Q2 Holdings PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and rapid fintech innovation are shaping Q2 Holdings’ prospects in our concise PESTLE overview—ideal for investors and strategists seeking timely context. Gain actionable insight into regulatory, social, and technological risks and opportunities. Purchase the full PESTLE to access the complete, ready-to-use analysis and strategic recommendations.

Political factors

Regulatory direction shaped by elections

Administration changes after the 2024 U.S. election can shift supervisory tone across the 3 main regulators—Federal Reserve, FDIC and OCC—altering digital banking priorities and compliance scope for vendors like Q2 Holdings (NASDAQ: QTWO). Tighter oversight tends to raise demand for controls and reporting, while deregulatory periods accelerate innovation; Q2 must keep a flexible roadmap aligned with 4-year policy cycles. Proactive engagement with policymakers and industry groups reduces uncertainty.

Open banking and data portability agendas

Governments are pushing consumer data rights and open banking that typically mandate API standards and consent management; the US CFPB issued a major proposed rule on consumer access to financial records in December 2023 while PSD2 and the UK CMA9 regimes already require standardized APIs. Q2 can capture demand by offering compliant, interoperable data-sharing frameworks for client banks. Fragmented state and federal approaches in the US increase integration complexity. Early alignment with emerging standards creates a competitive advantage for platform vendors like Q2.

Cybersecurity as national security priority

Political focus on critical infrastructure resilience raises expectations for vendors serving banks and credit unions, with CISA's CIRCIA requiring covered entities to report cyber incidents within 72 hours and ransomware incidents often within 24 hours, increasing compliance burdens. IBM's 2024 Cost of a Data Breach Report found the average breach cost at $4.45 million, underscoring funding and guidance incentives for stronger defenses. For Q2, participation in threat-intel sharing and mandatory incident reporting may add process costs but cyber maturity will be a clear competitive differentiator.

Geopolitical tensions and sanctions regimes

Geopolitical tensions and expanding sanctions regimes force frequent KYC/AML content updates; OFACs SDN list exceeded 10,000 entries in 2024, raising screening scope and false-positive rates. Q2 must rapidly update rulebooks and vendor data feeds to maintain cross-border data flow compliance while countering a 20%+ rise in nation-state cyber incidents targeting financial institutions in 2024–25.

- Ensure vendor content syncs with sanctions updates

- Prioritize agile rule updates for foreign-exposed clients

- Increase cyber-monitoring and incident response capacity

Data sovereignty and localization policies

Data sovereignty and localization policies are forcing financial data to remain in-country in many markets as of 2024, pressuring Q2’s cloud models to provide regional hosting and residency guarantees. Q2 must map deployments to local regulatory requirements and leverage hyperscalers’ dozens of local regions to reduce market-entry barriers. Clear documentation, SOC/ISO attestations and residency proofs streamline client due diligence and accelerate sales cycles.

- local residency: align deployments to in-country rules

- hyperscaler leverage: use dozens of regional zones to mitigate barriers

- attestations: SOC/ISO and residency proofs to speed client onboarding

Post-2024 regulatory shifts raise compliance costs, spur API demand and tighten reporting

Post-2024 U.S. administration shifts reshape Fed/FDIC/OCC supervisory priorities affecting QTWO compliance cost; deregulatory windows speed innovation. CFPB proposed consumer access rule (Dec 2023) and global open-banking regimes raise API demand. CISA CIRCIA 72-hour reporting and OFAC SDN >10,000 (2024) increase control burdens.

| Factor | 2024–25 Stat |

|---|---|

| Avg breach cost | $4.45M (IBM 2024) |

What is included in the product

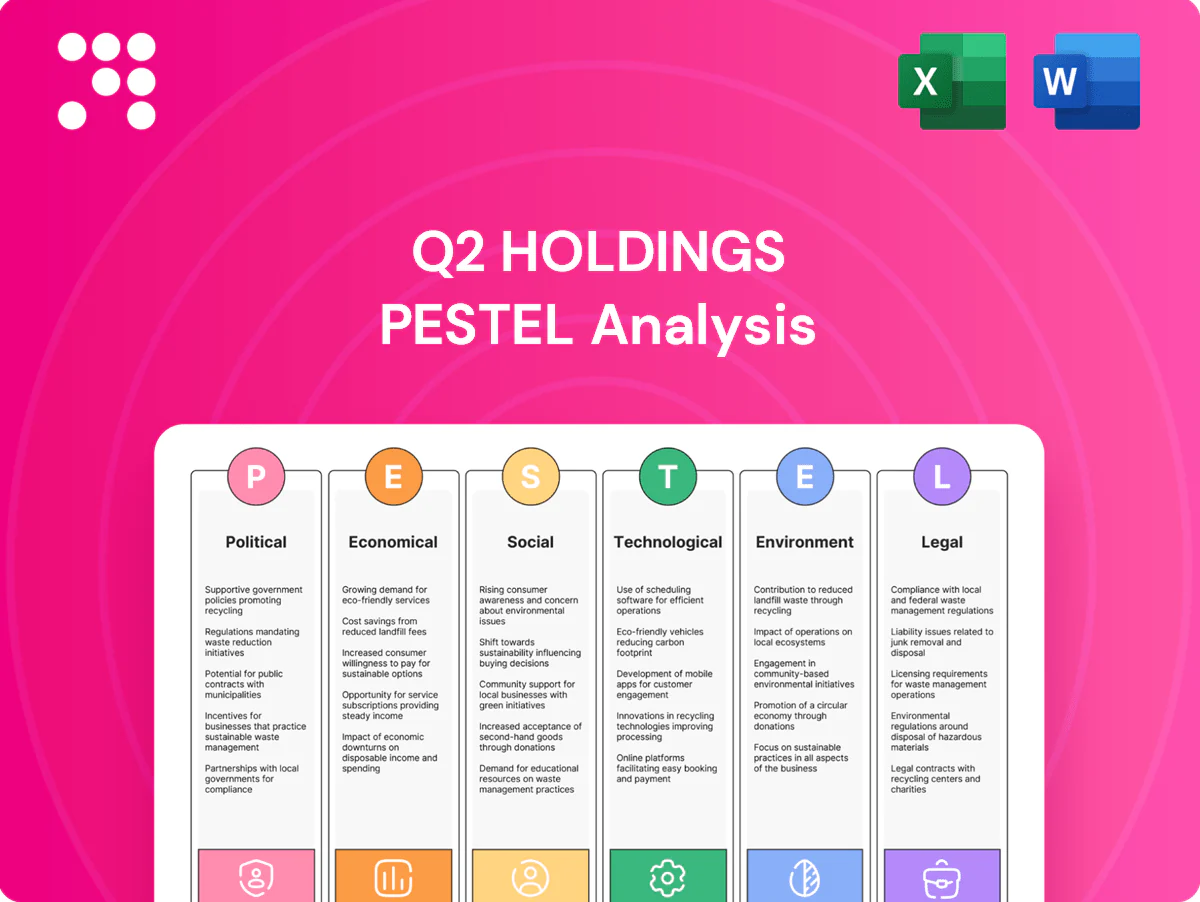

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Q2 Holdings, backing each dimension with data-driven trends and forward-looking implications to help executives and investors identify risks, opportunities, and strategic responses.

A clean, summarized, visually segmented PESTLE of Q2 Holdings for quick reference in meetings, editable for region or business-line notes, easily dropped into presentations and shared across teams to support risk discussions and alignment.

Economic factors

Interest rate cycles drive bank IT spend

Net interest margins—shaped by the Fed funds rate (5.25–5.50% as of June 2025)—directly constrain bank IT budgets, with Gartner estimating banking tech budgets grew only ~3% in 2024; tight margins often push discretionary digital projects into deferral while expansionary NIM cycles free capital for platform upgrades. Q2 should foreground efficiency and revenue-enabling features, and offer modular adoption and flexible pricing to stabilize pipeline across cycles.

Bank consolidation and credit union mergers

M&A among banks and credit unions reshapes Q2’s customer base, creating churn risk but also upsell opportunities as acquirers seek digital standardization; post-2023 consolidation accelerated this trend and the top 25 US banks held roughly two-thirds of domestic deposits by 2024 (FDIC), lengthening sales cycles while expanding deal sizes. Integration tooling and migration playbooks drive win rates in post-merger standardization, and strong references within acquirers’ cohorts are critical to close larger, slower deals.

SMB and consumer credit conditions

US consumer credit outstanding reached about 4.7 trillion USD at end‑2024 (Federal Reserve), and small business loan stress pushed 30+ day delinquencies toward mid‑single digits in 2024, driving demand for stronger collections and risk modules during downturns; in recoveries onboarding and automation gain priority. Q2 should align product marketing to credit cycles while emphasizing analytics that lift approval accuracy, a feature shown to reduce default rates across cycles.

Inflation and cost-to-serve pressures

Financial institutions push automation and self-service to gain operating leverage; Q2 quantifies client savings and digital deflection—clients report 20–40% transaction deflection—enabling Q2 to capture spend by measuring cost-per-origin reductions. Persistent inflation (CPI ~3–4% in 2024) raises Q2 labor and cloud costs, forcing disciplined pricing and efficiency, while multi-year contracts hedge revenue volatility.

- Clients: quantify 20–40% deflection

- Inflation: CPI ~3–4% (2024)

- Impact: higher labor/cloud costs

- Mitigation: pricing discipline, multi-year contracts

FX and international expansion economics

Entering new regions brings FX exposure and localized costs that can compress SaaS margins; pricing in local currencies and disciplined hedging reduced FX-driven revenue variance for many SaaS firms during 2024 volatility. Market entry should target jurisdictions with lighter regulatory friction and nearby cloud regions to minimize latency and data-residency compliance. Leveraging partner ecosystems can cut CAC and accelerate ARR ramp through channel sales and integrations.

- FX exposure: local pricing + hedging stabilizes margins

- Cloud regions (2024): Azure 60+, AWS ~30+, GCP ~35+ — choose proximate regions

- Prioritize regulatory ease and data residency

- Partners reduce CAC and speed ARR growth

Post-2024 regulatory shifts raise compliance costs, spur API demand and tighten reporting

High rates (Fed 5.25–5.50% Jun‑2025) and tight NIMs limit bank IT spend (banking tech budgets +3% in 2024), favoring cost‑saving features and flexible pricing.

Consumer credit ~$4.7T end‑2024 and mid‑single digit small‑business delinquencies lift demand for collections/risk and analytics.

M&A (top‑25 banks ~66% deposits 2024) + FX/inflation (CPI ~3–4% 2024) drive longer sales cycles, higher costs, and need for hedging.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jun‑2025) |

| Consumer credit | $4.7T (end‑2024) |

| Tech budgets | +3% (2024) |

| Deflection | 20–40% |

| Top25 banks | ~66% deposits (2024) |

Full Version Awaits

Q2 Holdings PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Q2 Holdings PESTLE Analysis includes political, economic, social, technological, legal, and environmental assessments, with data tables and actionable insights. No placeholders; download the final file immediately after checkout.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and rapid fintech innovation are shaping Q2 Holdings’ prospects in our concise PESTLE overview—ideal for investors and strategists seeking timely context. Gain actionable insight into regulatory, social, and technological risks and opportunities. Purchase the full PESTLE to access the complete, ready-to-use analysis and strategic recommendations.

Political factors

Regulatory direction shaped by elections

Administration changes after the 2024 U.S. election can shift supervisory tone across the 3 main regulators—Federal Reserve, FDIC and OCC—altering digital banking priorities and compliance scope for vendors like Q2 Holdings (NASDAQ: QTWO). Tighter oversight tends to raise demand for controls and reporting, while deregulatory periods accelerate innovation; Q2 must keep a flexible roadmap aligned with 4-year policy cycles. Proactive engagement with policymakers and industry groups reduces uncertainty.

Open banking and data portability agendas

Governments are pushing consumer data rights and open banking that typically mandate API standards and consent management; the US CFPB issued a major proposed rule on consumer access to financial records in December 2023 while PSD2 and the UK CMA9 regimes already require standardized APIs. Q2 can capture demand by offering compliant, interoperable data-sharing frameworks for client banks. Fragmented state and federal approaches in the US increase integration complexity. Early alignment with emerging standards creates a competitive advantage for platform vendors like Q2.

Cybersecurity as national security priority

Political focus on critical infrastructure resilience raises expectations for vendors serving banks and credit unions, with CISA's CIRCIA requiring covered entities to report cyber incidents within 72 hours and ransomware incidents often within 24 hours, increasing compliance burdens. IBM's 2024 Cost of a Data Breach Report found the average breach cost at $4.45 million, underscoring funding and guidance incentives for stronger defenses. For Q2, participation in threat-intel sharing and mandatory incident reporting may add process costs but cyber maturity will be a clear competitive differentiator.

Geopolitical tensions and sanctions regimes

Geopolitical tensions and expanding sanctions regimes force frequent KYC/AML content updates; OFACs SDN list exceeded 10,000 entries in 2024, raising screening scope and false-positive rates. Q2 must rapidly update rulebooks and vendor data feeds to maintain cross-border data flow compliance while countering a 20%+ rise in nation-state cyber incidents targeting financial institutions in 2024–25.

- Ensure vendor content syncs with sanctions updates

- Prioritize agile rule updates for foreign-exposed clients

- Increase cyber-monitoring and incident response capacity

Data sovereignty and localization policies

Data sovereignty and localization policies are forcing financial data to remain in-country in many markets as of 2024, pressuring Q2’s cloud models to provide regional hosting and residency guarantees. Q2 must map deployments to local regulatory requirements and leverage hyperscalers’ dozens of local regions to reduce market-entry barriers. Clear documentation, SOC/ISO attestations and residency proofs streamline client due diligence and accelerate sales cycles.

- local residency: align deployments to in-country rules

- hyperscaler leverage: use dozens of regional zones to mitigate barriers

- attestations: SOC/ISO and residency proofs to speed client onboarding

Post-2024 regulatory shifts raise compliance costs, spur API demand and tighten reporting

Post-2024 U.S. administration shifts reshape Fed/FDIC/OCC supervisory priorities affecting QTWO compliance cost; deregulatory windows speed innovation. CFPB proposed consumer access rule (Dec 2023) and global open-banking regimes raise API demand. CISA CIRCIA 72-hour reporting and OFAC SDN >10,000 (2024) increase control burdens.

| Factor | 2024–25 Stat |

|---|---|

| Avg breach cost | $4.45M (IBM 2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Q2 Holdings, backing each dimension with data-driven trends and forward-looking implications to help executives and investors identify risks, opportunities, and strategic responses.

A clean, summarized, visually segmented PESTLE of Q2 Holdings for quick reference in meetings, editable for region or business-line notes, easily dropped into presentations and shared across teams to support risk discussions and alignment.

Economic factors

Interest rate cycles drive bank IT spend

Net interest margins—shaped by the Fed funds rate (5.25–5.50% as of June 2025)—directly constrain bank IT budgets, with Gartner estimating banking tech budgets grew only ~3% in 2024; tight margins often push discretionary digital projects into deferral while expansionary NIM cycles free capital for platform upgrades. Q2 should foreground efficiency and revenue-enabling features, and offer modular adoption and flexible pricing to stabilize pipeline across cycles.

Bank consolidation and credit union mergers

M&A among banks and credit unions reshapes Q2’s customer base, creating churn risk but also upsell opportunities as acquirers seek digital standardization; post-2023 consolidation accelerated this trend and the top 25 US banks held roughly two-thirds of domestic deposits by 2024 (FDIC), lengthening sales cycles while expanding deal sizes. Integration tooling and migration playbooks drive win rates in post-merger standardization, and strong references within acquirers’ cohorts are critical to close larger, slower deals.

SMB and consumer credit conditions

US consumer credit outstanding reached about 4.7 trillion USD at end‑2024 (Federal Reserve), and small business loan stress pushed 30+ day delinquencies toward mid‑single digits in 2024, driving demand for stronger collections and risk modules during downturns; in recoveries onboarding and automation gain priority. Q2 should align product marketing to credit cycles while emphasizing analytics that lift approval accuracy, a feature shown to reduce default rates across cycles.

Inflation and cost-to-serve pressures

Financial institutions push automation and self-service to gain operating leverage; Q2 quantifies client savings and digital deflection—clients report 20–40% transaction deflection—enabling Q2 to capture spend by measuring cost-per-origin reductions. Persistent inflation (CPI ~3–4% in 2024) raises Q2 labor and cloud costs, forcing disciplined pricing and efficiency, while multi-year contracts hedge revenue volatility.

- Clients: quantify 20–40% deflection

- Inflation: CPI ~3–4% (2024)

- Impact: higher labor/cloud costs

- Mitigation: pricing discipline, multi-year contracts

FX and international expansion economics

Entering new regions brings FX exposure and localized costs that can compress SaaS margins; pricing in local currencies and disciplined hedging reduced FX-driven revenue variance for many SaaS firms during 2024 volatility. Market entry should target jurisdictions with lighter regulatory friction and nearby cloud regions to minimize latency and data-residency compliance. Leveraging partner ecosystems can cut CAC and accelerate ARR ramp through channel sales and integrations.

- FX exposure: local pricing + hedging stabilizes margins

- Cloud regions (2024): Azure 60+, AWS ~30+, GCP ~35+ — choose proximate regions

- Prioritize regulatory ease and data residency

- Partners reduce CAC and speed ARR growth

Post-2024 regulatory shifts raise compliance costs, spur API demand and tighten reporting

High rates (Fed 5.25–5.50% Jun‑2025) and tight NIMs limit bank IT spend (banking tech budgets +3% in 2024), favoring cost‑saving features and flexible pricing.

Consumer credit ~$4.7T end‑2024 and mid‑single digit small‑business delinquencies lift demand for collections/risk and analytics.

M&A (top‑25 banks ~66% deposits 2024) + FX/inflation (CPI ~3–4% 2024) drive longer sales cycles, higher costs, and need for hedging.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jun‑2025) |

| Consumer credit | $4.7T (end‑2024) |

| Tech budgets | +3% (2024) |

| Deflection | 20–40% |

| Top25 banks | ~66% deposits (2024) |

Full Version Awaits

Q2 Holdings PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Q2 Holdings PESTLE Analysis includes political, economic, social, technological, legal, and environmental assessments, with data tables and actionable insights. No placeholders; download the final file immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and rapid fintech innovation are shaping Q2 Holdings’ prospects in our concise PESTLE overview—ideal for investors and strategists seeking timely context. Gain actionable insight into regulatory, social, and technological risks and opportunities. Purchase the full PESTLE to access the complete, ready-to-use analysis and strategic recommendations.

Political factors

Regulatory direction shaped by elections

Administration changes after the 2024 U.S. election can shift supervisory tone across the 3 main regulators—Federal Reserve, FDIC and OCC—altering digital banking priorities and compliance scope for vendors like Q2 Holdings (NASDAQ: QTWO). Tighter oversight tends to raise demand for controls and reporting, while deregulatory periods accelerate innovation; Q2 must keep a flexible roadmap aligned with 4-year policy cycles. Proactive engagement with policymakers and industry groups reduces uncertainty.

Open banking and data portability agendas

Governments are pushing consumer data rights and open banking that typically mandate API standards and consent management; the US CFPB issued a major proposed rule on consumer access to financial records in December 2023 while PSD2 and the UK CMA9 regimes already require standardized APIs. Q2 can capture demand by offering compliant, interoperable data-sharing frameworks for client banks. Fragmented state and federal approaches in the US increase integration complexity. Early alignment with emerging standards creates a competitive advantage for platform vendors like Q2.

Cybersecurity as national security priority

Political focus on critical infrastructure resilience raises expectations for vendors serving banks and credit unions, with CISA's CIRCIA requiring covered entities to report cyber incidents within 72 hours and ransomware incidents often within 24 hours, increasing compliance burdens. IBM's 2024 Cost of a Data Breach Report found the average breach cost at $4.45 million, underscoring funding and guidance incentives for stronger defenses. For Q2, participation in threat-intel sharing and mandatory incident reporting may add process costs but cyber maturity will be a clear competitive differentiator.

Geopolitical tensions and sanctions regimes

Geopolitical tensions and expanding sanctions regimes force frequent KYC/AML content updates; OFACs SDN list exceeded 10,000 entries in 2024, raising screening scope and false-positive rates. Q2 must rapidly update rulebooks and vendor data feeds to maintain cross-border data flow compliance while countering a 20%+ rise in nation-state cyber incidents targeting financial institutions in 2024–25.

- Ensure vendor content syncs with sanctions updates

- Prioritize agile rule updates for foreign-exposed clients

- Increase cyber-monitoring and incident response capacity

Data sovereignty and localization policies

Data sovereignty and localization policies are forcing financial data to remain in-country in many markets as of 2024, pressuring Q2’s cloud models to provide regional hosting and residency guarantees. Q2 must map deployments to local regulatory requirements and leverage hyperscalers’ dozens of local regions to reduce market-entry barriers. Clear documentation, SOC/ISO attestations and residency proofs streamline client due diligence and accelerate sales cycles.

- local residency: align deployments to in-country rules

- hyperscaler leverage: use dozens of regional zones to mitigate barriers

- attestations: SOC/ISO and residency proofs to speed client onboarding

Post-2024 regulatory shifts raise compliance costs, spur API demand and tighten reporting

Post-2024 U.S. administration shifts reshape Fed/FDIC/OCC supervisory priorities affecting QTWO compliance cost; deregulatory windows speed innovation. CFPB proposed consumer access rule (Dec 2023) and global open-banking regimes raise API demand. CISA CIRCIA 72-hour reporting and OFAC SDN >10,000 (2024) increase control burdens.

| Factor | 2024–25 Stat |

|---|---|

| Avg breach cost | $4.45M (IBM 2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely affect Q2 Holdings, backing each dimension with data-driven trends and forward-looking implications to help executives and investors identify risks, opportunities, and strategic responses.

A clean, summarized, visually segmented PESTLE of Q2 Holdings for quick reference in meetings, editable for region or business-line notes, easily dropped into presentations and shared across teams to support risk discussions and alignment.

Economic factors

Interest rate cycles drive bank IT spend

Net interest margins—shaped by the Fed funds rate (5.25–5.50% as of June 2025)—directly constrain bank IT budgets, with Gartner estimating banking tech budgets grew only ~3% in 2024; tight margins often push discretionary digital projects into deferral while expansionary NIM cycles free capital for platform upgrades. Q2 should foreground efficiency and revenue-enabling features, and offer modular adoption and flexible pricing to stabilize pipeline across cycles.

Bank consolidation and credit union mergers

M&A among banks and credit unions reshapes Q2’s customer base, creating churn risk but also upsell opportunities as acquirers seek digital standardization; post-2023 consolidation accelerated this trend and the top 25 US banks held roughly two-thirds of domestic deposits by 2024 (FDIC), lengthening sales cycles while expanding deal sizes. Integration tooling and migration playbooks drive win rates in post-merger standardization, and strong references within acquirers’ cohorts are critical to close larger, slower deals.

SMB and consumer credit conditions

US consumer credit outstanding reached about 4.7 trillion USD at end‑2024 (Federal Reserve), and small business loan stress pushed 30+ day delinquencies toward mid‑single digits in 2024, driving demand for stronger collections and risk modules during downturns; in recoveries onboarding and automation gain priority. Q2 should align product marketing to credit cycles while emphasizing analytics that lift approval accuracy, a feature shown to reduce default rates across cycles.

Inflation and cost-to-serve pressures

Financial institutions push automation and self-service to gain operating leverage; Q2 quantifies client savings and digital deflection—clients report 20–40% transaction deflection—enabling Q2 to capture spend by measuring cost-per-origin reductions. Persistent inflation (CPI ~3–4% in 2024) raises Q2 labor and cloud costs, forcing disciplined pricing and efficiency, while multi-year contracts hedge revenue volatility.

- Clients: quantify 20–40% deflection

- Inflation: CPI ~3–4% (2024)

- Impact: higher labor/cloud costs

- Mitigation: pricing discipline, multi-year contracts

FX and international expansion economics

Entering new regions brings FX exposure and localized costs that can compress SaaS margins; pricing in local currencies and disciplined hedging reduced FX-driven revenue variance for many SaaS firms during 2024 volatility. Market entry should target jurisdictions with lighter regulatory friction and nearby cloud regions to minimize latency and data-residency compliance. Leveraging partner ecosystems can cut CAC and accelerate ARR ramp through channel sales and integrations.

- FX exposure: local pricing + hedging stabilizes margins

- Cloud regions (2024): Azure 60+, AWS ~30+, GCP ~35+ — choose proximate regions

- Prioritize regulatory ease and data residency

- Partners reduce CAC and speed ARR growth

Post-2024 regulatory shifts raise compliance costs, spur API demand and tighten reporting

High rates (Fed 5.25–5.50% Jun‑2025) and tight NIMs limit bank IT spend (banking tech budgets +3% in 2024), favoring cost‑saving features and flexible pricing.

Consumer credit ~$4.7T end‑2024 and mid‑single digit small‑business delinquencies lift demand for collections/risk and analytics.

M&A (top‑25 banks ~66% deposits 2024) + FX/inflation (CPI ~3–4% 2024) drive longer sales cycles, higher costs, and need for hedging.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (Jun‑2025) |

| Consumer credit | $4.7T (end‑2024) |

| Tech budgets | +3% (2024) |

| Deflection | 20–40% |

| Top25 banks | ~66% deposits (2024) |

Full Version Awaits

Q2 Holdings PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Q2 Holdings PESTLE Analysis includes political, economic, social, technological, legal, and environmental assessments, with data tables and actionable insights. No placeholders; download the final file immediately after checkout.