Puccini SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

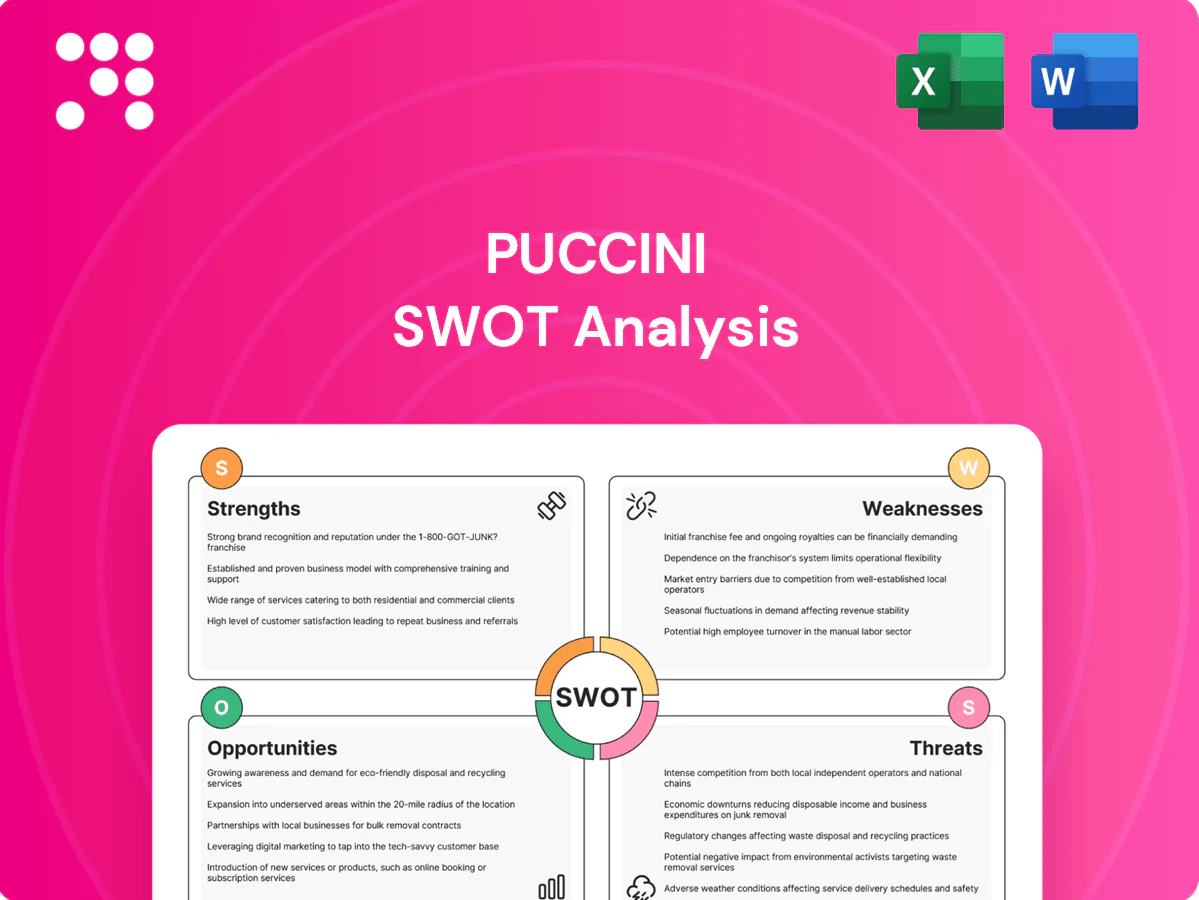

Puccini’s SWOT snapshot highlights distinctive strengths, market risks, and untapped growth corridors—vital intel for investors and strategists. Want the full story behind its competitive position and growth drivers? Purchase the complete SWOT analysis to get a professionally written, editable report and Excel matrix for planning and pitches.

Strengths

Niche accessories focus

Specializing in men’s ties, bow ties and pocket squares sharpens Puccini’s brand identity and operational expertise, enabling focused SKU planning and higher unit margins per accessory. Focused assortments streamline sourcing, quality control and merchandising, cutting inventory complexity versus broad apparel lines. This clarity targets style-conscious customers for formalwear; e-commerce channels (about 30% of global apparel sales in 2024) amplify reach.

Broad design and material range

Offering diverse patterns, colors and fabrics lets Puccini address multiple tastes and occasions, supporting both seasonal capsules and timeless basics; the global men's accessories market reached about USD 48.3bn in 2024, underscoring demand diversity. This depth enables upselling and bundling (tie + pocket square), lifting average order value, and reduces reliance on any single trend by spreading SKU-driven revenue across categories.

German quality positioning

German origin signals reliability and craftsmanship across Europe, supported by Germany’s €1.44 trillion goods exports in 2023 which reinforce the Made in Germany premium. Perceived quality underpins pricing integrity and wholesale credibility, enabling consistent MSRP strategies. It builds trust for online customers unfamiliar with Puccini and facilitates entry into premium boutique channels seeking reputable sourcing.

Dual-channel distribution

Dual-channel distribution combines wholesale reach with an official online store, diversifying revenue streams and lowering partner concentration risk; global e-commerce reached 21.8% of retail sales in 2024, validating DTC upside. Wholesale drives volume and brand presence while DTC preserves margins and customer data and enables rapid design testing and replenishment.

- Wholesale: volume & reach

- DTC: margins & first-party data

- Online store: fast testing & replenishment

- Channel mix: reduces partner concentration risk

Accessory-friendly operations

Accessory SKUs are size-agnostic, simplifying inventory management and enabling 30–40% higher SKU density per cubic meter versus apparel; 2024 channel data show accessory return rates near 5% vs apparel ~20%, improving unit economics and gross margin stability. Compact form factors cut logistics costs and support efficient international shipping from a centralized hub, lowering per-unit shipping spend.

- size-agnostic SKUs

- ~5% returns vs ~20% apparel

- higher SKU density, lower logistics

- central-hub international shipping

Focused tie accessories boost margins; returns ~5% vs apparel ~20%, e-commerce 21.8%.

Focused SKU set in ties, bow ties and pocket squares boosts gross margins and simplifies sourcing; accessories returned ~5% vs apparel ~20% in 2024. German origin supports premium pricing (Germany goods exports €1.44T in 2023). Dual-channel model captures wholesale scale and DTC margin upside as e‑commerce was 21.8% of retail sales in 2024.

| Metric | Value |

|---|---|

| Men's accessories market (2024) | USD 48.3bn |

| E‑commerce retail share (2024) | 21.8% |

| Germany goods exports (2023) | €1.44T |

| Accessory return rate (2024) | ~5% |

What is included in the product

Provides a concise SWOT analysis of Puccini, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess its competitive position and strategic risks.

Provides a concise Puccini SWOT matrix for fast alignment of artistic and operational strategy, easing stakeholder buy-in and decision-making.

Weaknesses

Narrow category scope

Confinement to men’s accessories limits Puccini’s total addressable market, with industry reports in 2024 showing men’s accessory spend represents roughly one-quarter of global accessory sales. Fewer cross-category baskets cap average order values and reduce repeat-purchase drivers. This narrow scope heightens vulnerability to category-specific demand swings and makes expansion risky, requiring careful brand stretch to avoid dilution.

Event-driven demand

Occasion wear sales concentrate around weddings, holidays and ceremonies, with the US wedding market estimated at about 79 billion in 2022 (The Knot), creating pronounced peaks. This seasonality complicates demand forecasting and working-capital planning as inventory must ramp for short windows. Off-peak periods often force discounting that compresses margins, while wholesale sell-in magnifies volatility by concentrating orders and returns around key seasons.

Brand awareness constraints

In a crowded accessories market, distinctiveness for Puccini may be modest against hundreds of contemporaries, limiting organic discovery. Limited global recognition raises online customer acquisition costs and weakens conversion despite the personal luxury goods market reaching about €336 billion in 2023 (Bain). Competing with heritage and designer labels with established equity is challenging, while wholesale retailer control can dilute curated brand presentation.

Wholesale dependency

Reliance on wholesale partners exposes Puccini to buyer assortment shifts and delistings, eroding sales predictability. Thinner wholesale margins and retailer-controlled promotions compress profitability and limit pricing power. Extended payment terms lengthen cash conversion cycles and raise receivables risk while inconsistent retailer merchandising weakens brand presentation.

- Exposure to buyer delistings

- Lower margins, promo-driven

- Longer payment cycles

- Inconsistent in-store visuals

Trend sensitivity

Formal accessory trends shift with workplace and cultural change, and McKinsey State of Fashion 2024 notes trend cycles now compress to roughly 3–4 months, so misjudging patterns or colors can convert into slow-moving stock and higher markdowns; Edited reported fashion markdowns near 28% in 2023. Fabric-mix bets (silk vs synthetics) raise obsolescence risk, and small misses across a wide SKU grid amplify inventory write-downs.

- Trend cycle: ~3–4 months (McKinsey 2024)

- Wholesale markdowns: ~28% (Edited 2023)

- High SKU breadth multiplies small forecasting errors

Men-only caps TAM; accessories ≈25%, markdowns ~28%

Puccini’s men-only focus limits TAM—men’s accessories ≈25% of global accessory spend—raising CAC and capping AOV. Seasonality (US wedding market ≈$79B) and 3–4 month trend cycles force inventory spikes and markdowns (~28%), compressing margins. Heavy wholesale exposure widens payment cycles and delisting risk versus heritage brands.

| Weakness | Metric | Value |

|---|---|---|

| TAM concentration | Share of accessories | ≈25% |

| Seasonality | US wedding market | $79B (2022) |

| Trend risk | Cycle / markdowns | 3–4 months / ~28% |

| Wholesale exposure | Risks | Delistings, longer payments |

Preview the Actual Deliverable

Puccini SWOT Analysis

This is the actual Puccini SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and reflects the structure and depth of the final file. Buy now to unlock the complete, editable version immediately after checkout.

Elevate Your Analysis with the Complete SWOT Report

Puccini’s SWOT snapshot highlights distinctive strengths, market risks, and untapped growth corridors—vital intel for investors and strategists. Want the full story behind its competitive position and growth drivers? Purchase the complete SWOT analysis to get a professionally written, editable report and Excel matrix for planning and pitches.

Strengths

Niche accessories focus

Specializing in men’s ties, bow ties and pocket squares sharpens Puccini’s brand identity and operational expertise, enabling focused SKU planning and higher unit margins per accessory. Focused assortments streamline sourcing, quality control and merchandising, cutting inventory complexity versus broad apparel lines. This clarity targets style-conscious customers for formalwear; e-commerce channels (about 30% of global apparel sales in 2024) amplify reach.

Broad design and material range

Offering diverse patterns, colors and fabrics lets Puccini address multiple tastes and occasions, supporting both seasonal capsules and timeless basics; the global men's accessories market reached about USD 48.3bn in 2024, underscoring demand diversity. This depth enables upselling and bundling (tie + pocket square), lifting average order value, and reduces reliance on any single trend by spreading SKU-driven revenue across categories.

German quality positioning

German origin signals reliability and craftsmanship across Europe, supported by Germany’s €1.44 trillion goods exports in 2023 which reinforce the Made in Germany premium. Perceived quality underpins pricing integrity and wholesale credibility, enabling consistent MSRP strategies. It builds trust for online customers unfamiliar with Puccini and facilitates entry into premium boutique channels seeking reputable sourcing.

Dual-channel distribution

Dual-channel distribution combines wholesale reach with an official online store, diversifying revenue streams and lowering partner concentration risk; global e-commerce reached 21.8% of retail sales in 2024, validating DTC upside. Wholesale drives volume and brand presence while DTC preserves margins and customer data and enables rapid design testing and replenishment.

- Wholesale: volume & reach

- DTC: margins & first-party data

- Online store: fast testing & replenishment

- Channel mix: reduces partner concentration risk

Accessory-friendly operations

Accessory SKUs are size-agnostic, simplifying inventory management and enabling 30–40% higher SKU density per cubic meter versus apparel; 2024 channel data show accessory return rates near 5% vs apparel ~20%, improving unit economics and gross margin stability. Compact form factors cut logistics costs and support efficient international shipping from a centralized hub, lowering per-unit shipping spend.

- size-agnostic SKUs

- ~5% returns vs ~20% apparel

- higher SKU density, lower logistics

- central-hub international shipping

Focused tie accessories boost margins; returns ~5% vs apparel ~20%, e-commerce 21.8%.

Focused SKU set in ties, bow ties and pocket squares boosts gross margins and simplifies sourcing; accessories returned ~5% vs apparel ~20% in 2024. German origin supports premium pricing (Germany goods exports €1.44T in 2023). Dual-channel model captures wholesale scale and DTC margin upside as e‑commerce was 21.8% of retail sales in 2024.

| Metric | Value |

|---|---|

| Men's accessories market (2024) | USD 48.3bn |

| E‑commerce retail share (2024) | 21.8% |

| Germany goods exports (2023) | €1.44T |

| Accessory return rate (2024) | ~5% |

What is included in the product

Provides a concise SWOT analysis of Puccini, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess its competitive position and strategic risks.

Provides a concise Puccini SWOT matrix for fast alignment of artistic and operational strategy, easing stakeholder buy-in and decision-making.

Weaknesses

Narrow category scope

Confinement to men’s accessories limits Puccini’s total addressable market, with industry reports in 2024 showing men’s accessory spend represents roughly one-quarter of global accessory sales. Fewer cross-category baskets cap average order values and reduce repeat-purchase drivers. This narrow scope heightens vulnerability to category-specific demand swings and makes expansion risky, requiring careful brand stretch to avoid dilution.

Event-driven demand

Occasion wear sales concentrate around weddings, holidays and ceremonies, with the US wedding market estimated at about 79 billion in 2022 (The Knot), creating pronounced peaks. This seasonality complicates demand forecasting and working-capital planning as inventory must ramp for short windows. Off-peak periods often force discounting that compresses margins, while wholesale sell-in magnifies volatility by concentrating orders and returns around key seasons.

Brand awareness constraints

In a crowded accessories market, distinctiveness for Puccini may be modest against hundreds of contemporaries, limiting organic discovery. Limited global recognition raises online customer acquisition costs and weakens conversion despite the personal luxury goods market reaching about €336 billion in 2023 (Bain). Competing with heritage and designer labels with established equity is challenging, while wholesale retailer control can dilute curated brand presentation.

Wholesale dependency

Reliance on wholesale partners exposes Puccini to buyer assortment shifts and delistings, eroding sales predictability. Thinner wholesale margins and retailer-controlled promotions compress profitability and limit pricing power. Extended payment terms lengthen cash conversion cycles and raise receivables risk while inconsistent retailer merchandising weakens brand presentation.

- Exposure to buyer delistings

- Lower margins, promo-driven

- Longer payment cycles

- Inconsistent in-store visuals

Trend sensitivity

Formal accessory trends shift with workplace and cultural change, and McKinsey State of Fashion 2024 notes trend cycles now compress to roughly 3–4 months, so misjudging patterns or colors can convert into slow-moving stock and higher markdowns; Edited reported fashion markdowns near 28% in 2023. Fabric-mix bets (silk vs synthetics) raise obsolescence risk, and small misses across a wide SKU grid amplify inventory write-downs.

- Trend cycle: ~3–4 months (McKinsey 2024)

- Wholesale markdowns: ~28% (Edited 2023)

- High SKU breadth multiplies small forecasting errors

Men-only caps TAM; accessories ≈25%, markdowns ~28%

Puccini’s men-only focus limits TAM—men’s accessories ≈25% of global accessory spend—raising CAC and capping AOV. Seasonality (US wedding market ≈$79B) and 3–4 month trend cycles force inventory spikes and markdowns (~28%), compressing margins. Heavy wholesale exposure widens payment cycles and delisting risk versus heritage brands.

| Weakness | Metric | Value |

|---|---|---|

| TAM concentration | Share of accessories | ≈25% |

| Seasonality | US wedding market | $79B (2022) |

| Trend risk | Cycle / markdowns | 3–4 months / ~28% |

| Wholesale exposure | Risks | Delistings, longer payments |

Preview the Actual Deliverable

Puccini SWOT Analysis

This is the actual Puccini SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and reflects the structure and depth of the final file. Buy now to unlock the complete, editable version immediately after checkout.

Description

Elevate Your Analysis with the Complete SWOT Report

Puccini’s SWOT snapshot highlights distinctive strengths, market risks, and untapped growth corridors—vital intel for investors and strategists. Want the full story behind its competitive position and growth drivers? Purchase the complete SWOT analysis to get a professionally written, editable report and Excel matrix for planning and pitches.

Strengths

Niche accessories focus

Specializing in men’s ties, bow ties and pocket squares sharpens Puccini’s brand identity and operational expertise, enabling focused SKU planning and higher unit margins per accessory. Focused assortments streamline sourcing, quality control and merchandising, cutting inventory complexity versus broad apparel lines. This clarity targets style-conscious customers for formalwear; e-commerce channels (about 30% of global apparel sales in 2024) amplify reach.

Broad design and material range

Offering diverse patterns, colors and fabrics lets Puccini address multiple tastes and occasions, supporting both seasonal capsules and timeless basics; the global men's accessories market reached about USD 48.3bn in 2024, underscoring demand diversity. This depth enables upselling and bundling (tie + pocket square), lifting average order value, and reduces reliance on any single trend by spreading SKU-driven revenue across categories.

German quality positioning

German origin signals reliability and craftsmanship across Europe, supported by Germany’s €1.44 trillion goods exports in 2023 which reinforce the Made in Germany premium. Perceived quality underpins pricing integrity and wholesale credibility, enabling consistent MSRP strategies. It builds trust for online customers unfamiliar with Puccini and facilitates entry into premium boutique channels seeking reputable sourcing.

Dual-channel distribution

Dual-channel distribution combines wholesale reach with an official online store, diversifying revenue streams and lowering partner concentration risk; global e-commerce reached 21.8% of retail sales in 2024, validating DTC upside. Wholesale drives volume and brand presence while DTC preserves margins and customer data and enables rapid design testing and replenishment.

- Wholesale: volume & reach

- DTC: margins & first-party data

- Online store: fast testing & replenishment

- Channel mix: reduces partner concentration risk

Accessory-friendly operations

Accessory SKUs are size-agnostic, simplifying inventory management and enabling 30–40% higher SKU density per cubic meter versus apparel; 2024 channel data show accessory return rates near 5% vs apparel ~20%, improving unit economics and gross margin stability. Compact form factors cut logistics costs and support efficient international shipping from a centralized hub, lowering per-unit shipping spend.

- size-agnostic SKUs

- ~5% returns vs ~20% apparel

- higher SKU density, lower logistics

- central-hub international shipping

Focused tie accessories boost margins; returns ~5% vs apparel ~20%, e-commerce 21.8%.

Focused SKU set in ties, bow ties and pocket squares boosts gross margins and simplifies sourcing; accessories returned ~5% vs apparel ~20% in 2024. German origin supports premium pricing (Germany goods exports €1.44T in 2023). Dual-channel model captures wholesale scale and DTC margin upside as e‑commerce was 21.8% of retail sales in 2024.

| Metric | Value |

|---|---|

| Men's accessories market (2024) | USD 48.3bn |

| E‑commerce retail share (2024) | 21.8% |

| Germany goods exports (2023) | €1.44T |

| Accessory return rate (2024) | ~5% |

What is included in the product

Provides a concise SWOT analysis of Puccini, highlighting internal strengths and weaknesses alongside external opportunities and threats to assess its competitive position and strategic risks.

Provides a concise Puccini SWOT matrix for fast alignment of artistic and operational strategy, easing stakeholder buy-in and decision-making.

Weaknesses

Narrow category scope

Confinement to men’s accessories limits Puccini’s total addressable market, with industry reports in 2024 showing men’s accessory spend represents roughly one-quarter of global accessory sales. Fewer cross-category baskets cap average order values and reduce repeat-purchase drivers. This narrow scope heightens vulnerability to category-specific demand swings and makes expansion risky, requiring careful brand stretch to avoid dilution.

Event-driven demand

Occasion wear sales concentrate around weddings, holidays and ceremonies, with the US wedding market estimated at about 79 billion in 2022 (The Knot), creating pronounced peaks. This seasonality complicates demand forecasting and working-capital planning as inventory must ramp for short windows. Off-peak periods often force discounting that compresses margins, while wholesale sell-in magnifies volatility by concentrating orders and returns around key seasons.

Brand awareness constraints

In a crowded accessories market, distinctiveness for Puccini may be modest against hundreds of contemporaries, limiting organic discovery. Limited global recognition raises online customer acquisition costs and weakens conversion despite the personal luxury goods market reaching about €336 billion in 2023 (Bain). Competing with heritage and designer labels with established equity is challenging, while wholesale retailer control can dilute curated brand presentation.

Wholesale dependency

Reliance on wholesale partners exposes Puccini to buyer assortment shifts and delistings, eroding sales predictability. Thinner wholesale margins and retailer-controlled promotions compress profitability and limit pricing power. Extended payment terms lengthen cash conversion cycles and raise receivables risk while inconsistent retailer merchandising weakens brand presentation.

- Exposure to buyer delistings

- Lower margins, promo-driven

- Longer payment cycles

- Inconsistent in-store visuals

Trend sensitivity

Formal accessory trends shift with workplace and cultural change, and McKinsey State of Fashion 2024 notes trend cycles now compress to roughly 3–4 months, so misjudging patterns or colors can convert into slow-moving stock and higher markdowns; Edited reported fashion markdowns near 28% in 2023. Fabric-mix bets (silk vs synthetics) raise obsolescence risk, and small misses across a wide SKU grid amplify inventory write-downs.

- Trend cycle: ~3–4 months (McKinsey 2024)

- Wholesale markdowns: ~28% (Edited 2023)

- High SKU breadth multiplies small forecasting errors

Men-only caps TAM; accessories ≈25%, markdowns ~28%

Puccini’s men-only focus limits TAM—men’s accessories ≈25% of global accessory spend—raising CAC and capping AOV. Seasonality (US wedding market ≈$79B) and 3–4 month trend cycles force inventory spikes and markdowns (~28%), compressing margins. Heavy wholesale exposure widens payment cycles and delisting risk versus heritage brands.

| Weakness | Metric | Value |

|---|---|---|

| TAM concentration | Share of accessories | ≈25% |

| Seasonality | US wedding market | $79B (2022) |

| Trend risk | Cycle / markdowns | 3–4 months / ~28% |

| Wholesale exposure | Risks | Delistings, longer payments |

Preview the Actual Deliverable

Puccini SWOT Analysis

This is the actual Puccini SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and reflects the structure and depth of the final file. Buy now to unlock the complete, editable version immediately after checkout.