PZ Cussons PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political, economic and technological forces shape PZ Cussons' strategy and risks. Our concise PESTLE highlights regulatory, market and sustainability trends affecting growth. Ready-made and actionable, buy the full analysis for a complete, editable report you can use today.

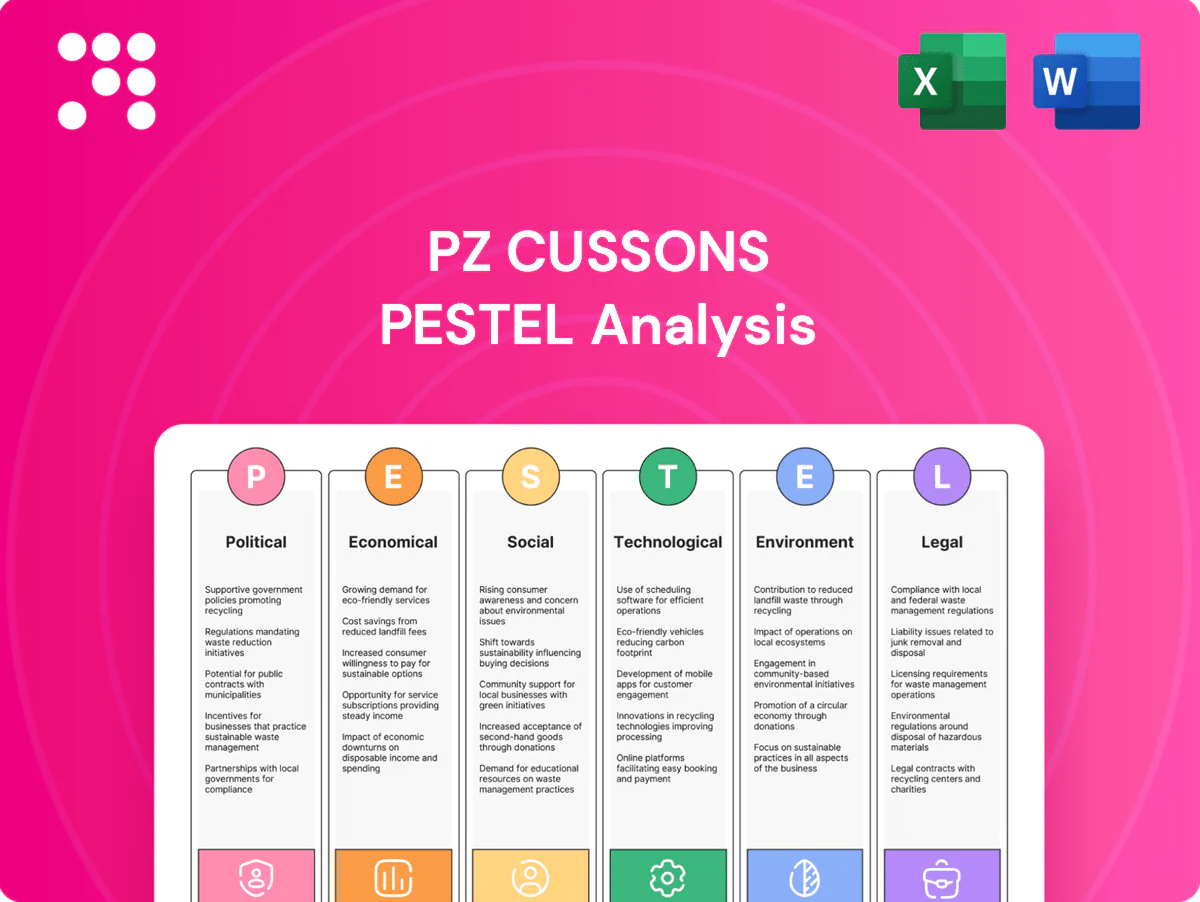

Political factors

Trade and tariffs

Shifts in import duties on chemicals, palm derivatives and packaging directly change landed costs; global palm oil production was about 77.8 million tonnes in 2023/24, underscoring supply concentration risk. Trade agreements or protectionist moves across Africa and Asia can rapidly reshape sourcing routes and input pricing. With the EU still ~45% of UK goods trade, stable UK–EU arrangements matter for compliance and logistics, so PZ Cussons must hedge against sudden tariff shocks in core markets.

FX and capital controls

Currency controls and repatriation limits in markets like Nigeria constrain cash conversion and pricing, with repatriation approvals often taking 60–120 days and local liquidity tight; Naira volatility—roughly a 40–50% depreciation versus the dollar between 2022–2024 across official and parallel rates—disrupts margin planning. Dual exchange rates and sudden devaluations compress gross margins by 10–30% in affected quarters, and restrictive dividend remittance rules pressure group treasury; active engagement with central banks and use of local financing lines can mitigate these risks.

Regulatory stability

Policy volatility around elections and reforms in key markets (Nigeria, Indonesia) can delay product approvals and distribution, with Nigeria’s 2024 inflation running about 22.7% tightening consumer purchasing power. Removal of subsidies and fiscal tightening typically cuts short-term demand; industrial policies increasingly incentivize local manufacturing via tariffs and incentives. Scenario planning keeps service levels steady amid shifts across PZ Cussons’ 20+ markets.

Health policy

Public health campaigns boost demand for soaps and sanitizers; WHO estimates handwashing can cut diarrhoeal disease by up to 50% and respiratory infections by ~20%, sustaining market pull for hygiene SKUs.

Regulatory standards for antimicrobial claims shape product positioning and labelling; emergency outbreak rules can trigger faster compliance checks and recalls.

Government partnerships help align formulations and distribution with national health priorities, improving uptake in public programmes.

- Campaign-driven demand: WHO health impact stats

- Compliance pressure: stricter antimicrobial claims

- Outbreak response: emergency rules tighten controls

- Partnerships: align products with national programmes

Localization mandates

Localization mandates in markets where PZ Cussons operates, notably Nigeria and Indonesia, raise input and staffing costs by requiring local content and hires but can be offset by sourcing from local suppliers to reduce import duties. Special economic zones and incentives in those jurisdictions can lower upfront capex through tax holidays and reduced tariffs. Political preference for domestic brands often improves shelf access and regulatory support. Maintaining global formulas while integrating approved local inputs preserves product quality and compliance.

- local-content: affects COGS via local sourcing

- sez-incentives: lower capex and tax burden

- political-support: eases market access for domestic brands

- quality-compliance: balance global formulas with local inputs

Tariff shifts, 77.8m t palm oil concentration, 40-50% Naira volatility squeeze margins

Political shifts in tariffs, trade and localisation drive input costs and market access; palm oil supply concentration (77.8m t in 2023/24) raises sourcing risk. Currency controls and Naira volatility (40–50% 2022–24) compress margins; Nigeria inflation ~22.7% (2024) weakens demand. Stable UK–EU ties (~45% of UK goods trade) matter for logistics and compliance.

| Metric | Value |

|---|---|

| Palm oil production (2023/24) | 77.8m t |

| Nigeria inflation (2024) | 22.7% |

| Naira depreciation (2022–24) | 40–50% |

| UK–EU goods trade | ~45% |

What is included in the product

Explores how external macro-environmental factors uniquely affect PZ Cussons across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal. Each section is data-backed with current trends and forward-looking insights to help executives, consultants, and investors identify risks and opportunities and support strategy, scenario planning, and funding decisions.

A concise, PESTLE-segmented summary of PZ Cussons' external risks and opportunities for quick inclusion in presentations or strategy sessions; editable notes let teams localize insights by region or product line.

Economic factors

Inflation pressure

High inflation in key markets — Nigeria >30% in 2024 and UK around 4% in 2024 — erodes consumer purchasing power and shifts demand to lower-priced SKUs.

Spikes in input costs for oils, surfactants and freight (palm oil and commodity oils up c.15% YoY in 2024; freight above pre‑pandemic levels) compress margins.

Price‑pack architecture and value SKUs help defend volumes, while active revenue management is critical to protect mix and market share.

FX volatility

Depreciating local currencies (for example the Nigerian naira, which weakened c.20% vs major currencies through 2023–24) push up imported input costs versus PZ Cussons’ locally priced products, squeezing margins.

Currency translation can materially alter reported GBP results, with FX swings regularly moving quarterly reported revenue and operating profit by multiple percentage points.

Hedging programmes, increasing local sourcing and natural offsets across categories, together with frequent RRP reviews (typically quarterly), help keep affordability and FX exposure under control.

Commodity cycles

Palm oil, oleochemical derivatives and packaging plastics follow global commodity cycles; Bursa Malaysia palm oil futures rose about 20% in 2023–24, pressuring COGS for personal-care producers like PZ Cussons.

Sudden spikes force agile reformulation, SKU downsizing or pack‑size shifts to protect margins and price positioning in emerging markets.

Long‑term supplier contracts and index‑linked clauses smooth volatility, while monitoring 3‑ to 12‑month futures curves supports rolling cost forecasts and hedging decisions.

Emerging market growth

Rising populations and urbanization in Africa (≈1.4bn population, urban share ~44% in 2024) and Asia expand PZ Cussons addressable demand; IMF forecasts 2024 GDP growth ~3.5% for Sub-Saharan Africa and ~5% for emerging Asia, supporting premiumization in personal care. Formal retail and e-commerce penetration are increasing, but channel strategy must balance modern trade and traditional outlets.

- Addressable market: Africa ≈1.4bn (2024)

- Urbanization: ~44% (2024)

- GDP growth: SSA ~3.5%, emerging Asia ~5% (2024)

- Retail: rising formal/e‑commerce penetration—dual channel focus required

Consumer downtrading

Macro slowdowns push UK shoppers toward smaller packs and value brands, prompting PZ Cussons to lean on its balance of premium and value SKUs to protect share; private label pressure rose, with Kantar reporting private label at about 48% of UK grocery in 2024. Promotional efficiency and ROI tracking are used to prevent margin dilution.

- Smaller packs

- Value brands

- Private label ~48% (Kantar 2024)

- ROI on promotions

Tariff shifts, 77.8m t palm oil concentration, 40-50% Naira volatility squeeze margins

High inflation (Nigeria >30% 2024; UK ~4% 2024), commodity cost rises and a ~20% naira depreciation have compressed margins, forcing SKU down‑trading and price‑pack shifts. Hedging, local sourcing and frequent RRP reviews mitigate FX and input shocks while urbanization and ~3.5% SSA / ~5% emerging Asia GDP support volume growth and premiumization.

| Metric | Value (2024) |

|---|---|

| Nigeria inflation | >30% |

| UK inflation | ~4% |

| Palm oil | +20% (2023–24) |

| Naira vs majors | -~20% |

| SSA GDP | ~3.5% |

| Emerging Asia GDP | ~5% |

| UK private label | ~48% |

Same Document Delivered

PZ Cussons PESTLE Analysis

The preview shown here is the exact PZ Cussons PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are identical to the downloadable file, with no placeholders or teasers. After payment you’ll instantly get this final, professionally structured document.

Skip the Research. Get the Strategy.

Discover how political, economic and technological forces shape PZ Cussons' strategy and risks. Our concise PESTLE highlights regulatory, market and sustainability trends affecting growth. Ready-made and actionable, buy the full analysis for a complete, editable report you can use today.

Political factors

Trade and tariffs

Shifts in import duties on chemicals, palm derivatives and packaging directly change landed costs; global palm oil production was about 77.8 million tonnes in 2023/24, underscoring supply concentration risk. Trade agreements or protectionist moves across Africa and Asia can rapidly reshape sourcing routes and input pricing. With the EU still ~45% of UK goods trade, stable UK–EU arrangements matter for compliance and logistics, so PZ Cussons must hedge against sudden tariff shocks in core markets.

FX and capital controls

Currency controls and repatriation limits in markets like Nigeria constrain cash conversion and pricing, with repatriation approvals often taking 60–120 days and local liquidity tight; Naira volatility—roughly a 40–50% depreciation versus the dollar between 2022–2024 across official and parallel rates—disrupts margin planning. Dual exchange rates and sudden devaluations compress gross margins by 10–30% in affected quarters, and restrictive dividend remittance rules pressure group treasury; active engagement with central banks and use of local financing lines can mitigate these risks.

Regulatory stability

Policy volatility around elections and reforms in key markets (Nigeria, Indonesia) can delay product approvals and distribution, with Nigeria’s 2024 inflation running about 22.7% tightening consumer purchasing power. Removal of subsidies and fiscal tightening typically cuts short-term demand; industrial policies increasingly incentivize local manufacturing via tariffs and incentives. Scenario planning keeps service levels steady amid shifts across PZ Cussons’ 20+ markets.

Health policy

Public health campaigns boost demand for soaps and sanitizers; WHO estimates handwashing can cut diarrhoeal disease by up to 50% and respiratory infections by ~20%, sustaining market pull for hygiene SKUs.

Regulatory standards for antimicrobial claims shape product positioning and labelling; emergency outbreak rules can trigger faster compliance checks and recalls.

Government partnerships help align formulations and distribution with national health priorities, improving uptake in public programmes.

- Campaign-driven demand: WHO health impact stats

- Compliance pressure: stricter antimicrobial claims

- Outbreak response: emergency rules tighten controls

- Partnerships: align products with national programmes

Localization mandates

Localization mandates in markets where PZ Cussons operates, notably Nigeria and Indonesia, raise input and staffing costs by requiring local content and hires but can be offset by sourcing from local suppliers to reduce import duties. Special economic zones and incentives in those jurisdictions can lower upfront capex through tax holidays and reduced tariffs. Political preference for domestic brands often improves shelf access and regulatory support. Maintaining global formulas while integrating approved local inputs preserves product quality and compliance.

- local-content: affects COGS via local sourcing

- sez-incentives: lower capex and tax burden

- political-support: eases market access for domestic brands

- quality-compliance: balance global formulas with local inputs

Tariff shifts, 77.8m t palm oil concentration, 40-50% Naira volatility squeeze margins

Political shifts in tariffs, trade and localisation drive input costs and market access; palm oil supply concentration (77.8m t in 2023/24) raises sourcing risk. Currency controls and Naira volatility (40–50% 2022–24) compress margins; Nigeria inflation ~22.7% (2024) weakens demand. Stable UK–EU ties (~45% of UK goods trade) matter for logistics and compliance.

| Metric | Value |

|---|---|

| Palm oil production (2023/24) | 77.8m t |

| Nigeria inflation (2024) | 22.7% |

| Naira depreciation (2022–24) | 40–50% |

| UK–EU goods trade | ~45% |

What is included in the product

Explores how external macro-environmental factors uniquely affect PZ Cussons across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal. Each section is data-backed with current trends and forward-looking insights to help executives, consultants, and investors identify risks and opportunities and support strategy, scenario planning, and funding decisions.

A concise, PESTLE-segmented summary of PZ Cussons' external risks and opportunities for quick inclusion in presentations or strategy sessions; editable notes let teams localize insights by region or product line.

Economic factors

Inflation pressure

High inflation in key markets — Nigeria >30% in 2024 and UK around 4% in 2024 — erodes consumer purchasing power and shifts demand to lower-priced SKUs.

Spikes in input costs for oils, surfactants and freight (palm oil and commodity oils up c.15% YoY in 2024; freight above pre‑pandemic levels) compress margins.

Price‑pack architecture and value SKUs help defend volumes, while active revenue management is critical to protect mix and market share.

FX volatility

Depreciating local currencies (for example the Nigerian naira, which weakened c.20% vs major currencies through 2023–24) push up imported input costs versus PZ Cussons’ locally priced products, squeezing margins.

Currency translation can materially alter reported GBP results, with FX swings regularly moving quarterly reported revenue and operating profit by multiple percentage points.

Hedging programmes, increasing local sourcing and natural offsets across categories, together with frequent RRP reviews (typically quarterly), help keep affordability and FX exposure under control.

Commodity cycles

Palm oil, oleochemical derivatives and packaging plastics follow global commodity cycles; Bursa Malaysia palm oil futures rose about 20% in 2023–24, pressuring COGS for personal-care producers like PZ Cussons.

Sudden spikes force agile reformulation, SKU downsizing or pack‑size shifts to protect margins and price positioning in emerging markets.

Long‑term supplier contracts and index‑linked clauses smooth volatility, while monitoring 3‑ to 12‑month futures curves supports rolling cost forecasts and hedging decisions.

Emerging market growth

Rising populations and urbanization in Africa (≈1.4bn population, urban share ~44% in 2024) and Asia expand PZ Cussons addressable demand; IMF forecasts 2024 GDP growth ~3.5% for Sub-Saharan Africa and ~5% for emerging Asia, supporting premiumization in personal care. Formal retail and e-commerce penetration are increasing, but channel strategy must balance modern trade and traditional outlets.

- Addressable market: Africa ≈1.4bn (2024)

- Urbanization: ~44% (2024)

- GDP growth: SSA ~3.5%, emerging Asia ~5% (2024)

- Retail: rising formal/e‑commerce penetration—dual channel focus required

Consumer downtrading

Macro slowdowns push UK shoppers toward smaller packs and value brands, prompting PZ Cussons to lean on its balance of premium and value SKUs to protect share; private label pressure rose, with Kantar reporting private label at about 48% of UK grocery in 2024. Promotional efficiency and ROI tracking are used to prevent margin dilution.

- Smaller packs

- Value brands

- Private label ~48% (Kantar 2024)

- ROI on promotions

Tariff shifts, 77.8m t palm oil concentration, 40-50% Naira volatility squeeze margins

High inflation (Nigeria >30% 2024; UK ~4% 2024), commodity cost rises and a ~20% naira depreciation have compressed margins, forcing SKU down‑trading and price‑pack shifts. Hedging, local sourcing and frequent RRP reviews mitigate FX and input shocks while urbanization and ~3.5% SSA / ~5% emerging Asia GDP support volume growth and premiumization.

| Metric | Value (2024) |

|---|---|

| Nigeria inflation | >30% |

| UK inflation | ~4% |

| Palm oil | +20% (2023–24) |

| Naira vs majors | -~20% |

| SSA GDP | ~3.5% |

| Emerging Asia GDP | ~5% |

| UK private label | ~48% |

Same Document Delivered

PZ Cussons PESTLE Analysis

The preview shown here is the exact PZ Cussons PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are identical to the downloadable file, with no placeholders or teasers. After payment you’ll instantly get this final, professionally structured document.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Discover how political, economic and technological forces shape PZ Cussons' strategy and risks. Our concise PESTLE highlights regulatory, market and sustainability trends affecting growth. Ready-made and actionable, buy the full analysis for a complete, editable report you can use today.

Political factors

Trade and tariffs

Shifts in import duties on chemicals, palm derivatives and packaging directly change landed costs; global palm oil production was about 77.8 million tonnes in 2023/24, underscoring supply concentration risk. Trade agreements or protectionist moves across Africa and Asia can rapidly reshape sourcing routes and input pricing. With the EU still ~45% of UK goods trade, stable UK–EU arrangements matter for compliance and logistics, so PZ Cussons must hedge against sudden tariff shocks in core markets.

FX and capital controls

Currency controls and repatriation limits in markets like Nigeria constrain cash conversion and pricing, with repatriation approvals often taking 60–120 days and local liquidity tight; Naira volatility—roughly a 40–50% depreciation versus the dollar between 2022–2024 across official and parallel rates—disrupts margin planning. Dual exchange rates and sudden devaluations compress gross margins by 10–30% in affected quarters, and restrictive dividend remittance rules pressure group treasury; active engagement with central banks and use of local financing lines can mitigate these risks.

Regulatory stability

Policy volatility around elections and reforms in key markets (Nigeria, Indonesia) can delay product approvals and distribution, with Nigeria’s 2024 inflation running about 22.7% tightening consumer purchasing power. Removal of subsidies and fiscal tightening typically cuts short-term demand; industrial policies increasingly incentivize local manufacturing via tariffs and incentives. Scenario planning keeps service levels steady amid shifts across PZ Cussons’ 20+ markets.

Health policy

Public health campaigns boost demand for soaps and sanitizers; WHO estimates handwashing can cut diarrhoeal disease by up to 50% and respiratory infections by ~20%, sustaining market pull for hygiene SKUs.

Regulatory standards for antimicrobial claims shape product positioning and labelling; emergency outbreak rules can trigger faster compliance checks and recalls.

Government partnerships help align formulations and distribution with national health priorities, improving uptake in public programmes.

- Campaign-driven demand: WHO health impact stats

- Compliance pressure: stricter antimicrobial claims

- Outbreak response: emergency rules tighten controls

- Partnerships: align products with national programmes

Localization mandates

Localization mandates in markets where PZ Cussons operates, notably Nigeria and Indonesia, raise input and staffing costs by requiring local content and hires but can be offset by sourcing from local suppliers to reduce import duties. Special economic zones and incentives in those jurisdictions can lower upfront capex through tax holidays and reduced tariffs. Political preference for domestic brands often improves shelf access and regulatory support. Maintaining global formulas while integrating approved local inputs preserves product quality and compliance.

- local-content: affects COGS via local sourcing

- sez-incentives: lower capex and tax burden

- political-support: eases market access for domestic brands

- quality-compliance: balance global formulas with local inputs

Tariff shifts, 77.8m t palm oil concentration, 40-50% Naira volatility squeeze margins

Political shifts in tariffs, trade and localisation drive input costs and market access; palm oil supply concentration (77.8m t in 2023/24) raises sourcing risk. Currency controls and Naira volatility (40–50% 2022–24) compress margins; Nigeria inflation ~22.7% (2024) weakens demand. Stable UK–EU ties (~45% of UK goods trade) matter for logistics and compliance.

| Metric | Value |

|---|---|

| Palm oil production (2023/24) | 77.8m t |

| Nigeria inflation (2024) | 22.7% |

| Naira depreciation (2022–24) | 40–50% |

| UK–EU goods trade | ~45% |

What is included in the product

Explores how external macro-environmental factors uniquely affect PZ Cussons across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal. Each section is data-backed with current trends and forward-looking insights to help executives, consultants, and investors identify risks and opportunities and support strategy, scenario planning, and funding decisions.

A concise, PESTLE-segmented summary of PZ Cussons' external risks and opportunities for quick inclusion in presentations or strategy sessions; editable notes let teams localize insights by region or product line.

Economic factors

Inflation pressure

High inflation in key markets — Nigeria >30% in 2024 and UK around 4% in 2024 — erodes consumer purchasing power and shifts demand to lower-priced SKUs.

Spikes in input costs for oils, surfactants and freight (palm oil and commodity oils up c.15% YoY in 2024; freight above pre‑pandemic levels) compress margins.

Price‑pack architecture and value SKUs help defend volumes, while active revenue management is critical to protect mix and market share.

FX volatility

Depreciating local currencies (for example the Nigerian naira, which weakened c.20% vs major currencies through 2023–24) push up imported input costs versus PZ Cussons’ locally priced products, squeezing margins.

Currency translation can materially alter reported GBP results, with FX swings regularly moving quarterly reported revenue and operating profit by multiple percentage points.

Hedging programmes, increasing local sourcing and natural offsets across categories, together with frequent RRP reviews (typically quarterly), help keep affordability and FX exposure under control.

Commodity cycles

Palm oil, oleochemical derivatives and packaging plastics follow global commodity cycles; Bursa Malaysia palm oil futures rose about 20% in 2023–24, pressuring COGS for personal-care producers like PZ Cussons.

Sudden spikes force agile reformulation, SKU downsizing or pack‑size shifts to protect margins and price positioning in emerging markets.

Long‑term supplier contracts and index‑linked clauses smooth volatility, while monitoring 3‑ to 12‑month futures curves supports rolling cost forecasts and hedging decisions.

Emerging market growth

Rising populations and urbanization in Africa (≈1.4bn population, urban share ~44% in 2024) and Asia expand PZ Cussons addressable demand; IMF forecasts 2024 GDP growth ~3.5% for Sub-Saharan Africa and ~5% for emerging Asia, supporting premiumization in personal care. Formal retail and e-commerce penetration are increasing, but channel strategy must balance modern trade and traditional outlets.

- Addressable market: Africa ≈1.4bn (2024)

- Urbanization: ~44% (2024)

- GDP growth: SSA ~3.5%, emerging Asia ~5% (2024)

- Retail: rising formal/e‑commerce penetration—dual channel focus required

Consumer downtrading

Macro slowdowns push UK shoppers toward smaller packs and value brands, prompting PZ Cussons to lean on its balance of premium and value SKUs to protect share; private label pressure rose, with Kantar reporting private label at about 48% of UK grocery in 2024. Promotional efficiency and ROI tracking are used to prevent margin dilution.

- Smaller packs

- Value brands

- Private label ~48% (Kantar 2024)

- ROI on promotions

Tariff shifts, 77.8m t palm oil concentration, 40-50% Naira volatility squeeze margins

High inflation (Nigeria >30% 2024; UK ~4% 2024), commodity cost rises and a ~20% naira depreciation have compressed margins, forcing SKU down‑trading and price‑pack shifts. Hedging, local sourcing and frequent RRP reviews mitigate FX and input shocks while urbanization and ~3.5% SSA / ~5% emerging Asia GDP support volume growth and premiumization.

| Metric | Value (2024) |

|---|---|

| Nigeria inflation | >30% |

| UK inflation | ~4% |

| Palm oil | +20% (2023–24) |

| Naira vs majors | -~20% |

| SSA GDP | ~3.5% |

| Emerging Asia GDP | ~5% |

| UK private label | ~48% |

Same Document Delivered

PZ Cussons PESTLE Analysis

The preview shown here is the exact PZ Cussons PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are identical to the downloadable file, with no placeholders or teasers. After payment you’ll instantly get this final, professionally structured document.