Progressive Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

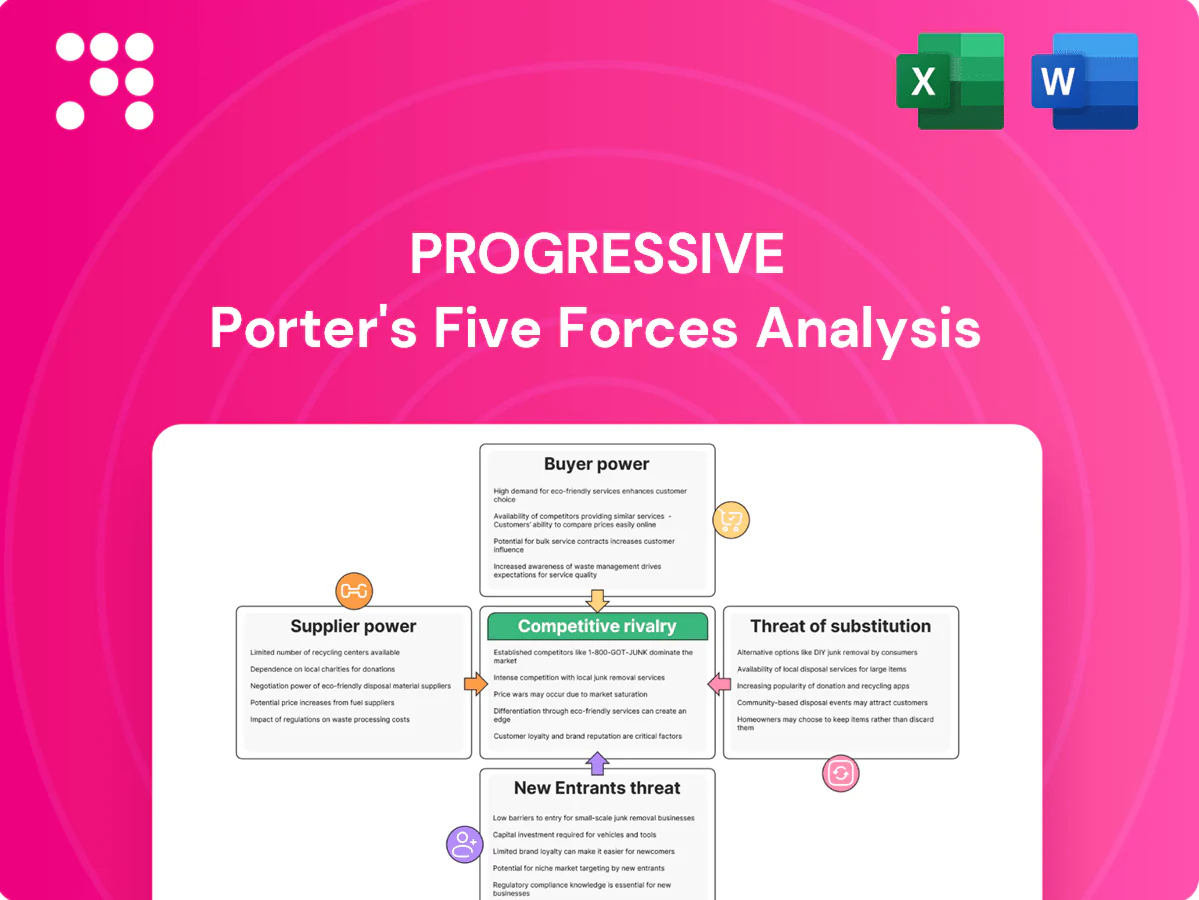

Progressive faces moderate buyer power, intense rivalry, evolving substitute threats from insurtech, constrained supplier leverage, and manageable new entrant risk due to scale and regulation. This snapshot highlights strategic pressure points but omits detailed ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, market pressures, and strategic opportunities tailored to Progressive.

Suppliers Bargaining Power

Data and telematics vendors

Progressive relies heavily on third-party credit, driving record and telematics data to price risk, with telematics enrollment exceeding 4 million devices and the company writing over 20 million policies in force in 2024, giving it scale to contest suppliers. A concentrated set of high-quality vendors can extract pricing and contractual concessions, and switching raises costs from model recalibration and compliance. Progressive’s scale enables multi-sourcing and negotiation leverage to mitigate supplier power.

Auto repair networks and parts

Claims fulfillment relies on repair shops and OEM/aftermarket parts suppliers; regional concentration and tight shop capacity in 2024 have increased cycle times and costs in high-density markets. Direct Repair Program partnerships and volume steerage reduce supplier leverage by directing repair flow and negotiating parts discounts. However, 2024 supply-chain shocks and parts inflation continue to pressure loss costs and repair timelines.

Reinsurance and capital markets

Catastrophe and excess-of-loss reinsurance remain key for risk transfer and capital efficiency; hard markets in 2023–24 pushed reinsurance pricing roughly 15–25% and raised attachment points, pressuring expense ratios. Progressive’s strong balance sheet (statutory surplus around $45 billion in 2024) and portfolio diversification improve negotiating leverage. Growth of alternative capital—ILS market ~45 billion in 2024—and higher retentions moderate supplier dependence.

IT platforms and cloud infrastructure

Reliance on core systems, cloud, and analytics creates vendor lock-in risks that can disrupt underwriting and claims during migrations or downtime; competitive cloud market shares in 2024 (AWS 32%, Microsoft 22%, Google 10% per Canalys) concentrate but do not monopolize supply. Progressive’s engineering depth and hybrid architectures reduce single-vendor dependence and operational exposure, while competitive cloud pricing limits supplier pricing power.

- Vendor lock-in risk: migration downtime can halt underwriting/claims

- 2024 cloud shares: AWS 32%, MS 22%, GCP 10%

- Hybrid architecture: lowers single-vendor exposure

- Competitive market: constrains supplier pricing power

Distribution intermediaries

Independent agents act as quasi-suppliers of demand for Progressive, with top agents able to negotiate higher commissions or marketing support; in 2024 Progressive emphasized expanding direct and digital channels to curb that leverage. Progressive’s direct-online growth in 2024 reduced reliance on high-power agents, and a multi-channel mix gives the company flexibility to shift volume and terms across channels.

- Agents = quasi-suppliers of demand

- Top agents can extract higher commissions/marketing

- Direct/digital growth in 2024 reduced agent leverage

- Multi-channel mix enables bargaining flexibility

Scale, telematics (4M+), and $45B surplus temper supplier power amid reinsurance price shock

Progressive depends on third-party data, repair shops, reinsurers and cloud vendors; scale, telematics (4M+ devices) and 20M policies in force plus statutory surplus ~$45B in 2024 limit supplier power, but concentrated vendors, parts inflation and hard reinsurance (+15–25% pricing 2023–24) sustain leverage. Direct/digital growth reduces agent bargaining.

| Metric | 2024 |

|---|---|

| Telematics devices | 4M+ |

| Policies in force | 20M+ |

| Statutory surplus | $45B |

| Reinsurance price change | +15–25% |

What is included in the product

Tailored Porter’s Five Forces analysis for Progressive that uncovers key drivers of competition, customer and supplier power, substitution and entrant risks, identifies disruptive threats and market dynamics protecting incumbents, and delivers strategic insights for investors, managers, and analysts.

A concise, one-sheet Progressive Porter’s Five Forces that relieves strategic uncertainty—customize pressure levels, swap in your data, and visualize impacts instantly with an intuitive spider chart for board-ready slides.

Customers Bargaining Power

Price-sensitive auto policyholders

Auto insurance is highly commoditized and easily shopped online, so policyholders exert strong price pressure and frequently switch at renewal with low friction, increasing sensitivity to premium changes in 2024.

Progressive offsets churn through usage-based discounts (Snapshot/Usage-Based Insurance) and bundling, which in 2024 continued to improve retention and lower lapse rates.

Progressive also leverages brand recognition, service quality and fast claims handling to defend margins against pure price competition.

Commercial auto and small business clients

Commercial auto and small business buyers exert moderate bargaining power: many are professional-brokered and larger accounts can negotiate terms and pricing, while 2024 data show small firms comprise 99.9% of US businesses (SBA). Progressive’s underwriting discipline and telematics/data edge support rate adequacy, and deep cross-sell capabilities raise perceived value versus standalone carriers.

Independent agents as buyers

Independent agents place business with carriers offering best value and ease and can quickly steer volume away if compensation or service lags; Progressive’s agent tools and fast quoting increase stickiness. Progressive reported over 40,000 independent agency relationships in 2024, and its robust direct channel presence helps counter concentrated agent bargaining power.

Switching and multi-quoting behavior

Frequent shopping and multi-quoting erode loyalty and compress margins as customers compare offers across channels.

Aggregators and comparison sites increased pricing transparency in 2024, per McKinsey, intensifying rate sensitivity.

Retention programs, personalized pricing and superior claims handling — highlighted by the 2024 J.D. Power U.S. Auto Insurance Study as the top loyalty driver — reduce defection risk.

- Frequent quoting compresses margins

- Aggregators boost transparency (2024 McKinsey)

- Retention + personalization cut churn

- Claims experience drives loyalty (2024 J.D. Power)

Regulatory-driven consumer protections

Regulatory-driven consumer protections constrain Progressive’s pricing via filing and approval processes, indirectly empowering buyers; regulators can demand refunds or rollbacks after adverse reviews. Progressive mitigates this through actuarially supported filings, strict compliance, and transparent communications to preserve trust and acceptance.

- Filing approvals limit price agility

- Regulators can force refunds/rollbacks

- Progressive uses actuarial justification

- Transparency supports customer trust

Customer price power forces insurers toward usage-based discounts, bundling and fast claims

Customers wield high price bargaining power in auto insurance due to easy online shopping and frequent multi-quoting, pressuring premiums in 2024. Progressive counters with Snapshot usage-based discounts, bundling and strong claims service to preserve retention and margins. Commercial buyers and 40,000+ independent agencies (2024) exert moderate negotiation leverage, while regulators and aggregators (2024 McKinsey) increase transparency and constrain pricing.

| Metric | 2024 Value |

|---|---|

| Independent agencies | 40,000+ (Progressive) |

| US small businesses | 99.9% (SBA) |

| Top loyalty driver | Claims experience (2024 J.D. Power) |

Preview the Actual Deliverable

Progressive Porter's Five Forces Analysis

This preview shows the exact Progressive Porter's Five Forces Analysis you'll receive—no surprises, no placeholders. It presents competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with supporting evidence and implications. The document is fully formatted and ready for immediate download after purchase.

A Must-Have Tool for Decision-Makers

Progressive faces moderate buyer power, intense rivalry, evolving substitute threats from insurtech, constrained supplier leverage, and manageable new entrant risk due to scale and regulation. This snapshot highlights strategic pressure points but omits detailed ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, market pressures, and strategic opportunities tailored to Progressive.

Suppliers Bargaining Power

Data and telematics vendors

Progressive relies heavily on third-party credit, driving record and telematics data to price risk, with telematics enrollment exceeding 4 million devices and the company writing over 20 million policies in force in 2024, giving it scale to contest suppliers. A concentrated set of high-quality vendors can extract pricing and contractual concessions, and switching raises costs from model recalibration and compliance. Progressive’s scale enables multi-sourcing and negotiation leverage to mitigate supplier power.

Auto repair networks and parts

Claims fulfillment relies on repair shops and OEM/aftermarket parts suppliers; regional concentration and tight shop capacity in 2024 have increased cycle times and costs in high-density markets. Direct Repair Program partnerships and volume steerage reduce supplier leverage by directing repair flow and negotiating parts discounts. However, 2024 supply-chain shocks and parts inflation continue to pressure loss costs and repair timelines.

Reinsurance and capital markets

Catastrophe and excess-of-loss reinsurance remain key for risk transfer and capital efficiency; hard markets in 2023–24 pushed reinsurance pricing roughly 15–25% and raised attachment points, pressuring expense ratios. Progressive’s strong balance sheet (statutory surplus around $45 billion in 2024) and portfolio diversification improve negotiating leverage. Growth of alternative capital—ILS market ~45 billion in 2024—and higher retentions moderate supplier dependence.

IT platforms and cloud infrastructure

Reliance on core systems, cloud, and analytics creates vendor lock-in risks that can disrupt underwriting and claims during migrations or downtime; competitive cloud market shares in 2024 (AWS 32%, Microsoft 22%, Google 10% per Canalys) concentrate but do not monopolize supply. Progressive’s engineering depth and hybrid architectures reduce single-vendor dependence and operational exposure, while competitive cloud pricing limits supplier pricing power.

- Vendor lock-in risk: migration downtime can halt underwriting/claims

- 2024 cloud shares: AWS 32%, MS 22%, GCP 10%

- Hybrid architecture: lowers single-vendor exposure

- Competitive market: constrains supplier pricing power

Distribution intermediaries

Independent agents act as quasi-suppliers of demand for Progressive, with top agents able to negotiate higher commissions or marketing support; in 2024 Progressive emphasized expanding direct and digital channels to curb that leverage. Progressive’s direct-online growth in 2024 reduced reliance on high-power agents, and a multi-channel mix gives the company flexibility to shift volume and terms across channels.

- Agents = quasi-suppliers of demand

- Top agents can extract higher commissions/marketing

- Direct/digital growth in 2024 reduced agent leverage

- Multi-channel mix enables bargaining flexibility

Scale, telematics (4M+), and $45B surplus temper supplier power amid reinsurance price shock

Progressive depends on third-party data, repair shops, reinsurers and cloud vendors; scale, telematics (4M+ devices) and 20M policies in force plus statutory surplus ~$45B in 2024 limit supplier power, but concentrated vendors, parts inflation and hard reinsurance (+15–25% pricing 2023–24) sustain leverage. Direct/digital growth reduces agent bargaining.

| Metric | 2024 |

|---|---|

| Telematics devices | 4M+ |

| Policies in force | 20M+ |

| Statutory surplus | $45B |

| Reinsurance price change | +15–25% |

What is included in the product

Tailored Porter’s Five Forces analysis for Progressive that uncovers key drivers of competition, customer and supplier power, substitution and entrant risks, identifies disruptive threats and market dynamics protecting incumbents, and delivers strategic insights for investors, managers, and analysts.

A concise, one-sheet Progressive Porter’s Five Forces that relieves strategic uncertainty—customize pressure levels, swap in your data, and visualize impacts instantly with an intuitive spider chart for board-ready slides.

Customers Bargaining Power

Price-sensitive auto policyholders

Auto insurance is highly commoditized and easily shopped online, so policyholders exert strong price pressure and frequently switch at renewal with low friction, increasing sensitivity to premium changes in 2024.

Progressive offsets churn through usage-based discounts (Snapshot/Usage-Based Insurance) and bundling, which in 2024 continued to improve retention and lower lapse rates.

Progressive also leverages brand recognition, service quality and fast claims handling to defend margins against pure price competition.

Commercial auto and small business clients

Commercial auto and small business buyers exert moderate bargaining power: many are professional-brokered and larger accounts can negotiate terms and pricing, while 2024 data show small firms comprise 99.9% of US businesses (SBA). Progressive’s underwriting discipline and telematics/data edge support rate adequacy, and deep cross-sell capabilities raise perceived value versus standalone carriers.

Independent agents as buyers

Independent agents place business with carriers offering best value and ease and can quickly steer volume away if compensation or service lags; Progressive’s agent tools and fast quoting increase stickiness. Progressive reported over 40,000 independent agency relationships in 2024, and its robust direct channel presence helps counter concentrated agent bargaining power.

Switching and multi-quoting behavior

Frequent shopping and multi-quoting erode loyalty and compress margins as customers compare offers across channels.

Aggregators and comparison sites increased pricing transparency in 2024, per McKinsey, intensifying rate sensitivity.

Retention programs, personalized pricing and superior claims handling — highlighted by the 2024 J.D. Power U.S. Auto Insurance Study as the top loyalty driver — reduce defection risk.

- Frequent quoting compresses margins

- Aggregators boost transparency (2024 McKinsey)

- Retention + personalization cut churn

- Claims experience drives loyalty (2024 J.D. Power)

Regulatory-driven consumer protections

Regulatory-driven consumer protections constrain Progressive’s pricing via filing and approval processes, indirectly empowering buyers; regulators can demand refunds or rollbacks after adverse reviews. Progressive mitigates this through actuarially supported filings, strict compliance, and transparent communications to preserve trust and acceptance.

- Filing approvals limit price agility

- Regulators can force refunds/rollbacks

- Progressive uses actuarial justification

- Transparency supports customer trust

Customer price power forces insurers toward usage-based discounts, bundling and fast claims

Customers wield high price bargaining power in auto insurance due to easy online shopping and frequent multi-quoting, pressuring premiums in 2024. Progressive counters with Snapshot usage-based discounts, bundling and strong claims service to preserve retention and margins. Commercial buyers and 40,000+ independent agencies (2024) exert moderate negotiation leverage, while regulators and aggregators (2024 McKinsey) increase transparency and constrain pricing.

| Metric | 2024 Value |

|---|---|

| Independent agencies | 40,000+ (Progressive) |

| US small businesses | 99.9% (SBA) |

| Top loyalty driver | Claims experience (2024 J.D. Power) |

Preview the Actual Deliverable

Progressive Porter's Five Forces Analysis

This preview shows the exact Progressive Porter's Five Forces Analysis you'll receive—no surprises, no placeholders. It presents competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with supporting evidence and implications. The document is fully formatted and ready for immediate download after purchase.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Progressive faces moderate buyer power, intense rivalry, evolving substitute threats from insurtech, constrained supplier leverage, and manageable new entrant risk due to scale and regulation. This snapshot highlights strategic pressure points but omits detailed ratings, visuals, and actionable recommendations. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, market pressures, and strategic opportunities tailored to Progressive.

Suppliers Bargaining Power

Data and telematics vendors

Progressive relies heavily on third-party credit, driving record and telematics data to price risk, with telematics enrollment exceeding 4 million devices and the company writing over 20 million policies in force in 2024, giving it scale to contest suppliers. A concentrated set of high-quality vendors can extract pricing and contractual concessions, and switching raises costs from model recalibration and compliance. Progressive’s scale enables multi-sourcing and negotiation leverage to mitigate supplier power.

Auto repair networks and parts

Claims fulfillment relies on repair shops and OEM/aftermarket parts suppliers; regional concentration and tight shop capacity in 2024 have increased cycle times and costs in high-density markets. Direct Repair Program partnerships and volume steerage reduce supplier leverage by directing repair flow and negotiating parts discounts. However, 2024 supply-chain shocks and parts inflation continue to pressure loss costs and repair timelines.

Reinsurance and capital markets

Catastrophe and excess-of-loss reinsurance remain key for risk transfer and capital efficiency; hard markets in 2023–24 pushed reinsurance pricing roughly 15–25% and raised attachment points, pressuring expense ratios. Progressive’s strong balance sheet (statutory surplus around $45 billion in 2024) and portfolio diversification improve negotiating leverage. Growth of alternative capital—ILS market ~45 billion in 2024—and higher retentions moderate supplier dependence.

IT platforms and cloud infrastructure

Reliance on core systems, cloud, and analytics creates vendor lock-in risks that can disrupt underwriting and claims during migrations or downtime; competitive cloud market shares in 2024 (AWS 32%, Microsoft 22%, Google 10% per Canalys) concentrate but do not monopolize supply. Progressive’s engineering depth and hybrid architectures reduce single-vendor dependence and operational exposure, while competitive cloud pricing limits supplier pricing power.

- Vendor lock-in risk: migration downtime can halt underwriting/claims

- 2024 cloud shares: AWS 32%, MS 22%, GCP 10%

- Hybrid architecture: lowers single-vendor exposure

- Competitive market: constrains supplier pricing power

Distribution intermediaries

Independent agents act as quasi-suppliers of demand for Progressive, with top agents able to negotiate higher commissions or marketing support; in 2024 Progressive emphasized expanding direct and digital channels to curb that leverage. Progressive’s direct-online growth in 2024 reduced reliance on high-power agents, and a multi-channel mix gives the company flexibility to shift volume and terms across channels.

- Agents = quasi-suppliers of demand

- Top agents can extract higher commissions/marketing

- Direct/digital growth in 2024 reduced agent leverage

- Multi-channel mix enables bargaining flexibility

Scale, telematics (4M+), and $45B surplus temper supplier power amid reinsurance price shock

Progressive depends on third-party data, repair shops, reinsurers and cloud vendors; scale, telematics (4M+ devices) and 20M policies in force plus statutory surplus ~$45B in 2024 limit supplier power, but concentrated vendors, parts inflation and hard reinsurance (+15–25% pricing 2023–24) sustain leverage. Direct/digital growth reduces agent bargaining.

| Metric | 2024 |

|---|---|

| Telematics devices | 4M+ |

| Policies in force | 20M+ |

| Statutory surplus | $45B |

| Reinsurance price change | +15–25% |

What is included in the product

Tailored Porter’s Five Forces analysis for Progressive that uncovers key drivers of competition, customer and supplier power, substitution and entrant risks, identifies disruptive threats and market dynamics protecting incumbents, and delivers strategic insights for investors, managers, and analysts.

A concise, one-sheet Progressive Porter’s Five Forces that relieves strategic uncertainty—customize pressure levels, swap in your data, and visualize impacts instantly with an intuitive spider chart for board-ready slides.

Customers Bargaining Power

Price-sensitive auto policyholders

Auto insurance is highly commoditized and easily shopped online, so policyholders exert strong price pressure and frequently switch at renewal with low friction, increasing sensitivity to premium changes in 2024.

Progressive offsets churn through usage-based discounts (Snapshot/Usage-Based Insurance) and bundling, which in 2024 continued to improve retention and lower lapse rates.

Progressive also leverages brand recognition, service quality and fast claims handling to defend margins against pure price competition.

Commercial auto and small business clients

Commercial auto and small business buyers exert moderate bargaining power: many are professional-brokered and larger accounts can negotiate terms and pricing, while 2024 data show small firms comprise 99.9% of US businesses (SBA). Progressive’s underwriting discipline and telematics/data edge support rate adequacy, and deep cross-sell capabilities raise perceived value versus standalone carriers.

Independent agents as buyers

Independent agents place business with carriers offering best value and ease and can quickly steer volume away if compensation or service lags; Progressive’s agent tools and fast quoting increase stickiness. Progressive reported over 40,000 independent agency relationships in 2024, and its robust direct channel presence helps counter concentrated agent bargaining power.

Switching and multi-quoting behavior

Frequent shopping and multi-quoting erode loyalty and compress margins as customers compare offers across channels.

Aggregators and comparison sites increased pricing transparency in 2024, per McKinsey, intensifying rate sensitivity.

Retention programs, personalized pricing and superior claims handling — highlighted by the 2024 J.D. Power U.S. Auto Insurance Study as the top loyalty driver — reduce defection risk.

- Frequent quoting compresses margins

- Aggregators boost transparency (2024 McKinsey)

- Retention + personalization cut churn

- Claims experience drives loyalty (2024 J.D. Power)

Regulatory-driven consumer protections

Regulatory-driven consumer protections constrain Progressive’s pricing via filing and approval processes, indirectly empowering buyers; regulators can demand refunds or rollbacks after adverse reviews. Progressive mitigates this through actuarially supported filings, strict compliance, and transparent communications to preserve trust and acceptance.

- Filing approvals limit price agility

- Regulators can force refunds/rollbacks

- Progressive uses actuarial justification

- Transparency supports customer trust

Customer price power forces insurers toward usage-based discounts, bundling and fast claims

Customers wield high price bargaining power in auto insurance due to easy online shopping and frequent multi-quoting, pressuring premiums in 2024. Progressive counters with Snapshot usage-based discounts, bundling and strong claims service to preserve retention and margins. Commercial buyers and 40,000+ independent agencies (2024) exert moderate negotiation leverage, while regulators and aggregators (2024 McKinsey) increase transparency and constrain pricing.

| Metric | 2024 Value |

|---|---|

| Independent agencies | 40,000+ (Progressive) |

| US small businesses | 99.9% (SBA) |

| Top loyalty driver | Claims experience (2024 J.D. Power) |

Preview the Actual Deliverable

Progressive Porter's Five Forces Analysis

This preview shows the exact Progressive Porter's Five Forces Analysis you'll receive—no surprises, no placeholders. It presents competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with supporting evidence and implications. The document is fully formatted and ready for immediate download after purchase.