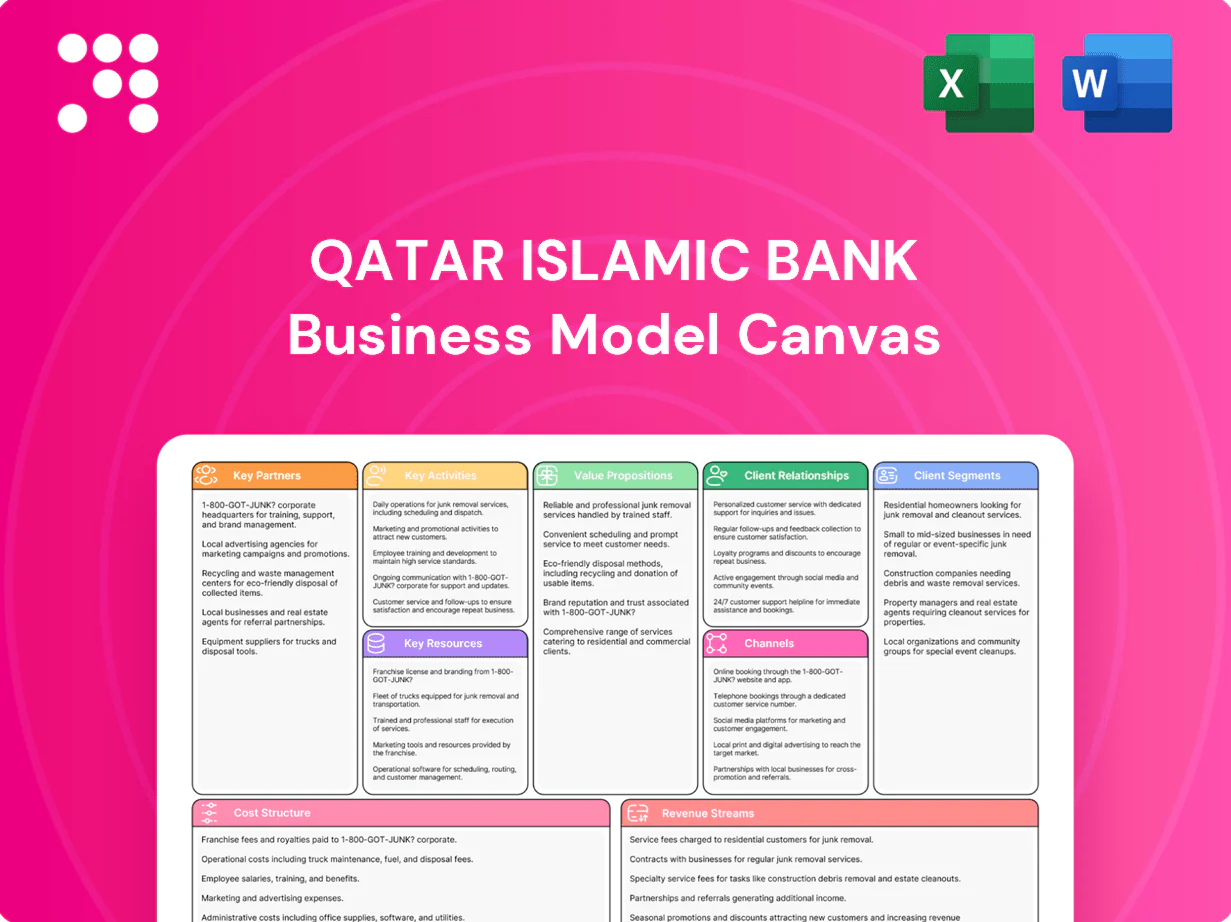

Qatar Islamic Bank Business Model Canvas

Islamic Banking Business Model Canvas: 3-5 insights on value, risk and growth

Unlock the full strategic blueprint behind Qatar Islamic Bank with our concise Business Model Canvas—three to five clear insights on how it creates value, manages risk, and captures market share in Islamic finance. This downloadable, editable canvas includes customer segments, revenue streams, key partners and cost structure to fuel benchmarking, investor due diligence, or strategic planning. Purchase the full file to access detailed, company-specific analysis ready for immediate use.

Partnerships

Shariah Board

Qatar Islamic Bank’s independent Shariah Board, typically a five-member panel of scholars, vets and issues fatwas for structures like Murabaha, Ijara and Mudaraba, ensuring product compliance with Islamic jurisprudence.

They review contracts, approve product structures and mandate ongoing Shariah audits that underpin credibility and mitigate Shariah non-compliance risk for the bank’s QAR-scale retail and corporate portfolios.

Correspondent Banks

Correspondent banks, both Islamic and conventional, underpin QIB’s cross-border settlements and trade finance, enabling remittances, letters of credit and treasury placements that support corporate and institutional clients. Global remittances reached about $643 billion in 2023, illustrating scale of flows facilitated by these networks. Such partnerships extend QIB’s reach into key markets and help close parts of the global trade finance gap estimated at roughly $1.7 trillion.

Fintech and Tech Vendors

Fintech and tech vendors supply QIB with core banking engines, digital channels, cybersecurity, and analytics, enabling a 25% year-on-year rise in mobile transactions in 2024 and faster digital onboarding.

Government and Regulators

Close alignment with Qatar Central Bank and national bodies ensures QIB meets prudential standards and positions it as Qatar's largest Islamic bank by assets (reported QAR 140.9bn in 2023), strengthening capital and liquidity resilience. Ongoing engagement supports AML, KYC and data standards, enabling timely participation in national initiatives like Qatar National Vision 2030 and reducing regulatory uncertainty.

- Regulatory alignment: Qatar Central Bank

- AML/KYC/data compliance

- Participation: Qatar National Vision 2030

- 2023 assets: QAR 140.9bn

Corporate and Takaful Alliances

Alliances with Takaful providers bundle protection with home, auto and SME financing, boosting customer retention and compliance with Sharia services; Qatar Islamic Bank, with c. QAR 115bn in assets (2024), uses these bundles to enhance cross-sell and reduce credit risk. Partnerships with large corporates and developers unlock payroll, supply-chain and project finance flows, while co-marketing lifts acquisition; structured deals deepen wallet share through tailored cash-management and sukuk-linked facilities.

- Corporate payroll integrations — steady inflow of salary accounts

- Takaful bundles — higher cross-sell, lower NPL volatility

- Structured project finance — larger ticket sizes, longer tenors

Shariah and banks power trade finance; fintech boosts 25% mobile growth

Shariah board certifies Murabaha/Ijara/Mudaraba products and enforces Shariah audits; correspondent banks enable trade finance and remittances (global remittances $643bn in 2023; $1.7trn trade finance gap); fintech vendors drive 25% YoY mobile transaction growth (2024); close regulatory ties with Qatar Central Bank underpin prudential strength (QIB assets QAR 140.9bn in 2023).

| Partnership | Role | Metric |

|---|---|---|

| Shariah Board | Compliance | — |

| Correspondent Banks | Cross-border | $643bn remittances 2023 |

| Fintech Vendors | Digital | 25% mobile Tx growth 2024 |

| Qatar Central Bank | Regulation | QIB assets QAR 140.9bn 2023 |

What is included in the product

A concise, pre-written Business Model Canvas for Qatar Islamic Bank outlining nine BMC blocks—Sharia-compliant value propositions, retail and corporate customer segments, multichannel distribution, profit-sharing and fee-based revenue, key partners and Islamic governance, cost structure and risk controls, competitive strengths and growth opportunities—suitable for presentations, investor discussions, and strategic planning.

High-level view of Qatar Islamic Bank’s business model with editable cells, relieving the pain of scattered analysis and saving hours on formatting and structuring your own model for quick boardroom-ready reviews.

Activities

Shariah-Compliant Financing

Origination and underwriting of Murabaha, Ijara, Istisna and Mudaraba facilities follow strict Shariah-compliant workflows, with pricing and risk assessment tailored to each contract structure. Documentation and asset flows are tightly managed through custody and trade records to ensure Shariah traceability. Ongoing portfolio monitoring tracks performance, asset quality and compliance across retail, corporate and project finance segments.

Deposit Mobilization

Grow current, savings and investment accounts under profit‑sharing models to expand a deposit base (QAR 65bn reported in 2024), optimize product mix and expected profit rates to improve margins, manage liquidity to balance funding cost and stability, and run targeted campaigns to attract retail, SME and high‑net‑worth segments.

Treasury and Liquidity

Treasury manages cash, placements, Sukuk investments and Shariah‑compliant hedging instruments to optimize yield within Islamic principles. It maintains LCR and NSFR above the Basel III regulatory minima of 100% to ensure short‑ and long‑term liquidity coverage. Daily execution of interbank Murabaha and Wakala supports funding, balance‑sheet resilience and steady income generation.

Digital Banking Delivery

Operate mobile, online and API channels to deliver seamless banking across platforms, improving UX, security and uptime; in 2024 Qatar internet penetration reached about 99%, enabling broad digital reach. Drive straight-through processing and eKYC to cut onboarding times and transaction friction. Use analytics to personalize offers, boost conversion and lower drop-off.

- Channels: mobile, online, APIs

- Processes: STP, eKYC

- Focus: UX, security, analytics

Risk and Compliance

Credit, market, operational and Shariah risk frameworks govern Qatar Islamic Bank’s underwriting, trading and product approvals, aligned to Basel III minimum CET1 of 4.5% and international Shariah standards. AML, sanctions screening and Qatar data protection rules are embedded across onboarding and transaction monitoring, meeting FATF-based controls. Regular stress tests and limits maintain capital buffers above regulatory minima; continuous audit and model validation ensure adherence.

- Risk coverage: credit, market, operational, Shariah

- Regulatory anchors: Basel III CET1 4.5%

- Controls: AML, sanctions, data privacy (Qatar rules, FATF-aligned)

- Safeguards: stress tests, limits, continuous audit

Shariah finance origination: Murabaha, Ijara, digital STP and QAR 65bn deposits

Origination and underwriting of Murabaha, Ijara, Istisna and Mudaraba with strict Shariah workflows, custody and portfolio monitoring across retail, corporate and project finance.

Grow current, savings and investment accounts under profit‑sharing; deposits QAR 65bn (2024) to optimize funding mix and margins.

Treasury manages Sukuk, interbank Murabaha/Wakala and maintains LCR/NSFR above 100% for liquidity resilience.

Operate mobile, online and API channels; Qatar internet penetration ~99% (2024) to drive STP, eKYC and analytics.

| Metric | Value (2024) |

|---|---|

| Deposits | QAR 65bn |

| LCR / NSFR | >=100% |

| Internet penetration | ~99% |

| Regulatory CET1 min | 4.5% |

Preview Before You Purchase

Business Model Canvas

The Qatar Islamic Bank Business Model Canvas you’re previewing is the actual deliverable, not a mockup. It’s a direct snapshot of the full document you’ll receive after purchase. Upon buying, you’ll immediately download the same editable file, formatted and ready to use in Word and Excel. No placeholders, no surprises—what you see is what you get.

Islamic Banking Business Model Canvas: 3-5 insights on value, risk and growth

Unlock the full strategic blueprint behind Qatar Islamic Bank with our concise Business Model Canvas—three to five clear insights on how it creates value, manages risk, and captures market share in Islamic finance. This downloadable, editable canvas includes customer segments, revenue streams, key partners and cost structure to fuel benchmarking, investor due diligence, or strategic planning. Purchase the full file to access detailed, company-specific analysis ready for immediate use.

Partnerships

Shariah Board

Qatar Islamic Bank’s independent Shariah Board, typically a five-member panel of scholars, vets and issues fatwas for structures like Murabaha, Ijara and Mudaraba, ensuring product compliance with Islamic jurisprudence.

They review contracts, approve product structures and mandate ongoing Shariah audits that underpin credibility and mitigate Shariah non-compliance risk for the bank’s QAR-scale retail and corporate portfolios.

Correspondent Banks

Correspondent banks, both Islamic and conventional, underpin QIB’s cross-border settlements and trade finance, enabling remittances, letters of credit and treasury placements that support corporate and institutional clients. Global remittances reached about $643 billion in 2023, illustrating scale of flows facilitated by these networks. Such partnerships extend QIB’s reach into key markets and help close parts of the global trade finance gap estimated at roughly $1.7 trillion.

Fintech and Tech Vendors

Fintech and tech vendors supply QIB with core banking engines, digital channels, cybersecurity, and analytics, enabling a 25% year-on-year rise in mobile transactions in 2024 and faster digital onboarding.

Government and Regulators

Close alignment with Qatar Central Bank and national bodies ensures QIB meets prudential standards and positions it as Qatar's largest Islamic bank by assets (reported QAR 140.9bn in 2023), strengthening capital and liquidity resilience. Ongoing engagement supports AML, KYC and data standards, enabling timely participation in national initiatives like Qatar National Vision 2030 and reducing regulatory uncertainty.

- Regulatory alignment: Qatar Central Bank

- AML/KYC/data compliance

- Participation: Qatar National Vision 2030

- 2023 assets: QAR 140.9bn

Corporate and Takaful Alliances

Alliances with Takaful providers bundle protection with home, auto and SME financing, boosting customer retention and compliance with Sharia services; Qatar Islamic Bank, with c. QAR 115bn in assets (2024), uses these bundles to enhance cross-sell and reduce credit risk. Partnerships with large corporates and developers unlock payroll, supply-chain and project finance flows, while co-marketing lifts acquisition; structured deals deepen wallet share through tailored cash-management and sukuk-linked facilities.

- Corporate payroll integrations — steady inflow of salary accounts

- Takaful bundles — higher cross-sell, lower NPL volatility

- Structured project finance — larger ticket sizes, longer tenors

Shariah and banks power trade finance; fintech boosts 25% mobile growth

Shariah board certifies Murabaha/Ijara/Mudaraba products and enforces Shariah audits; correspondent banks enable trade finance and remittances (global remittances $643bn in 2023; $1.7trn trade finance gap); fintech vendors drive 25% YoY mobile transaction growth (2024); close regulatory ties with Qatar Central Bank underpin prudential strength (QIB assets QAR 140.9bn in 2023).

| Partnership | Role | Metric |

|---|---|---|

| Shariah Board | Compliance | — |

| Correspondent Banks | Cross-border | $643bn remittances 2023 |

| Fintech Vendors | Digital | 25% mobile Tx growth 2024 |

| Qatar Central Bank | Regulation | QIB assets QAR 140.9bn 2023 |

What is included in the product

A concise, pre-written Business Model Canvas for Qatar Islamic Bank outlining nine BMC blocks—Sharia-compliant value propositions, retail and corporate customer segments, multichannel distribution, profit-sharing and fee-based revenue, key partners and Islamic governance, cost structure and risk controls, competitive strengths and growth opportunities—suitable for presentations, investor discussions, and strategic planning.

High-level view of Qatar Islamic Bank’s business model with editable cells, relieving the pain of scattered analysis and saving hours on formatting and structuring your own model for quick boardroom-ready reviews.

Activities

Shariah-Compliant Financing

Origination and underwriting of Murabaha, Ijara, Istisna and Mudaraba facilities follow strict Shariah-compliant workflows, with pricing and risk assessment tailored to each contract structure. Documentation and asset flows are tightly managed through custody and trade records to ensure Shariah traceability. Ongoing portfolio monitoring tracks performance, asset quality and compliance across retail, corporate and project finance segments.

Deposit Mobilization

Grow current, savings and investment accounts under profit‑sharing models to expand a deposit base (QAR 65bn reported in 2024), optimize product mix and expected profit rates to improve margins, manage liquidity to balance funding cost and stability, and run targeted campaigns to attract retail, SME and high‑net‑worth segments.

Treasury and Liquidity

Treasury manages cash, placements, Sukuk investments and Shariah‑compliant hedging instruments to optimize yield within Islamic principles. It maintains LCR and NSFR above the Basel III regulatory minima of 100% to ensure short‑ and long‑term liquidity coverage. Daily execution of interbank Murabaha and Wakala supports funding, balance‑sheet resilience and steady income generation.

Digital Banking Delivery

Operate mobile, online and API channels to deliver seamless banking across platforms, improving UX, security and uptime; in 2024 Qatar internet penetration reached about 99%, enabling broad digital reach. Drive straight-through processing and eKYC to cut onboarding times and transaction friction. Use analytics to personalize offers, boost conversion and lower drop-off.

- Channels: mobile, online, APIs

- Processes: STP, eKYC

- Focus: UX, security, analytics

Risk and Compliance

Credit, market, operational and Shariah risk frameworks govern Qatar Islamic Bank’s underwriting, trading and product approvals, aligned to Basel III minimum CET1 of 4.5% and international Shariah standards. AML, sanctions screening and Qatar data protection rules are embedded across onboarding and transaction monitoring, meeting FATF-based controls. Regular stress tests and limits maintain capital buffers above regulatory minima; continuous audit and model validation ensure adherence.

- Risk coverage: credit, market, operational, Shariah

- Regulatory anchors: Basel III CET1 4.5%

- Controls: AML, sanctions, data privacy (Qatar rules, FATF-aligned)

- Safeguards: stress tests, limits, continuous audit

Shariah finance origination: Murabaha, Ijara, digital STP and QAR 65bn deposits

Origination and underwriting of Murabaha, Ijara, Istisna and Mudaraba with strict Shariah workflows, custody and portfolio monitoring across retail, corporate and project finance.

Grow current, savings and investment accounts under profit‑sharing; deposits QAR 65bn (2024) to optimize funding mix and margins.

Treasury manages Sukuk, interbank Murabaha/Wakala and maintains LCR/NSFR above 100% for liquidity resilience.

Operate mobile, online and API channels; Qatar internet penetration ~99% (2024) to drive STP, eKYC and analytics.

| Metric | Value (2024) |

|---|---|

| Deposits | QAR 65bn |

| LCR / NSFR | >=100% |

| Internet penetration | ~99% |

| Regulatory CET1 min | 4.5% |

Preview Before You Purchase

Business Model Canvas

The Qatar Islamic Bank Business Model Canvas you’re previewing is the actual deliverable, not a mockup. It’s a direct snapshot of the full document you’ll receive after purchase. Upon buying, you’ll immediately download the same editable file, formatted and ready to use in Word and Excel. No placeholders, no surprises—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Islamic Banking Business Model Canvas: 3-5 insights on value, risk and growth

Unlock the full strategic blueprint behind Qatar Islamic Bank with our concise Business Model Canvas—three to five clear insights on how it creates value, manages risk, and captures market share in Islamic finance. This downloadable, editable canvas includes customer segments, revenue streams, key partners and cost structure to fuel benchmarking, investor due diligence, or strategic planning. Purchase the full file to access detailed, company-specific analysis ready for immediate use.

Partnerships

Shariah Board

Qatar Islamic Bank’s independent Shariah Board, typically a five-member panel of scholars, vets and issues fatwas for structures like Murabaha, Ijara and Mudaraba, ensuring product compliance with Islamic jurisprudence.

They review contracts, approve product structures and mandate ongoing Shariah audits that underpin credibility and mitigate Shariah non-compliance risk for the bank’s QAR-scale retail and corporate portfolios.

Correspondent Banks

Correspondent banks, both Islamic and conventional, underpin QIB’s cross-border settlements and trade finance, enabling remittances, letters of credit and treasury placements that support corporate and institutional clients. Global remittances reached about $643 billion in 2023, illustrating scale of flows facilitated by these networks. Such partnerships extend QIB’s reach into key markets and help close parts of the global trade finance gap estimated at roughly $1.7 trillion.

Fintech and Tech Vendors

Fintech and tech vendors supply QIB with core banking engines, digital channels, cybersecurity, and analytics, enabling a 25% year-on-year rise in mobile transactions in 2024 and faster digital onboarding.

Government and Regulators

Close alignment with Qatar Central Bank and national bodies ensures QIB meets prudential standards and positions it as Qatar's largest Islamic bank by assets (reported QAR 140.9bn in 2023), strengthening capital and liquidity resilience. Ongoing engagement supports AML, KYC and data standards, enabling timely participation in national initiatives like Qatar National Vision 2030 and reducing regulatory uncertainty.

- Regulatory alignment: Qatar Central Bank

- AML/KYC/data compliance

- Participation: Qatar National Vision 2030

- 2023 assets: QAR 140.9bn

Corporate and Takaful Alliances

Alliances with Takaful providers bundle protection with home, auto and SME financing, boosting customer retention and compliance with Sharia services; Qatar Islamic Bank, with c. QAR 115bn in assets (2024), uses these bundles to enhance cross-sell and reduce credit risk. Partnerships with large corporates and developers unlock payroll, supply-chain and project finance flows, while co-marketing lifts acquisition; structured deals deepen wallet share through tailored cash-management and sukuk-linked facilities.

- Corporate payroll integrations — steady inflow of salary accounts

- Takaful bundles — higher cross-sell, lower NPL volatility

- Structured project finance — larger ticket sizes, longer tenors

Shariah and banks power trade finance; fintech boosts 25% mobile growth

Shariah board certifies Murabaha/Ijara/Mudaraba products and enforces Shariah audits; correspondent banks enable trade finance and remittances (global remittances $643bn in 2023; $1.7trn trade finance gap); fintech vendors drive 25% YoY mobile transaction growth (2024); close regulatory ties with Qatar Central Bank underpin prudential strength (QIB assets QAR 140.9bn in 2023).

| Partnership | Role | Metric |

|---|---|---|

| Shariah Board | Compliance | — |

| Correspondent Banks | Cross-border | $643bn remittances 2023 |

| Fintech Vendors | Digital | 25% mobile Tx growth 2024 |

| Qatar Central Bank | Regulation | QIB assets QAR 140.9bn 2023 |

What is included in the product

A concise, pre-written Business Model Canvas for Qatar Islamic Bank outlining nine BMC blocks—Sharia-compliant value propositions, retail and corporate customer segments, multichannel distribution, profit-sharing and fee-based revenue, key partners and Islamic governance, cost structure and risk controls, competitive strengths and growth opportunities—suitable for presentations, investor discussions, and strategic planning.

High-level view of Qatar Islamic Bank’s business model with editable cells, relieving the pain of scattered analysis and saving hours on formatting and structuring your own model for quick boardroom-ready reviews.

Activities

Shariah-Compliant Financing

Origination and underwriting of Murabaha, Ijara, Istisna and Mudaraba facilities follow strict Shariah-compliant workflows, with pricing and risk assessment tailored to each contract structure. Documentation and asset flows are tightly managed through custody and trade records to ensure Shariah traceability. Ongoing portfolio monitoring tracks performance, asset quality and compliance across retail, corporate and project finance segments.

Deposit Mobilization

Grow current, savings and investment accounts under profit‑sharing models to expand a deposit base (QAR 65bn reported in 2024), optimize product mix and expected profit rates to improve margins, manage liquidity to balance funding cost and stability, and run targeted campaigns to attract retail, SME and high‑net‑worth segments.

Treasury and Liquidity

Treasury manages cash, placements, Sukuk investments and Shariah‑compliant hedging instruments to optimize yield within Islamic principles. It maintains LCR and NSFR above the Basel III regulatory minima of 100% to ensure short‑ and long‑term liquidity coverage. Daily execution of interbank Murabaha and Wakala supports funding, balance‑sheet resilience and steady income generation.

Digital Banking Delivery

Operate mobile, online and API channels to deliver seamless banking across platforms, improving UX, security and uptime; in 2024 Qatar internet penetration reached about 99%, enabling broad digital reach. Drive straight-through processing and eKYC to cut onboarding times and transaction friction. Use analytics to personalize offers, boost conversion and lower drop-off.

- Channels: mobile, online, APIs

- Processes: STP, eKYC

- Focus: UX, security, analytics

Risk and Compliance

Credit, market, operational and Shariah risk frameworks govern Qatar Islamic Bank’s underwriting, trading and product approvals, aligned to Basel III minimum CET1 of 4.5% and international Shariah standards. AML, sanctions screening and Qatar data protection rules are embedded across onboarding and transaction monitoring, meeting FATF-based controls. Regular stress tests and limits maintain capital buffers above regulatory minima; continuous audit and model validation ensure adherence.

- Risk coverage: credit, market, operational, Shariah

- Regulatory anchors: Basel III CET1 4.5%

- Controls: AML, sanctions, data privacy (Qatar rules, FATF-aligned)

- Safeguards: stress tests, limits, continuous audit

Shariah finance origination: Murabaha, Ijara, digital STP and QAR 65bn deposits

Origination and underwriting of Murabaha, Ijara, Istisna and Mudaraba with strict Shariah workflows, custody and portfolio monitoring across retail, corporate and project finance.

Grow current, savings and investment accounts under profit‑sharing; deposits QAR 65bn (2024) to optimize funding mix and margins.

Treasury manages Sukuk, interbank Murabaha/Wakala and maintains LCR/NSFR above 100% for liquidity resilience.

Operate mobile, online and API channels; Qatar internet penetration ~99% (2024) to drive STP, eKYC and analytics.

| Metric | Value (2024) |

|---|---|

| Deposits | QAR 65bn |

| LCR / NSFR | >=100% |

| Internet penetration | ~99% |

| Regulatory CET1 min | 4.5% |

Preview Before You Purchase

Business Model Canvas

The Qatar Islamic Bank Business Model Canvas you’re previewing is the actual deliverable, not a mockup. It’s a direct snapshot of the full document you’ll receive after purchase. Upon buying, you’ll immediately download the same editable file, formatted and ready to use in Word and Excel. No placeholders, no surprises—what you see is what you get.