ProAssurance Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

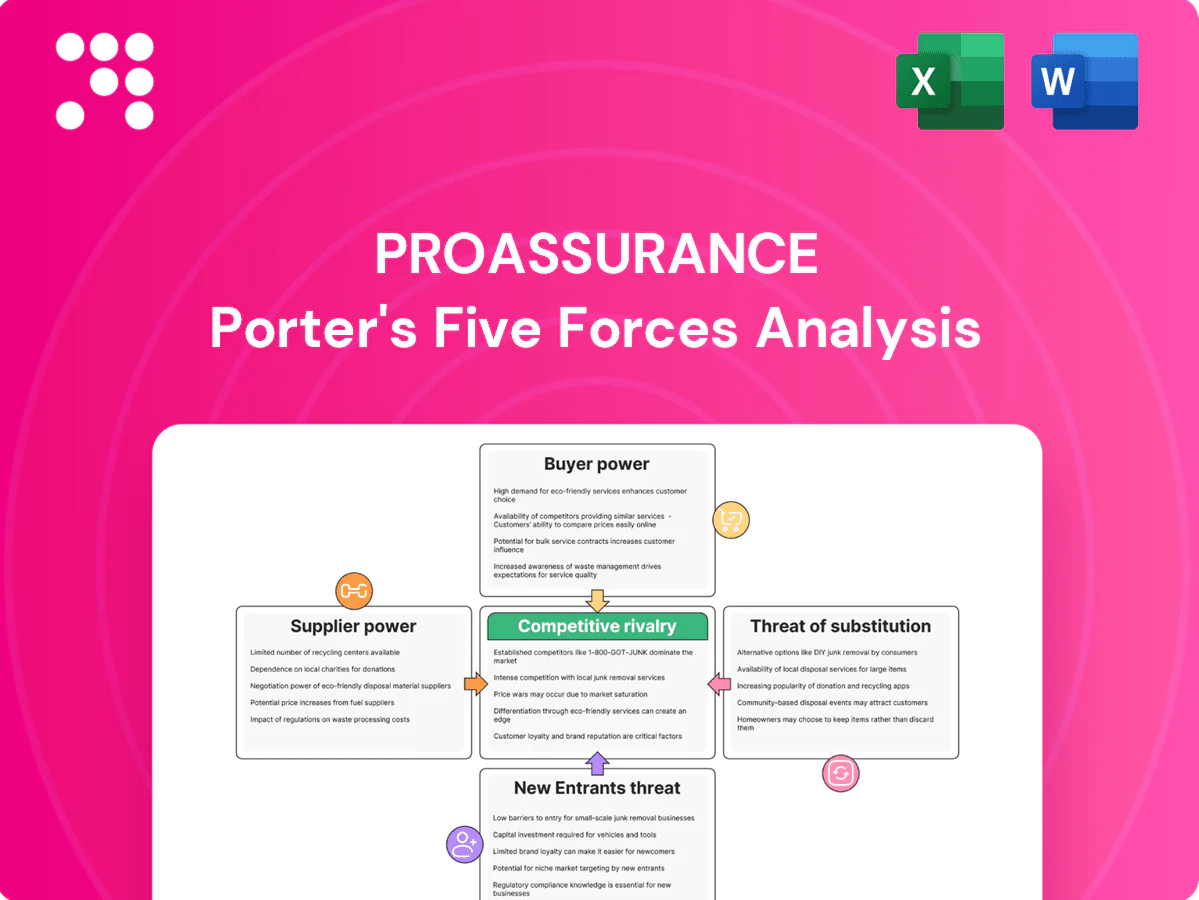

ProAssurance’s Porter’s Five Forces analysis highlights moderate buyer power, concentrated supplier dynamics, high regulatory barriers, low threat of substitutes, and medium competitive rivalry driven by specialty insurers. This snapshot reveals strategic pressures on margins and growth. Unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Reinsurers shape pricing and capacity

ProAssurance relies on reinsurance to manage peak exposures and long-tail medical professional liability, and 2024 renewals remained closely watched by carriers and cedants. Concentration among top reinsurers such as Swiss Re, Munich Re and Hannover Re can tighten capacity or terms, giving reinsurers leverage over ceding commissions, exclusions and attachment points. Diversifying panels and securing multi-year treaties partially offsets that power.

Specialized defense counsel and TPAs are limited

High-quality medical malpractice defense firms and expert TPAs remain limited in key jurisdictions in 2024, concentrating expertise and caseloads. Scarcity plus case complexity allow top firms to command premium fees and priority scheduling. Supplier switching risks loss of institutional knowledge and worse outcomes on open claims. Preferred panels and volume commitments are used to moderate costs and secure access.

Actuarial and underwriting talent is scarce

Long-tail healthcare liability demands niche actuarial and underwriting expertise; actuaries' median wage was 125,900 USD and insurance underwriters 78,050 USD per BLS May 2023. Tight labor markets and credential scarcity increase wage pressure and retention risk, giving talent suppliers leverage over pay and flexibility. In-house training and analytics investment can reduce dependence.

Core systems, data, and analytics vendors matter

Core systems (policy admin, claims platforms) and healthcare data vendors drive pricing and adjudication for ProAssurance; vendor lock-in and integration complexity raise switching frictions and downtime risk, enabling price uplifts and module upsells while exposing operational concentration.

- Vendor concentration: raises switching cost

- Integration complexity: increases downtime risk

- Upsell pressure: modular pricing leverage

- Mitigants: API-first and multi-vendor strategies

Capital and rating agencies influence terms

Reinsurance concentration and scarce specialty capacity boost supplier pricing power

Reinsurance concentration (Swiss Re, Munich Re, Hannover Re) and limited specialty defense/TPA capacity give suppliers notable leverage in pricing, terms and scheduling in 2024. Talent scarcity and system/vendor lock‑in raise switching costs and wage pressure; fed funds 5.25–5.50% (mid‑2024) elevates capital costs, amplifying supplier bargaining on reinsurance and tech contracts.

| Metric | 2024/data |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2024) |

| Top reinsurers | Swiss Re, Munich Re, Hannover Re (concentrated) |

| Actuary wage | USD 125,900 (BLS May 2023) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market-entry risks specific to ProAssurance, assessing supplier and buyer power, substitute threats, competitive rivalry, and barriers that protect incumbency; identifies disruptive forces and emerging threats to pricing, profitability, and market share.

A clear one-sheet Porter's Five Forces summary for ProAssurance that instantly highlights strategic pressures and eases boardroom decisions. Customize force levels, swap in your own data, and export a clean radar chart perfect for pitch decks or executive reports.

Customers Bargaining Power

Large health systems and groups negotiate hard

Hospitals, IDNs and large physician groups concentrate premium and wield volume leverage, with roughly 60% of US physicians now employed by health systems or corporate entities, increasing buyer clout. They demand tailored coverage, risk-sharing structures and rate concessions tied to performance metrics. Loss-sensitive programs and multi-year deals shift pricing power toward buyers. ProAssurance must balance margins with retention on marquee accounts.

Brokers control access and terms

Wholesale and retail brokers aggregate physician demand and coordinate competitive remarketing, raising commission pressure and driving standardized policy terms; in 2024 broker leverage intensified amid a soft malpractice market, compressing ProAssurance margins, making strong broker relationships and differentiated analytics-driven service critical to win advocacy.

Price sensitivity in cyclical markets

Professional liability's cyclical swings drive strong price sensitivity: soft markets see buyers switch for modest savings, often just a few percent, intensifying discounting, while hard markets allow carriers to push rate increases—market volatility can exceed 10% year-over-year—yet buyers still demand demonstrable value. Clear outcomes data and risk-management services justify premiums and reduce churn by quantifying avoided claims and loss ratios.

Switching costs via tail and prior-acts

Tail coverage, prior-acts endorsements and consent-to-settle create frictions that raise perceived switching costs for ProAssurance clients by preserving continuity of indemnity and defense; ProAssurance reported 2024 net written premiums near 1.02 billion, underscoring scale in med-mal continuity offerings. Competitors commonly offer retroactive dates to bridge gaps, muting lock-in while buyers weigh long-term claims handling versus short-term price; strong claims performance and lower loss ratios in 2024 increased perceived stickiness.

- Tail coverage preserves post-termination protection

- Prior-acts endorsements limit exposure gaps

- Consent-to-settle enhances control over resolution

- Competitor retro dates reduce absolute lock-in

- 2024 scale and claims performance bolster perceived switching costs

Segment heterogeneity tempers power

Segment heterogeneity tempers customer power: smaller practices and medtech startups generally wield far less leverage than large health systems, and ProAssurance’s 2023 statutory surplus around $1.3 billion supports selective underwriting rather than price concessions.

Niche exposures and specialized underwriting reduce direct comparability between buyers, while custom risk engineering shifts negotiations from pure price to loss-control services; portfolio mix management lets ProAssurance balance buyer power across lines.

- smaller practices vs enterprises: lower leverage

- specialized underwriting: reduces comparability

- risk engineering: shifts talks from price

- portfolio mix: balances overall buyer power

Concentrated physician buyers pressure rates; surplus enables selective underwriting

Concentrated buyers (~60% physicians employed by systems) exert strong leverage; ProAssurance NWP ~1.02B in 2024 limits margin flexibility. Brokers intensified pressure in the 2024 soft market, compressing rates amid >10% cyclical volatility. Tail/prior-acts raise switching costs; 2023 statutory surplus ~1.3B enables selective underwriting to defend margins.

| Metric | Value |

|---|---|

| Physicians employed by systems (2024) | ~60% |

| ProAssurance NWP (2024) | $1.02B |

| Statutory surplus (2023) | $1.3B |

| Market volatility | >10% YoY |

What You See Is What You Get

ProAssurance Porter's Five Forces Analysis

This preview shows the exact ProAssurance Porter’s Five Forces Analysis you'll receive upon purchase—no placeholders or mockups. The full, professionally formatted document is ready for immediate download and use, containing the same detailed competitive assessment, industry forces, and strategic implications you see here.

Go Beyond the Preview—Access the Full Strategic Report

ProAssurance’s Porter’s Five Forces analysis highlights moderate buyer power, concentrated supplier dynamics, high regulatory barriers, low threat of substitutes, and medium competitive rivalry driven by specialty insurers. This snapshot reveals strategic pressures on margins and growth. Unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Reinsurers shape pricing and capacity

ProAssurance relies on reinsurance to manage peak exposures and long-tail medical professional liability, and 2024 renewals remained closely watched by carriers and cedants. Concentration among top reinsurers such as Swiss Re, Munich Re and Hannover Re can tighten capacity or terms, giving reinsurers leverage over ceding commissions, exclusions and attachment points. Diversifying panels and securing multi-year treaties partially offsets that power.

Specialized defense counsel and TPAs are limited

High-quality medical malpractice defense firms and expert TPAs remain limited in key jurisdictions in 2024, concentrating expertise and caseloads. Scarcity plus case complexity allow top firms to command premium fees and priority scheduling. Supplier switching risks loss of institutional knowledge and worse outcomes on open claims. Preferred panels and volume commitments are used to moderate costs and secure access.

Actuarial and underwriting talent is scarce

Long-tail healthcare liability demands niche actuarial and underwriting expertise; actuaries' median wage was 125,900 USD and insurance underwriters 78,050 USD per BLS May 2023. Tight labor markets and credential scarcity increase wage pressure and retention risk, giving talent suppliers leverage over pay and flexibility. In-house training and analytics investment can reduce dependence.

Core systems, data, and analytics vendors matter

Core systems (policy admin, claims platforms) and healthcare data vendors drive pricing and adjudication for ProAssurance; vendor lock-in and integration complexity raise switching frictions and downtime risk, enabling price uplifts and module upsells while exposing operational concentration.

- Vendor concentration: raises switching cost

- Integration complexity: increases downtime risk

- Upsell pressure: modular pricing leverage

- Mitigants: API-first and multi-vendor strategies

Capital and rating agencies influence terms

Reinsurance concentration and scarce specialty capacity boost supplier pricing power

Reinsurance concentration (Swiss Re, Munich Re, Hannover Re) and limited specialty defense/TPA capacity give suppliers notable leverage in pricing, terms and scheduling in 2024. Talent scarcity and system/vendor lock‑in raise switching costs and wage pressure; fed funds 5.25–5.50% (mid‑2024) elevates capital costs, amplifying supplier bargaining on reinsurance and tech contracts.

| Metric | 2024/data |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2024) |

| Top reinsurers | Swiss Re, Munich Re, Hannover Re (concentrated) |

| Actuary wage | USD 125,900 (BLS May 2023) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market-entry risks specific to ProAssurance, assessing supplier and buyer power, substitute threats, competitive rivalry, and barriers that protect incumbency; identifies disruptive forces and emerging threats to pricing, profitability, and market share.

A clear one-sheet Porter's Five Forces summary for ProAssurance that instantly highlights strategic pressures and eases boardroom decisions. Customize force levels, swap in your own data, and export a clean radar chart perfect for pitch decks or executive reports.

Customers Bargaining Power

Large health systems and groups negotiate hard

Hospitals, IDNs and large physician groups concentrate premium and wield volume leverage, with roughly 60% of US physicians now employed by health systems or corporate entities, increasing buyer clout. They demand tailored coverage, risk-sharing structures and rate concessions tied to performance metrics. Loss-sensitive programs and multi-year deals shift pricing power toward buyers. ProAssurance must balance margins with retention on marquee accounts.

Brokers control access and terms

Wholesale and retail brokers aggregate physician demand and coordinate competitive remarketing, raising commission pressure and driving standardized policy terms; in 2024 broker leverage intensified amid a soft malpractice market, compressing ProAssurance margins, making strong broker relationships and differentiated analytics-driven service critical to win advocacy.

Price sensitivity in cyclical markets

Professional liability's cyclical swings drive strong price sensitivity: soft markets see buyers switch for modest savings, often just a few percent, intensifying discounting, while hard markets allow carriers to push rate increases—market volatility can exceed 10% year-over-year—yet buyers still demand demonstrable value. Clear outcomes data and risk-management services justify premiums and reduce churn by quantifying avoided claims and loss ratios.

Switching costs via tail and prior-acts

Tail coverage, prior-acts endorsements and consent-to-settle create frictions that raise perceived switching costs for ProAssurance clients by preserving continuity of indemnity and defense; ProAssurance reported 2024 net written premiums near 1.02 billion, underscoring scale in med-mal continuity offerings. Competitors commonly offer retroactive dates to bridge gaps, muting lock-in while buyers weigh long-term claims handling versus short-term price; strong claims performance and lower loss ratios in 2024 increased perceived stickiness.

- Tail coverage preserves post-termination protection

- Prior-acts endorsements limit exposure gaps

- Consent-to-settle enhances control over resolution

- Competitor retro dates reduce absolute lock-in

- 2024 scale and claims performance bolster perceived switching costs

Segment heterogeneity tempers power

Segment heterogeneity tempers customer power: smaller practices and medtech startups generally wield far less leverage than large health systems, and ProAssurance’s 2023 statutory surplus around $1.3 billion supports selective underwriting rather than price concessions.

Niche exposures and specialized underwriting reduce direct comparability between buyers, while custom risk engineering shifts negotiations from pure price to loss-control services; portfolio mix management lets ProAssurance balance buyer power across lines.

- smaller practices vs enterprises: lower leverage

- specialized underwriting: reduces comparability

- risk engineering: shifts talks from price

- portfolio mix: balances overall buyer power

Concentrated physician buyers pressure rates; surplus enables selective underwriting

Concentrated buyers (~60% physicians employed by systems) exert strong leverage; ProAssurance NWP ~1.02B in 2024 limits margin flexibility. Brokers intensified pressure in the 2024 soft market, compressing rates amid >10% cyclical volatility. Tail/prior-acts raise switching costs; 2023 statutory surplus ~1.3B enables selective underwriting to defend margins.

| Metric | Value |

|---|---|

| Physicians employed by systems (2024) | ~60% |

| ProAssurance NWP (2024) | $1.02B |

| Statutory surplus (2023) | $1.3B |

| Market volatility | >10% YoY |

What You See Is What You Get

ProAssurance Porter's Five Forces Analysis

This preview shows the exact ProAssurance Porter’s Five Forces Analysis you'll receive upon purchase—no placeholders or mockups. The full, professionally formatted document is ready for immediate download and use, containing the same detailed competitive assessment, industry forces, and strategic implications you see here.

Description

Go Beyond the Preview—Access the Full Strategic Report

ProAssurance’s Porter’s Five Forces analysis highlights moderate buyer power, concentrated supplier dynamics, high regulatory barriers, low threat of substitutes, and medium competitive rivalry driven by specialty insurers. This snapshot reveals strategic pressures on margins and growth. Unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Reinsurers shape pricing and capacity

ProAssurance relies on reinsurance to manage peak exposures and long-tail medical professional liability, and 2024 renewals remained closely watched by carriers and cedants. Concentration among top reinsurers such as Swiss Re, Munich Re and Hannover Re can tighten capacity or terms, giving reinsurers leverage over ceding commissions, exclusions and attachment points. Diversifying panels and securing multi-year treaties partially offsets that power.

Specialized defense counsel and TPAs are limited

High-quality medical malpractice defense firms and expert TPAs remain limited in key jurisdictions in 2024, concentrating expertise and caseloads. Scarcity plus case complexity allow top firms to command premium fees and priority scheduling. Supplier switching risks loss of institutional knowledge and worse outcomes on open claims. Preferred panels and volume commitments are used to moderate costs and secure access.

Actuarial and underwriting talent is scarce

Long-tail healthcare liability demands niche actuarial and underwriting expertise; actuaries' median wage was 125,900 USD and insurance underwriters 78,050 USD per BLS May 2023. Tight labor markets and credential scarcity increase wage pressure and retention risk, giving talent suppliers leverage over pay and flexibility. In-house training and analytics investment can reduce dependence.

Core systems, data, and analytics vendors matter

Core systems (policy admin, claims platforms) and healthcare data vendors drive pricing and adjudication for ProAssurance; vendor lock-in and integration complexity raise switching frictions and downtime risk, enabling price uplifts and module upsells while exposing operational concentration.

- Vendor concentration: raises switching cost

- Integration complexity: increases downtime risk

- Upsell pressure: modular pricing leverage

- Mitigants: API-first and multi-vendor strategies

Capital and rating agencies influence terms

Reinsurance concentration and scarce specialty capacity boost supplier pricing power

Reinsurance concentration (Swiss Re, Munich Re, Hannover Re) and limited specialty defense/TPA capacity give suppliers notable leverage in pricing, terms and scheduling in 2024. Talent scarcity and system/vendor lock‑in raise switching costs and wage pressure; fed funds 5.25–5.50% (mid‑2024) elevates capital costs, amplifying supplier bargaining on reinsurance and tech contracts.

| Metric | 2024/data |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2024) |

| Top reinsurers | Swiss Re, Munich Re, Hannover Re (concentrated) |

| Actuary wage | USD 125,900 (BLS May 2023) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market-entry risks specific to ProAssurance, assessing supplier and buyer power, substitute threats, competitive rivalry, and barriers that protect incumbency; identifies disruptive forces and emerging threats to pricing, profitability, and market share.

A clear one-sheet Porter's Five Forces summary for ProAssurance that instantly highlights strategic pressures and eases boardroom decisions. Customize force levels, swap in your own data, and export a clean radar chart perfect for pitch decks or executive reports.

Customers Bargaining Power

Large health systems and groups negotiate hard

Hospitals, IDNs and large physician groups concentrate premium and wield volume leverage, with roughly 60% of US physicians now employed by health systems or corporate entities, increasing buyer clout. They demand tailored coverage, risk-sharing structures and rate concessions tied to performance metrics. Loss-sensitive programs and multi-year deals shift pricing power toward buyers. ProAssurance must balance margins with retention on marquee accounts.

Brokers control access and terms

Wholesale and retail brokers aggregate physician demand and coordinate competitive remarketing, raising commission pressure and driving standardized policy terms; in 2024 broker leverage intensified amid a soft malpractice market, compressing ProAssurance margins, making strong broker relationships and differentiated analytics-driven service critical to win advocacy.

Price sensitivity in cyclical markets

Professional liability's cyclical swings drive strong price sensitivity: soft markets see buyers switch for modest savings, often just a few percent, intensifying discounting, while hard markets allow carriers to push rate increases—market volatility can exceed 10% year-over-year—yet buyers still demand demonstrable value. Clear outcomes data and risk-management services justify premiums and reduce churn by quantifying avoided claims and loss ratios.

Switching costs via tail and prior-acts

Tail coverage, prior-acts endorsements and consent-to-settle create frictions that raise perceived switching costs for ProAssurance clients by preserving continuity of indemnity and defense; ProAssurance reported 2024 net written premiums near 1.02 billion, underscoring scale in med-mal continuity offerings. Competitors commonly offer retroactive dates to bridge gaps, muting lock-in while buyers weigh long-term claims handling versus short-term price; strong claims performance and lower loss ratios in 2024 increased perceived stickiness.

- Tail coverage preserves post-termination protection

- Prior-acts endorsements limit exposure gaps

- Consent-to-settle enhances control over resolution

- Competitor retro dates reduce absolute lock-in

- 2024 scale and claims performance bolster perceived switching costs

Segment heterogeneity tempers power

Segment heterogeneity tempers customer power: smaller practices and medtech startups generally wield far less leverage than large health systems, and ProAssurance’s 2023 statutory surplus around $1.3 billion supports selective underwriting rather than price concessions.

Niche exposures and specialized underwriting reduce direct comparability between buyers, while custom risk engineering shifts negotiations from pure price to loss-control services; portfolio mix management lets ProAssurance balance buyer power across lines.

- smaller practices vs enterprises: lower leverage

- specialized underwriting: reduces comparability

- risk engineering: shifts talks from price

- portfolio mix: balances overall buyer power

Concentrated physician buyers pressure rates; surplus enables selective underwriting

Concentrated buyers (~60% physicians employed by systems) exert strong leverage; ProAssurance NWP ~1.02B in 2024 limits margin flexibility. Brokers intensified pressure in the 2024 soft market, compressing rates amid >10% cyclical volatility. Tail/prior-acts raise switching costs; 2023 statutory surplus ~1.3B enables selective underwriting to defend margins.

| Metric | Value |

|---|---|

| Physicians employed by systems (2024) | ~60% |

| ProAssurance NWP (2024) | $1.02B |

| Statutory surplus (2023) | $1.3B |

| Market volatility | >10% YoY |

What You See Is What You Get

ProAssurance Porter's Five Forces Analysis

This preview shows the exact ProAssurance Porter’s Five Forces Analysis you'll receive upon purchase—no placeholders or mockups. The full, professionally formatted document is ready for immediate download and use, containing the same detailed competitive assessment, industry forces, and strategic implications you see here.