ProAct Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

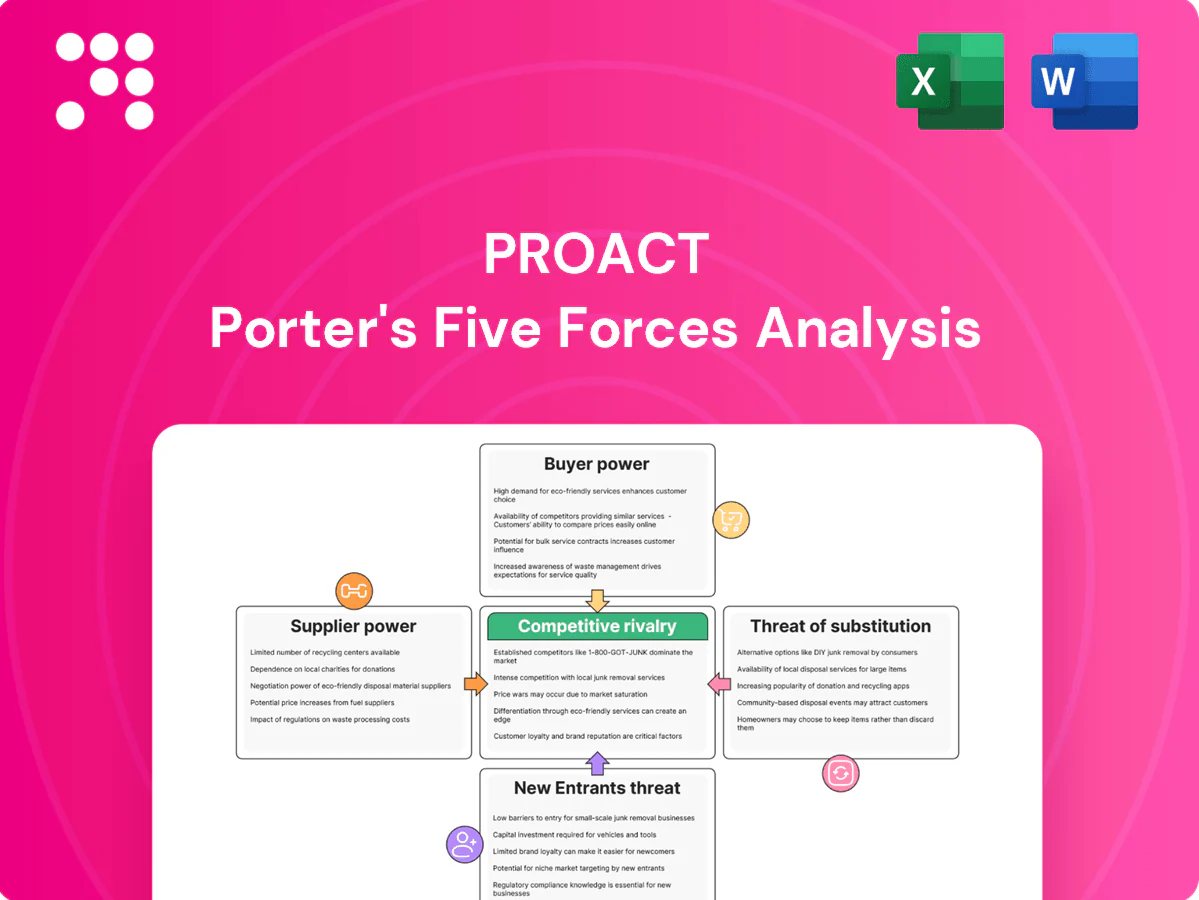

ProAct's competitive landscape is shaped by powerful forces, from the intense rivalry among existing players to the constant threat of new entrants disrupting the market. Understanding these dynamics is crucial for any business aiming to thrive.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ProAct’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Key Technology Vendors

Proact's reliance on a limited number of key technology vendors for its data center and cloud solutions, like NetApp and VMware, significantly impacts supplier bargaining power. When these markets are concentrated, a few dominant suppliers can dictate pricing and contract terms, potentially increasing Proact's operational costs.

The strategic importance of Proact's partnerships and certifications with these critical infrastructure providers highlights their leverage. These relationships are not just about sourcing; they are foundational to the quality and comprehensiveness of Proact's service delivery.

Switching Costs for Proact

Switching core technology suppliers, such as for storage platforms or virtualization software, presents significant hurdles for Proact. These transitions can incur substantial costs related to retraining personnel, re-engineering existing solutions, and the potential for service interruptions for clients. For instance, a major cloud provider change could cost millions in migration and validation efforts.

These elevated switching costs inherently bolster the bargaining power of Proact's current, established technology vendors. While Proact's expertise in integrating various technologies offers some flexibility, fundamental shifts in core infrastructure remain a costly undertaking, reinforcing supplier leverage.

Uniqueness and Differentiation of Supplier Offerings

Suppliers offering highly specialized or proprietary technologies, such as those in advanced data protection or AI infrastructure, wield significant bargaining power. If Proact relies on a supplier's unique product with few viable alternatives, its ability to negotiate favorable terms diminishes. For instance, the burgeoning demand for AI infrastructure in 2024 is likely to further bolster the negotiating leverage of niche technology providers in this space, potentially increasing component costs.

Threat of Forward Integration by Suppliers

Large technology providers, particularly those with cloud offerings like Microsoft Azure and Amazon Web Services (AWS), present a potential threat by being able to offer services directly to Proact's clients, effectively cutting out Proact. This risk is less pronounced for Proact's specialized managed services, which often involve complex, multi-vendor integrations. However, it underscores the imperative for Proact to consistently demonstrate value beyond mere infrastructure management to maintain its competitive edge.

For instance, in 2024, cloud infrastructure spending continued its robust growth, with AWS and Microsoft Azure holding significant market shares. AWS reported over $65 billion in revenue for 2023, and Microsoft's Intelligent Cloud segment, which includes Azure, saw substantial growth. This indicates the scale of these players and their potential to leverage their platforms for direct customer engagement.

- Direct Service Offering: Major cloud providers can bundle managed services with their core cloud products, potentially offering a more integrated solution to customers.

- Value Proposition Differentiation: Proact must continually enhance its service offerings to provide unique value that cannot be easily replicated by these large technology suppliers.

- Partnership Dynamics: Maintaining strong, collaborative relationships with these suppliers is crucial to mitigate the threat and leverage their platforms effectively.

Availability of Substitute Inputs

The availability of substitute inputs significantly impacts supplier bargaining power. When numerous alternatives exist for a component, customers can switch more easily, diminishing the supplier's leverage. For instance, the rise of open-source software and readily available commodity hardware for data centers can dilute the power of traditional proprietary vendors.

ProAct's business model, focused on flexible IT solutions, is well-positioned to capitalize on this. By utilizing a diverse range of inputs for non-specialized needs, ProAct can reduce its reliance on any single supplier. This strategy is particularly effective for components like standard server racks or basic networking equipment where multiple manufacturers offer comparable products.

However, the situation shifts for specialized hardware and software critical to data center operations. For these bespoke or proprietary solutions, the availability of direct substitutes can be quite limited. For example, advanced AI processing units or highly integrated cloud management platforms may have few, if any, direct alternatives, thereby strengthening the bargaining power of the suppliers offering them.

- Limited Substitutes for Specialized Hardware: In 2024, the global market for high-performance computing (HPC) hardware, including specialized GPUs and AI accelerators, saw continued consolidation, with a few key players dominating. This limited the availability of direct substitutes, potentially increasing supplier power for ProAct when sourcing these critical components.

- Open-Source Adoption Growth: Conversely, the adoption of open-source solutions in areas like operating systems and containerization continued to grow. In 2024, estimates suggest that over 70% of enterprise workloads ran on Linux-based systems, providing ProAct with significant leverage when negotiating with providers of commodity server components and related software.

- Commodity Component Price Volatility: While substitutes exist for many commodity IT components, their prices can be subject to significant volatility based on global supply chain dynamics. For example, fluctuations in the cost of memory chips or solid-state drives in 2024 demonstrated how even with multiple suppliers, market conditions can temporarily shift bargaining power.

- ProAct's Diversification Strategy: ProAct’s strategy to offer flexible IT solutions inherently involves building relationships with a broad base of suppliers. This diversification mitigates the risk of over-reliance on any single vendor for non-specialized equipment, thereby maintaining a degree of control over input costs and availability.

Supplier Power: Impact on Operational Costs and Strategic Flexibility

The bargaining power of suppliers significantly influences ProAct's operational costs and strategic flexibility. When suppliers offer highly specialized or proprietary technologies, like advanced AI infrastructure components in 2024, their leverage increases due to limited alternatives.

High switching costs associated with core technology vendors, such as for virtualization software, further empower these suppliers. These costs, encompassing retraining and potential service disruptions, can run into millions, reinforcing vendor control over pricing and terms.

The availability of substitute inputs is a key factor; while commodity IT components have many alternatives, specialized hardware for areas like AI in 2024 saw limited substitutes, strengthening supplier positions. ProAct's diversification strategy helps mitigate this for non-specialized needs.

| Supplier Characteristic | Impact on ProAct | 2024 Context/Data |

|---|---|---|

| Concentrated Market / Few Dominant Players | Increased supplier leverage, potential for higher pricing | Cloud infrastructure dominated by AWS and Microsoft Azure, with significant market share growth in 2023. |

| High Switching Costs for ProAct | Reinforces existing supplier power, reduces ProAct's negotiation flexibility | Migrating core cloud infrastructure can cost millions, making transitions difficult. |

| Proprietary/Specialized Offerings | Strong supplier bargaining power due to lack of direct substitutes | AI hardware market in 2024 showed consolidation, limiting alternatives for high-performance components. |

| Availability of Substitutes | Weakens supplier power for commodity inputs, strengthens for specialized ones | Over 70% of enterprise workloads ran on Linux in 2024, providing leverage for commodity server needs. |

What is included in the product

ProAct's Porter's Five Forces Analysis dissects the competitive intensity within its industry, examining threats from new entrants, the power of buyers and suppliers, the availability of substitutes, and the rivalry among existing competitors.

ProAct Porter's Five Forces Analysis pinpoints and quantifies competitive pressures, allowing you to proactively address threats before they impact profitability.

Customers Bargaining Power

Customer Concentration and Size

Proact's customer base spans across Europe, serving both small and medium-sized enterprises (SMEs) and larger corporations. This diversity is a key strength, as it reduces reliance on any single client.

However, if a substantial portion of Proact's revenue is concentrated among a few major clients, these large customers would possess significant bargaining power. They could leverage this position to negotiate lower prices or more favorable contract terms, impacting Proact's profitability.

While Proact's broad customer spread generally dilutes individual customer power, the importance of large enterprise contracts cannot be understated. For instance, in 2023, Proact reported that its top ten customers accounted for approximately 20% of its total revenue, highlighting the continued influence of its larger clients.

Switching Costs for Customers

Migrating data and applications between data centers or cloud providers is a complex and costly undertaking, often involving significant time and potential disruption to business operations. These substantial switching costs typically diminish a customer's bargaining power, as the effort required to switch to a competitor becomes a deterrent.

ProAct's business model, which deeply integrates with client data lifecycles, further amplifies these switching costs. For instance, in 2024, the average cost for an enterprise to migrate its data center infrastructure was estimated to be in the millions of dollars, with some projects exceeding tens of millions, depending on data volume and complexity.

Availability of Alternative Service Providers

The European data center and cloud services market is highly fragmented, offering customers a wide array of choices. This abundance of colocation providers, managed service providers, and major hyperscale cloud players like AWS, Azure, and Google Cloud significantly amplifies customer bargaining power. When services are standardized, customers can easily switch providers, demanding better pricing and terms.

For instance, in 2024, the global cloud computing market was projected to reach over $600 billion, indicating intense competition among providers to attract and retain customers. This competitive landscape means that customers, especially those with predictable and large-scale needs, can negotiate favorable contracts.

Proact distinguishes itself in this environment by focusing on specialized consulting services and tailored hybrid cloud solutions. This differentiation strategy aims to reduce the commoditization of its offerings, thereby mitigating the direct impact of customer bargaining power driven solely by the availability of alternatives.

Customer Price Sensitivity

Customer price sensitivity is a significant factor for IT infrastructure and cloud service providers like Proact, particularly when economic uncertainty prevails. Customers actively compare pricing across different vendors, intensifying pressure to optimize IT budgets. This competitive landscape necessitates Proact maintaining competitive pricing structures.

The ability for customers to easily compare prices across various IT infrastructure and cloud service providers directly impacts Proact's pricing power. In 2024, many businesses are still focused on cost optimization, making price a primary decision-making criterion. For instance, a report from Gartner in late 2023 indicated that over 60% of IT leaders were prioritizing cost reduction initiatives for the upcoming fiscal year.

- Price Comparison Tools: The proliferation of online comparison platforms and readily available pricing information empowers customers to easily benchmark Proact's offerings against competitors.

- Budgetary Constraints: Many organizations are operating under tight IT budgets in 2024, leading to a heightened sensitivity to the overall cost of services.

- Value-Based Justification: Proact often counters price sensitivity by emphasizing its value proposition, focusing on efficiency gains and maximizing value extraction to justify its pricing.

Threat of Customer Backward Integration

The threat of customer backward integration, where customers build their own capabilities, can significantly impact an industry. For instance, large enterprises might opt to develop or expand their on-premise data centers or manage their cloud infrastructure directly, particularly when dealing with highly sensitive data or strict regulatory compliance. This strategic move allows them to lessen their dependence on external service providers.

This capability of backward integration, however, is often constrained by the considerable complexity, substantial costs, and the need for specialized expertise. These factors collectively limit the feasibility of such endeavors for a broad spectrum of customers.

- High Capital Investment: Building and maintaining data centers can require billions of dollars in upfront capital, deterring many potential integrators. For example, a hyperscale data center can cost upwards of $1 billion to construct.

- Technical Expertise Gap: Operating and securing advanced IT infrastructure demands highly specialized skills that many companies may not possess internally. The global shortage of cybersecurity professionals, estimated at 3.4 million in 2024, highlights this challenge.

- Scalability and Flexibility Issues: In-house solutions may struggle to match the scalability and flexibility offered by specialized cloud providers, especially during periods of rapid growth or fluctuating demand.

Customer Bargaining Power in IT & Cloud Services: Key Factors

The bargaining power of customers in the IT infrastructure and cloud services sector is influenced by several factors, including switching costs, market fragmentation, and price sensitivity. Proact's strategy of offering specialized consulting and tailored solutions aims to differentiate its services and reduce commoditization, thereby lessening customer leverage.

High switching costs, stemming from the complexity and expense of migrating data and applications, generally limit customer power. However, the highly fragmented European market, with numerous providers, empowers customers to easily compare and switch, demanding better terms. In 2024, businesses remain focused on cost optimization, making price a critical decision factor, with many IT leaders prioritizing cost reduction initiatives.

The threat of backward integration, where customers build their own capabilities, is often mitigated by the substantial capital investment, technical expertise required, and scalability challenges. For instance, constructing a hyperscale data center can cost over $1 billion, and the global cybersecurity talent shortage in 2024 highlights the expertise gap.

| Factor | Impact on Customer Bargaining Power | Proact's Mitigation Strategy | Supporting Data (2024 Estimates/Trends) |

|---|---|---|---|

| Switching Costs | Lowers customer power due to migration complexity and expense. | Deep integration with client data lifecycles. | Enterprise data center migration costs can reach millions of dollars. |

| Market Fragmentation | Increases customer power due to abundant choices and easy comparison. | Focus on specialized consulting and tailored hybrid cloud solutions. | Global cloud computing market projected over $600 billion, indicating intense competition. |

| Price Sensitivity | Increases customer power, especially during economic uncertainty. | Emphasize value proposition, efficiency gains, and justifiable pricing. | Over 60% of IT leaders prioritized cost reduction in late 2023. |

| Backward Integration Threat | Lowers customer power due to high capital, expertise, and scalability barriers. | N/A (inherent industry barrier). | Hyperscale data center construction costs exceed $1 billion; 3.4 million cybersecurity professionals needed globally in 2024. |

Same Document Delivered

ProAct Porter's Five Forces Analysis

The document you see here is the complete ProAct Porter's Five Forces Analysis, exactly as it will be delivered upon purchase. This comprehensive analysis, covering all essential components of Porter's framework, is ready for immediate download and application. You're previewing the final, professionally formatted version, ensuring you receive precisely what you need to understand competitive forces.

A Must-Have Tool for Decision-Makers

ProAct's competitive landscape is shaped by powerful forces, from the intense rivalry among existing players to the constant threat of new entrants disrupting the market. Understanding these dynamics is crucial for any business aiming to thrive.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ProAct’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Key Technology Vendors

Proact's reliance on a limited number of key technology vendors for its data center and cloud solutions, like NetApp and VMware, significantly impacts supplier bargaining power. When these markets are concentrated, a few dominant suppliers can dictate pricing and contract terms, potentially increasing Proact's operational costs.

The strategic importance of Proact's partnerships and certifications with these critical infrastructure providers highlights their leverage. These relationships are not just about sourcing; they are foundational to the quality and comprehensiveness of Proact's service delivery.

Switching Costs for Proact

Switching core technology suppliers, such as for storage platforms or virtualization software, presents significant hurdles for Proact. These transitions can incur substantial costs related to retraining personnel, re-engineering existing solutions, and the potential for service interruptions for clients. For instance, a major cloud provider change could cost millions in migration and validation efforts.

These elevated switching costs inherently bolster the bargaining power of Proact's current, established technology vendors. While Proact's expertise in integrating various technologies offers some flexibility, fundamental shifts in core infrastructure remain a costly undertaking, reinforcing supplier leverage.

Uniqueness and Differentiation of Supplier Offerings

Suppliers offering highly specialized or proprietary technologies, such as those in advanced data protection or AI infrastructure, wield significant bargaining power. If Proact relies on a supplier's unique product with few viable alternatives, its ability to negotiate favorable terms diminishes. For instance, the burgeoning demand for AI infrastructure in 2024 is likely to further bolster the negotiating leverage of niche technology providers in this space, potentially increasing component costs.

Threat of Forward Integration by Suppliers

Large technology providers, particularly those with cloud offerings like Microsoft Azure and Amazon Web Services (AWS), present a potential threat by being able to offer services directly to Proact's clients, effectively cutting out Proact. This risk is less pronounced for Proact's specialized managed services, which often involve complex, multi-vendor integrations. However, it underscores the imperative for Proact to consistently demonstrate value beyond mere infrastructure management to maintain its competitive edge.

For instance, in 2024, cloud infrastructure spending continued its robust growth, with AWS and Microsoft Azure holding significant market shares. AWS reported over $65 billion in revenue for 2023, and Microsoft's Intelligent Cloud segment, which includes Azure, saw substantial growth. This indicates the scale of these players and their potential to leverage their platforms for direct customer engagement.

- Direct Service Offering: Major cloud providers can bundle managed services with their core cloud products, potentially offering a more integrated solution to customers.

- Value Proposition Differentiation: Proact must continually enhance its service offerings to provide unique value that cannot be easily replicated by these large technology suppliers.

- Partnership Dynamics: Maintaining strong, collaborative relationships with these suppliers is crucial to mitigate the threat and leverage their platforms effectively.

Availability of Substitute Inputs

The availability of substitute inputs significantly impacts supplier bargaining power. When numerous alternatives exist for a component, customers can switch more easily, diminishing the supplier's leverage. For instance, the rise of open-source software and readily available commodity hardware for data centers can dilute the power of traditional proprietary vendors.

ProAct's business model, focused on flexible IT solutions, is well-positioned to capitalize on this. By utilizing a diverse range of inputs for non-specialized needs, ProAct can reduce its reliance on any single supplier. This strategy is particularly effective for components like standard server racks or basic networking equipment where multiple manufacturers offer comparable products.

However, the situation shifts for specialized hardware and software critical to data center operations. For these bespoke or proprietary solutions, the availability of direct substitutes can be quite limited. For example, advanced AI processing units or highly integrated cloud management platforms may have few, if any, direct alternatives, thereby strengthening the bargaining power of the suppliers offering them.

- Limited Substitutes for Specialized Hardware: In 2024, the global market for high-performance computing (HPC) hardware, including specialized GPUs and AI accelerators, saw continued consolidation, with a few key players dominating. This limited the availability of direct substitutes, potentially increasing supplier power for ProAct when sourcing these critical components.

- Open-Source Adoption Growth: Conversely, the adoption of open-source solutions in areas like operating systems and containerization continued to grow. In 2024, estimates suggest that over 70% of enterprise workloads ran on Linux-based systems, providing ProAct with significant leverage when negotiating with providers of commodity server components and related software.

- Commodity Component Price Volatility: While substitutes exist for many commodity IT components, their prices can be subject to significant volatility based on global supply chain dynamics. For example, fluctuations in the cost of memory chips or solid-state drives in 2024 demonstrated how even with multiple suppliers, market conditions can temporarily shift bargaining power.

- ProAct's Diversification Strategy: ProAct’s strategy to offer flexible IT solutions inherently involves building relationships with a broad base of suppliers. This diversification mitigates the risk of over-reliance on any single vendor for non-specialized equipment, thereby maintaining a degree of control over input costs and availability.

Supplier Power: Impact on Operational Costs and Strategic Flexibility

The bargaining power of suppliers significantly influences ProAct's operational costs and strategic flexibility. When suppliers offer highly specialized or proprietary technologies, like advanced AI infrastructure components in 2024, their leverage increases due to limited alternatives.

High switching costs associated with core technology vendors, such as for virtualization software, further empower these suppliers. These costs, encompassing retraining and potential service disruptions, can run into millions, reinforcing vendor control over pricing and terms.

The availability of substitute inputs is a key factor; while commodity IT components have many alternatives, specialized hardware for areas like AI in 2024 saw limited substitutes, strengthening supplier positions. ProAct's diversification strategy helps mitigate this for non-specialized needs.

| Supplier Characteristic | Impact on ProAct | 2024 Context/Data |

|---|---|---|

| Concentrated Market / Few Dominant Players | Increased supplier leverage, potential for higher pricing | Cloud infrastructure dominated by AWS and Microsoft Azure, with significant market share growth in 2023. |

| High Switching Costs for ProAct | Reinforces existing supplier power, reduces ProAct's negotiation flexibility | Migrating core cloud infrastructure can cost millions, making transitions difficult. |

| Proprietary/Specialized Offerings | Strong supplier bargaining power due to lack of direct substitutes | AI hardware market in 2024 showed consolidation, limiting alternatives for high-performance components. |

| Availability of Substitutes | Weakens supplier power for commodity inputs, strengthens for specialized ones | Over 70% of enterprise workloads ran on Linux in 2024, providing leverage for commodity server needs. |

What is included in the product

ProAct's Porter's Five Forces Analysis dissects the competitive intensity within its industry, examining threats from new entrants, the power of buyers and suppliers, the availability of substitutes, and the rivalry among existing competitors.

ProAct Porter's Five Forces Analysis pinpoints and quantifies competitive pressures, allowing you to proactively address threats before they impact profitability.

Customers Bargaining Power

Customer Concentration and Size

Proact's customer base spans across Europe, serving both small and medium-sized enterprises (SMEs) and larger corporations. This diversity is a key strength, as it reduces reliance on any single client.

However, if a substantial portion of Proact's revenue is concentrated among a few major clients, these large customers would possess significant bargaining power. They could leverage this position to negotiate lower prices or more favorable contract terms, impacting Proact's profitability.

While Proact's broad customer spread generally dilutes individual customer power, the importance of large enterprise contracts cannot be understated. For instance, in 2023, Proact reported that its top ten customers accounted for approximately 20% of its total revenue, highlighting the continued influence of its larger clients.

Switching Costs for Customers

Migrating data and applications between data centers or cloud providers is a complex and costly undertaking, often involving significant time and potential disruption to business operations. These substantial switching costs typically diminish a customer's bargaining power, as the effort required to switch to a competitor becomes a deterrent.

ProAct's business model, which deeply integrates with client data lifecycles, further amplifies these switching costs. For instance, in 2024, the average cost for an enterprise to migrate its data center infrastructure was estimated to be in the millions of dollars, with some projects exceeding tens of millions, depending on data volume and complexity.

Availability of Alternative Service Providers

The European data center and cloud services market is highly fragmented, offering customers a wide array of choices. This abundance of colocation providers, managed service providers, and major hyperscale cloud players like AWS, Azure, and Google Cloud significantly amplifies customer bargaining power. When services are standardized, customers can easily switch providers, demanding better pricing and terms.

For instance, in 2024, the global cloud computing market was projected to reach over $600 billion, indicating intense competition among providers to attract and retain customers. This competitive landscape means that customers, especially those with predictable and large-scale needs, can negotiate favorable contracts.

Proact distinguishes itself in this environment by focusing on specialized consulting services and tailored hybrid cloud solutions. This differentiation strategy aims to reduce the commoditization of its offerings, thereby mitigating the direct impact of customer bargaining power driven solely by the availability of alternatives.

Customer Price Sensitivity

Customer price sensitivity is a significant factor for IT infrastructure and cloud service providers like Proact, particularly when economic uncertainty prevails. Customers actively compare pricing across different vendors, intensifying pressure to optimize IT budgets. This competitive landscape necessitates Proact maintaining competitive pricing structures.

The ability for customers to easily compare prices across various IT infrastructure and cloud service providers directly impacts Proact's pricing power. In 2024, many businesses are still focused on cost optimization, making price a primary decision-making criterion. For instance, a report from Gartner in late 2023 indicated that over 60% of IT leaders were prioritizing cost reduction initiatives for the upcoming fiscal year.

- Price Comparison Tools: The proliferation of online comparison platforms and readily available pricing information empowers customers to easily benchmark Proact's offerings against competitors.

- Budgetary Constraints: Many organizations are operating under tight IT budgets in 2024, leading to a heightened sensitivity to the overall cost of services.

- Value-Based Justification: Proact often counters price sensitivity by emphasizing its value proposition, focusing on efficiency gains and maximizing value extraction to justify its pricing.

Threat of Customer Backward Integration

The threat of customer backward integration, where customers build their own capabilities, can significantly impact an industry. For instance, large enterprises might opt to develop or expand their on-premise data centers or manage their cloud infrastructure directly, particularly when dealing with highly sensitive data or strict regulatory compliance. This strategic move allows them to lessen their dependence on external service providers.

This capability of backward integration, however, is often constrained by the considerable complexity, substantial costs, and the need for specialized expertise. These factors collectively limit the feasibility of such endeavors for a broad spectrum of customers.

- High Capital Investment: Building and maintaining data centers can require billions of dollars in upfront capital, deterring many potential integrators. For example, a hyperscale data center can cost upwards of $1 billion to construct.

- Technical Expertise Gap: Operating and securing advanced IT infrastructure demands highly specialized skills that many companies may not possess internally. The global shortage of cybersecurity professionals, estimated at 3.4 million in 2024, highlights this challenge.

- Scalability and Flexibility Issues: In-house solutions may struggle to match the scalability and flexibility offered by specialized cloud providers, especially during periods of rapid growth or fluctuating demand.

Customer Bargaining Power in IT & Cloud Services: Key Factors

The bargaining power of customers in the IT infrastructure and cloud services sector is influenced by several factors, including switching costs, market fragmentation, and price sensitivity. Proact's strategy of offering specialized consulting and tailored solutions aims to differentiate its services and reduce commoditization, thereby lessening customer leverage.

High switching costs, stemming from the complexity and expense of migrating data and applications, generally limit customer power. However, the highly fragmented European market, with numerous providers, empowers customers to easily compare and switch, demanding better terms. In 2024, businesses remain focused on cost optimization, making price a critical decision factor, with many IT leaders prioritizing cost reduction initiatives.

The threat of backward integration, where customers build their own capabilities, is often mitigated by the substantial capital investment, technical expertise required, and scalability challenges. For instance, constructing a hyperscale data center can cost over $1 billion, and the global cybersecurity talent shortage in 2024 highlights the expertise gap.

| Factor | Impact on Customer Bargaining Power | Proact's Mitigation Strategy | Supporting Data (2024 Estimates/Trends) |

|---|---|---|---|

| Switching Costs | Lowers customer power due to migration complexity and expense. | Deep integration with client data lifecycles. | Enterprise data center migration costs can reach millions of dollars. |

| Market Fragmentation | Increases customer power due to abundant choices and easy comparison. | Focus on specialized consulting and tailored hybrid cloud solutions. | Global cloud computing market projected over $600 billion, indicating intense competition. |

| Price Sensitivity | Increases customer power, especially during economic uncertainty. | Emphasize value proposition, efficiency gains, and justifiable pricing. | Over 60% of IT leaders prioritized cost reduction in late 2023. |

| Backward Integration Threat | Lowers customer power due to high capital, expertise, and scalability barriers. | N/A (inherent industry barrier). | Hyperscale data center construction costs exceed $1 billion; 3.4 million cybersecurity professionals needed globally in 2024. |

Same Document Delivered

ProAct Porter's Five Forces Analysis

The document you see here is the complete ProAct Porter's Five Forces Analysis, exactly as it will be delivered upon purchase. This comprehensive analysis, covering all essential components of Porter's framework, is ready for immediate download and application. You're previewing the final, professionally formatted version, ensuring you receive precisely what you need to understand competitive forces.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

ProAct's competitive landscape is shaped by powerful forces, from the intense rivalry among existing players to the constant threat of new entrants disrupting the market. Understanding these dynamics is crucial for any business aiming to thrive.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ProAct’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Key Technology Vendors

Proact's reliance on a limited number of key technology vendors for its data center and cloud solutions, like NetApp and VMware, significantly impacts supplier bargaining power. When these markets are concentrated, a few dominant suppliers can dictate pricing and contract terms, potentially increasing Proact's operational costs.

The strategic importance of Proact's partnerships and certifications with these critical infrastructure providers highlights their leverage. These relationships are not just about sourcing; they are foundational to the quality and comprehensiveness of Proact's service delivery.

Switching Costs for Proact

Switching core technology suppliers, such as for storage platforms or virtualization software, presents significant hurdles for Proact. These transitions can incur substantial costs related to retraining personnel, re-engineering existing solutions, and the potential for service interruptions for clients. For instance, a major cloud provider change could cost millions in migration and validation efforts.

These elevated switching costs inherently bolster the bargaining power of Proact's current, established technology vendors. While Proact's expertise in integrating various technologies offers some flexibility, fundamental shifts in core infrastructure remain a costly undertaking, reinforcing supplier leverage.

Uniqueness and Differentiation of Supplier Offerings

Suppliers offering highly specialized or proprietary technologies, such as those in advanced data protection or AI infrastructure, wield significant bargaining power. If Proact relies on a supplier's unique product with few viable alternatives, its ability to negotiate favorable terms diminishes. For instance, the burgeoning demand for AI infrastructure in 2024 is likely to further bolster the negotiating leverage of niche technology providers in this space, potentially increasing component costs.

Threat of Forward Integration by Suppliers

Large technology providers, particularly those with cloud offerings like Microsoft Azure and Amazon Web Services (AWS), present a potential threat by being able to offer services directly to Proact's clients, effectively cutting out Proact. This risk is less pronounced for Proact's specialized managed services, which often involve complex, multi-vendor integrations. However, it underscores the imperative for Proact to consistently demonstrate value beyond mere infrastructure management to maintain its competitive edge.

For instance, in 2024, cloud infrastructure spending continued its robust growth, with AWS and Microsoft Azure holding significant market shares. AWS reported over $65 billion in revenue for 2023, and Microsoft's Intelligent Cloud segment, which includes Azure, saw substantial growth. This indicates the scale of these players and their potential to leverage their platforms for direct customer engagement.

- Direct Service Offering: Major cloud providers can bundle managed services with their core cloud products, potentially offering a more integrated solution to customers.

- Value Proposition Differentiation: Proact must continually enhance its service offerings to provide unique value that cannot be easily replicated by these large technology suppliers.

- Partnership Dynamics: Maintaining strong, collaborative relationships with these suppliers is crucial to mitigate the threat and leverage their platforms effectively.

Availability of Substitute Inputs

The availability of substitute inputs significantly impacts supplier bargaining power. When numerous alternatives exist for a component, customers can switch more easily, diminishing the supplier's leverage. For instance, the rise of open-source software and readily available commodity hardware for data centers can dilute the power of traditional proprietary vendors.

ProAct's business model, focused on flexible IT solutions, is well-positioned to capitalize on this. By utilizing a diverse range of inputs for non-specialized needs, ProAct can reduce its reliance on any single supplier. This strategy is particularly effective for components like standard server racks or basic networking equipment where multiple manufacturers offer comparable products.

However, the situation shifts for specialized hardware and software critical to data center operations. For these bespoke or proprietary solutions, the availability of direct substitutes can be quite limited. For example, advanced AI processing units or highly integrated cloud management platforms may have few, if any, direct alternatives, thereby strengthening the bargaining power of the suppliers offering them.

- Limited Substitutes for Specialized Hardware: In 2024, the global market for high-performance computing (HPC) hardware, including specialized GPUs and AI accelerators, saw continued consolidation, with a few key players dominating. This limited the availability of direct substitutes, potentially increasing supplier power for ProAct when sourcing these critical components.

- Open-Source Adoption Growth: Conversely, the adoption of open-source solutions in areas like operating systems and containerization continued to grow. In 2024, estimates suggest that over 70% of enterprise workloads ran on Linux-based systems, providing ProAct with significant leverage when negotiating with providers of commodity server components and related software.

- Commodity Component Price Volatility: While substitutes exist for many commodity IT components, their prices can be subject to significant volatility based on global supply chain dynamics. For example, fluctuations in the cost of memory chips or solid-state drives in 2024 demonstrated how even with multiple suppliers, market conditions can temporarily shift bargaining power.

- ProAct's Diversification Strategy: ProAct’s strategy to offer flexible IT solutions inherently involves building relationships with a broad base of suppliers. This diversification mitigates the risk of over-reliance on any single vendor for non-specialized equipment, thereby maintaining a degree of control over input costs and availability.

Supplier Power: Impact on Operational Costs and Strategic Flexibility

The bargaining power of suppliers significantly influences ProAct's operational costs and strategic flexibility. When suppliers offer highly specialized or proprietary technologies, like advanced AI infrastructure components in 2024, their leverage increases due to limited alternatives.

High switching costs associated with core technology vendors, such as for virtualization software, further empower these suppliers. These costs, encompassing retraining and potential service disruptions, can run into millions, reinforcing vendor control over pricing and terms.

The availability of substitute inputs is a key factor; while commodity IT components have many alternatives, specialized hardware for areas like AI in 2024 saw limited substitutes, strengthening supplier positions. ProAct's diversification strategy helps mitigate this for non-specialized needs.

| Supplier Characteristic | Impact on ProAct | 2024 Context/Data |

|---|---|---|

| Concentrated Market / Few Dominant Players | Increased supplier leverage, potential for higher pricing | Cloud infrastructure dominated by AWS and Microsoft Azure, with significant market share growth in 2023. |

| High Switching Costs for ProAct | Reinforces existing supplier power, reduces ProAct's negotiation flexibility | Migrating core cloud infrastructure can cost millions, making transitions difficult. |

| Proprietary/Specialized Offerings | Strong supplier bargaining power due to lack of direct substitutes | AI hardware market in 2024 showed consolidation, limiting alternatives for high-performance components. |

| Availability of Substitutes | Weakens supplier power for commodity inputs, strengthens for specialized ones | Over 70% of enterprise workloads ran on Linux in 2024, providing leverage for commodity server needs. |

What is included in the product

ProAct's Porter's Five Forces Analysis dissects the competitive intensity within its industry, examining threats from new entrants, the power of buyers and suppliers, the availability of substitutes, and the rivalry among existing competitors.

ProAct Porter's Five Forces Analysis pinpoints and quantifies competitive pressures, allowing you to proactively address threats before they impact profitability.

Customers Bargaining Power

Customer Concentration and Size

Proact's customer base spans across Europe, serving both small and medium-sized enterprises (SMEs) and larger corporations. This diversity is a key strength, as it reduces reliance on any single client.

However, if a substantial portion of Proact's revenue is concentrated among a few major clients, these large customers would possess significant bargaining power. They could leverage this position to negotiate lower prices or more favorable contract terms, impacting Proact's profitability.

While Proact's broad customer spread generally dilutes individual customer power, the importance of large enterprise contracts cannot be understated. For instance, in 2023, Proact reported that its top ten customers accounted for approximately 20% of its total revenue, highlighting the continued influence of its larger clients.

Switching Costs for Customers

Migrating data and applications between data centers or cloud providers is a complex and costly undertaking, often involving significant time and potential disruption to business operations. These substantial switching costs typically diminish a customer's bargaining power, as the effort required to switch to a competitor becomes a deterrent.

ProAct's business model, which deeply integrates with client data lifecycles, further amplifies these switching costs. For instance, in 2024, the average cost for an enterprise to migrate its data center infrastructure was estimated to be in the millions of dollars, with some projects exceeding tens of millions, depending on data volume and complexity.

Availability of Alternative Service Providers

The European data center and cloud services market is highly fragmented, offering customers a wide array of choices. This abundance of colocation providers, managed service providers, and major hyperscale cloud players like AWS, Azure, and Google Cloud significantly amplifies customer bargaining power. When services are standardized, customers can easily switch providers, demanding better pricing and terms.

For instance, in 2024, the global cloud computing market was projected to reach over $600 billion, indicating intense competition among providers to attract and retain customers. This competitive landscape means that customers, especially those with predictable and large-scale needs, can negotiate favorable contracts.

Proact distinguishes itself in this environment by focusing on specialized consulting services and tailored hybrid cloud solutions. This differentiation strategy aims to reduce the commoditization of its offerings, thereby mitigating the direct impact of customer bargaining power driven solely by the availability of alternatives.

Customer Price Sensitivity

Customer price sensitivity is a significant factor for IT infrastructure and cloud service providers like Proact, particularly when economic uncertainty prevails. Customers actively compare pricing across different vendors, intensifying pressure to optimize IT budgets. This competitive landscape necessitates Proact maintaining competitive pricing structures.

The ability for customers to easily compare prices across various IT infrastructure and cloud service providers directly impacts Proact's pricing power. In 2024, many businesses are still focused on cost optimization, making price a primary decision-making criterion. For instance, a report from Gartner in late 2023 indicated that over 60% of IT leaders were prioritizing cost reduction initiatives for the upcoming fiscal year.

- Price Comparison Tools: The proliferation of online comparison platforms and readily available pricing information empowers customers to easily benchmark Proact's offerings against competitors.

- Budgetary Constraints: Many organizations are operating under tight IT budgets in 2024, leading to a heightened sensitivity to the overall cost of services.

- Value-Based Justification: Proact often counters price sensitivity by emphasizing its value proposition, focusing on efficiency gains and maximizing value extraction to justify its pricing.

Threat of Customer Backward Integration

The threat of customer backward integration, where customers build their own capabilities, can significantly impact an industry. For instance, large enterprises might opt to develop or expand their on-premise data centers or manage their cloud infrastructure directly, particularly when dealing with highly sensitive data or strict regulatory compliance. This strategic move allows them to lessen their dependence on external service providers.

This capability of backward integration, however, is often constrained by the considerable complexity, substantial costs, and the need for specialized expertise. These factors collectively limit the feasibility of such endeavors for a broad spectrum of customers.

- High Capital Investment: Building and maintaining data centers can require billions of dollars in upfront capital, deterring many potential integrators. For example, a hyperscale data center can cost upwards of $1 billion to construct.

- Technical Expertise Gap: Operating and securing advanced IT infrastructure demands highly specialized skills that many companies may not possess internally. The global shortage of cybersecurity professionals, estimated at 3.4 million in 2024, highlights this challenge.

- Scalability and Flexibility Issues: In-house solutions may struggle to match the scalability and flexibility offered by specialized cloud providers, especially during periods of rapid growth or fluctuating demand.

Customer Bargaining Power in IT & Cloud Services: Key Factors

The bargaining power of customers in the IT infrastructure and cloud services sector is influenced by several factors, including switching costs, market fragmentation, and price sensitivity. Proact's strategy of offering specialized consulting and tailored solutions aims to differentiate its services and reduce commoditization, thereby lessening customer leverage.

High switching costs, stemming from the complexity and expense of migrating data and applications, generally limit customer power. However, the highly fragmented European market, with numerous providers, empowers customers to easily compare and switch, demanding better terms. In 2024, businesses remain focused on cost optimization, making price a critical decision factor, with many IT leaders prioritizing cost reduction initiatives.

The threat of backward integration, where customers build their own capabilities, is often mitigated by the substantial capital investment, technical expertise required, and scalability challenges. For instance, constructing a hyperscale data center can cost over $1 billion, and the global cybersecurity talent shortage in 2024 highlights the expertise gap.

| Factor | Impact on Customer Bargaining Power | Proact's Mitigation Strategy | Supporting Data (2024 Estimates/Trends) |

|---|---|---|---|

| Switching Costs | Lowers customer power due to migration complexity and expense. | Deep integration with client data lifecycles. | Enterprise data center migration costs can reach millions of dollars. |

| Market Fragmentation | Increases customer power due to abundant choices and easy comparison. | Focus on specialized consulting and tailored hybrid cloud solutions. | Global cloud computing market projected over $600 billion, indicating intense competition. |

| Price Sensitivity | Increases customer power, especially during economic uncertainty. | Emphasize value proposition, efficiency gains, and justifiable pricing. | Over 60% of IT leaders prioritized cost reduction in late 2023. |

| Backward Integration Threat | Lowers customer power due to high capital, expertise, and scalability barriers. | N/A (inherent industry barrier). | Hyperscale data center construction costs exceed $1 billion; 3.4 million cybersecurity professionals needed globally in 2024. |

Same Document Delivered

ProAct Porter's Five Forces Analysis

The document you see here is the complete ProAct Porter's Five Forces Analysis, exactly as it will be delivered upon purchase. This comprehensive analysis, covering all essential components of Porter's framework, is ready for immediate download and application. You're previewing the final, professionally formatted version, ensuring you receive precisely what you need to understand competitive forces.