms, pressuring ceding costs. Principal's diversified risk profile and strong capital position support negotiation leverage. Macro rates (Fed funds 5.25–5.50% in 2024) and credit spreads still drive cost of capital.

- Reinsurance pricing: double-digit increases 2023–24

- Fed funds: 5.25–5.50% (2024)

- Strong balance sheet = better negotiating leverage

Specialized talent and advisors

Quant PMs, underwriters, actuaries and distribution talent are scarce for Principal; 2024 BLS medians show actuaries ~$129,470 and insurance underwriters ~$83,060, while top quant total pay often exceeds $300k, keeping supplier leverage high. Labor tightness and ~10% compensation pressure in 2024 raise costs; culture, clear career paths and variable pay have been key retention levers. Outsourced consultants supply scarce expertise but can steer product design and pricing, amplifying supplier influence.

- Scarcity: high demand for quants/actuaries/underwriters

- Compensation: 2024 pay pressure ~10%

- Retention: culture, career paths, variable pay

- Consultants: add expertise and influence pricing

Principal faces moderate supplier power; scale offsets vendor concentration and rising reinsurance

Principal faces moderate supplier power: concentrated vendors (Bloomberg ~325,000 terminals; cloud AWS 31%/MSFT 24%/GCP 11% in 2024) raise switching costs but multivendor/in‑house tools and scale (AUM/AUA ~$744bn in 2024) reduce leverage. Subadvisors and top quants command premiums; reinsurance saw double‑digit price rises in 2023–24. Distribution extracts 10–50 bps; strong balance sheet aids negotiation.

| Supplier | Metric | Impact |

|---|---|---|

| Market data/cloud | Bloomberg 325k; AWS31%/MSFT24%/GCP11% | High switching cost |

| Subadvisors | Specialty fees, capacity constraints | Premium pricing |

| Reinsurance | Double‑digit price rises 2023–24 | Higher ceding costs |

What is included in the product

Concise Porter's Five Forces for Principal Financial Group identifying competitive rivalry, buyer/supplier power, threat of substitutes and entrants, plus disruptive trends and regulatory barriers shaping profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for Principal Financial Group that quickly highlights competitive threats and bargaining dynamics—customizable pressure levels let you model regulatory shifts or new entrants and drop directly into pitch decks or boardroom slides.

Customers Bargaining Power

Institutional plan sponsors

Institutional plan sponsors exert strong bargaining power: large employers and public plans run competitive RFPs and relentlessly benchmark fees, with many large plans achieving average total plan costs near 0.39% in 2024 (Vanguard How America Saves 2024). Their scale secures volume discounts and custom mandates; switching costs exist but are manageable during periodic re-enrollment cycles, so performance, service levels, and fiduciary compliance drive renewals.

Retail investors and advisors

Retail investors are highly price-aware with easy fee and performance comparisons across funds and annuities, driving fee sensitivity; independent advisors — controlling large retail flows — can redirect business rapidly. Digital account opening and e-signatures in 2024 have cut switching friction significantly, increasing churn risk. Principal’s brand trust and integrated advisory platforms partially offset pure price competition, supporting retention.

Fee compression dynamics

Indexing and ETFs, which captured over 50% of U.S. mutual fund and ETF assets by 2024, anchor fees at industry-low levels and pressure Principal to match sub-0.20% ETF-style pricing on core products. Buyers increasingly demand lower-expense share classes and advisory rebates, forcing margin squeeze across retail and institutional channels. Outcome-based and unitized fees face heightened scrutiny from consultants and regulators. Clear value articulation around service, guarantees, and measurable outcomes is essential to defend pricing.

Product substitutability

Clients can swap active for passive, annuities for bond ladders, or move insurance across carriers, increasing buyer leverage; passive strategies held about 50% of U.S. equity assets by 2024. Bundling planning and benefits integration raises stickiness and retention, while clear product differentiation reduces apples-to-apples price pressure.

- Product substitutability: high

- Passive share ~50% (2024)

- Bundling raises switching costs

Data transparency and benchmarking

Platforms publish performance, risk, and fee metrics continuously via vendors like Bloomberg and Morningstar, enabling buyers to benchmark managers in real time; buyers leverage peer-group comparisons to demand fee concessions and mandate changes. Underperformance triggers accelerated redemptions and mandate losses, while superior disclosures and consistent alpha reduce churn and stabilize flows.

- Continuous public metrics

- Benchmark-driven fee pressure

- Underperformance → faster redemptions

- Disclosure + alpha = lower churn

Scale drives fees to 0.39%; passive >50% forces core0.20%

Institutional plan sponsors exert strong leverage: RFPs/benchmarks drive fees to ~0.39% average total plan cost (Vanguard How America Saves 2024), with scale enabling discounts.

Retail investors and advisors are fee-sensitive; digital onboarding lowers switching friction and raises churn risk.

Passive/ETF share ~50%+ in 2024, forcing sub-0.20% pricing on core products; bundling and guarantees defend margins.

| Metric | 2024 Value |

|---|---|

| Institutional avg total plan cost | 0.39% |

| Passive/ETF share | ~50% |

| Core fee pressure | ~<0.20% |

Preview Before You Purchase

Principal Financial Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of Principal Financial Group examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic and investment decisions. The preview you see is the exact, professionally formatted document you'll receive instantly after purchase—no placeholders or samples. It's ready for download and immediate use in your analysis or presentations.

From Overview to Strategy Blueprint

Principal Financial Group faces nuanced competitive pressures from large insurers, rising fintech substitutes, and regulatory shifts that shape margins and growth prospects. This snapshot highlights buyer bargaining, supplier constraints, and entry barriers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategy insights tailored to Principal Financial Group.

Suppliers Bargaining Power

Critical data and tech vendors

Principal depends on market data, custodial platforms, and cloud providers to run investment and admin systems; Bloomberg had about 325,000 terminals in 2024 and global cloud infra market share was roughly AWS 31%, Microsoft 24%, Google 11% (Synergy). Vendor concentration in core systems raises switching costs and outage risk, but multivendor strategies and in-house tooling reduce supplier leverage, while contracting scale secures volume discounts and enforceable SLAs.

Third-party asset managers

Third-party subadvisors supply niche strategies that can command pricing power when performance is scarce; Principal reported roughly $713 billion in AUM in 2024, but relies on external managers to fill specialized sleeves. Principal mitigates supplier power through multi-manager lineups and robust internal teams. Strong track records and capacity constraints among top subadvisors still drive premium fees and tighter terms.

Distribution intermediaries

Broker-dealers, recordkeepers and benefits consultants gate access to plan sponsors and retail flows, with shelf space and preferred lists extracting higher revenue sharing or marketing support often in the range of 10–50 bps. Principal’s own recordkeeping footprint — supporting millions of retirement participants and contributing to its $744 billion in assets under management and administration in 2024 — reduces channel dependence. Fiduciary and transparency rules have curtailed opaque economics but keep placement and shelf access strategically valuable.

Reinsurers and capital providers

Life and annuity operations rely on reinsurance and capital markets to manage risk and solvency; 2023–24 reinsurance cycles hardened with double-digit price increases and tighter terms, pressuring ceding costs. Principal's diversified risk profile and strong capital position support negotiation leverage. Macro rates (Fed funds 5.25–5.50% in 2024) and credit spreads still drive cost of capital.

- Reinsurance pricing: double-digit increases 2023–24

- Fed funds: 5.25–5.50% (2024)

- Strong balance sheet = better negotiating leverage

Specialized talent and advisors

Quant PMs, underwriters, actuaries and distribution talent are scarce for Principal; 2024 BLS medians show actuaries ~$129,470 and insurance underwriters ~$83,060, while top quant total pay often exceeds $300k, keeping supplier leverage high. Labor tightness and ~10% compensation pressure in 2024 raise costs; culture, clear career paths and variable pay have been key retention levers. Outsourced consultants supply scarce expertise but can steer product design and pricing, amplifying supplier influence.

- Scarcity: high demand for quants/actuaries/underwriters

- Compensation: 2024 pay pressure ~10%

- Retention: culture, career paths, variable pay

- Consultants: add expertise and influence pricing

Principal faces moderate supplier power; scale offsets vendor concentration and rising reinsurance

Principal faces moderate supplier power: concentrated vendors (Bloomberg ~325,000 terminals; cloud AWS 31%/MSFT 24%/GCP 11% in 2024) raise switching costs but multivendor/in‑house tools and scale (AUM/AUA ~$744bn in 2024) reduce leverage. Subadvisors and top quants command premiums; reinsurance saw double‑digit price rises in 2023–24. Distribution extracts 10–50 bps; strong balance sheet aids negotiation.

| Supplier | Metric | Impact |

|---|---|---|

| Market data/cloud | Bloomberg 325k; AWS31%/MSFT24%/GCP11% | High switching cost |

| Subadvisors | Specialty fees, capacity constraints | Premium pricing |

| Reinsurance | Double‑digit price rises 2023–24 | Higher ceding costs |

What is included in the product

Concise Porter's Five Forces for Principal Financial Group identifying competitive rivalry, buyer/supplier power, threat of substitutes and entrants, plus disruptive trends and regulatory barriers shaping profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for Principal Financial Group that quickly highlights competitive threats and bargaining dynamics—customizable pressure levels let you model regulatory shifts or new entrants and drop directly into pitch decks or boardroom slides.

Customers Bargaining Power

Institutional plan sponsors

Institutional plan sponsors exert strong bargaining power: large employers and public plans run competitive RFPs and relentlessly benchmark fees, with many large plans achieving average total plan costs near 0.39% in 2024 (Vanguard How America Saves 2024). Their scale secures volume discounts and custom mandates; switching costs exist but are manageable during periodic re-enrollment cycles, so performance, service levels, and fiduciary compliance drive renewals.

Retail investors and advisors

Retail investors are highly price-aware with easy fee and performance comparisons across funds and annuities, driving fee sensitivity; independent advisors — controlling large retail flows — can redirect business rapidly. Digital account opening and e-signatures in 2024 have cut switching friction significantly, increasing churn risk. Principal’s brand trust and integrated advisory platforms partially offset pure price competition, supporting retention.

Fee compression dynamics

Indexing and ETFs, which captured over 50% of U.S. mutual fund and ETF assets by 2024, anchor fees at industry-low levels and pressure Principal to match sub-0.20% ETF-style pricing on core products. Buyers increasingly demand lower-expense share classes and advisory rebates, forcing margin squeeze across retail and institutional channels. Outcome-based and unitized fees face heightened scrutiny from consultants and regulators. Clear value articulation around service, guarantees, and measurable outcomes is essential to defend pricing.

Product substitutability

Clients can swap active for passive, annuities for bond ladders, or move insurance across carriers, increasing buyer leverage; passive strategies held about 50% of U.S. equity assets by 2024. Bundling planning and benefits integration raises stickiness and retention, while clear product differentiation reduces apples-to-apples price pressure.

- Product substitutability: high

- Passive share ~50% (2024)

- Bundling raises switching costs

Data transparency and benchmarking

Platforms publish performance, risk, and fee metrics continuously via vendors like Bloomberg and Morningstar, enabling buyers to benchmark managers in real time; buyers leverage peer-group comparisons to demand fee concessions and mandate changes. Underperformance triggers accelerated redemptions and mandate losses, while superior disclosures and consistent alpha reduce churn and stabilize flows.

- Continuous public metrics

- Benchmark-driven fee pressure

- Underperformance → faster redemptions

- Disclosure + alpha = lower churn

Scale drives fees to 0.39%; passive >50% forces core0.20%

Institutional plan sponsors exert strong leverage: RFPs/benchmarks drive fees to ~0.39% average total plan cost (Vanguard How America Saves 2024), with scale enabling discounts.

Retail investors and advisors are fee-sensitive; digital onboarding lowers switching friction and raises churn risk.

Passive/ETF share ~50%+ in 2024, forcing sub-0.20% pricing on core products; bundling and guarantees defend margins.

| Metric | 2024 Value |

|---|---|

| Institutional avg total plan cost | 0.39% |

| Passive/ETF share | ~50% |

| Core fee pressure | ~<0.20% |

Preview Before You Purchase

Principal Financial Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of Principal Financial Group examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic and investment decisions. The preview you see is the exact, professionally formatted document you'll receive instantly after purchase—no placeholders or samples. It's ready for download and immediate use in your analysis or presentations.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Principal Financial Group faces nuanced competitive pressures from large insurers, rising fintech substitutes, and regulatory shifts that shape margins and growth prospects. This snapshot highlights buyer bargaining, supplier constraints, and entry barriers but only scratches the surface. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable strategy insights tailored to Principal Financial Group.

Suppliers Bargaining Power

Critical data and tech vendors

Principal depends on market data, custodial platforms, and cloud providers to run investment and admin systems; Bloomberg had about 325,000 terminals in 2024 and global cloud infra market share was roughly AWS 31%, Microsoft 24%, Google 11% (Synergy). Vendor concentration in core systems raises switching costs and outage risk, but multivendor strategies and in-house tooling reduce supplier leverage, while contracting scale secures volume discounts and enforceable SLAs.

Third-party asset managers

Third-party subadvisors supply niche strategies that can command pricing power when performance is scarce; Principal reported roughly $713 billion in AUM in 2024, but relies on external managers to fill specialized sleeves. Principal mitigates supplier power through multi-manager lineups and robust internal teams. Strong track records and capacity constraints among top subadvisors still drive premium fees and tighter terms.

Distribution intermediaries

Broker-dealers, recordkeepers and benefits consultants gate access to plan sponsors and retail flows, with shelf space and preferred lists extracting higher revenue sharing or marketing support often in the range of 10–50 bps. Principal’s own recordkeeping footprint — supporting millions of retirement participants and contributing to its $744 billion in assets under management and administration in 2024 — reduces channel dependence. Fiduciary and transparency rules have curtailed opaque economics but keep placement and shelf access strategically valuable.

Reinsurers and capital providers

Life and annuity operations rely on reinsurance and capital markets to manage risk and solvency; 2023–24 reinsurance cycles hardened with double-digit price increases and tighter terms, pressuring ceding costs. Principal's diversified risk profile and strong capital position support negotiation leverage. Macro rates (Fed funds 5.25–5.50% in 2024) and credit spreads still drive cost of capital.

- Reinsurance pricing: double-digit increases 2023–24

- Fed funds: 5.25–5.50% (2024)

- Strong balance sheet = better negotiating leverage

Specialized talent and advisors

Quant PMs, underwriters, actuaries and distribution talent are scarce for Principal; 2024 BLS medians show actuaries ~$129,470 and insurance underwriters ~$83,060, while top quant total pay often exceeds $300k, keeping supplier leverage high. Labor tightness and ~10% compensation pressure in 2024 raise costs; culture, clear career paths and variable pay have been key retention levers. Outsourced consultants supply scarce expertise but can steer product design and pricing, amplifying supplier influence.

- Scarcity: high demand for quants/actuaries/underwriters

- Compensation: 2024 pay pressure ~10%

- Retention: culture, career paths, variable pay

- Consultants: add expertise and influence pricing

Principal faces moderate supplier power; scale offsets vendor concentration and rising reinsurance

Principal faces moderate supplier power: concentrated vendors (Bloomberg ~325,000 terminals; cloud AWS 31%/MSFT 24%/GCP 11% in 2024) raise switching costs but multivendor/in‑house tools and scale (AUM/AUA ~$744bn in 2024) reduce leverage. Subadvisors and top quants command premiums; reinsurance saw double‑digit price rises in 2023–24. Distribution extracts 10–50 bps; strong balance sheet aids negotiation.

| Supplier | Metric | Impact |

|---|---|---|

| Market data/cloud | Bloomberg 325k; AWS31%/MSFT24%/GCP11% | High switching cost |

| Subadvisors | Specialty fees, capacity constraints | Premium pricing |

| Reinsurance | Double‑digit price rises 2023–24 | Higher ceding costs |

What is included in the product

Concise Porter's Five Forces for Principal Financial Group identifying competitive rivalry, buyer/supplier power, threat of substitutes and entrants, plus disruptive trends and regulatory barriers shaping profitability and strategic positioning.

A concise Porter's Five Forces one-sheet for Principal Financial Group that quickly highlights competitive threats and bargaining dynamics—customizable pressure levels let you model regulatory shifts or new entrants and drop directly into pitch decks or boardroom slides.

Customers Bargaining Power

Institutional plan sponsors

Institutional plan sponsors exert strong bargaining power: large employers and public plans run competitive RFPs and relentlessly benchmark fees, with many large plans achieving average total plan costs near 0.39% in 2024 (Vanguard How America Saves 2024). Their scale secures volume discounts and custom mandates; switching costs exist but are manageable during periodic re-enrollment cycles, so performance, service levels, and fiduciary compliance drive renewals.

Retail investors and advisors

Retail investors are highly price-aware with easy fee and performance comparisons across funds and annuities, driving fee sensitivity; independent advisors — controlling large retail flows — can redirect business rapidly. Digital account opening and e-signatures in 2024 have cut switching friction significantly, increasing churn risk. Principal’s brand trust and integrated advisory platforms partially offset pure price competition, supporting retention.

Fee compression dynamics

Indexing and ETFs, which captured over 50% of U.S. mutual fund and ETF assets by 2024, anchor fees at industry-low levels and pressure Principal to match sub-0.20% ETF-style pricing on core products. Buyers increasingly demand lower-expense share classes and advisory rebates, forcing margin squeeze across retail and institutional channels. Outcome-based and unitized fees face heightened scrutiny from consultants and regulators. Clear value articulation around service, guarantees, and measurable outcomes is essential to defend pricing.

Product substitutability

Clients can swap active for passive, annuities for bond ladders, or move insurance across carriers, increasing buyer leverage; passive strategies held about 50% of U.S. equity assets by 2024. Bundling planning and benefits integration raises stickiness and retention, while clear product differentiation reduces apples-to-apples price pressure.

- Product substitutability: high

- Passive share ~50% (2024)

- Bundling raises switching costs

Data transparency and benchmarking

Platforms publish performance, risk, and fee metrics continuously via vendors like Bloomberg and Morningstar, enabling buyers to benchmark managers in real time; buyers leverage peer-group comparisons to demand fee concessions and mandate changes. Underperformance triggers accelerated redemptions and mandate losses, while superior disclosures and consistent alpha reduce churn and stabilize flows.

- Continuous public metrics

- Benchmark-driven fee pressure

- Underperformance → faster redemptions

- Disclosure + alpha = lower churn

Scale drives fees to 0.39%; passive >50% forces core0.20%

Institutional plan sponsors exert strong leverage: RFPs/benchmarks drive fees to ~0.39% average total plan cost (Vanguard How America Saves 2024), with scale enabling discounts.

Retail investors and advisors are fee-sensitive; digital onboarding lowers switching friction and raises churn risk.

Passive/ETF share ~50%+ in 2024, forcing sub-0.20% pricing on core products; bundling and guarantees defend margins.

| Metric | 2024 Value |

|---|---|

| Institutional avg total plan cost | 0.39% |

| Passive/ETF share | ~50% |

| Core fee pressure | ~<0.20% |

Preview Before You Purchase

Principal Financial Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of Principal Financial Group examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry to inform strategic and investment decisions. The preview you see is the exact, professionally formatted document you'll receive instantly after purchase—no placeholders or samples. It's ready for download and immediate use in your analysis or presentations.