Procaps Group SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Procaps Group’s SWOT highlights robust R&D and regional market reach, offset by regulatory and supply-chain vulnerabilities and intense generic competition. Want the full strategic picture with financial context and executable recommendations? Purchase the complete SWOT for a professionally formatted Word report plus an editable Excel matrix to plan, pitch, or invest with confidence.

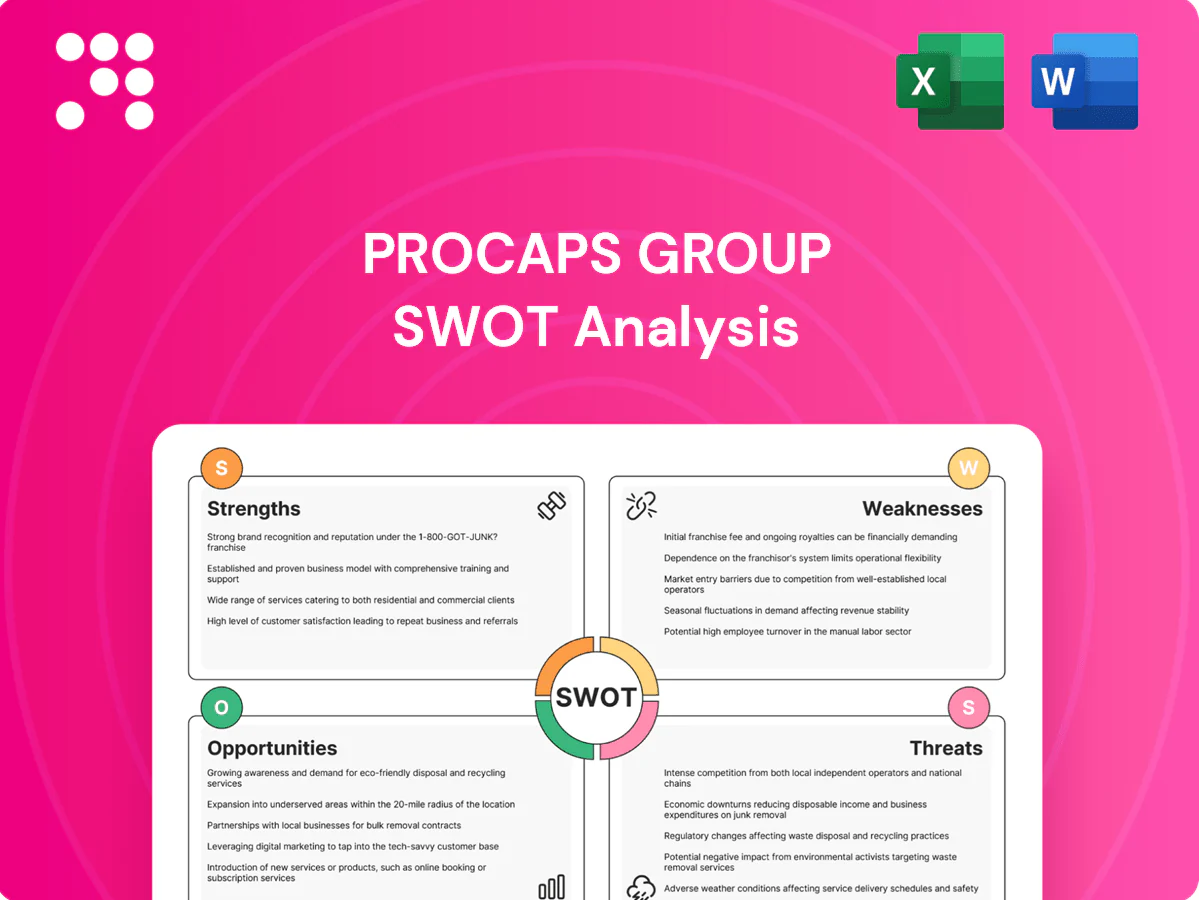

Strengths

Softgel technology leadership

Procaps' leadership in advanced softgel delivery yields superior bioavailability—softgels can boost absorption of lipophilic actives by as much as 30–50%—enabling clear product differentiation. Proprietary formulations and process know‑how create tangible switching costs for CDMO clients and support premium pricing and faster time‑to‑market. This competency expands addressable markets across Rx, OTC and nutraceutical categories and underpins commercial resilience.

Integrated CDMO and own brands

Procaps balances CDMO contracts with owned brands, diversifying revenue and reducing cycle risk; CDMO provides steady plant utilization and cash flow while branded products capture higher gross margins, supporting margin expansion. Cross‑learning between services and brands accelerates formulation speed and quality, improving pipeline visibility and customer stickiness. Procaps (Nasdaq: PCPS) reported roughly USD 300M revenue in 2024, underscoring scale.

Strong LATAM footprint

Procaps Group's established regulatory and distribution capabilities across Latin America leverage a regional pharmaceutical market valued at ≈USD 80bn in 2023 (IQVIA), providing scale and access. Deep local knowledge of pricing, tenders, and patient needs enhances market execution and reimbursement success. Regional proximity shortens lead times and lowers logistics costs, while the LATAM base supports faster launches of regionally relevant therapies.

Diversified portfolio breadth

Procaps spans prescription, OTC and nutraceuticals, reducing exposure to any single market and smoothing revenue volatility; multiple therapeutic areas temper demand cycles while nutraceuticals enable faster innovation and brand-led growth, supporting cross-selling and portfolio risk balancing.

- Segment diversity: prescription, OTC, nutraceuticals

- Therapeutic breadth: demand smoothing

- Fast innovation: nutraceuticals

- Commercial leverage: cross‑selling, risk balance

Quality and compliance track record

Procaps Group's consistent GMP certifications and audit-ready facilities reduce onboarding friction for global clients by demonstrating regulatory compliance and quality governance. Reliable manufacturing lowers recall and warranty risk, strengthening trust with partners and distributors. This quality reputation supports market access in the U.S. and other highly regulated jurisdictions.

- GMP certifications and audit readiness

- Lower client onboarding friction

- Reduced recall and warranty risk

- Facilitates entry into U.S. and regulated markets

Softgel bioavailability 30–50% backs USD 300M 2024 LATAM

Procaps' softgel leadership boosts bioavailability by 30–50%, enabling product differentiation and premium pricing. Proprietary formulations and CDMO scale supported USD 300M revenue in 2024, diversifying cash flow across Rx/OTC/nutraceuticals. Regional LATAM reach taps an ≈USD 80bn market (2023), with GMP-certified facilities easing access to regulated markets.

| Metric | Value |

|---|---|

| 2024 Revenue | USD 300M |

| Softgel bioavailability | +30–50% |

| LATAM pharma market (2023) | ≈USD 80bn |

What is included in the product

Delivers a strategic overview of Procaps Group’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to its pharmaceutical manufacturing, product diversification and geographic expansion; highlights competitive position, regulatory and supply‑chain risks, and growth drivers for informed strategic decisions.

Delivers a concise SWOT matrix for Procaps Group to align strategy quickly and resolve prioritization bottlenecks. Editable format enables rapid updates so teams can address shifting regulatory, supply-chain, and product challenges without delay.

Weaknesses

Geographic concentration in LATAM

Heavy LATAM exposure leaves Procaps highly vulnerable to currency swings and regional macro shocks, amplifying earnings volatility. Shifts in reimbursement and tender dynamics in key markets often compress margins and pressure pricing. Political and regulatory unpredictability can delay approvals and market access, and the geographic concentration reduces natural hedging across currencies and policy regimes.

Platform concentration in softgels

Heavy reliance on softgel technology narrows Procaps Group’s addressable formulation space compared with competitors offering injectables and complex solid-dosage forms.

Client demand is shifting toward advanced delivery systems like injectables and biologics, risking share loss if Procaps does not diversify.

Over-dependence intensifies competitive scrutiny on cost and quality and exposes production to utilization declines if softgel demand falls.

Scale disadvantage vs global CDMOs

Procaps faces a scale disadvantage vs global CDMOs, which collectively form a >$150 billion market (2023) and operate broader capabilities and footprints; this pressures pricing and dilutes Procaps’ negotiating leverage with multinational clients. Limited scale constrains investment pace in cutting‑edge modalities such as biologics and complex delivery systems, and can extend sales cycles for large, cross‑border contracts.

Capex and working capital intensity

Capex-heavy CDMO operations force continual spend on lines, validation and compliance; inventory and receivables—especially tied to tender cycles—can trap cash, while utilization swings compress margins and extend payback, tightening financial flexibility in downturns.

- Capex intensity: ongoing plant/validation spend

- Working capital: high inventory and receivables

- Utilization risk: margin/payback variability

- Liquidity: tighter in sector downturns

Limited U.S. brand recognition

Despite expanding U.S. operations, Procaps remains modestly known among American buyers and consumers, raising customer acquisition costs and lengthening time‑to‑revenue; navigating FDA pathways and PBM dynamics adds regulatory and commercial complexity, and building trust will need sustained marketing and clinical evidence.

- PBM concentration ~80% controlled by 3 firms

- Higher CAC and longer payback cycles

- Regulatory timelines and evidence demands

LATAM concentration, softgel dependence and capex strain compress margins and earnings visibility

Heavy LATAM concentration increases FX and political risk, compressing margins and earnings visibility. Dependence on softgels narrows addressable market as demand shifts to injectables/biologics. Scale and U.S. brand awareness lag global CDMOs, raising CAC and limiting large-client wins. Capex and working capital intensity strain liquidity during utilization dips.

| Metric | Value |

|---|---|

| Global CDMO market (2023) | >$150B |

| PBM concentration | ~80% via 3 firms |

| Key risks | FX, capex, utilization |

What You See Is What You Get

Procaps Group SWOT Analysis

This is the actual Procaps Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report; buying unlocks the complete, editable file. Get immediate access to the full, structured analysis after checkout.

Elevate Your Analysis with the Complete SWOT Report

Procaps Group’s SWOT highlights robust R&D and regional market reach, offset by regulatory and supply-chain vulnerabilities and intense generic competition. Want the full strategic picture with financial context and executable recommendations? Purchase the complete SWOT for a professionally formatted Word report plus an editable Excel matrix to plan, pitch, or invest with confidence.

Strengths

Softgel technology leadership

Procaps' leadership in advanced softgel delivery yields superior bioavailability—softgels can boost absorption of lipophilic actives by as much as 30–50%—enabling clear product differentiation. Proprietary formulations and process know‑how create tangible switching costs for CDMO clients and support premium pricing and faster time‑to‑market. This competency expands addressable markets across Rx, OTC and nutraceutical categories and underpins commercial resilience.

Integrated CDMO and own brands

Procaps balances CDMO contracts with owned brands, diversifying revenue and reducing cycle risk; CDMO provides steady plant utilization and cash flow while branded products capture higher gross margins, supporting margin expansion. Cross‑learning between services and brands accelerates formulation speed and quality, improving pipeline visibility and customer stickiness. Procaps (Nasdaq: PCPS) reported roughly USD 300M revenue in 2024, underscoring scale.

Strong LATAM footprint

Procaps Group's established regulatory and distribution capabilities across Latin America leverage a regional pharmaceutical market valued at ≈USD 80bn in 2023 (IQVIA), providing scale and access. Deep local knowledge of pricing, tenders, and patient needs enhances market execution and reimbursement success. Regional proximity shortens lead times and lowers logistics costs, while the LATAM base supports faster launches of regionally relevant therapies.

Diversified portfolio breadth

Procaps spans prescription, OTC and nutraceuticals, reducing exposure to any single market and smoothing revenue volatility; multiple therapeutic areas temper demand cycles while nutraceuticals enable faster innovation and brand-led growth, supporting cross-selling and portfolio risk balancing.

- Segment diversity: prescription, OTC, nutraceuticals

- Therapeutic breadth: demand smoothing

- Fast innovation: nutraceuticals

- Commercial leverage: cross‑selling, risk balance

Quality and compliance track record

Procaps Group's consistent GMP certifications and audit-ready facilities reduce onboarding friction for global clients by demonstrating regulatory compliance and quality governance. Reliable manufacturing lowers recall and warranty risk, strengthening trust with partners and distributors. This quality reputation supports market access in the U.S. and other highly regulated jurisdictions.

- GMP certifications and audit readiness

- Lower client onboarding friction

- Reduced recall and warranty risk

- Facilitates entry into U.S. and regulated markets

Softgel bioavailability 30–50% backs USD 300M 2024 LATAM

Procaps' softgel leadership boosts bioavailability by 30–50%, enabling product differentiation and premium pricing. Proprietary formulations and CDMO scale supported USD 300M revenue in 2024, diversifying cash flow across Rx/OTC/nutraceuticals. Regional LATAM reach taps an ≈USD 80bn market (2023), with GMP-certified facilities easing access to regulated markets.

| Metric | Value |

|---|---|

| 2024 Revenue | USD 300M |

| Softgel bioavailability | +30–50% |

| LATAM pharma market (2023) | ≈USD 80bn |

What is included in the product

Delivers a strategic overview of Procaps Group’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to its pharmaceutical manufacturing, product diversification and geographic expansion; highlights competitive position, regulatory and supply‑chain risks, and growth drivers for informed strategic decisions.

Delivers a concise SWOT matrix for Procaps Group to align strategy quickly and resolve prioritization bottlenecks. Editable format enables rapid updates so teams can address shifting regulatory, supply-chain, and product challenges without delay.

Weaknesses

Geographic concentration in LATAM

Heavy LATAM exposure leaves Procaps highly vulnerable to currency swings and regional macro shocks, amplifying earnings volatility. Shifts in reimbursement and tender dynamics in key markets often compress margins and pressure pricing. Political and regulatory unpredictability can delay approvals and market access, and the geographic concentration reduces natural hedging across currencies and policy regimes.

Platform concentration in softgels

Heavy reliance on softgel technology narrows Procaps Group’s addressable formulation space compared with competitors offering injectables and complex solid-dosage forms.

Client demand is shifting toward advanced delivery systems like injectables and biologics, risking share loss if Procaps does not diversify.

Over-dependence intensifies competitive scrutiny on cost and quality and exposes production to utilization declines if softgel demand falls.

Scale disadvantage vs global CDMOs

Procaps faces a scale disadvantage vs global CDMOs, which collectively form a >$150 billion market (2023) and operate broader capabilities and footprints; this pressures pricing and dilutes Procaps’ negotiating leverage with multinational clients. Limited scale constrains investment pace in cutting‑edge modalities such as biologics and complex delivery systems, and can extend sales cycles for large, cross‑border contracts.

Capex and working capital intensity

Capex-heavy CDMO operations force continual spend on lines, validation and compliance; inventory and receivables—especially tied to tender cycles—can trap cash, while utilization swings compress margins and extend payback, tightening financial flexibility in downturns.

- Capex intensity: ongoing plant/validation spend

- Working capital: high inventory and receivables

- Utilization risk: margin/payback variability

- Liquidity: tighter in sector downturns

Limited U.S. brand recognition

Despite expanding U.S. operations, Procaps remains modestly known among American buyers and consumers, raising customer acquisition costs and lengthening time‑to‑revenue; navigating FDA pathways and PBM dynamics adds regulatory and commercial complexity, and building trust will need sustained marketing and clinical evidence.

- PBM concentration ~80% controlled by 3 firms

- Higher CAC and longer payback cycles

- Regulatory timelines and evidence demands

LATAM concentration, softgel dependence and capex strain compress margins and earnings visibility

Heavy LATAM concentration increases FX and political risk, compressing margins and earnings visibility. Dependence on softgels narrows addressable market as demand shifts to injectables/biologics. Scale and U.S. brand awareness lag global CDMOs, raising CAC and limiting large-client wins. Capex and working capital intensity strain liquidity during utilization dips.

| Metric | Value |

|---|---|

| Global CDMO market (2023) | >$150B |

| PBM concentration | ~80% via 3 firms |

| Key risks | FX, capex, utilization |

What You See Is What You Get

Procaps Group SWOT Analysis

This is the actual Procaps Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report; buying unlocks the complete, editable file. Get immediate access to the full, structured analysis after checkout.

Description

Elevate Your Analysis with the Complete SWOT Report

Procaps Group’s SWOT highlights robust R&D and regional market reach, offset by regulatory and supply-chain vulnerabilities and intense generic competition. Want the full strategic picture with financial context and executable recommendations? Purchase the complete SWOT for a professionally formatted Word report plus an editable Excel matrix to plan, pitch, or invest with confidence.

Strengths

Softgel technology leadership

Procaps' leadership in advanced softgel delivery yields superior bioavailability—softgels can boost absorption of lipophilic actives by as much as 30–50%—enabling clear product differentiation. Proprietary formulations and process know‑how create tangible switching costs for CDMO clients and support premium pricing and faster time‑to‑market. This competency expands addressable markets across Rx, OTC and nutraceutical categories and underpins commercial resilience.

Integrated CDMO and own brands

Procaps balances CDMO contracts with owned brands, diversifying revenue and reducing cycle risk; CDMO provides steady plant utilization and cash flow while branded products capture higher gross margins, supporting margin expansion. Cross‑learning between services and brands accelerates formulation speed and quality, improving pipeline visibility and customer stickiness. Procaps (Nasdaq: PCPS) reported roughly USD 300M revenue in 2024, underscoring scale.

Strong LATAM footprint

Procaps Group's established regulatory and distribution capabilities across Latin America leverage a regional pharmaceutical market valued at ≈USD 80bn in 2023 (IQVIA), providing scale and access. Deep local knowledge of pricing, tenders, and patient needs enhances market execution and reimbursement success. Regional proximity shortens lead times and lowers logistics costs, while the LATAM base supports faster launches of regionally relevant therapies.

Diversified portfolio breadth

Procaps spans prescription, OTC and nutraceuticals, reducing exposure to any single market and smoothing revenue volatility; multiple therapeutic areas temper demand cycles while nutraceuticals enable faster innovation and brand-led growth, supporting cross-selling and portfolio risk balancing.

- Segment diversity: prescription, OTC, nutraceuticals

- Therapeutic breadth: demand smoothing

- Fast innovation: nutraceuticals

- Commercial leverage: cross‑selling, risk balance

Quality and compliance track record

Procaps Group's consistent GMP certifications and audit-ready facilities reduce onboarding friction for global clients by demonstrating regulatory compliance and quality governance. Reliable manufacturing lowers recall and warranty risk, strengthening trust with partners and distributors. This quality reputation supports market access in the U.S. and other highly regulated jurisdictions.

- GMP certifications and audit readiness

- Lower client onboarding friction

- Reduced recall and warranty risk

- Facilitates entry into U.S. and regulated markets

Softgel bioavailability 30–50% backs USD 300M 2024 LATAM

Procaps' softgel leadership boosts bioavailability by 30–50%, enabling product differentiation and premium pricing. Proprietary formulations and CDMO scale supported USD 300M revenue in 2024, diversifying cash flow across Rx/OTC/nutraceuticals. Regional LATAM reach taps an ≈USD 80bn market (2023), with GMP-certified facilities easing access to regulated markets.

| Metric | Value |

|---|---|

| 2024 Revenue | USD 300M |

| Softgel bioavailability | +30–50% |

| LATAM pharma market (2023) | ≈USD 80bn |

What is included in the product

Delivers a strategic overview of Procaps Group’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to its pharmaceutical manufacturing, product diversification and geographic expansion; highlights competitive position, regulatory and supply‑chain risks, and growth drivers for informed strategic decisions.

Delivers a concise SWOT matrix for Procaps Group to align strategy quickly and resolve prioritization bottlenecks. Editable format enables rapid updates so teams can address shifting regulatory, supply-chain, and product challenges without delay.

Weaknesses

Geographic concentration in LATAM

Heavy LATAM exposure leaves Procaps highly vulnerable to currency swings and regional macro shocks, amplifying earnings volatility. Shifts in reimbursement and tender dynamics in key markets often compress margins and pressure pricing. Political and regulatory unpredictability can delay approvals and market access, and the geographic concentration reduces natural hedging across currencies and policy regimes.

Platform concentration in softgels

Heavy reliance on softgel technology narrows Procaps Group’s addressable formulation space compared with competitors offering injectables and complex solid-dosage forms.

Client demand is shifting toward advanced delivery systems like injectables and biologics, risking share loss if Procaps does not diversify.

Over-dependence intensifies competitive scrutiny on cost and quality and exposes production to utilization declines if softgel demand falls.

Scale disadvantage vs global CDMOs

Procaps faces a scale disadvantage vs global CDMOs, which collectively form a >$150 billion market (2023) and operate broader capabilities and footprints; this pressures pricing and dilutes Procaps’ negotiating leverage with multinational clients. Limited scale constrains investment pace in cutting‑edge modalities such as biologics and complex delivery systems, and can extend sales cycles for large, cross‑border contracts.

Capex and working capital intensity

Capex-heavy CDMO operations force continual spend on lines, validation and compliance; inventory and receivables—especially tied to tender cycles—can trap cash, while utilization swings compress margins and extend payback, tightening financial flexibility in downturns.

- Capex intensity: ongoing plant/validation spend

- Working capital: high inventory and receivables

- Utilization risk: margin/payback variability

- Liquidity: tighter in sector downturns

Limited U.S. brand recognition

Despite expanding U.S. operations, Procaps remains modestly known among American buyers and consumers, raising customer acquisition costs and lengthening time‑to‑revenue; navigating FDA pathways and PBM dynamics adds regulatory and commercial complexity, and building trust will need sustained marketing and clinical evidence.

- PBM concentration ~80% controlled by 3 firms

- Higher CAC and longer payback cycles

- Regulatory timelines and evidence demands

LATAM concentration, softgel dependence and capex strain compress margins and earnings visibility

Heavy LATAM concentration increases FX and political risk, compressing margins and earnings visibility. Dependence on softgels narrows addressable market as demand shifts to injectables/biologics. Scale and U.S. brand awareness lag global CDMOs, raising CAC and limiting large-client wins. Capex and working capital intensity strain liquidity during utilization dips.

| Metric | Value |

|---|---|

| Global CDMO market (2023) | >$150B |

| PBM concentration | ~80% via 3 firms |

| Key risks | FX, capex, utilization |

What You See Is What You Get

Procaps Group SWOT Analysis

This is the actual Procaps Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report; buying unlocks the complete, editable file. Get immediate access to the full, structured analysis after checkout.