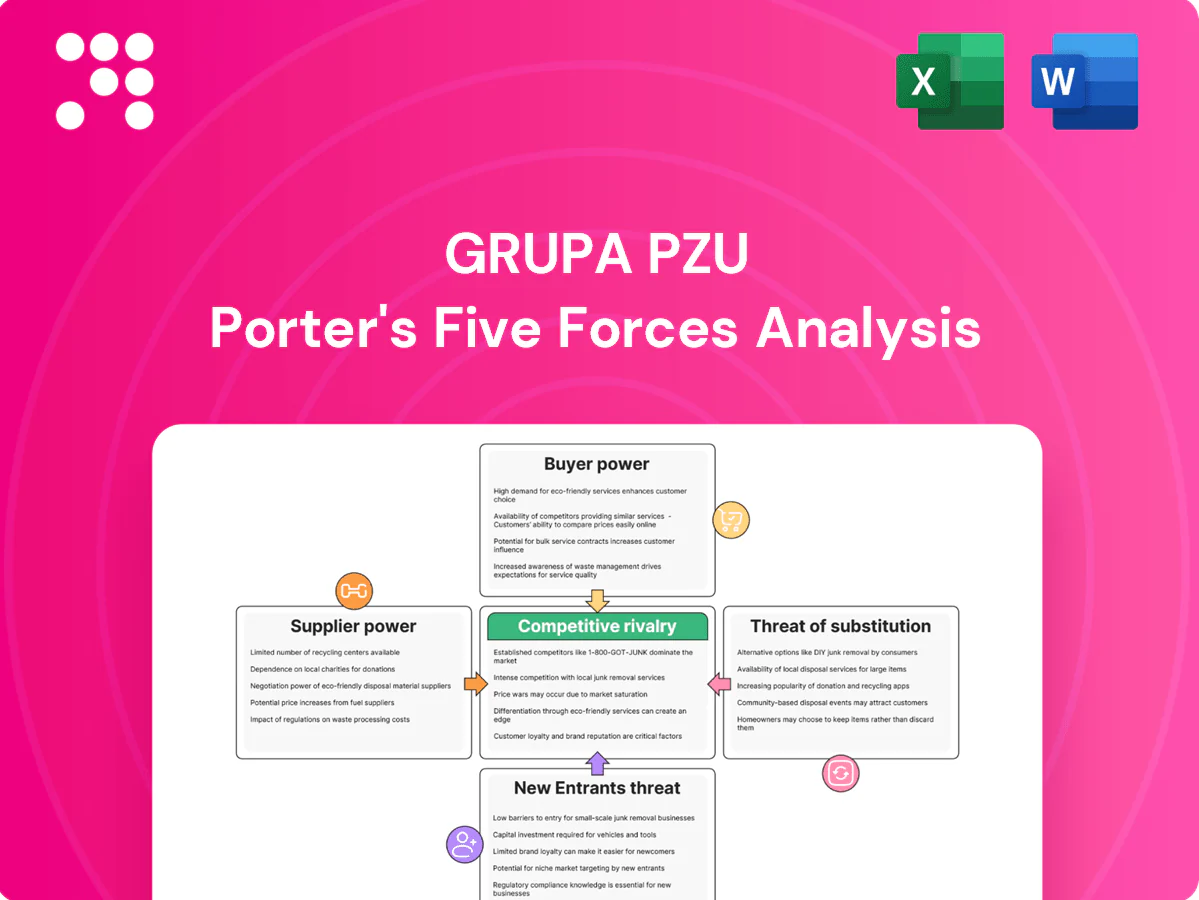

Grupa PZU Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Grupa PZU faces moderate buyer power, concentrated supplier partners, regulatory pressure, limited substitutes, and high rivalry—shaping its underwriting margins and growth prospects. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupa PZU’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Reinsurers hold selective leverage

Catastrophe and large-risk covers depend on a concentrated global reinsurance pool, giving top reinsurers notable pricing power; PZU’s scale and long-standing relationships (Poland market share ~35% in 2024) mitigate but do not remove renewal pressure in hard markets. Growth of alternative capital—ILS capital exceeded USD100bn in 2024—diversifies sources, yet tighter capacity cycles can quickly raise cession costs and tighten terms.

Specialized data and IT vendors matter

Core systems, fraud analytics and telematics providers are relatively concentrated, raising switching costs and enabling vendor lock-in that can push up prices and slow upgrade cadence. As Poland’s largest insurer, PZU (≈30% market share) can blunt this by dual-sourcing and building in-house capabilities. Increasing cybersecurity and cloud compliance requirements further amplify dependence on specialized vendors.

Healthcare networks as critical inputs

Private clinics and diagnostics networks determine service costs and access for health products, especially in outpatient care. In urban centres leading providers and large chains hold strong bargaining clout. PZU, Poland's largest insurer with roughly 30% market share in 2024, uses PZU Zdrowie and other assets to integrate care and strengthen negotiating position, though local capacity constraints can still tighten terms.

Capital and talent as strategic suppliers

Financial markets supplied regulatory capital and investment yield as Poland's 10‑year government bond averaged about 5% in 2024, compressing underwriting margins when rate cycles turned; market volatility and wage inflation pushed input costs higher. Scarce actuarial, data‑science and risk talent command premiums; PZU’s strong brand and scale ease capital access and recruitment.

- Regulatory capital: higher yields in 2024 (~5% 10y)

- Talent scarcity: premium wages for actuaries/data scientists

- Brand advantage: easier capital & hiring

- Cost pressures: market volatility + wage inflation

Intermediaries shape acquisition costs

Brokers and bancassurance partners act as gatekeepers for PZU’s corporate and retail flows; top channels can demand higher commissions or exclusivity, pressuring acquisition costs. PZU’s multi-channel reach and c.16 million clients and ~30% Polish market share in 2024 reduce single-counterparty dependence. Growth in digital direct sales in 2024 has rebalanced negotiating power toward PZU.

- Brokers/bancassurance: gatekeepers

- Top channels: higher commissions/exclusivity

- Multi-channel + c.16M clients, ~30% market share (2024)

- Digital direct growth shifts power to PZU

Reinsurance concentration boosts reinsurer pricing power; large insurer share cushions renewals

Reinsurance concentration gives top reinsurers strong pricing power; PZU’s scale and ~30–35% Poland market share in 2024 cushions renewals but does not eliminate cost pressure. Alternative capital (ILS > USD100bn in 2024) eases dependence but amplifies volatility in capacity cycles. Vendor concentration (core systems, telematics, clinics) raises switching costs and premium input risk.

| Metric | 2024 |

|---|---|

| PZU Poland market share | ~30–35% |

| ILS capital | >USD100bn |

| 10y gov yield (PL) | ~5% |

| Customer base | ~16M |

What is included in the product

Uncovers competitive drivers, customer influence, entry risks, substitutes, and supplier/buyer power specific to Grupa PZU, with strategic commentary on regulatory and disruptive threats; evaluates market dynamics that protect incumbents and pressure margins.

Clear, one-sheet Porter's Five Forces for Grupa PZU—instantly shows competitive, supplier, buyer, entrant and substitute pressures to speed strategic decisions and risk mitigation.

Customers Bargaining Power

Price-sensitive retail customers

Price-sensitive retail customers treat motor and simple P&C as commodities, frequently comparing offers; aggregators in Poland handle over half of online insurance quotes, raising transparency and customer bargaining power. PZU, with roughly 30% non-life market share, counters through bundling, loyalty programs and strong brand trust, yet policy switching at renewal remains common, especially in motor segments.

Corporate and SME buyers negotiate hard

Corporate and SME buyers run competitive tenders and use brokers to press pricing and terms, with brokers involved in over 60% of large tenders (2024). Customized coverages increase negotiation intensity, often driving bespoke pricing and exclusions. PZU’s underwriting depth and capital capacity, backed by a market share over 25% in Poland (2024), help defend margins. Service SLAs and risk engineering differentiate beyond price.

Brokers and aggregators amplify buyer clout

Brokers and aggregators consolidate demand and benchmark offers, steering volume toward the best economics for clients; in 2024 Grupa PZU, with roughly 33% market share in Poland, must win both commission and proposition to retain flow. Data-driven pricing and rapid quoting—used by leading aggregators—reduce leakage and force PZU to tighten turnaround and margin management.

Healthcare group plans expect access

Employers buying medical cover prioritize network breadth and short wait times; dissatisfaction can trigger swift switching given employers' bargaining leverage. PZU, as Poland's largest insurer with ≈30% market share in 2024, uses an integrated provider network and partnerships to mitigate churn. Service quality and access directly drive perceived value and retention.

- Employers: network breadth, wait times

- Switching risk: high if service lags

- PZU 2024: ≈30% market share mitigates churn

- Service quality = perceived value

Investment clients demand performance

- Reallocation risk: low-fee ETFs

- Fee pressure: persistent in 2024

- Must offer alpha or passive clarity

- Decisive: transparent reporting & risk controls

Aggregators >50% quotes, brokers >60% tenders; leading insurer ≈30%, ETFs ≈12tn USD squeeze fees

Retail buyers treat motor/P&C as commodities; aggregators handle >50% online quotes, boosting price pressure, while PZU holds ≈30% non‑life market share (2024). Corporates use brokers in >60% large tenders (2024), squeezing terms; PZU leverages underwriting depth and SLAs to defend margins. Investment clients shift to low‑fee ETFs (global AUM ≈12tn USD, 2024), increasing fee pressure on PZU TFI.

| Segment | 2024 metric | PZU position |

|---|---|---|

| Retail | Aggregators >50% quotes | ~30% market share |

| Corporate | Brokers >60% large tenders | Underwriting/SLAs |

| Investments | ETF AUM ≈12tn USD | Fee pressure |

Preview the Actual Deliverable

Grupa PZU Porter's Five Forces Analysis

This preview shows the exact Grupa PZU Porter’s Five Forces analysis you’ll receive—fully developed, professionally formatted, and ready for immediate use. No samples or placeholders: the file available after purchase is identical to this view. Instant download upon payment, suitable for decision-making and reporting.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Grupa PZU faces moderate buyer power, concentrated supplier partners, regulatory pressure, limited substitutes, and high rivalry—shaping its underwriting margins and growth prospects. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupa PZU’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Reinsurers hold selective leverage

Catastrophe and large-risk covers depend on a concentrated global reinsurance pool, giving top reinsurers notable pricing power; PZU’s scale and long-standing relationships (Poland market share ~35% in 2024) mitigate but do not remove renewal pressure in hard markets. Growth of alternative capital—ILS capital exceeded USD100bn in 2024—diversifies sources, yet tighter capacity cycles can quickly raise cession costs and tighten terms.

Specialized data and IT vendors matter

Core systems, fraud analytics and telematics providers are relatively concentrated, raising switching costs and enabling vendor lock-in that can push up prices and slow upgrade cadence. As Poland’s largest insurer, PZU (≈30% market share) can blunt this by dual-sourcing and building in-house capabilities. Increasing cybersecurity and cloud compliance requirements further amplify dependence on specialized vendors.

Healthcare networks as critical inputs

Private clinics and diagnostics networks determine service costs and access for health products, especially in outpatient care. In urban centres leading providers and large chains hold strong bargaining clout. PZU, Poland's largest insurer with roughly 30% market share in 2024, uses PZU Zdrowie and other assets to integrate care and strengthen negotiating position, though local capacity constraints can still tighten terms.

Capital and talent as strategic suppliers

Financial markets supplied regulatory capital and investment yield as Poland's 10‑year government bond averaged about 5% in 2024, compressing underwriting margins when rate cycles turned; market volatility and wage inflation pushed input costs higher. Scarce actuarial, data‑science and risk talent command premiums; PZU’s strong brand and scale ease capital access and recruitment.

- Regulatory capital: higher yields in 2024 (~5% 10y)

- Talent scarcity: premium wages for actuaries/data scientists

- Brand advantage: easier capital & hiring

- Cost pressures: market volatility + wage inflation

Intermediaries shape acquisition costs

Brokers and bancassurance partners act as gatekeepers for PZU’s corporate and retail flows; top channels can demand higher commissions or exclusivity, pressuring acquisition costs. PZU’s multi-channel reach and c.16 million clients and ~30% Polish market share in 2024 reduce single-counterparty dependence. Growth in digital direct sales in 2024 has rebalanced negotiating power toward PZU.

- Brokers/bancassurance: gatekeepers

- Top channels: higher commissions/exclusivity

- Multi-channel + c.16M clients, ~30% market share (2024)

- Digital direct growth shifts power to PZU

Reinsurance concentration boosts reinsurer pricing power; large insurer share cushions renewals

Reinsurance concentration gives top reinsurers strong pricing power; PZU’s scale and ~30–35% Poland market share in 2024 cushions renewals but does not eliminate cost pressure. Alternative capital (ILS > USD100bn in 2024) eases dependence but amplifies volatility in capacity cycles. Vendor concentration (core systems, telematics, clinics) raises switching costs and premium input risk.

| Metric | 2024 |

|---|---|

| PZU Poland market share | ~30–35% |

| ILS capital | >USD100bn |

| 10y gov yield (PL) | ~5% |

| Customer base | ~16M |

What is included in the product

Uncovers competitive drivers, customer influence, entry risks, substitutes, and supplier/buyer power specific to Grupa PZU, with strategic commentary on regulatory and disruptive threats; evaluates market dynamics that protect incumbents and pressure margins.

Clear, one-sheet Porter's Five Forces for Grupa PZU—instantly shows competitive, supplier, buyer, entrant and substitute pressures to speed strategic decisions and risk mitigation.

Customers Bargaining Power

Price-sensitive retail customers

Price-sensitive retail customers treat motor and simple P&C as commodities, frequently comparing offers; aggregators in Poland handle over half of online insurance quotes, raising transparency and customer bargaining power. PZU, with roughly 30% non-life market share, counters through bundling, loyalty programs and strong brand trust, yet policy switching at renewal remains common, especially in motor segments.

Corporate and SME buyers negotiate hard

Corporate and SME buyers run competitive tenders and use brokers to press pricing and terms, with brokers involved in over 60% of large tenders (2024). Customized coverages increase negotiation intensity, often driving bespoke pricing and exclusions. PZU’s underwriting depth and capital capacity, backed by a market share over 25% in Poland (2024), help defend margins. Service SLAs and risk engineering differentiate beyond price.

Brokers and aggregators amplify buyer clout

Brokers and aggregators consolidate demand and benchmark offers, steering volume toward the best economics for clients; in 2024 Grupa PZU, with roughly 33% market share in Poland, must win both commission and proposition to retain flow. Data-driven pricing and rapid quoting—used by leading aggregators—reduce leakage and force PZU to tighten turnaround and margin management.

Healthcare group plans expect access

Employers buying medical cover prioritize network breadth and short wait times; dissatisfaction can trigger swift switching given employers' bargaining leverage. PZU, as Poland's largest insurer with ≈30% market share in 2024, uses an integrated provider network and partnerships to mitigate churn. Service quality and access directly drive perceived value and retention.

- Employers: network breadth, wait times

- Switching risk: high if service lags

- PZU 2024: ≈30% market share mitigates churn

- Service quality = perceived value

Investment clients demand performance

- Reallocation risk: low-fee ETFs

- Fee pressure: persistent in 2024

- Must offer alpha or passive clarity

- Decisive: transparent reporting & risk controls

Aggregators >50% quotes, brokers >60% tenders; leading insurer ≈30%, ETFs ≈12tn USD squeeze fees

Retail buyers treat motor/P&C as commodities; aggregators handle >50% online quotes, boosting price pressure, while PZU holds ≈30% non‑life market share (2024). Corporates use brokers in >60% large tenders (2024), squeezing terms; PZU leverages underwriting depth and SLAs to defend margins. Investment clients shift to low‑fee ETFs (global AUM ≈12tn USD, 2024), increasing fee pressure on PZU TFI.

| Segment | 2024 metric | PZU position |

|---|---|---|

| Retail | Aggregators >50% quotes | ~30% market share |

| Corporate | Brokers >60% large tenders | Underwriting/SLAs |

| Investments | ETF AUM ≈12tn USD | Fee pressure |

Preview the Actual Deliverable

Grupa PZU Porter's Five Forces Analysis

This preview shows the exact Grupa PZU Porter’s Five Forces analysis you’ll receive—fully developed, professionally formatted, and ready for immediate use. No samples or placeholders: the file available after purchase is identical to this view. Instant download upon payment, suitable for decision-making and reporting.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Grupa PZU faces moderate buyer power, concentrated supplier partners, regulatory pressure, limited substitutes, and high rivalry—shaping its underwriting margins and growth prospects. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupa PZU’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Reinsurers hold selective leverage

Catastrophe and large-risk covers depend on a concentrated global reinsurance pool, giving top reinsurers notable pricing power; PZU’s scale and long-standing relationships (Poland market share ~35% in 2024) mitigate but do not remove renewal pressure in hard markets. Growth of alternative capital—ILS capital exceeded USD100bn in 2024—diversifies sources, yet tighter capacity cycles can quickly raise cession costs and tighten terms.

Specialized data and IT vendors matter

Core systems, fraud analytics and telematics providers are relatively concentrated, raising switching costs and enabling vendor lock-in that can push up prices and slow upgrade cadence. As Poland’s largest insurer, PZU (≈30% market share) can blunt this by dual-sourcing and building in-house capabilities. Increasing cybersecurity and cloud compliance requirements further amplify dependence on specialized vendors.

Healthcare networks as critical inputs

Private clinics and diagnostics networks determine service costs and access for health products, especially in outpatient care. In urban centres leading providers and large chains hold strong bargaining clout. PZU, Poland's largest insurer with roughly 30% market share in 2024, uses PZU Zdrowie and other assets to integrate care and strengthen negotiating position, though local capacity constraints can still tighten terms.

Capital and talent as strategic suppliers

Financial markets supplied regulatory capital and investment yield as Poland's 10‑year government bond averaged about 5% in 2024, compressing underwriting margins when rate cycles turned; market volatility and wage inflation pushed input costs higher. Scarce actuarial, data‑science and risk talent command premiums; PZU’s strong brand and scale ease capital access and recruitment.

- Regulatory capital: higher yields in 2024 (~5% 10y)

- Talent scarcity: premium wages for actuaries/data scientists

- Brand advantage: easier capital & hiring

- Cost pressures: market volatility + wage inflation

Intermediaries shape acquisition costs

Brokers and bancassurance partners act as gatekeepers for PZU’s corporate and retail flows; top channels can demand higher commissions or exclusivity, pressuring acquisition costs. PZU’s multi-channel reach and c.16 million clients and ~30% Polish market share in 2024 reduce single-counterparty dependence. Growth in digital direct sales in 2024 has rebalanced negotiating power toward PZU.

- Brokers/bancassurance: gatekeepers

- Top channels: higher commissions/exclusivity

- Multi-channel + c.16M clients, ~30% market share (2024)

- Digital direct growth shifts power to PZU

Reinsurance concentration boosts reinsurer pricing power; large insurer share cushions renewals

Reinsurance concentration gives top reinsurers strong pricing power; PZU’s scale and ~30–35% Poland market share in 2024 cushions renewals but does not eliminate cost pressure. Alternative capital (ILS > USD100bn in 2024) eases dependence but amplifies volatility in capacity cycles. Vendor concentration (core systems, telematics, clinics) raises switching costs and premium input risk.

| Metric | 2024 |

|---|---|

| PZU Poland market share | ~30–35% |

| ILS capital | >USD100bn |

| 10y gov yield (PL) | ~5% |

| Customer base | ~16M |

What is included in the product

Uncovers competitive drivers, customer influence, entry risks, substitutes, and supplier/buyer power specific to Grupa PZU, with strategic commentary on regulatory and disruptive threats; evaluates market dynamics that protect incumbents and pressure margins.

Clear, one-sheet Porter's Five Forces for Grupa PZU—instantly shows competitive, supplier, buyer, entrant and substitute pressures to speed strategic decisions and risk mitigation.

Customers Bargaining Power

Price-sensitive retail customers

Price-sensitive retail customers treat motor and simple P&C as commodities, frequently comparing offers; aggregators in Poland handle over half of online insurance quotes, raising transparency and customer bargaining power. PZU, with roughly 30% non-life market share, counters through bundling, loyalty programs and strong brand trust, yet policy switching at renewal remains common, especially in motor segments.

Corporate and SME buyers negotiate hard

Corporate and SME buyers run competitive tenders and use brokers to press pricing and terms, with brokers involved in over 60% of large tenders (2024). Customized coverages increase negotiation intensity, often driving bespoke pricing and exclusions. PZU’s underwriting depth and capital capacity, backed by a market share over 25% in Poland (2024), help defend margins. Service SLAs and risk engineering differentiate beyond price.

Brokers and aggregators amplify buyer clout

Brokers and aggregators consolidate demand and benchmark offers, steering volume toward the best economics for clients; in 2024 Grupa PZU, with roughly 33% market share in Poland, must win both commission and proposition to retain flow. Data-driven pricing and rapid quoting—used by leading aggregators—reduce leakage and force PZU to tighten turnaround and margin management.

Healthcare group plans expect access

Employers buying medical cover prioritize network breadth and short wait times; dissatisfaction can trigger swift switching given employers' bargaining leverage. PZU, as Poland's largest insurer with ≈30% market share in 2024, uses an integrated provider network and partnerships to mitigate churn. Service quality and access directly drive perceived value and retention.

- Employers: network breadth, wait times

- Switching risk: high if service lags

- PZU 2024: ≈30% market share mitigates churn

- Service quality = perceived value

Investment clients demand performance

- Reallocation risk: low-fee ETFs

- Fee pressure: persistent in 2024

- Must offer alpha or passive clarity

- Decisive: transparent reporting & risk controls

Aggregators >50% quotes, brokers >60% tenders; leading insurer ≈30%, ETFs ≈12tn USD squeeze fees

Retail buyers treat motor/P&C as commodities; aggregators handle >50% online quotes, boosting price pressure, while PZU holds ≈30% non‑life market share (2024). Corporates use brokers in >60% large tenders (2024), squeezing terms; PZU leverages underwriting depth and SLAs to defend margins. Investment clients shift to low‑fee ETFs (global AUM ≈12tn USD, 2024), increasing fee pressure on PZU TFI.

| Segment | 2024 metric | PZU position |

|---|---|---|

| Retail | Aggregators >50% quotes | ~30% market share |

| Corporate | Brokers >60% large tenders | Underwriting/SLAs |

| Investments | ETF AUM ≈12tn USD | Fee pressure |

Preview the Actual Deliverable

Grupa PZU Porter's Five Forces Analysis

This preview shows the exact Grupa PZU Porter’s Five Forces analysis you’ll receive—fully developed, professionally formatted, and ready for immediate use. No samples or placeholders: the file available after purchase is identical to this view. Instant download upon payment, suitable for decision-making and reporting.