Procore Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

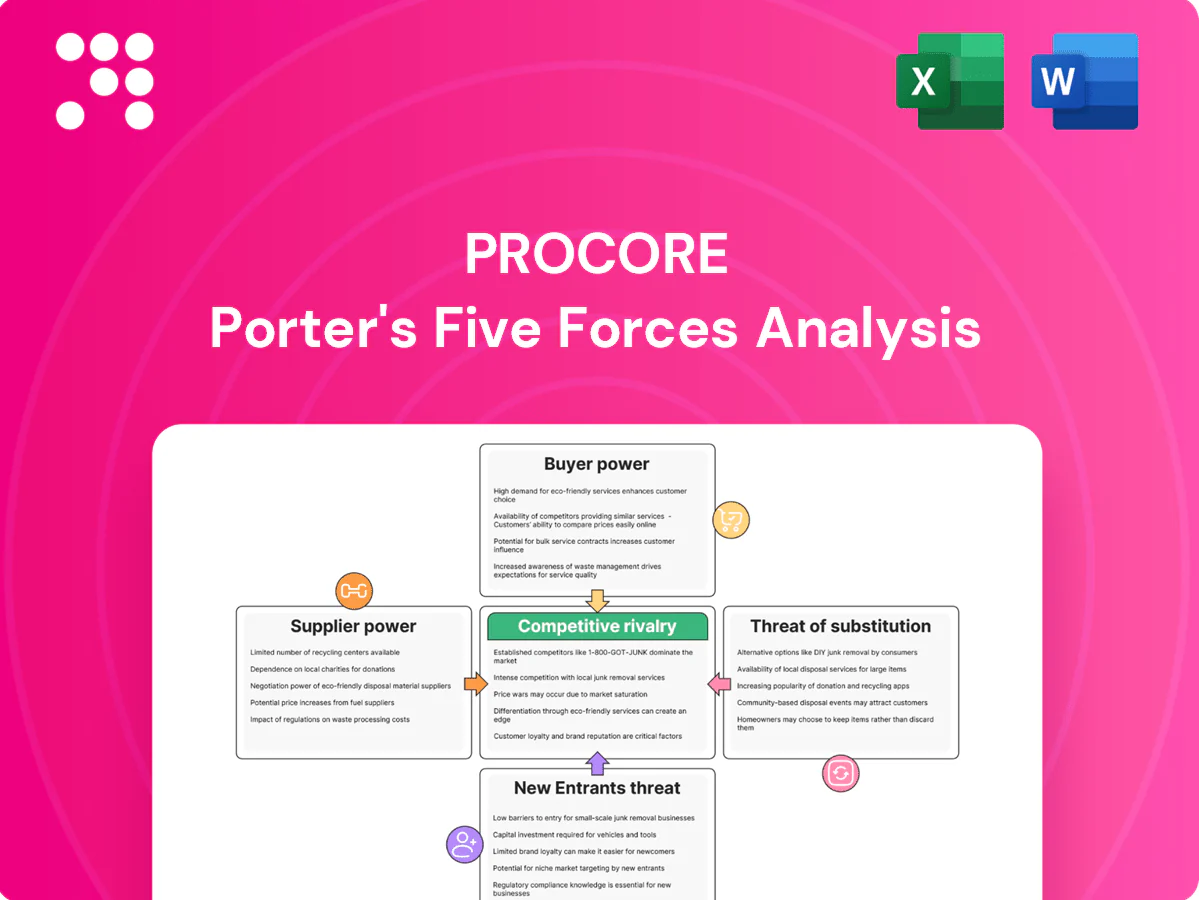

Procore faces moderate supplier power, rising buyer expectations, and significant rivalry as construction tech adoption accelerates; barriers to entry and substitutes shape its growth opportunities. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights to inform investment or competitive planning.

Suppliers Bargaining Power

Cloud infra dependence

Procore depends on hyperscalers for hosting, compute, storage and databases, exposing it to a concentrated supplier market where AWS, Azure and GCP held roughly 66% of cloud share in 2024, creating switching frictions and potential price escalation. Long-term contracts and reserved instances temper short-term volatility but do not eliminate cost pass-through risk to customers. Hyperscaler outages or regional limits, such as major AWS incidents in 2023, can breach SLAs and hurt customer satisfaction.

APIs and integration vendors

Value for Procore hinges on seamless ERPs, BIM, estimating and payroll integrations, with key partners such as Autodesk (BIM) and Sage (ERP) able to influence product roadmaps and certification access. API policy changes or deprecations increase adaptation and maintenance costs for customers and partners. However, open APIs and a broad ecosystem—Procore Marketplace lists 400+ integrations (Procore, 2024)—reduce single-partner supplier leverage.

Third-party data/identity tools

Dependencies on mapping, payments, e-signature and identity verification concentrate vendor risk for Procore, with 2024 industry surveys reporting 68% of platforms affected by third-party API pricing or compliance shifts. Pricing changes or regulatory updates can materially increase Procore’s operational spend and margins. Multi-sourcing and modular architecture reduce lock-in, but certification and audit requirements raise switching costs and integration timelines.

Talent and specialized engineering

Skilled cloud, mobile, and construction-tech engineers are scarce, raising supplier power; in 2024 median US cloud engineer pay approached $150,000 and tech wage inflation ran ~6–8%, while Big Tech poaching elevates costs and turnover.

- Remote work: global talent pools, global bidding

- Equity use: retention vs dilution pressure

- Wage inflation: increases hiring costs

Marketplace developers

Marketplace developers expand Procore's functionality and vertical depth; as of 2024 Procore's App Marketplace hosts over 300 third-party apps, boosting platform stickiness. Leading apps can demand favorable terms or co-marketing; if top apps exit or go exclusive elsewhere, ecosystem value and customer retention fall. Curation, revenue-sharing arrangements and SDK support are used to balance incentives and supplier dependency.

- 300+ third-party apps (2024)

- Top apps can secure preferential terms or co-marketing

- Exclusivity or exits erode ecosystem value

- Curation, revenue splits and SDKs mitigate supplier power

Construction software faces hyperscaler leverage, API pricing risk, and rising cloud engineer costs

Procore faces concentrated supplier power from hyperscalers (AWS/Azure/GCP ~66% cloud share in 2024) and key integrations (Autodesk, Sage) that can influence roadmap and costs. Third-party API pricing/compliance affected ~68% of platforms in 2024, raising margin risk; Procore Marketplace hosts 300+ apps (2024), which both diffuse and concentrate supplier leverage. Skilled cloud engineers cost pressure—median US pay ~$150,000 in 2024, wage inflation ~6–8%.

| Metric | 2024 |

|---|---|

| Hyperscaler share | ~66% |

| Platforms hit by API shifts | 68% |

| Marketplace apps | 300+ |

| Median cloud engineer pay (US) | $150,000 |

What is included in the product

Tailored Porter’s Five Forces analysis for Procore uncovering competitive intensity, supplier and buyer bargaining power, threats from substitutes and new entrants, and industry rivalry—highlighting disruptive risks and strategic levers that affect Procore’s pricing, margins, and growth prospects.

A one-sheet Procore Porter’s Five Forces summary that highlights buyer/supplier power, threat of substitutes, new entrants and rivalry—instantly pinpointing strategic pain points and action areas for faster, clearer decision-making.

Customers Bargaining Power

Consolidated enterprise buyers

Large owners and ENR Top 400 contractors buy at scale and extract volume discounts, often securing double-digit concessions. Their reference value and multi-year commitments raise leverage and lower churn risk. They demand integrations, SOC 2/type II security assurances and bespoke support. Procore surpassed $1B+ revenue in 2024, highlighting enterprise concentration and pricing pressure.

SMB contractors’ price sensitivity

SMB subcontractors often run on single-digit net margins (roughly 3–6%) and face strong cyclicality, making them highly price- and ROI-sensitive and prone to choosing lower-cost point solutions. Month-to-month licensing and modular packaging reduce lock-in and materially raise buyer power. Demonstrable time-to-value within days to weeks is essential to win conversions and curb churn.

Switching costs and data migration

Project continuity, workflows, and accumulated historical data in Procore create meaningful switching friction that reduces buyer power once a contractor is mid-project; Procore reported over 1.6 million users in 2024, underscoring embedded scale. Buyers still can switch at project boundaries or pilot rivals on new jobs, and rising interoperability expectations temper lock-in perceptions.

Procurement and compliance demands

Enterprise procurement enforces strict security, uptime and data residency rules, driving RFPs and competitive bake-offs that increase buyer leverage. In 2024 many customers require proof-of-value pilots before rollout, and added compliance layers raise cost-to-serve and lengthen procurement cycles. These demands compress pricing power and slow revenue recognition for vendors like Procore.

- RFPs strengthen bargaining

- PoV pilots often mandated

- Compliance raises cost-to-serve

- Data residency/uptime drive selection

Outcome accountability

Buyers judge Procore on schedule adherence, rework reduction, and budget control; failure in outcomes often triggers demands for concessions or expansion credits. Procore reported 2024 revenue of about $640.7 million, and customers leverage that scale when pushing for remedies. Robust analytics and executive dashboards cut perceived delivery risk while value-based case studies blunt price objections.

- Schedule adherence: KPI-led dashboards

- Rework: lower defect rates via analytics

- Budget control: ties to revenue-backed SLAs

- Concessions: expansion credits used when outcomes lag

Scale raises mid-project switching friction; enterprise buyers gain leverage, SMBs price-sensitive

Large owners and ENR Top 400 extract double-digit discounts and drive RFPs; Procore scale (1.6M users in 2024) raises switching friction mid-project but enterprise demands (SOC 2, data residency, PoV pilots) increase buyer leverage. SMBs (3–6% net margins) are highly price-sensitive; month-to-month licensing magnifies churn risk.

| Metric | 2024 |

|---|---|

| Users | 1.6M |

| Revenue (reported) | $640.7M |

| SMB net margins | 3–6% |

Same Document Delivered

Procore Porter's Five Forces Analysis

This preview shows the exact Procore Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted, professionally written and ready for download the moment you buy. You're viewing the final, complete file and will get instant access to this identical deliverable. Use it as-is for valuation, strategy, or reporting needs.

A Must-Have Tool for Decision-Makers

Procore faces moderate supplier power, rising buyer expectations, and significant rivalry as construction tech adoption accelerates; barriers to entry and substitutes shape its growth opportunities. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights to inform investment or competitive planning.

Suppliers Bargaining Power

Cloud infra dependence

Procore depends on hyperscalers for hosting, compute, storage and databases, exposing it to a concentrated supplier market where AWS, Azure and GCP held roughly 66% of cloud share in 2024, creating switching frictions and potential price escalation. Long-term contracts and reserved instances temper short-term volatility but do not eliminate cost pass-through risk to customers. Hyperscaler outages or regional limits, such as major AWS incidents in 2023, can breach SLAs and hurt customer satisfaction.

APIs and integration vendors

Value for Procore hinges on seamless ERPs, BIM, estimating and payroll integrations, with key partners such as Autodesk (BIM) and Sage (ERP) able to influence product roadmaps and certification access. API policy changes or deprecations increase adaptation and maintenance costs for customers and partners. However, open APIs and a broad ecosystem—Procore Marketplace lists 400+ integrations (Procore, 2024)—reduce single-partner supplier leverage.

Third-party data/identity tools

Dependencies on mapping, payments, e-signature and identity verification concentrate vendor risk for Procore, with 2024 industry surveys reporting 68% of platforms affected by third-party API pricing or compliance shifts. Pricing changes or regulatory updates can materially increase Procore’s operational spend and margins. Multi-sourcing and modular architecture reduce lock-in, but certification and audit requirements raise switching costs and integration timelines.

Talent and specialized engineering

Skilled cloud, mobile, and construction-tech engineers are scarce, raising supplier power; in 2024 median US cloud engineer pay approached $150,000 and tech wage inflation ran ~6–8%, while Big Tech poaching elevates costs and turnover.

- Remote work: global talent pools, global bidding

- Equity use: retention vs dilution pressure

- Wage inflation: increases hiring costs

Marketplace developers

Marketplace developers expand Procore's functionality and vertical depth; as of 2024 Procore's App Marketplace hosts over 300 third-party apps, boosting platform stickiness. Leading apps can demand favorable terms or co-marketing; if top apps exit or go exclusive elsewhere, ecosystem value and customer retention fall. Curation, revenue-sharing arrangements and SDK support are used to balance incentives and supplier dependency.

- 300+ third-party apps (2024)

- Top apps can secure preferential terms or co-marketing

- Exclusivity or exits erode ecosystem value

- Curation, revenue splits and SDKs mitigate supplier power

Construction software faces hyperscaler leverage, API pricing risk, and rising cloud engineer costs

Procore faces concentrated supplier power from hyperscalers (AWS/Azure/GCP ~66% cloud share in 2024) and key integrations (Autodesk, Sage) that can influence roadmap and costs. Third-party API pricing/compliance affected ~68% of platforms in 2024, raising margin risk; Procore Marketplace hosts 300+ apps (2024), which both diffuse and concentrate supplier leverage. Skilled cloud engineers cost pressure—median US pay ~$150,000 in 2024, wage inflation ~6–8%.

| Metric | 2024 |

|---|---|

| Hyperscaler share | ~66% |

| Platforms hit by API shifts | 68% |

| Marketplace apps | 300+ |

| Median cloud engineer pay (US) | $150,000 |

What is included in the product

Tailored Porter’s Five Forces analysis for Procore uncovering competitive intensity, supplier and buyer bargaining power, threats from substitutes and new entrants, and industry rivalry—highlighting disruptive risks and strategic levers that affect Procore’s pricing, margins, and growth prospects.

A one-sheet Procore Porter’s Five Forces summary that highlights buyer/supplier power, threat of substitutes, new entrants and rivalry—instantly pinpointing strategic pain points and action areas for faster, clearer decision-making.

Customers Bargaining Power

Consolidated enterprise buyers

Large owners and ENR Top 400 contractors buy at scale and extract volume discounts, often securing double-digit concessions. Their reference value and multi-year commitments raise leverage and lower churn risk. They demand integrations, SOC 2/type II security assurances and bespoke support. Procore surpassed $1B+ revenue in 2024, highlighting enterprise concentration and pricing pressure.

SMB contractors’ price sensitivity

SMB subcontractors often run on single-digit net margins (roughly 3–6%) and face strong cyclicality, making them highly price- and ROI-sensitive and prone to choosing lower-cost point solutions. Month-to-month licensing and modular packaging reduce lock-in and materially raise buyer power. Demonstrable time-to-value within days to weeks is essential to win conversions and curb churn.

Switching costs and data migration

Project continuity, workflows, and accumulated historical data in Procore create meaningful switching friction that reduces buyer power once a contractor is mid-project; Procore reported over 1.6 million users in 2024, underscoring embedded scale. Buyers still can switch at project boundaries or pilot rivals on new jobs, and rising interoperability expectations temper lock-in perceptions.

Procurement and compliance demands

Enterprise procurement enforces strict security, uptime and data residency rules, driving RFPs and competitive bake-offs that increase buyer leverage. In 2024 many customers require proof-of-value pilots before rollout, and added compliance layers raise cost-to-serve and lengthen procurement cycles. These demands compress pricing power and slow revenue recognition for vendors like Procore.

- RFPs strengthen bargaining

- PoV pilots often mandated

- Compliance raises cost-to-serve

- Data residency/uptime drive selection

Outcome accountability

Buyers judge Procore on schedule adherence, rework reduction, and budget control; failure in outcomes often triggers demands for concessions or expansion credits. Procore reported 2024 revenue of about $640.7 million, and customers leverage that scale when pushing for remedies. Robust analytics and executive dashboards cut perceived delivery risk while value-based case studies blunt price objections.

- Schedule adherence: KPI-led dashboards

- Rework: lower defect rates via analytics

- Budget control: ties to revenue-backed SLAs

- Concessions: expansion credits used when outcomes lag

Scale raises mid-project switching friction; enterprise buyers gain leverage, SMBs price-sensitive

Large owners and ENR Top 400 extract double-digit discounts and drive RFPs; Procore scale (1.6M users in 2024) raises switching friction mid-project but enterprise demands (SOC 2, data residency, PoV pilots) increase buyer leverage. SMBs (3–6% net margins) are highly price-sensitive; month-to-month licensing magnifies churn risk.

| Metric | 2024 |

|---|---|

| Users | 1.6M |

| Revenue (reported) | $640.7M |

| SMB net margins | 3–6% |

Same Document Delivered

Procore Porter's Five Forces Analysis

This preview shows the exact Procore Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted, professionally written and ready for download the moment you buy. You're viewing the final, complete file and will get instant access to this identical deliverable. Use it as-is for valuation, strategy, or reporting needs.

Description

A Must-Have Tool for Decision-Makers

Procore faces moderate supplier power, rising buyer expectations, and significant rivalry as construction tech adoption accelerates; barriers to entry and substitutes shape its growth opportunities. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights to inform investment or competitive planning.

Suppliers Bargaining Power

Cloud infra dependence

Procore depends on hyperscalers for hosting, compute, storage and databases, exposing it to a concentrated supplier market where AWS, Azure and GCP held roughly 66% of cloud share in 2024, creating switching frictions and potential price escalation. Long-term contracts and reserved instances temper short-term volatility but do not eliminate cost pass-through risk to customers. Hyperscaler outages or regional limits, such as major AWS incidents in 2023, can breach SLAs and hurt customer satisfaction.

APIs and integration vendors

Value for Procore hinges on seamless ERPs, BIM, estimating and payroll integrations, with key partners such as Autodesk (BIM) and Sage (ERP) able to influence product roadmaps and certification access. API policy changes or deprecations increase adaptation and maintenance costs for customers and partners. However, open APIs and a broad ecosystem—Procore Marketplace lists 400+ integrations (Procore, 2024)—reduce single-partner supplier leverage.

Third-party data/identity tools

Dependencies on mapping, payments, e-signature and identity verification concentrate vendor risk for Procore, with 2024 industry surveys reporting 68% of platforms affected by third-party API pricing or compliance shifts. Pricing changes or regulatory updates can materially increase Procore’s operational spend and margins. Multi-sourcing and modular architecture reduce lock-in, but certification and audit requirements raise switching costs and integration timelines.

Talent and specialized engineering

Skilled cloud, mobile, and construction-tech engineers are scarce, raising supplier power; in 2024 median US cloud engineer pay approached $150,000 and tech wage inflation ran ~6–8%, while Big Tech poaching elevates costs and turnover.

- Remote work: global talent pools, global bidding

- Equity use: retention vs dilution pressure

- Wage inflation: increases hiring costs

Marketplace developers

Marketplace developers expand Procore's functionality and vertical depth; as of 2024 Procore's App Marketplace hosts over 300 third-party apps, boosting platform stickiness. Leading apps can demand favorable terms or co-marketing; if top apps exit or go exclusive elsewhere, ecosystem value and customer retention fall. Curation, revenue-sharing arrangements and SDK support are used to balance incentives and supplier dependency.

- 300+ third-party apps (2024)

- Top apps can secure preferential terms or co-marketing

- Exclusivity or exits erode ecosystem value

- Curation, revenue splits and SDKs mitigate supplier power

Construction software faces hyperscaler leverage, API pricing risk, and rising cloud engineer costs

Procore faces concentrated supplier power from hyperscalers (AWS/Azure/GCP ~66% cloud share in 2024) and key integrations (Autodesk, Sage) that can influence roadmap and costs. Third-party API pricing/compliance affected ~68% of platforms in 2024, raising margin risk; Procore Marketplace hosts 300+ apps (2024), which both diffuse and concentrate supplier leverage. Skilled cloud engineers cost pressure—median US pay ~$150,000 in 2024, wage inflation ~6–8%.

| Metric | 2024 |

|---|---|

| Hyperscaler share | ~66% |

| Platforms hit by API shifts | 68% |

| Marketplace apps | 300+ |

| Median cloud engineer pay (US) | $150,000 |

What is included in the product

Tailored Porter’s Five Forces analysis for Procore uncovering competitive intensity, supplier and buyer bargaining power, threats from substitutes and new entrants, and industry rivalry—highlighting disruptive risks and strategic levers that affect Procore’s pricing, margins, and growth prospects.

A one-sheet Procore Porter’s Five Forces summary that highlights buyer/supplier power, threat of substitutes, new entrants and rivalry—instantly pinpointing strategic pain points and action areas for faster, clearer decision-making.

Customers Bargaining Power

Consolidated enterprise buyers

Large owners and ENR Top 400 contractors buy at scale and extract volume discounts, often securing double-digit concessions. Their reference value and multi-year commitments raise leverage and lower churn risk. They demand integrations, SOC 2/type II security assurances and bespoke support. Procore surpassed $1B+ revenue in 2024, highlighting enterprise concentration and pricing pressure.

SMB contractors’ price sensitivity

SMB subcontractors often run on single-digit net margins (roughly 3–6%) and face strong cyclicality, making them highly price- and ROI-sensitive and prone to choosing lower-cost point solutions. Month-to-month licensing and modular packaging reduce lock-in and materially raise buyer power. Demonstrable time-to-value within days to weeks is essential to win conversions and curb churn.

Switching costs and data migration

Project continuity, workflows, and accumulated historical data in Procore create meaningful switching friction that reduces buyer power once a contractor is mid-project; Procore reported over 1.6 million users in 2024, underscoring embedded scale. Buyers still can switch at project boundaries or pilot rivals on new jobs, and rising interoperability expectations temper lock-in perceptions.

Procurement and compliance demands

Enterprise procurement enforces strict security, uptime and data residency rules, driving RFPs and competitive bake-offs that increase buyer leverage. In 2024 many customers require proof-of-value pilots before rollout, and added compliance layers raise cost-to-serve and lengthen procurement cycles. These demands compress pricing power and slow revenue recognition for vendors like Procore.

- RFPs strengthen bargaining

- PoV pilots often mandated

- Compliance raises cost-to-serve

- Data residency/uptime drive selection

Outcome accountability

Buyers judge Procore on schedule adherence, rework reduction, and budget control; failure in outcomes often triggers demands for concessions or expansion credits. Procore reported 2024 revenue of about $640.7 million, and customers leverage that scale when pushing for remedies. Robust analytics and executive dashboards cut perceived delivery risk while value-based case studies blunt price objections.

- Schedule adherence: KPI-led dashboards

- Rework: lower defect rates via analytics

- Budget control: ties to revenue-backed SLAs

- Concessions: expansion credits used when outcomes lag

Scale raises mid-project switching friction; enterprise buyers gain leverage, SMBs price-sensitive

Large owners and ENR Top 400 extract double-digit discounts and drive RFPs; Procore scale (1.6M users in 2024) raises switching friction mid-project but enterprise demands (SOC 2, data residency, PoV pilots) increase buyer leverage. SMBs (3–6% net margins) are highly price-sensitive; month-to-month licensing magnifies churn risk.

| Metric | 2024 |

|---|---|

| Users | 1.6M |

| Revenue (reported) | $640.7M |

| SMB net margins | 3–6% |

Same Document Delivered

Procore Porter's Five Forces Analysis

This preview shows the exact Procore Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted, professionally written and ready for download the moment you buy. You're viewing the final, complete file and will get instant access to this identical deliverable. Use it as-is for valuation, strategy, or reporting needs.