Puuilo Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Puuilo’s Porter’s Five Forces snapshot highlights key pressures — supplier leverage, buyer power, new entrant risk, substitute threats, and competitive rivalry — shaping its retail position. This brief overview teases strategic implications and operational vulnerabilities. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Puuilo.

Suppliers Bargaining Power

Fragmented suppliers

Many Puuilo product categories (DIY, pet, auto, garden) are sourced from numerous small and medium suppliers, diluting any single vendor’s leverage; across the EU 99.8% of firms are SMEs (Eurostat 2023), underscoring supplier fragmentation. Puuilo can benchmark prices and terms across alternatives, run tenders and maintain dual‑sourcing to drive down costs. Fragmentation enables rapid replacement of underperforming suppliers, improving supply resilience and margin control.

Private label scope

Expanding private-label lines shifts bargaining power toward Puuilo by cutting reliance on branded vendors and increasing margin capture through higher-margin own brands, while enhancing shelf control and product differentiation; however, rigorous quality assurance programs and managing minimum order quantity exposure are essential to mitigate reputational and inventory risks.

Import dependence

Global sourcing exposes Puuilo to FX, freight and lead-time pass-throughs — EUR/USD averaged ~1.09 in 2024 and Drewry WCI stayed elevated near USD 1,800/FEU, letting suppliers transfer costs. Long supply chains boost supplier power when capacity tightens, evidenced by sporadic 2024 port congestion and extended lead times. Hedging and multi-origin sourcing reduce FX/freight exposure, while nearshoring and seasonal buys demand agile, data-driven planning.

Logistics to Nordics

Serving a dispersed Finnish footprint (Finland population ~5.54 million, density ~18/km2 in 2024) gives logistics providers bargaining leverage; high per-km transport costs squeeze margins in Puuilo’s low-price model. Pooling volumes across categories and cross-docking measurably lower unit costs and reduce that leverage, while contracting multiple carriers cuts carrier-concentration risk.

- Dispersed footprint: raises leverage

- High transport cost: margin pressure

- Volume pooling/cross-dock: lowers leverage

- Multiple carriers: reduces concentration risk

Low switching costs

- Low switching costs limit supplier margins

- Framework agreements + KPIs drive consistency

- Niche/regulatory items retain supplier power

Low supplier power amid fragmented EU SME sourcing, offset by freight, FX and niche risks

Supplier power at Puuilo is generally low due to fragmented SME supplier base and standardised SKUs, strengthened by dual‑sourcing, tenders and private‑label expansion; exceptions exist for niche/regulatory SKUs. Global sourcing and freight/FX (EUR/USD ~1.09 in 2024; Drewry WCI ~1,800/FEU 2024) plus dispersed Finnish logistics raise supplier/carrier leverage.

| Metric | Value |

|---|---|

| EU SMEs (Eurostat) | 99.8% (2023) |

| Finland pop | 5.54M (2024) |

| EUR/USD | ~1.09 (2024) |

| Drewry WCI | ~1,800 USD/FEU (2024) |

What is included in the product

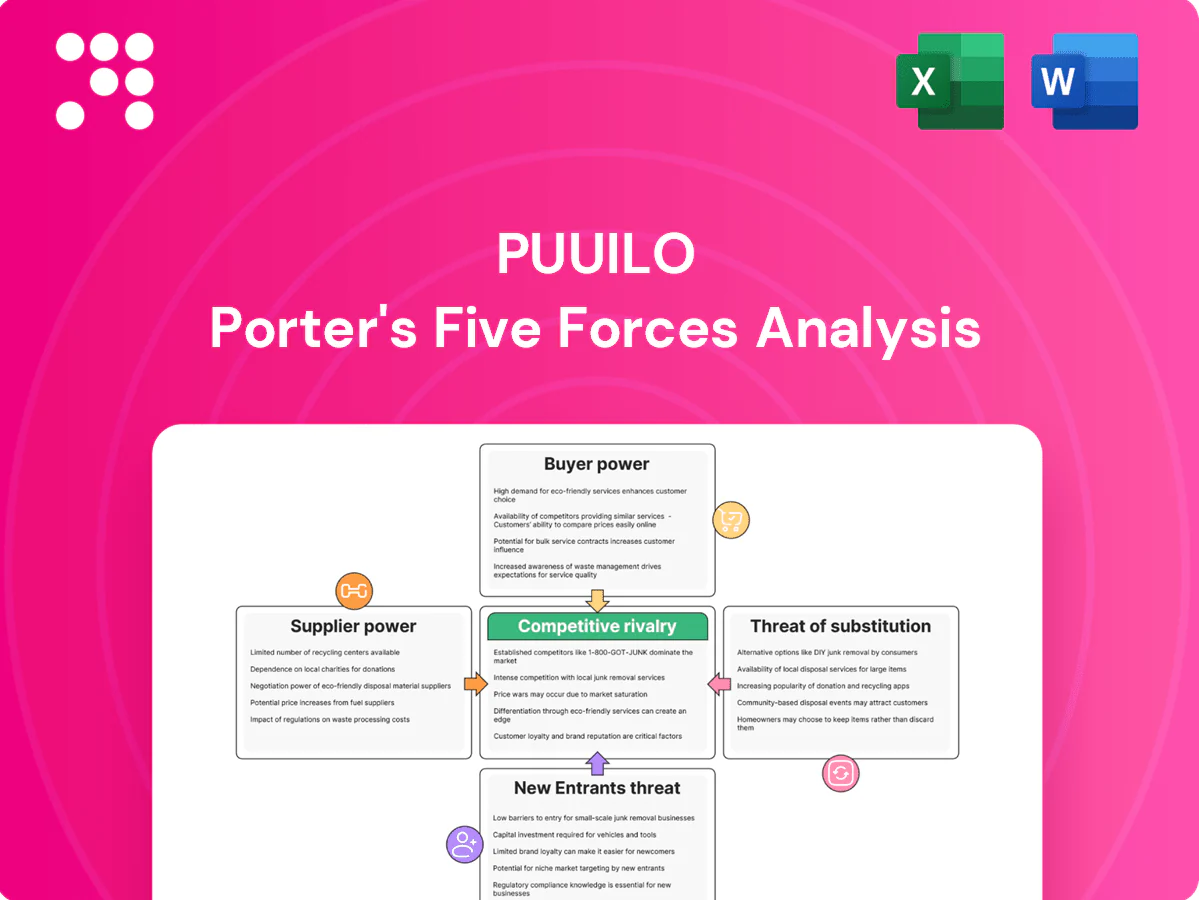

Provides a tailored Porter's Five Forces analysis for Puuilo, uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and industry rivalry, with strategic insights on disruptive threats, pricing influence, and barriers that protect incumbents.

Clear one-sheet Puuilo Porter's Five Forces summary for rapid decision-making, with customizable pressure levels and an instant spider chart to visualize strategic threats and opportunities.

Customers Bargaining Power

Highly price-sensitive

Puuilo’s discount positioning draws value-focused shoppers who readily switch on price; with 55 stores in Finland as of 2024, small price gaps can redirect local volumes to rivals. Frequent promotions by Puuilo and peers have conditioned customers to expect deals, raising purchase elasticity. Commoditized SKUs amplify buyer power, making margins sensitive to even modest markdowns.

Easy comparisons

Online search and retailer flyers from Tokmanni, Biltema, Jula and others make prices highly transparent, and with click-and-collect adoption up ~25% in Nordic DIY channels in 2024 customers compare offers across chains in minutes. Low switching costs let shoppers split baskets between stores, while price-matching and basket-value tactics (loyalty thresholds, free-click-and-collect) are used to retain spend.

Mixed B2C/B2B

Tradespeople and microbusinesses buy recurrently and in bulk, giving them negotiating weight that drives discount requests and contract pricing. In Finland SMEs make up 99.8% of firms, creating meaningful B2B volume for mixed B2C/B2B retailers like Puuilo. Loyalty tiers and anchored contract prices lock relationships, while service reliability and deep stock reduce churn and strengthen customer stickiness.

Limited differentiation

- Low differentiation — price/convenience drivers

- Assortment breadth — reduces switching

- Seasonal depth — ties customers to store

- Add‑ons (rental, advice) — increase stickiness

Loyalty and data

Loyalty programs, targeted offers and CRM reduce effective buyer power by personalizing value; 2024 retail studies show CRM-driven targeting can lift repeat-purchase rates by 5–10% and targeted promotions raise conversion up to 20%. Data-driven pricing shields margins on inelastic SKUs while basket analytics steer promotions to traffic drivers, shifting focus from item price to total basket value.

- Loyalty penetration: member-driven sales concentration

- CRM lift: +5–10% repeat rate (2024)

- Targeted promo conversion: up to +20% (2024)

Discount retailer: 55 stores, +25% click-&-collect; CRM and promos curb buyer pressure

Puuilo’s discount positioning and commoditized SKUs give buyers high price sensitivity; 55 stores (2024) mean local price gaps shift volumes. Price transparency and click‑and‑collect adoption (+25% 2024) lower switching costs; SMEs (99.8% of firms) add bulk negotiating power. CRM and targeted promos (CRM lift 5–10%, promo conversion up to 20% 2024) mitigate buyer pressure.

| Metric | Value (2024) |

|---|---|

| Stores | 55 |

| Click‑&‑collect growth | +25% |

| SME share (Finland) | 99.8% |

| CRM repeat lift | 5–10% |

| Promo conversion lift | up to 20% |

Preview the Actual Deliverable

Puuilo Porter's Five Forces Analysis

This preview of the Puuilo Porter's Five Forces analysis is the exact document you’ll receive after purchase—no placeholders, no mockups. It contains the full competitive assessment of supplier and buyer power, threat of entrants and substitutes, and industry rivalry, professionally formatted and ready to download. Purchase grants instant access to this identical file for immediate use.

A Must-Have Tool for Decision-Makers

Puuilo’s Porter’s Five Forces snapshot highlights key pressures — supplier leverage, buyer power, new entrant risk, substitute threats, and competitive rivalry — shaping its retail position. This brief overview teases strategic implications and operational vulnerabilities. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Puuilo.

Suppliers Bargaining Power

Fragmented suppliers

Many Puuilo product categories (DIY, pet, auto, garden) are sourced from numerous small and medium suppliers, diluting any single vendor’s leverage; across the EU 99.8% of firms are SMEs (Eurostat 2023), underscoring supplier fragmentation. Puuilo can benchmark prices and terms across alternatives, run tenders and maintain dual‑sourcing to drive down costs. Fragmentation enables rapid replacement of underperforming suppliers, improving supply resilience and margin control.

Private label scope

Expanding private-label lines shifts bargaining power toward Puuilo by cutting reliance on branded vendors and increasing margin capture through higher-margin own brands, while enhancing shelf control and product differentiation; however, rigorous quality assurance programs and managing minimum order quantity exposure are essential to mitigate reputational and inventory risks.

Import dependence

Global sourcing exposes Puuilo to FX, freight and lead-time pass-throughs — EUR/USD averaged ~1.09 in 2024 and Drewry WCI stayed elevated near USD 1,800/FEU, letting suppliers transfer costs. Long supply chains boost supplier power when capacity tightens, evidenced by sporadic 2024 port congestion and extended lead times. Hedging and multi-origin sourcing reduce FX/freight exposure, while nearshoring and seasonal buys demand agile, data-driven planning.

Logistics to Nordics

Serving a dispersed Finnish footprint (Finland population ~5.54 million, density ~18/km2 in 2024) gives logistics providers bargaining leverage; high per-km transport costs squeeze margins in Puuilo’s low-price model. Pooling volumes across categories and cross-docking measurably lower unit costs and reduce that leverage, while contracting multiple carriers cuts carrier-concentration risk.

- Dispersed footprint: raises leverage

- High transport cost: margin pressure

- Volume pooling/cross-dock: lowers leverage

- Multiple carriers: reduces concentration risk

Low switching costs

- Low switching costs limit supplier margins

- Framework agreements + KPIs drive consistency

- Niche/regulatory items retain supplier power

Low supplier power amid fragmented EU SME sourcing, offset by freight, FX and niche risks

Supplier power at Puuilo is generally low due to fragmented SME supplier base and standardised SKUs, strengthened by dual‑sourcing, tenders and private‑label expansion; exceptions exist for niche/regulatory SKUs. Global sourcing and freight/FX (EUR/USD ~1.09 in 2024; Drewry WCI ~1,800/FEU 2024) plus dispersed Finnish logistics raise supplier/carrier leverage.

| Metric | Value |

|---|---|

| EU SMEs (Eurostat) | 99.8% (2023) |

| Finland pop | 5.54M (2024) |

| EUR/USD | ~1.09 (2024) |

| Drewry WCI | ~1,800 USD/FEU (2024) |

What is included in the product

Provides a tailored Porter's Five Forces analysis for Puuilo, uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and industry rivalry, with strategic insights on disruptive threats, pricing influence, and barriers that protect incumbents.

Clear one-sheet Puuilo Porter's Five Forces summary for rapid decision-making, with customizable pressure levels and an instant spider chart to visualize strategic threats and opportunities.

Customers Bargaining Power

Highly price-sensitive

Puuilo’s discount positioning draws value-focused shoppers who readily switch on price; with 55 stores in Finland as of 2024, small price gaps can redirect local volumes to rivals. Frequent promotions by Puuilo and peers have conditioned customers to expect deals, raising purchase elasticity. Commoditized SKUs amplify buyer power, making margins sensitive to even modest markdowns.

Easy comparisons

Online search and retailer flyers from Tokmanni, Biltema, Jula and others make prices highly transparent, and with click-and-collect adoption up ~25% in Nordic DIY channels in 2024 customers compare offers across chains in minutes. Low switching costs let shoppers split baskets between stores, while price-matching and basket-value tactics (loyalty thresholds, free-click-and-collect) are used to retain spend.

Mixed B2C/B2B

Tradespeople and microbusinesses buy recurrently and in bulk, giving them negotiating weight that drives discount requests and contract pricing. In Finland SMEs make up 99.8% of firms, creating meaningful B2B volume for mixed B2C/B2B retailers like Puuilo. Loyalty tiers and anchored contract prices lock relationships, while service reliability and deep stock reduce churn and strengthen customer stickiness.

Limited differentiation

- Low differentiation — price/convenience drivers

- Assortment breadth — reduces switching

- Seasonal depth — ties customers to store

- Add‑ons (rental, advice) — increase stickiness

Loyalty and data

Loyalty programs, targeted offers and CRM reduce effective buyer power by personalizing value; 2024 retail studies show CRM-driven targeting can lift repeat-purchase rates by 5–10% and targeted promotions raise conversion up to 20%. Data-driven pricing shields margins on inelastic SKUs while basket analytics steer promotions to traffic drivers, shifting focus from item price to total basket value.

- Loyalty penetration: member-driven sales concentration

- CRM lift: +5–10% repeat rate (2024)

- Targeted promo conversion: up to +20% (2024)

Discount retailer: 55 stores, +25% click-&-collect; CRM and promos curb buyer pressure

Puuilo’s discount positioning and commoditized SKUs give buyers high price sensitivity; 55 stores (2024) mean local price gaps shift volumes. Price transparency and click‑and‑collect adoption (+25% 2024) lower switching costs; SMEs (99.8% of firms) add bulk negotiating power. CRM and targeted promos (CRM lift 5–10%, promo conversion up to 20% 2024) mitigate buyer pressure.

| Metric | Value (2024) |

|---|---|

| Stores | 55 |

| Click‑&‑collect growth | +25% |

| SME share (Finland) | 99.8% |

| CRM repeat lift | 5–10% |

| Promo conversion lift | up to 20% |

Preview the Actual Deliverable

Puuilo Porter's Five Forces Analysis

This preview of the Puuilo Porter's Five Forces analysis is the exact document you’ll receive after purchase—no placeholders, no mockups. It contains the full competitive assessment of supplier and buyer power, threat of entrants and substitutes, and industry rivalry, professionally formatted and ready to download. Purchase grants instant access to this identical file for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Puuilo’s Porter’s Five Forces snapshot highlights key pressures — supplier leverage, buyer power, new entrant risk, substitute threats, and competitive rivalry — shaping its retail position. This brief overview teases strategic implications and operational vulnerabilities. Unlock the full Porter’s Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Puuilo.

Suppliers Bargaining Power

Fragmented suppliers

Many Puuilo product categories (DIY, pet, auto, garden) are sourced from numerous small and medium suppliers, diluting any single vendor’s leverage; across the EU 99.8% of firms are SMEs (Eurostat 2023), underscoring supplier fragmentation. Puuilo can benchmark prices and terms across alternatives, run tenders and maintain dual‑sourcing to drive down costs. Fragmentation enables rapid replacement of underperforming suppliers, improving supply resilience and margin control.

Private label scope

Expanding private-label lines shifts bargaining power toward Puuilo by cutting reliance on branded vendors and increasing margin capture through higher-margin own brands, while enhancing shelf control and product differentiation; however, rigorous quality assurance programs and managing minimum order quantity exposure are essential to mitigate reputational and inventory risks.

Import dependence

Global sourcing exposes Puuilo to FX, freight and lead-time pass-throughs — EUR/USD averaged ~1.09 in 2024 and Drewry WCI stayed elevated near USD 1,800/FEU, letting suppliers transfer costs. Long supply chains boost supplier power when capacity tightens, evidenced by sporadic 2024 port congestion and extended lead times. Hedging and multi-origin sourcing reduce FX/freight exposure, while nearshoring and seasonal buys demand agile, data-driven planning.

Logistics to Nordics

Serving a dispersed Finnish footprint (Finland population ~5.54 million, density ~18/km2 in 2024) gives logistics providers bargaining leverage; high per-km transport costs squeeze margins in Puuilo’s low-price model. Pooling volumes across categories and cross-docking measurably lower unit costs and reduce that leverage, while contracting multiple carriers cuts carrier-concentration risk.

- Dispersed footprint: raises leverage

- High transport cost: margin pressure

- Volume pooling/cross-dock: lowers leverage

- Multiple carriers: reduces concentration risk

Low switching costs

- Low switching costs limit supplier margins

- Framework agreements + KPIs drive consistency

- Niche/regulatory items retain supplier power

Low supplier power amid fragmented EU SME sourcing, offset by freight, FX and niche risks

Supplier power at Puuilo is generally low due to fragmented SME supplier base and standardised SKUs, strengthened by dual‑sourcing, tenders and private‑label expansion; exceptions exist for niche/regulatory SKUs. Global sourcing and freight/FX (EUR/USD ~1.09 in 2024; Drewry WCI ~1,800/FEU 2024) plus dispersed Finnish logistics raise supplier/carrier leverage.

| Metric | Value |

|---|---|

| EU SMEs (Eurostat) | 99.8% (2023) |

| Finland pop | 5.54M (2024) |

| EUR/USD | ~1.09 (2024) |

| Drewry WCI | ~1,800 USD/FEU (2024) |

What is included in the product

Provides a tailored Porter's Five Forces analysis for Puuilo, uncovering competitive intensity, buyer and supplier power, threat of substitutes and new entrants, and industry rivalry, with strategic insights on disruptive threats, pricing influence, and barriers that protect incumbents.

Clear one-sheet Puuilo Porter's Five Forces summary for rapid decision-making, with customizable pressure levels and an instant spider chart to visualize strategic threats and opportunities.

Customers Bargaining Power

Highly price-sensitive

Puuilo’s discount positioning draws value-focused shoppers who readily switch on price; with 55 stores in Finland as of 2024, small price gaps can redirect local volumes to rivals. Frequent promotions by Puuilo and peers have conditioned customers to expect deals, raising purchase elasticity. Commoditized SKUs amplify buyer power, making margins sensitive to even modest markdowns.

Easy comparisons

Online search and retailer flyers from Tokmanni, Biltema, Jula and others make prices highly transparent, and with click-and-collect adoption up ~25% in Nordic DIY channels in 2024 customers compare offers across chains in minutes. Low switching costs let shoppers split baskets between stores, while price-matching and basket-value tactics (loyalty thresholds, free-click-and-collect) are used to retain spend.

Mixed B2C/B2B

Tradespeople and microbusinesses buy recurrently and in bulk, giving them negotiating weight that drives discount requests and contract pricing. In Finland SMEs make up 99.8% of firms, creating meaningful B2B volume for mixed B2C/B2B retailers like Puuilo. Loyalty tiers and anchored contract prices lock relationships, while service reliability and deep stock reduce churn and strengthen customer stickiness.

Limited differentiation

- Low differentiation — price/convenience drivers

- Assortment breadth — reduces switching

- Seasonal depth — ties customers to store

- Add‑ons (rental, advice) — increase stickiness

Loyalty and data

Loyalty programs, targeted offers and CRM reduce effective buyer power by personalizing value; 2024 retail studies show CRM-driven targeting can lift repeat-purchase rates by 5–10% and targeted promotions raise conversion up to 20%. Data-driven pricing shields margins on inelastic SKUs while basket analytics steer promotions to traffic drivers, shifting focus from item price to total basket value.

- Loyalty penetration: member-driven sales concentration

- CRM lift: +5–10% repeat rate (2024)

- Targeted promo conversion: up to +20% (2024)

Discount retailer: 55 stores, +25% click-&-collect; CRM and promos curb buyer pressure

Puuilo’s discount positioning and commoditized SKUs give buyers high price sensitivity; 55 stores (2024) mean local price gaps shift volumes. Price transparency and click‑and‑collect adoption (+25% 2024) lower switching costs; SMEs (99.8% of firms) add bulk negotiating power. CRM and targeted promos (CRM lift 5–10%, promo conversion up to 20% 2024) mitigate buyer pressure.

| Metric | Value (2024) |

|---|---|

| Stores | 55 |

| Click‑&‑collect growth | +25% |

| SME share (Finland) | 99.8% |

| CRM repeat lift | 5–10% |

| Promo conversion lift | up to 20% |

Preview the Actual Deliverable

Puuilo Porter's Five Forces Analysis

This preview of the Puuilo Porter's Five Forces analysis is the exact document you’ll receive after purchase—no placeholders, no mockups. It contains the full competitive assessment of supplier and buyer power, threat of entrants and substitutes, and industry rivalry, professionally formatted and ready to download. Purchase grants instant access to this identical file for immediate use.