Procore SWOT Analysis

Your Strategic Toolkit Starts Here

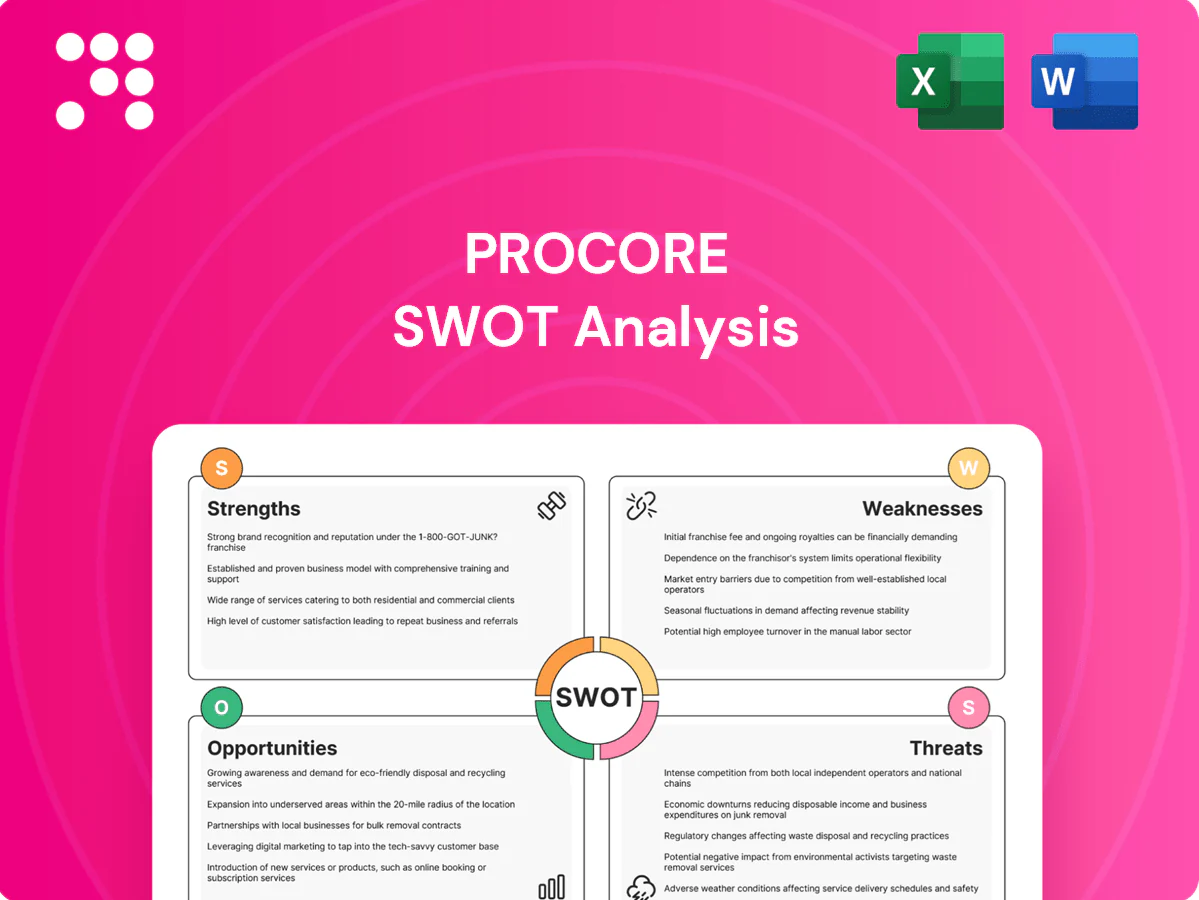

Procore’s SWOT highlights its strong market share, product integration strengths, and scalability, alongside competitive pressures and execution risks. Our full SWOT digs into financials, strategic levers, and market scenarios with expert commentary. Purchase the complete report for a ready-to-use Word and Excel package to inform investments and strategy.

Strengths

End-to-end construction platform

Procore’s end-to-end platform consolidates project management, financials, quality, safety and field productivity into a single source of truth, cutting stakeholder silos and rework. This breadth drives cross-module adoption and higher platform stickiness, simplifying vendor management for enterprise construction firms. As of 2024 Procore served over 17,000 customers and roughly 1.6 million users, underscoring enterprise-scale traction.

Strong network effects and collaboration hub

Owners, GCs and specialty contractors collaborate in Procore shared workflows and data; with over 1.5 million users and 2,000+ customers as of 2024, document exchanges, RFIs, submittals and change orders flow faster and more accurately. These multi-sided interactions raise switching costs, strengthening retention (net dollar retention >100% in 2024) and expanding ecosystem influence.

Cloud-native, mobile-first workflows

Procore delivers real-time jobsite data through intuitive mobile apps, enabling field-to-office visibility that accelerates decisions and boosts quality and safety. Customers report faster issue resolution and reduced rework across projects; the platform is used on roughly 1.3 million projects globally. Cloud delivery enables quicker deployments and continuous updates versus legacy on-prem tools. This architecture scales across complex, multi-location programs and supported Procore’s FY2024 revenue of about $747 million.

Robust integrations and open APIs

Robust integrations connect ERP, accounting, BIM, scheduling and point solutions to streamline data flow and reduce handoffs; open APIs let customers tailor workflows and cut duplicate entry, accelerating time-to-value and lowering change-management friction. Procore’s extensible ecosystem positions it as a system-of-engagement, supported by 300+ Marketplace integrations and ~1.3M users across 125 countries (2024 company figures).

- Connections: ERP, accounting, BIM, scheduling

- Open APIs: customizable workflows, fewer duplicate entries

- Scale: 300+ integrations; ~1.3M users (2024)

Brand recognition and construction focus

Procore is widely recognized as the construction category leader, serving over 16,000 customers and more than 1.3 million users globally; deep domain expertise drives features tailored to subcontractor and GC workflows, boosting credibility with enterprise GCs and owners and enabling faster iteration on sector-specific pain points.

- Category leader: >16,000 customers

- Scale: >1.3M users

- Enterprise trust: strong GC/owner adoption

- Rapid sector-focused product iteration

End-to-end construction platform: >17k customers, ~1.6M users, $747M revenue, NDR >100%

Procore’s end-to-end construction platform drives cross-module adoption and high stickiness, serving >17,000 customers and ~1.6M users (2024) with FY2024 revenue ~$747M. Multi-sided workflows raise switching costs and net dollar retention >100% (2024). Open APIs and 300+ integrations accelerate deployments and reduce handoffs.

| Metric | 2024 |

|---|---|

| Customers | >17,000 |

| Users | ~1.6M |

| Revenue | ~$747M |

| Integrations | 300+ |

| NDR | >100% |

What is included in the product

Provides a concise SWOT analysis highlighting Procore’s core strengths, operational weaknesses, market opportunities, and external threats to assess its competitive position and growth prospects.

Delivers a concise SWOT matrix tailored to Procore for fast strategic alignment across construction-tech teams. Editable format enables quick updates to address product and market pain points and produce stakeholder-ready presentations.

Weaknesses

High total cost for full suite

Comprehensive Procore deployments can cost tens to hundreds of thousands of dollars for full-suite implementations, pricing that can be prohibitive for smaller contractors with tight margins. Budget sensitivity in construction often slows adoption or limits module uptake, with sales cycles commonly stretching 6–12 months as firms evaluate ROI. Perceived high total cost and pricing complexity create openings for lower-priced competitors targeting SMBs.

Implementation and change management burden

Rolling out Procore multi-module workflows typically requires 6–12 months of training and process redesign, and resistance from field crews can push time-to-value out by 3+ months. Data migration and integration setup often consume an extra 20–30% of IT and operations effort. In complex organizations uneven adoption across projects frequently produces partial deployment and inconsistent ROI.

Dependence on construction cycle health

Dependence on construction cycle health means project starts and capital spending directly drive Procore seat counts and usage, so downturns or delayed projects pressure new bookings and expansion. Budget freezes commonly stall upsell and maintenance revenue, and heavy revenue concentration in cyclical end markets increases quarterly volatility and customer churn risk.

Feature overlap with point solutions

Feature overlap with specialty estimating, BIM, and scheduling tools can push experts toward best-of-breed vendors, creating integration complexity and buyer confusion that slows procurement and deployment. Customers often cherry-pick modules, lowering average contract value and pressuring margin expansion. Maintaining parity with niche leaders increases R&D spend and diverts product focus.

- Specialty tool preference

- Integration complexity

- Module cherry-picking

- Higher R&D burden

Data fragmentation across stakeholders

Data fragmentation across owners, GCs and subs leads to varying standards and inconsistent data quality, which weakens Procore’s analytics and forecasting accuracy across multi-party projects.

Universal adoption across subcontractors remains difficult, and governance plus permissions must balance open collaboration with regulatory and contractual compliance.

High upfront cost and 6-12 month deployments stall SMB adoption

High upfront and total cost (tens–hundreds k) limits SMB adoption and extends 6–12 month sales cycles. Deployments need 6–12 months plus 20–30% extra IT effort for data migration, with field resistance adding 3+ months to time-to-value. Cycle sensitivity and module cherry-picking reduce ACV and increase churn risk.

| Weakness | Metric |

|---|---|

| Cost barrier | tens–hundreds k |

| Deployment time | 6–12 months |

| Integration effort | +20–30% IT |

| Field delay | +3 months |

Same Document Delivered

Procore SWOT Analysis

This is the actual Procore SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and it reflects the same structured, editable content. Buy now to unlock the complete, detailed version.

Your Strategic Toolkit Starts Here

Procore’s SWOT highlights its strong market share, product integration strengths, and scalability, alongside competitive pressures and execution risks. Our full SWOT digs into financials, strategic levers, and market scenarios with expert commentary. Purchase the complete report for a ready-to-use Word and Excel package to inform investments and strategy.

Strengths

End-to-end construction platform

Procore’s end-to-end platform consolidates project management, financials, quality, safety and field productivity into a single source of truth, cutting stakeholder silos and rework. This breadth drives cross-module adoption and higher platform stickiness, simplifying vendor management for enterprise construction firms. As of 2024 Procore served over 17,000 customers and roughly 1.6 million users, underscoring enterprise-scale traction.

Strong network effects and collaboration hub

Owners, GCs and specialty contractors collaborate in Procore shared workflows and data; with over 1.5 million users and 2,000+ customers as of 2024, document exchanges, RFIs, submittals and change orders flow faster and more accurately. These multi-sided interactions raise switching costs, strengthening retention (net dollar retention >100% in 2024) and expanding ecosystem influence.

Cloud-native, mobile-first workflows

Procore delivers real-time jobsite data through intuitive mobile apps, enabling field-to-office visibility that accelerates decisions and boosts quality and safety. Customers report faster issue resolution and reduced rework across projects; the platform is used on roughly 1.3 million projects globally. Cloud delivery enables quicker deployments and continuous updates versus legacy on-prem tools. This architecture scales across complex, multi-location programs and supported Procore’s FY2024 revenue of about $747 million.

Robust integrations and open APIs

Robust integrations connect ERP, accounting, BIM, scheduling and point solutions to streamline data flow and reduce handoffs; open APIs let customers tailor workflows and cut duplicate entry, accelerating time-to-value and lowering change-management friction. Procore’s extensible ecosystem positions it as a system-of-engagement, supported by 300+ Marketplace integrations and ~1.3M users across 125 countries (2024 company figures).

- Connections: ERP, accounting, BIM, scheduling

- Open APIs: customizable workflows, fewer duplicate entries

- Scale: 300+ integrations; ~1.3M users (2024)

Brand recognition and construction focus

Procore is widely recognized as the construction category leader, serving over 16,000 customers and more than 1.3 million users globally; deep domain expertise drives features tailored to subcontractor and GC workflows, boosting credibility with enterprise GCs and owners and enabling faster iteration on sector-specific pain points.

- Category leader: >16,000 customers

- Scale: >1.3M users

- Enterprise trust: strong GC/owner adoption

- Rapid sector-focused product iteration

End-to-end construction platform: >17k customers, ~1.6M users, $747M revenue, NDR >100%

Procore’s end-to-end construction platform drives cross-module adoption and high stickiness, serving >17,000 customers and ~1.6M users (2024) with FY2024 revenue ~$747M. Multi-sided workflows raise switching costs and net dollar retention >100% (2024). Open APIs and 300+ integrations accelerate deployments and reduce handoffs.

| Metric | 2024 |

|---|---|

| Customers | >17,000 |

| Users | ~1.6M |

| Revenue | ~$747M |

| Integrations | 300+ |

| NDR | >100% |

What is included in the product

Provides a concise SWOT analysis highlighting Procore’s core strengths, operational weaknesses, market opportunities, and external threats to assess its competitive position and growth prospects.

Delivers a concise SWOT matrix tailored to Procore for fast strategic alignment across construction-tech teams. Editable format enables quick updates to address product and market pain points and produce stakeholder-ready presentations.

Weaknesses

High total cost for full suite

Comprehensive Procore deployments can cost tens to hundreds of thousands of dollars for full-suite implementations, pricing that can be prohibitive for smaller contractors with tight margins. Budget sensitivity in construction often slows adoption or limits module uptake, with sales cycles commonly stretching 6–12 months as firms evaluate ROI. Perceived high total cost and pricing complexity create openings for lower-priced competitors targeting SMBs.

Implementation and change management burden

Rolling out Procore multi-module workflows typically requires 6–12 months of training and process redesign, and resistance from field crews can push time-to-value out by 3+ months. Data migration and integration setup often consume an extra 20–30% of IT and operations effort. In complex organizations uneven adoption across projects frequently produces partial deployment and inconsistent ROI.

Dependence on construction cycle health

Dependence on construction cycle health means project starts and capital spending directly drive Procore seat counts and usage, so downturns or delayed projects pressure new bookings and expansion. Budget freezes commonly stall upsell and maintenance revenue, and heavy revenue concentration in cyclical end markets increases quarterly volatility and customer churn risk.

Feature overlap with point solutions

Feature overlap with specialty estimating, BIM, and scheduling tools can push experts toward best-of-breed vendors, creating integration complexity and buyer confusion that slows procurement and deployment. Customers often cherry-pick modules, lowering average contract value and pressuring margin expansion. Maintaining parity with niche leaders increases R&D spend and diverts product focus.

- Specialty tool preference

- Integration complexity

- Module cherry-picking

- Higher R&D burden

Data fragmentation across stakeholders

Data fragmentation across owners, GCs and subs leads to varying standards and inconsistent data quality, which weakens Procore’s analytics and forecasting accuracy across multi-party projects.

Universal adoption across subcontractors remains difficult, and governance plus permissions must balance open collaboration with regulatory and contractual compliance.

High upfront cost and 6-12 month deployments stall SMB adoption

High upfront and total cost (tens–hundreds k) limits SMB adoption and extends 6–12 month sales cycles. Deployments need 6–12 months plus 20–30% extra IT effort for data migration, with field resistance adding 3+ months to time-to-value. Cycle sensitivity and module cherry-picking reduce ACV and increase churn risk.

| Weakness | Metric |

|---|---|

| Cost barrier | tens–hundreds k |

| Deployment time | 6–12 months |

| Integration effort | +20–30% IT |

| Field delay | +3 months |

Same Document Delivered

Procore SWOT Analysis

This is the actual Procore SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and it reflects the same structured, editable content. Buy now to unlock the complete, detailed version.

Description

Your Strategic Toolkit Starts Here

Procore’s SWOT highlights its strong market share, product integration strengths, and scalability, alongside competitive pressures and execution risks. Our full SWOT digs into financials, strategic levers, and market scenarios with expert commentary. Purchase the complete report for a ready-to-use Word and Excel package to inform investments and strategy.

Strengths

End-to-end construction platform

Procore’s end-to-end platform consolidates project management, financials, quality, safety and field productivity into a single source of truth, cutting stakeholder silos and rework. This breadth drives cross-module adoption and higher platform stickiness, simplifying vendor management for enterprise construction firms. As of 2024 Procore served over 17,000 customers and roughly 1.6 million users, underscoring enterprise-scale traction.

Strong network effects and collaboration hub

Owners, GCs and specialty contractors collaborate in Procore shared workflows and data; with over 1.5 million users and 2,000+ customers as of 2024, document exchanges, RFIs, submittals and change orders flow faster and more accurately. These multi-sided interactions raise switching costs, strengthening retention (net dollar retention >100% in 2024) and expanding ecosystem influence.

Cloud-native, mobile-first workflows

Procore delivers real-time jobsite data through intuitive mobile apps, enabling field-to-office visibility that accelerates decisions and boosts quality and safety. Customers report faster issue resolution and reduced rework across projects; the platform is used on roughly 1.3 million projects globally. Cloud delivery enables quicker deployments and continuous updates versus legacy on-prem tools. This architecture scales across complex, multi-location programs and supported Procore’s FY2024 revenue of about $747 million.

Robust integrations and open APIs

Robust integrations connect ERP, accounting, BIM, scheduling and point solutions to streamline data flow and reduce handoffs; open APIs let customers tailor workflows and cut duplicate entry, accelerating time-to-value and lowering change-management friction. Procore’s extensible ecosystem positions it as a system-of-engagement, supported by 300+ Marketplace integrations and ~1.3M users across 125 countries (2024 company figures).

- Connections: ERP, accounting, BIM, scheduling

- Open APIs: customizable workflows, fewer duplicate entries

- Scale: 300+ integrations; ~1.3M users (2024)

Brand recognition and construction focus

Procore is widely recognized as the construction category leader, serving over 16,000 customers and more than 1.3 million users globally; deep domain expertise drives features tailored to subcontractor and GC workflows, boosting credibility with enterprise GCs and owners and enabling faster iteration on sector-specific pain points.

- Category leader: >16,000 customers

- Scale: >1.3M users

- Enterprise trust: strong GC/owner adoption

- Rapid sector-focused product iteration

End-to-end construction platform: >17k customers, ~1.6M users, $747M revenue, NDR >100%

Procore’s end-to-end construction platform drives cross-module adoption and high stickiness, serving >17,000 customers and ~1.6M users (2024) with FY2024 revenue ~$747M. Multi-sided workflows raise switching costs and net dollar retention >100% (2024). Open APIs and 300+ integrations accelerate deployments and reduce handoffs.

| Metric | 2024 |

|---|---|

| Customers | >17,000 |

| Users | ~1.6M |

| Revenue | ~$747M |

| Integrations | 300+ |

| NDR | >100% |

What is included in the product

Provides a concise SWOT analysis highlighting Procore’s core strengths, operational weaknesses, market opportunities, and external threats to assess its competitive position and growth prospects.

Delivers a concise SWOT matrix tailored to Procore for fast strategic alignment across construction-tech teams. Editable format enables quick updates to address product and market pain points and produce stakeholder-ready presentations.

Weaknesses

High total cost for full suite

Comprehensive Procore deployments can cost tens to hundreds of thousands of dollars for full-suite implementations, pricing that can be prohibitive for smaller contractors with tight margins. Budget sensitivity in construction often slows adoption or limits module uptake, with sales cycles commonly stretching 6–12 months as firms evaluate ROI. Perceived high total cost and pricing complexity create openings for lower-priced competitors targeting SMBs.

Implementation and change management burden

Rolling out Procore multi-module workflows typically requires 6–12 months of training and process redesign, and resistance from field crews can push time-to-value out by 3+ months. Data migration and integration setup often consume an extra 20–30% of IT and operations effort. In complex organizations uneven adoption across projects frequently produces partial deployment and inconsistent ROI.

Dependence on construction cycle health

Dependence on construction cycle health means project starts and capital spending directly drive Procore seat counts and usage, so downturns or delayed projects pressure new bookings and expansion. Budget freezes commonly stall upsell and maintenance revenue, and heavy revenue concentration in cyclical end markets increases quarterly volatility and customer churn risk.

Feature overlap with point solutions

Feature overlap with specialty estimating, BIM, and scheduling tools can push experts toward best-of-breed vendors, creating integration complexity and buyer confusion that slows procurement and deployment. Customers often cherry-pick modules, lowering average contract value and pressuring margin expansion. Maintaining parity with niche leaders increases R&D spend and diverts product focus.

- Specialty tool preference

- Integration complexity

- Module cherry-picking

- Higher R&D burden

Data fragmentation across stakeholders

Data fragmentation across owners, GCs and subs leads to varying standards and inconsistent data quality, which weakens Procore’s analytics and forecasting accuracy across multi-party projects.

Universal adoption across subcontractors remains difficult, and governance plus permissions must balance open collaboration with regulatory and contractual compliance.

High upfront cost and 6-12 month deployments stall SMB adoption

High upfront and total cost (tens–hundreds k) limits SMB adoption and extends 6–12 month sales cycles. Deployments need 6–12 months plus 20–30% extra IT effort for data migration, with field resistance adding 3+ months to time-to-value. Cycle sensitivity and module cherry-picking reduce ACV and increase churn risk.

| Weakness | Metric |

|---|---|

| Cost barrier | tens–hundreds k |

| Deployment time | 6–12 months |

| Integration effort | +20–30% IT |

| Field delay | +3 months |

Same Document Delivered

Procore SWOT Analysis

This is the actual Procore SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and it reflects the same structured, editable content. Buy now to unlock the complete, detailed version.