ProAct PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our PESTLE Analysis of ProAct—concise, evidence-based insights into political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors, consultants and strategists, it saves research time and supports decision-making with actionable conclusions. Purchase the full report to access the complete, editable analysis and immediate strategic intelligence.

Political factors

EU digital policy shifts

Changing EU agendas on digital sovereignty and industrial policy steer cloud and local data strategies, driven by NextGenerationEU (€806.9bn) and Digital Europe funding (€7.5bn for 2021–27) that allocate grants and procurement preferences. Funding and incentives increasingly favor regional providers and projects aligned with the Chips Act (public/private mobilization ~€43bn). Proact can align offerings to national and EU priorities to capture public and regulated contracts. Policy reversals or delays, however, create planning uncertainty for multi-year bids.

Geopolitical tensions and sanctions

Since the Russia‑Ukraine war began in Feb 2022 and with Middle East escalation after Oct 2023, widening US and EU export controls (notably restrictions on advanced chips and design tools) have strained supply chains and vendor availability. Sanctions already limit access to hardware, chips and vendor support, forcing ProAct to diversify suppliers and hold larger inventory buffers. Clients will increasingly demand documented geopolitical‑risk assurances and supply‑continuity SLAs.

Public sector procurement dynamics

Government cloud-first and security-first mandates are driving stronger public sector demand for certified cloud services. The EU public procurement market is roughly €2 trillion annually, where certification and local hosting preferences can be barriers or competitive advantages. Proact can leverage regional data centers to meet tender criteria and data-residency rules. Long procurement cycles, often 6–12 months, reduce cash flow visibility for providers.

Brexit and cross-border operations

Brexit-driven UK-EU regulatory divergence—despite the EU adequacy decision for the UK (June 2021, still in force in 2025)—complicates data transfers, certifications and staffing for ProAct, while customs frictions increase hardware transit times and costs. ProAct requires mirrored services and dual compliance footprints across UK/EU and agile pricing to manage sterling/euro/regulatory volatility.

- Data: EU adequacy decision (June 2021) in force

- Operations: dual compliance + mirrored services required

- Risk: customs delays inflate hardware costs; price agility needed

Cybersecurity national strategies

National critical infrastructure policies are raising security baselines and driving ~10% year‑over‑year public cyberbudget growth in 2024, boosting demand for managed security and resilient backup; average breach cost remains high at $4.45M (IBM, 2023), making compliance a buying priority. Proact can package compliance‑led services for regulated sectors as 78% of buyers cite compliance as a top supplier filter.

- Policy: raised baselines, tighter controls

- Funding: ~10% YoY public cyberbudget growth (2024)

- Cost risk: average breach $4.45M (2023)

- Buyer shift: 78% prioritize compliance‑certified vendors

EU funds and Chips Act lift regional procurement; export controls force bigger inventories

EU digital sovereignty funds (NextGenerationEU €806.9bn; Digital Europe €7.5bn 2021–27) and Chips Act (~€43bn) steer procurement to regional suppliers, creating tender opportunities but planning uncertainty. Export controls since 2022 and post‑Oct 2023 Middle East escalation force supply diversification and bigger inventories. Public sector demand rises (EU procurement ~€2tn/yr; public cyber budgets + ~10% YoY in 2024).

| Metric | Value |

|---|---|

| NextGenerationEU | €806.9bn |

| Digital Europe | €7.5bn (2021–27) |

| Chips Act | ~€43bn |

| EU procurement | ~€2tn/yr |

| Public cyber budgets | +~10% YoY (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect ProAct across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region-specific trends and forward-looking insights to help executives identify threats, opportunities and strategic responses.

Condenses the full PESTLE into a clean, visually segmented summary that’s editable for region- or business-specific notes, easily dropped into presentations and shared across teams for fast alignment during planning sessions.

Economic factors

IT spend cycles and GDP growth

Enterprise IT budgets closely track macro growth and inflation: IMF WEO projects global GDP growth of 3.1% in 2024 and 3.0% in 2025 while Gartner forecast global IT spending to rise ~4% in 2024 to about 5.3 trillion USD. Economic slowdowns typically defer capex but accelerate opex for managed services; Proact can pivot between project-based engagements and as-a-service offerings to stabilize revenue. A diversified vertical mix further hedges cyclicality by offsetting sector-specific downturns.

Energy price volatility

Data centers are energy intensive and exposed to price spikes, with IEA estimating they consumed about 200 TWh (~1% of global electricity) in 2022, pressuring margins during volatile markets. Long-term PPAs and efficiency upgrades (lowering PUE and energy per compute) protect unit economics. Proact can pass through or index energy costs in SLAs to stabilize cash flow. Clients prioritize predictable total cost of ownership when procuring services.

Currency fluctuations (EUR/GBP/SEK)

Multi-country operations expose ProAct to FX risk as EUR/GBP ≈0.86 and EUR/SEK ≈11.60 (July 2025), affecting service revenues and hardware imports; 2024–25 intra-year moves of 5–8% materially shift margins. Active hedging and local-currency pricing reduce volatility, while balancing sourcing and billing currencies limits mismatch. Transparent, contract-stated surcharges preserve margins and prevent client bill shock.

Hardware supply and pricing cycles

Server, storage and GPU supply constraints raised lead times to 8–16 weeks and pushed datacenter GPU prices down ~20–30% in 2024 as inventories normalized, forcing ProAct to manage project backlogs with phased rollouts and tight expectation controls; services revenue helped offset hardware margin compression.

- Standardize SKUs

- Multi-vendor sourcing

- Phased rollouts to reduce churn

- Services mix cushions margins

M&A and market consolidation

European MSP/DC markets continue consolidating for scale and reach; Proact can accelerate capability acquisition in security, AI and edge while protecting customer satisfaction through disciplined integration. Private-equity dry powder remained around $2.1 trillion in 2024, intensifying PE-backed rollups and pricing pressure across Europe.

- Consolidation: scale + reach

- Targets: security, AI, edge

- Integration: preserves CSAT & synergies

- Risk: PE rollups heighten pricing pressure

EU funds and Chips Act lift regional procurement; export controls force bigger inventories

Global GDP ~3.1% (2024) and 3.0% (2025, IMF) while global IT spend +~4% to $5.3T (2024, Gartner); Proact must balance capex vs opex. Data centers ~200 TWh (2022, IEA) → energy hedges/efficiency vital. EUR/GBP 0.86, EUR/SEK 11.60 (Jul 2025) — FX hedging needed. GPU prices fell 20–30% (2024); PE dry powder ~$2.1T fuels consolidation.

| Metric | Value |

|---|---|

| GDP growth | 3.1%/3.0% |

| IT spend 2024 | $5.3T (+4%) |

| Data center energy | ~200 TWh |

| FX (Jul 2025) | EUR/GBP 0.86; EUR/SEK 11.60 |

| GPU price change 2024 | -20–30% |

| PE dry powder 2024 | $2.1T |

What You See Is What You Get

ProAct PESTLE Analysis

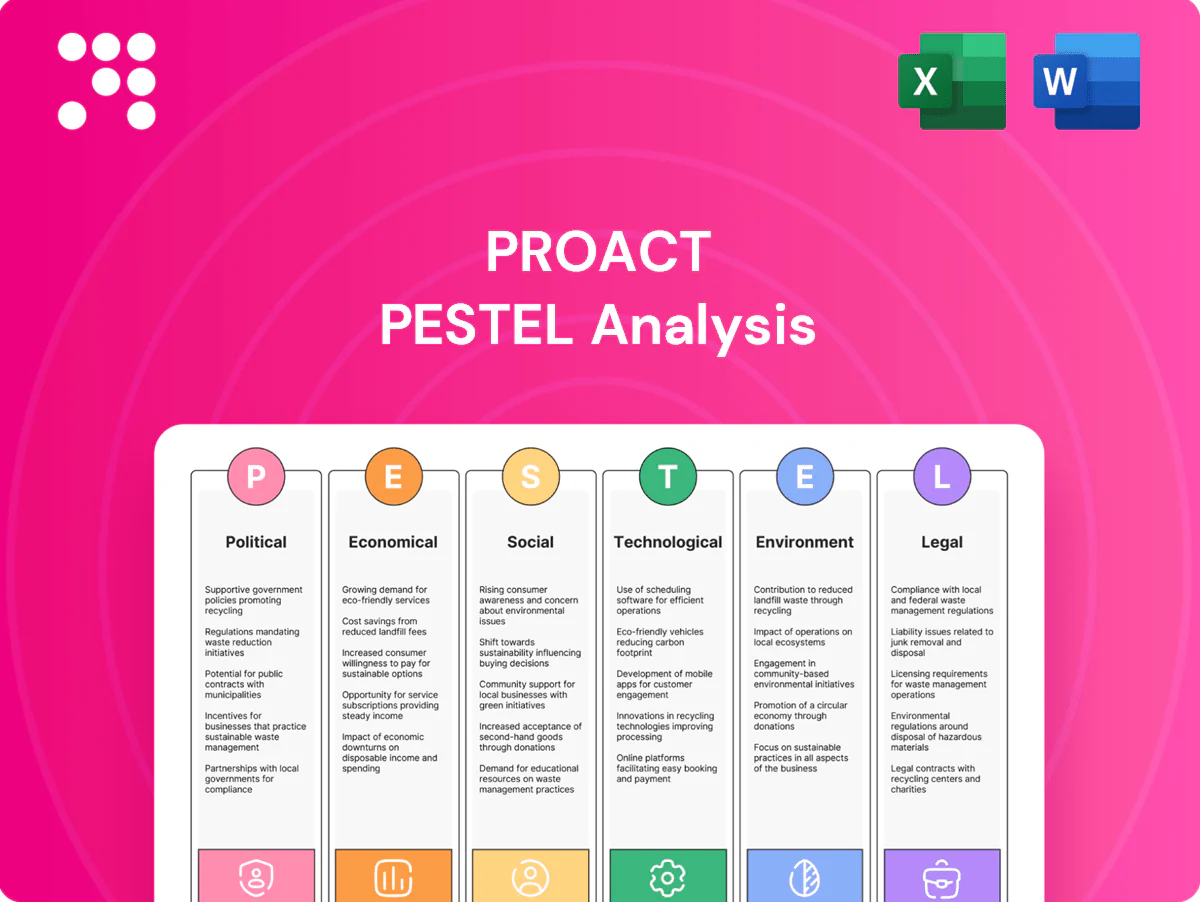

The ProAct PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes complete, professionally structured political, economic, social, technological, legal and environmental assessments. No placeholders or teasers; this is the final file available for immediate download.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our PESTLE Analysis of ProAct—concise, evidence-based insights into political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors, consultants and strategists, it saves research time and supports decision-making with actionable conclusions. Purchase the full report to access the complete, editable analysis and immediate strategic intelligence.

Political factors

EU digital policy shifts

Changing EU agendas on digital sovereignty and industrial policy steer cloud and local data strategies, driven by NextGenerationEU (€806.9bn) and Digital Europe funding (€7.5bn for 2021–27) that allocate grants and procurement preferences. Funding and incentives increasingly favor regional providers and projects aligned with the Chips Act (public/private mobilization ~€43bn). Proact can align offerings to national and EU priorities to capture public and regulated contracts. Policy reversals or delays, however, create planning uncertainty for multi-year bids.

Geopolitical tensions and sanctions

Since the Russia‑Ukraine war began in Feb 2022 and with Middle East escalation after Oct 2023, widening US and EU export controls (notably restrictions on advanced chips and design tools) have strained supply chains and vendor availability. Sanctions already limit access to hardware, chips and vendor support, forcing ProAct to diversify suppliers and hold larger inventory buffers. Clients will increasingly demand documented geopolitical‑risk assurances and supply‑continuity SLAs.

Public sector procurement dynamics

Government cloud-first and security-first mandates are driving stronger public sector demand for certified cloud services. The EU public procurement market is roughly €2 trillion annually, where certification and local hosting preferences can be barriers or competitive advantages. Proact can leverage regional data centers to meet tender criteria and data-residency rules. Long procurement cycles, often 6–12 months, reduce cash flow visibility for providers.

Brexit and cross-border operations

Brexit-driven UK-EU regulatory divergence—despite the EU adequacy decision for the UK (June 2021, still in force in 2025)—complicates data transfers, certifications and staffing for ProAct, while customs frictions increase hardware transit times and costs. ProAct requires mirrored services and dual compliance footprints across UK/EU and agile pricing to manage sterling/euro/regulatory volatility.

- Data: EU adequacy decision (June 2021) in force

- Operations: dual compliance + mirrored services required

- Risk: customs delays inflate hardware costs; price agility needed

Cybersecurity national strategies

National critical infrastructure policies are raising security baselines and driving ~10% year‑over‑year public cyberbudget growth in 2024, boosting demand for managed security and resilient backup; average breach cost remains high at $4.45M (IBM, 2023), making compliance a buying priority. Proact can package compliance‑led services for regulated sectors as 78% of buyers cite compliance as a top supplier filter.

- Policy: raised baselines, tighter controls

- Funding: ~10% YoY public cyberbudget growth (2024)

- Cost risk: average breach $4.45M (2023)

- Buyer shift: 78% prioritize compliance‑certified vendors

EU funds and Chips Act lift regional procurement; export controls force bigger inventories

EU digital sovereignty funds (NextGenerationEU €806.9bn; Digital Europe €7.5bn 2021–27) and Chips Act (~€43bn) steer procurement to regional suppliers, creating tender opportunities but planning uncertainty. Export controls since 2022 and post‑Oct 2023 Middle East escalation force supply diversification and bigger inventories. Public sector demand rises (EU procurement ~€2tn/yr; public cyber budgets + ~10% YoY in 2024).

| Metric | Value |

|---|---|

| NextGenerationEU | €806.9bn |

| Digital Europe | €7.5bn (2021–27) |

| Chips Act | ~€43bn |

| EU procurement | ~€2tn/yr |

| Public cyber budgets | +~10% YoY (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect ProAct across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region-specific trends and forward-looking insights to help executives identify threats, opportunities and strategic responses.

Condenses the full PESTLE into a clean, visually segmented summary that’s editable for region- or business-specific notes, easily dropped into presentations and shared across teams for fast alignment during planning sessions.

Economic factors

IT spend cycles and GDP growth

Enterprise IT budgets closely track macro growth and inflation: IMF WEO projects global GDP growth of 3.1% in 2024 and 3.0% in 2025 while Gartner forecast global IT spending to rise ~4% in 2024 to about 5.3 trillion USD. Economic slowdowns typically defer capex but accelerate opex for managed services; Proact can pivot between project-based engagements and as-a-service offerings to stabilize revenue. A diversified vertical mix further hedges cyclicality by offsetting sector-specific downturns.

Energy price volatility

Data centers are energy intensive and exposed to price spikes, with IEA estimating they consumed about 200 TWh (~1% of global electricity) in 2022, pressuring margins during volatile markets. Long-term PPAs and efficiency upgrades (lowering PUE and energy per compute) protect unit economics. Proact can pass through or index energy costs in SLAs to stabilize cash flow. Clients prioritize predictable total cost of ownership when procuring services.

Currency fluctuations (EUR/GBP/SEK)

Multi-country operations expose ProAct to FX risk as EUR/GBP ≈0.86 and EUR/SEK ≈11.60 (July 2025), affecting service revenues and hardware imports; 2024–25 intra-year moves of 5–8% materially shift margins. Active hedging and local-currency pricing reduce volatility, while balancing sourcing and billing currencies limits mismatch. Transparent, contract-stated surcharges preserve margins and prevent client bill shock.

Hardware supply and pricing cycles

Server, storage and GPU supply constraints raised lead times to 8–16 weeks and pushed datacenter GPU prices down ~20–30% in 2024 as inventories normalized, forcing ProAct to manage project backlogs with phased rollouts and tight expectation controls; services revenue helped offset hardware margin compression.

- Standardize SKUs

- Multi-vendor sourcing

- Phased rollouts to reduce churn

- Services mix cushions margins

M&A and market consolidation

European MSP/DC markets continue consolidating for scale and reach; Proact can accelerate capability acquisition in security, AI and edge while protecting customer satisfaction through disciplined integration. Private-equity dry powder remained around $2.1 trillion in 2024, intensifying PE-backed rollups and pricing pressure across Europe.

- Consolidation: scale + reach

- Targets: security, AI, edge

- Integration: preserves CSAT & synergies

- Risk: PE rollups heighten pricing pressure

EU funds and Chips Act lift regional procurement; export controls force bigger inventories

Global GDP ~3.1% (2024) and 3.0% (2025, IMF) while global IT spend +~4% to $5.3T (2024, Gartner); Proact must balance capex vs opex. Data centers ~200 TWh (2022, IEA) → energy hedges/efficiency vital. EUR/GBP 0.86, EUR/SEK 11.60 (Jul 2025) — FX hedging needed. GPU prices fell 20–30% (2024); PE dry powder ~$2.1T fuels consolidation.

| Metric | Value |

|---|---|

| GDP growth | 3.1%/3.0% |

| IT spend 2024 | $5.3T (+4%) |

| Data center energy | ~200 TWh |

| FX (Jul 2025) | EUR/GBP 0.86; EUR/SEK 11.60 |

| GPU price change 2024 | -20–30% |

| PE dry powder 2024 | $2.1T |

What You See Is What You Get

ProAct PESTLE Analysis

The ProAct PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes complete, professionally structured political, economic, social, technological, legal and environmental assessments. No placeholders or teasers; this is the final file available for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain a competitive edge with our PESTLE Analysis of ProAct—concise, evidence-based insights into political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors, consultants and strategists, it saves research time and supports decision-making with actionable conclusions. Purchase the full report to access the complete, editable analysis and immediate strategic intelligence.

Political factors

EU digital policy shifts

Changing EU agendas on digital sovereignty and industrial policy steer cloud and local data strategies, driven by NextGenerationEU (€806.9bn) and Digital Europe funding (€7.5bn for 2021–27) that allocate grants and procurement preferences. Funding and incentives increasingly favor regional providers and projects aligned with the Chips Act (public/private mobilization ~€43bn). Proact can align offerings to national and EU priorities to capture public and regulated contracts. Policy reversals or delays, however, create planning uncertainty for multi-year bids.

Geopolitical tensions and sanctions

Since the Russia‑Ukraine war began in Feb 2022 and with Middle East escalation after Oct 2023, widening US and EU export controls (notably restrictions on advanced chips and design tools) have strained supply chains and vendor availability. Sanctions already limit access to hardware, chips and vendor support, forcing ProAct to diversify suppliers and hold larger inventory buffers. Clients will increasingly demand documented geopolitical‑risk assurances and supply‑continuity SLAs.

Public sector procurement dynamics

Government cloud-first and security-first mandates are driving stronger public sector demand for certified cloud services. The EU public procurement market is roughly €2 trillion annually, where certification and local hosting preferences can be barriers or competitive advantages. Proact can leverage regional data centers to meet tender criteria and data-residency rules. Long procurement cycles, often 6–12 months, reduce cash flow visibility for providers.

Brexit and cross-border operations

Brexit-driven UK-EU regulatory divergence—despite the EU adequacy decision for the UK (June 2021, still in force in 2025)—complicates data transfers, certifications and staffing for ProAct, while customs frictions increase hardware transit times and costs. ProAct requires mirrored services and dual compliance footprints across UK/EU and agile pricing to manage sterling/euro/regulatory volatility.

- Data: EU adequacy decision (June 2021) in force

- Operations: dual compliance + mirrored services required

- Risk: customs delays inflate hardware costs; price agility needed

Cybersecurity national strategies

National critical infrastructure policies are raising security baselines and driving ~10% year‑over‑year public cyberbudget growth in 2024, boosting demand for managed security and resilient backup; average breach cost remains high at $4.45M (IBM, 2023), making compliance a buying priority. Proact can package compliance‑led services for regulated sectors as 78% of buyers cite compliance as a top supplier filter.

- Policy: raised baselines, tighter controls

- Funding: ~10% YoY public cyberbudget growth (2024)

- Cost risk: average breach $4.45M (2023)

- Buyer shift: 78% prioritize compliance‑certified vendors

EU funds and Chips Act lift regional procurement; export controls force bigger inventories

EU digital sovereignty funds (NextGenerationEU €806.9bn; Digital Europe €7.5bn 2021–27) and Chips Act (~€43bn) steer procurement to regional suppliers, creating tender opportunities but planning uncertainty. Export controls since 2022 and post‑Oct 2023 Middle East escalation force supply diversification and bigger inventories. Public sector demand rises (EU procurement ~€2tn/yr; public cyber budgets + ~10% YoY in 2024).

| Metric | Value |

|---|---|

| NextGenerationEU | €806.9bn |

| Digital Europe | €7.5bn (2021–27) |

| Chips Act | ~€43bn |

| EU procurement | ~€2tn/yr |

| Public cyber budgets | +~10% YoY (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect ProAct across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed, region-specific trends and forward-looking insights to help executives identify threats, opportunities and strategic responses.

Condenses the full PESTLE into a clean, visually segmented summary that’s editable for region- or business-specific notes, easily dropped into presentations and shared across teams for fast alignment during planning sessions.

Economic factors

IT spend cycles and GDP growth

Enterprise IT budgets closely track macro growth and inflation: IMF WEO projects global GDP growth of 3.1% in 2024 and 3.0% in 2025 while Gartner forecast global IT spending to rise ~4% in 2024 to about 5.3 trillion USD. Economic slowdowns typically defer capex but accelerate opex for managed services; Proact can pivot between project-based engagements and as-a-service offerings to stabilize revenue. A diversified vertical mix further hedges cyclicality by offsetting sector-specific downturns.

Energy price volatility

Data centers are energy intensive and exposed to price spikes, with IEA estimating they consumed about 200 TWh (~1% of global electricity) in 2022, pressuring margins during volatile markets. Long-term PPAs and efficiency upgrades (lowering PUE and energy per compute) protect unit economics. Proact can pass through or index energy costs in SLAs to stabilize cash flow. Clients prioritize predictable total cost of ownership when procuring services.

Currency fluctuations (EUR/GBP/SEK)

Multi-country operations expose ProAct to FX risk as EUR/GBP ≈0.86 and EUR/SEK ≈11.60 (July 2025), affecting service revenues and hardware imports; 2024–25 intra-year moves of 5–8% materially shift margins. Active hedging and local-currency pricing reduce volatility, while balancing sourcing and billing currencies limits mismatch. Transparent, contract-stated surcharges preserve margins and prevent client bill shock.

Hardware supply and pricing cycles

Server, storage and GPU supply constraints raised lead times to 8–16 weeks and pushed datacenter GPU prices down ~20–30% in 2024 as inventories normalized, forcing ProAct to manage project backlogs with phased rollouts and tight expectation controls; services revenue helped offset hardware margin compression.

- Standardize SKUs

- Multi-vendor sourcing

- Phased rollouts to reduce churn

- Services mix cushions margins

M&A and market consolidation

European MSP/DC markets continue consolidating for scale and reach; Proact can accelerate capability acquisition in security, AI and edge while protecting customer satisfaction through disciplined integration. Private-equity dry powder remained around $2.1 trillion in 2024, intensifying PE-backed rollups and pricing pressure across Europe.

- Consolidation: scale + reach

- Targets: security, AI, edge

- Integration: preserves CSAT & synergies

- Risk: PE rollups heighten pricing pressure

EU funds and Chips Act lift regional procurement; export controls force bigger inventories

Global GDP ~3.1% (2024) and 3.0% (2025, IMF) while global IT spend +~4% to $5.3T (2024, Gartner); Proact must balance capex vs opex. Data centers ~200 TWh (2022, IEA) → energy hedges/efficiency vital. EUR/GBP 0.86, EUR/SEK 11.60 (Jul 2025) — FX hedging needed. GPU prices fell 20–30% (2024); PE dry powder ~$2.1T fuels consolidation.

| Metric | Value |

|---|---|

| GDP growth | 3.1%/3.0% |

| IT spend 2024 | $5.3T (+4%) |

| Data center energy | ~200 TWh |

| FX (Jul 2025) | EUR/GBP 0.86; EUR/SEK 11.60 |

| GPU price change 2024 | -20–30% |

| PE dry powder 2024 | $2.1T |

What You See Is What You Get

ProAct PESTLE Analysis

The ProAct PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes complete, professionally structured political, economic, social, technological, legal and environmental assessments. No placeholders or teasers; this is the final file available for immediate download.