QS Communications Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

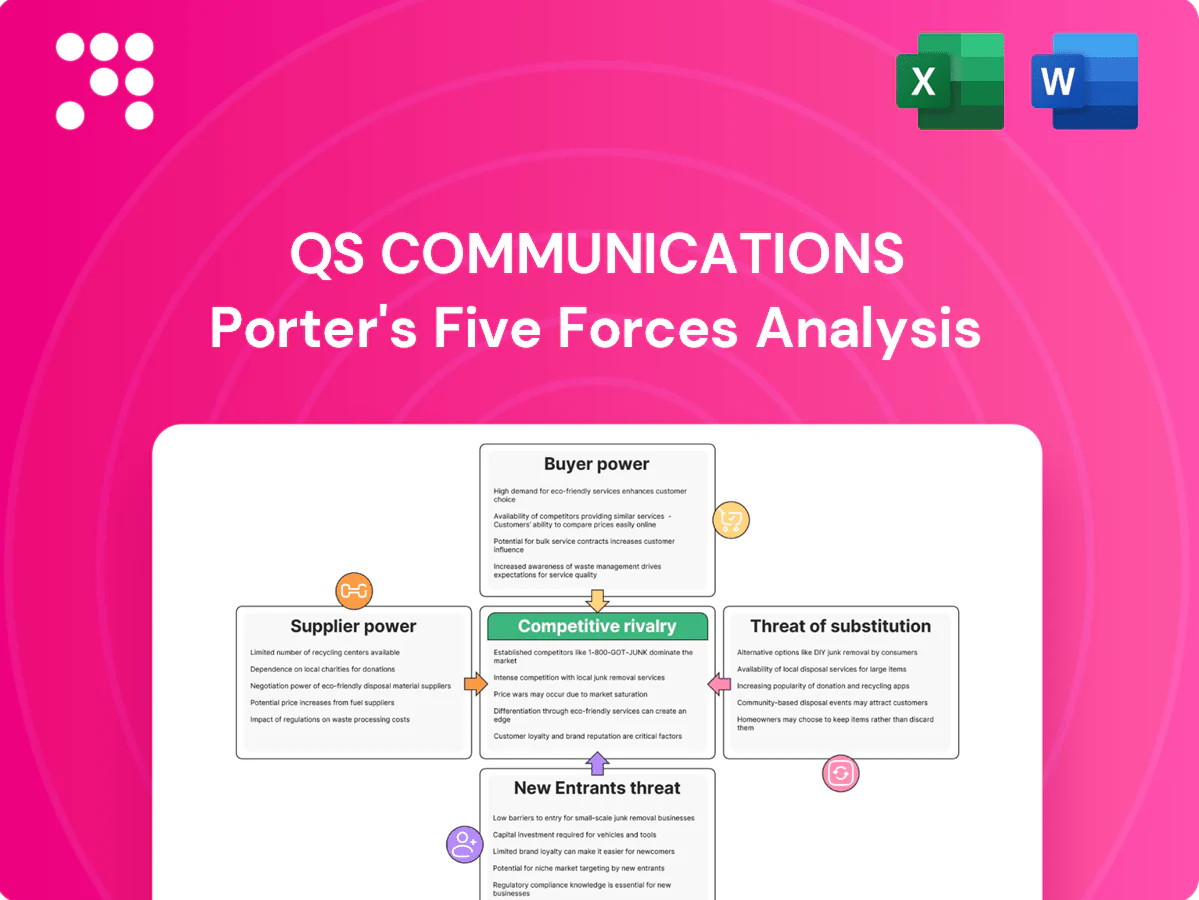

QS Communications faces shifting buyer and supplier leverage, evolving substitute threats, and moderate entry barriers that together shape its competitive outlook; this snapshot highlights key pressures but omits force-by-force ratings and strategic implications. Unlock the full Porter's Five Forces Analysis to trace competitive intensity, quantify risks, and equip decisions with actionable insights.

Suppliers Bargaining Power

Supplier Power 1

QSC depends on hyperscalers and SAP, with 2024 cloud market shares roughly AWS 32%, Microsoft Azure 23% and Google Cloud 11%, giving those suppliers strong pricing and contractual leverage. Partner tiers and certification rules impose revenue commitments and training costs that can squeeze margins. Multi-cloud and vendor diversification mitigate single-supplier dependence. Long-term alliances deliver MDFs, discounts and joint go-to-market programs that partly offset supplier power.

Supplier Power 2

Cybersecurity vendors (Microsoft, CrowdStrike, Palo Alto) remain concentrated and largely subscription-based, with the global cybersecurity market at about $217 billion in 2024; bundled licenses, feature roadmaps, and annual price uplifts can compress QSC’s service margins. Standardized APIs and mature open-source tools (e.g., Zeek, Suricata) give QSC negotiation leverage. Enterprise certifications and SLA-backed support make large account switching costly and slow.

Supplier Power 3

Talent is a critical supplier for QS Communications: scarce SAP, cloud and security specialists pushed average IT salary growth toward 8–10% in 2023–24, driving wage inflation and higher delivery costs. Tight German/EU labor markets raised annual tech attrition to roughly 12–15%, increasing recruitment and transition expenses. Nearshore and offshore partners can expand capacity and cut unit costs by 20–40% versus onshore rates. Strong employer branding and structured training pipelines reduce human-capital supplier power and lower churn.

Supplier Power 4

Data center colocation, connectivity and telecom carriers drive QS Communications costs and SLA performance; location constraints and migration risks keep supplier power elevated despite alternative providers. Energy price volatility in Europe continues to pass through to hosting costs, pressuring margins. Tiered SLAs and a multi-site footprint improve negotiation leverage and resilience.

- Colocation and carrier dependence limits switching

- Location and migration risk sustain supplier leverage

- Energy volatility feeds hosting cost pass-through

- Tiered SLAs + multi-site reduce supplier power

Supplier Power 5

- Recurring audit costs

- Certification-dependent pricing 5-15%

- Process rigidity from renewals

- Compliance as sales enabler

Hyperscaler power, talent inflation and attrition squeeze margins; nearshore and certs mitigate

QSC faces high supplier power from hyperscalers (2024 market shares: AWS 32%, Azure 23%, Google 11%) and concentrated cybersecurity vendors (global market ~$217B in 2024), while talent wage inflation (8–10% in 2023–24) and 12–15% tech attrition raise delivery costs; multi-cloud, nearshore (20–40% cost savings) and certifications (5–15% premium; certification market +6% in 2024) partially offset pressure.

| Metric | 2024 / range |

|---|---|

| Hyperscaler share | AWS 32%, Azure 23%, GCP 11% |

| Cybersecurity market | $217B |

| IT salary growth | 8–10% |

| Attrition | 12–15% |

| Nearshore saving | 20–40% |

| Certification premium | 5–15% (market +6%) |

What is included in the product

Provides a tailored Porter's Five Forces assessment for QS Communications, uncovering competitive intensity, buyer and supplier power, threat of substitutes, and barriers to entry. Includes strategic commentary on disruptive forces, market dynamics, and implications for pricing, profitability, and growth opportunities.

A one-sheet Porter's Five Forces summary tailored for QS Communications—perfect for quick strategic decisions, investor updates, and calming stakeholder concerns.

Customers Bargaining Power

Buyer Power 1

SME customers are highly fragmented (SMEs ~99% of firms in the EU) and price-sensitive, with surveys showing ~65% cite cost as the top selection factor, increasing comparison shopping. For commoditized cloud and managed services switching costs are moderate, keeping pricing pressure as the global public cloud market neared $600B in 2024. Integrated SAP and security ops create strong lock-in—ERP migrations often cost hundreds of thousands and average SOC contract tenures ~3 years—raising exit barriers. Clear SLAs and outcome-based pricing (adoption ~28% in managed services 2024) can rebalance buyer leverage.

Buyer Power 2

Many SMEs drive Buyer Power 2 via competitive tenders and framework agreements, commonly seeking discounts of 20–40% on communications and cloud services; 2024 benchmarks show transparent cloud pricing narrows vendors' margin flexibility. Bundled services and multi-year deals (typical terms 24–36 months) trade lower price for stickiness, while clear value on compliance, 99.9%+ uptime and measurable business outcomes shifts negotiations away from pure price.

Buyer Power 3

Buyers can insource selective capabilities or co-source to retain control, pressuring vendors as internal IT often handles L1/L2 tasks and squeezes external scope and rates. QSC can defend share by offering specialized expertise in SAP migrations and security operations plus guaranteed 24/7 coverage. Co-managed models align incentives, reduce churn, and make switches costlier for buyers.

Buyer Power 4

Buyers face many alternatives as global integrators and local MSPs expanded offerings in 2024, with the managed services market surpassing $250B, enabling easy switch options. Side-by-side pilots and PoCs—used by roughly 70% of enterprises in 2024—permit low‑risk experimentation before full awards. Strong referenceability, vertical templates, and rapid time‑to‑value often neutralize cheaper quotes, while land‑and‑expand motions reduce initial buyer leverage on enterprise deals.

- Alternatives: global integrators + local MSPs

- PoCs: ~70% enterprise adoption in 2024

- Neutralizers: references, vertical templates, fast ROI

- Sales motion: land‑and‑expand reduces upfront buyer leverage

Buyer Power 5

Rising expectations for cybersecurity, compliance and AI/automation are increasing buyer evaluation rigor, with IDC projecting global security spending of about $188 billion in 2024; customers now require measurable KPIs, financial penalties and continuous optimization across service contracts. QS Communications can align value by embedding shared-savings models or performance bonuses and offering robust reporting and governance to reduce mid-contract renegotiation pressure.

- Buyer focus: measurable KPIs

- Contractual levers: financial penalties, performance bonuses

- Value alignment: shared-savings models

- Risk mitigation: robust reporting & governance

SME cost pressure vs ERP lock‑in: PoCs and $250B services widen options

SME buyers (~99% of EU firms) are fragmented and price‑sensitive; ~65% cite cost as top factor, driving discounting. Moderate switching costs for cloud keep pressure, but ERP/SOC lock‑in (SAP migrations costly; SOC avg tenure ~3 yrs) raises exit barriers. PoCs (~70% adoption) and a $250B+ managed services market (2024) increase alternative options but strong references/verticals reduce pure price leverage.

| Metric | 2024 | Impact |

|---|---|---|

| SME share EU | ~99% | Fragmentation |

| Cost as top factor | ~65% | Price pressure |

| PoC adoption | ~70% | Low‑risk switching |

| Managed services market | $250B+ | More suppliers |

Same Document Delivered

QS Communications Porter's Five Forces Analysis

This preview displays the exact QS Communications Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is complete, professionally formatted, and ready for download and use the moment you buy. What you see here is precisely the deliverable you'll get.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

QS Communications faces shifting buyer and supplier leverage, evolving substitute threats, and moderate entry barriers that together shape its competitive outlook; this snapshot highlights key pressures but omits force-by-force ratings and strategic implications. Unlock the full Porter's Five Forces Analysis to trace competitive intensity, quantify risks, and equip decisions with actionable insights.

Suppliers Bargaining Power

Supplier Power 1

QSC depends on hyperscalers and SAP, with 2024 cloud market shares roughly AWS 32%, Microsoft Azure 23% and Google Cloud 11%, giving those suppliers strong pricing and contractual leverage. Partner tiers and certification rules impose revenue commitments and training costs that can squeeze margins. Multi-cloud and vendor diversification mitigate single-supplier dependence. Long-term alliances deliver MDFs, discounts and joint go-to-market programs that partly offset supplier power.

Supplier Power 2

Cybersecurity vendors (Microsoft, CrowdStrike, Palo Alto) remain concentrated and largely subscription-based, with the global cybersecurity market at about $217 billion in 2024; bundled licenses, feature roadmaps, and annual price uplifts can compress QSC’s service margins. Standardized APIs and mature open-source tools (e.g., Zeek, Suricata) give QSC negotiation leverage. Enterprise certifications and SLA-backed support make large account switching costly and slow.

Supplier Power 3

Talent is a critical supplier for QS Communications: scarce SAP, cloud and security specialists pushed average IT salary growth toward 8–10% in 2023–24, driving wage inflation and higher delivery costs. Tight German/EU labor markets raised annual tech attrition to roughly 12–15%, increasing recruitment and transition expenses. Nearshore and offshore partners can expand capacity and cut unit costs by 20–40% versus onshore rates. Strong employer branding and structured training pipelines reduce human-capital supplier power and lower churn.

Supplier Power 4

Data center colocation, connectivity and telecom carriers drive QS Communications costs and SLA performance; location constraints and migration risks keep supplier power elevated despite alternative providers. Energy price volatility in Europe continues to pass through to hosting costs, pressuring margins. Tiered SLAs and a multi-site footprint improve negotiation leverage and resilience.

- Colocation and carrier dependence limits switching

- Location and migration risk sustain supplier leverage

- Energy volatility feeds hosting cost pass-through

- Tiered SLAs + multi-site reduce supplier power

Supplier Power 5

- Recurring audit costs

- Certification-dependent pricing 5-15%

- Process rigidity from renewals

- Compliance as sales enabler

Hyperscaler power, talent inflation and attrition squeeze margins; nearshore and certs mitigate

QSC faces high supplier power from hyperscalers (2024 market shares: AWS 32%, Azure 23%, Google 11%) and concentrated cybersecurity vendors (global market ~$217B in 2024), while talent wage inflation (8–10% in 2023–24) and 12–15% tech attrition raise delivery costs; multi-cloud, nearshore (20–40% cost savings) and certifications (5–15% premium; certification market +6% in 2024) partially offset pressure.

| Metric | 2024 / range |

|---|---|

| Hyperscaler share | AWS 32%, Azure 23%, GCP 11% |

| Cybersecurity market | $217B |

| IT salary growth | 8–10% |

| Attrition | 12–15% |

| Nearshore saving | 20–40% |

| Certification premium | 5–15% (market +6%) |

What is included in the product

Provides a tailored Porter's Five Forces assessment for QS Communications, uncovering competitive intensity, buyer and supplier power, threat of substitutes, and barriers to entry. Includes strategic commentary on disruptive forces, market dynamics, and implications for pricing, profitability, and growth opportunities.

A one-sheet Porter's Five Forces summary tailored for QS Communications—perfect for quick strategic decisions, investor updates, and calming stakeholder concerns.

Customers Bargaining Power

Buyer Power 1

SME customers are highly fragmented (SMEs ~99% of firms in the EU) and price-sensitive, with surveys showing ~65% cite cost as the top selection factor, increasing comparison shopping. For commoditized cloud and managed services switching costs are moderate, keeping pricing pressure as the global public cloud market neared $600B in 2024. Integrated SAP and security ops create strong lock-in—ERP migrations often cost hundreds of thousands and average SOC contract tenures ~3 years—raising exit barriers. Clear SLAs and outcome-based pricing (adoption ~28% in managed services 2024) can rebalance buyer leverage.

Buyer Power 2

Many SMEs drive Buyer Power 2 via competitive tenders and framework agreements, commonly seeking discounts of 20–40% on communications and cloud services; 2024 benchmarks show transparent cloud pricing narrows vendors' margin flexibility. Bundled services and multi-year deals (typical terms 24–36 months) trade lower price for stickiness, while clear value on compliance, 99.9%+ uptime and measurable business outcomes shifts negotiations away from pure price.

Buyer Power 3

Buyers can insource selective capabilities or co-source to retain control, pressuring vendors as internal IT often handles L1/L2 tasks and squeezes external scope and rates. QSC can defend share by offering specialized expertise in SAP migrations and security operations plus guaranteed 24/7 coverage. Co-managed models align incentives, reduce churn, and make switches costlier for buyers.

Buyer Power 4

Buyers face many alternatives as global integrators and local MSPs expanded offerings in 2024, with the managed services market surpassing $250B, enabling easy switch options. Side-by-side pilots and PoCs—used by roughly 70% of enterprises in 2024—permit low‑risk experimentation before full awards. Strong referenceability, vertical templates, and rapid time‑to‑value often neutralize cheaper quotes, while land‑and‑expand motions reduce initial buyer leverage on enterprise deals.

- Alternatives: global integrators + local MSPs

- PoCs: ~70% enterprise adoption in 2024

- Neutralizers: references, vertical templates, fast ROI

- Sales motion: land‑and‑expand reduces upfront buyer leverage

Buyer Power 5

Rising expectations for cybersecurity, compliance and AI/automation are increasing buyer evaluation rigor, with IDC projecting global security spending of about $188 billion in 2024; customers now require measurable KPIs, financial penalties and continuous optimization across service contracts. QS Communications can align value by embedding shared-savings models or performance bonuses and offering robust reporting and governance to reduce mid-contract renegotiation pressure.

- Buyer focus: measurable KPIs

- Contractual levers: financial penalties, performance bonuses

- Value alignment: shared-savings models

- Risk mitigation: robust reporting & governance

SME cost pressure vs ERP lock‑in: PoCs and $250B services widen options

SME buyers (~99% of EU firms) are fragmented and price‑sensitive; ~65% cite cost as top factor, driving discounting. Moderate switching costs for cloud keep pressure, but ERP/SOC lock‑in (SAP migrations costly; SOC avg tenure ~3 yrs) raises exit barriers. PoCs (~70% adoption) and a $250B+ managed services market (2024) increase alternative options but strong references/verticals reduce pure price leverage.

| Metric | 2024 | Impact |

|---|---|---|

| SME share EU | ~99% | Fragmentation |

| Cost as top factor | ~65% | Price pressure |

| PoC adoption | ~70% | Low‑risk switching |

| Managed services market | $250B+ | More suppliers |

Same Document Delivered

QS Communications Porter's Five Forces Analysis

This preview displays the exact QS Communications Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is complete, professionally formatted, and ready for download and use the moment you buy. What you see here is precisely the deliverable you'll get.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

QS Communications faces shifting buyer and supplier leverage, evolving substitute threats, and moderate entry barriers that together shape its competitive outlook; this snapshot highlights key pressures but omits force-by-force ratings and strategic implications. Unlock the full Porter's Five Forces Analysis to trace competitive intensity, quantify risks, and equip decisions with actionable insights.

Suppliers Bargaining Power

Supplier Power 1

QSC depends on hyperscalers and SAP, with 2024 cloud market shares roughly AWS 32%, Microsoft Azure 23% and Google Cloud 11%, giving those suppliers strong pricing and contractual leverage. Partner tiers and certification rules impose revenue commitments and training costs that can squeeze margins. Multi-cloud and vendor diversification mitigate single-supplier dependence. Long-term alliances deliver MDFs, discounts and joint go-to-market programs that partly offset supplier power.

Supplier Power 2

Cybersecurity vendors (Microsoft, CrowdStrike, Palo Alto) remain concentrated and largely subscription-based, with the global cybersecurity market at about $217 billion in 2024; bundled licenses, feature roadmaps, and annual price uplifts can compress QSC’s service margins. Standardized APIs and mature open-source tools (e.g., Zeek, Suricata) give QSC negotiation leverage. Enterprise certifications and SLA-backed support make large account switching costly and slow.

Supplier Power 3

Talent is a critical supplier for QS Communications: scarce SAP, cloud and security specialists pushed average IT salary growth toward 8–10% in 2023–24, driving wage inflation and higher delivery costs. Tight German/EU labor markets raised annual tech attrition to roughly 12–15%, increasing recruitment and transition expenses. Nearshore and offshore partners can expand capacity and cut unit costs by 20–40% versus onshore rates. Strong employer branding and structured training pipelines reduce human-capital supplier power and lower churn.

Supplier Power 4

Data center colocation, connectivity and telecom carriers drive QS Communications costs and SLA performance; location constraints and migration risks keep supplier power elevated despite alternative providers. Energy price volatility in Europe continues to pass through to hosting costs, pressuring margins. Tiered SLAs and a multi-site footprint improve negotiation leverage and resilience.

- Colocation and carrier dependence limits switching

- Location and migration risk sustain supplier leverage

- Energy volatility feeds hosting cost pass-through

- Tiered SLAs + multi-site reduce supplier power

Supplier Power 5

- Recurring audit costs

- Certification-dependent pricing 5-15%

- Process rigidity from renewals

- Compliance as sales enabler

Hyperscaler power, talent inflation and attrition squeeze margins; nearshore and certs mitigate

QSC faces high supplier power from hyperscalers (2024 market shares: AWS 32%, Azure 23%, Google 11%) and concentrated cybersecurity vendors (global market ~$217B in 2024), while talent wage inflation (8–10% in 2023–24) and 12–15% tech attrition raise delivery costs; multi-cloud, nearshore (20–40% cost savings) and certifications (5–15% premium; certification market +6% in 2024) partially offset pressure.

| Metric | 2024 / range |

|---|---|

| Hyperscaler share | AWS 32%, Azure 23%, GCP 11% |

| Cybersecurity market | $217B |

| IT salary growth | 8–10% |

| Attrition | 12–15% |

| Nearshore saving | 20–40% |

| Certification premium | 5–15% (market +6%) |

What is included in the product

Provides a tailored Porter's Five Forces assessment for QS Communications, uncovering competitive intensity, buyer and supplier power, threat of substitutes, and barriers to entry. Includes strategic commentary on disruptive forces, market dynamics, and implications for pricing, profitability, and growth opportunities.

A one-sheet Porter's Five Forces summary tailored for QS Communications—perfect for quick strategic decisions, investor updates, and calming stakeholder concerns.

Customers Bargaining Power

Buyer Power 1

SME customers are highly fragmented (SMEs ~99% of firms in the EU) and price-sensitive, with surveys showing ~65% cite cost as the top selection factor, increasing comparison shopping. For commoditized cloud and managed services switching costs are moderate, keeping pricing pressure as the global public cloud market neared $600B in 2024. Integrated SAP and security ops create strong lock-in—ERP migrations often cost hundreds of thousands and average SOC contract tenures ~3 years—raising exit barriers. Clear SLAs and outcome-based pricing (adoption ~28% in managed services 2024) can rebalance buyer leverage.

Buyer Power 2

Many SMEs drive Buyer Power 2 via competitive tenders and framework agreements, commonly seeking discounts of 20–40% on communications and cloud services; 2024 benchmarks show transparent cloud pricing narrows vendors' margin flexibility. Bundled services and multi-year deals (typical terms 24–36 months) trade lower price for stickiness, while clear value on compliance, 99.9%+ uptime and measurable business outcomes shifts negotiations away from pure price.

Buyer Power 3

Buyers can insource selective capabilities or co-source to retain control, pressuring vendors as internal IT often handles L1/L2 tasks and squeezes external scope and rates. QSC can defend share by offering specialized expertise in SAP migrations and security operations plus guaranteed 24/7 coverage. Co-managed models align incentives, reduce churn, and make switches costlier for buyers.

Buyer Power 4

Buyers face many alternatives as global integrators and local MSPs expanded offerings in 2024, with the managed services market surpassing $250B, enabling easy switch options. Side-by-side pilots and PoCs—used by roughly 70% of enterprises in 2024—permit low‑risk experimentation before full awards. Strong referenceability, vertical templates, and rapid time‑to‑value often neutralize cheaper quotes, while land‑and‑expand motions reduce initial buyer leverage on enterprise deals.

- Alternatives: global integrators + local MSPs

- PoCs: ~70% enterprise adoption in 2024

- Neutralizers: references, vertical templates, fast ROI

- Sales motion: land‑and‑expand reduces upfront buyer leverage

Buyer Power 5

Rising expectations for cybersecurity, compliance and AI/automation are increasing buyer evaluation rigor, with IDC projecting global security spending of about $188 billion in 2024; customers now require measurable KPIs, financial penalties and continuous optimization across service contracts. QS Communications can align value by embedding shared-savings models or performance bonuses and offering robust reporting and governance to reduce mid-contract renegotiation pressure.

- Buyer focus: measurable KPIs

- Contractual levers: financial penalties, performance bonuses

- Value alignment: shared-savings models

- Risk mitigation: robust reporting & governance

SME cost pressure vs ERP lock‑in: PoCs and $250B services widen options

SME buyers (~99% of EU firms) are fragmented and price‑sensitive; ~65% cite cost as top factor, driving discounting. Moderate switching costs for cloud keep pressure, but ERP/SOC lock‑in (SAP migrations costly; SOC avg tenure ~3 yrs) raises exit barriers. PoCs (~70% adoption) and a $250B+ managed services market (2024) increase alternative options but strong references/verticals reduce pure price leverage.

| Metric | 2024 | Impact |

|---|---|---|

| SME share EU | ~99% | Fragmentation |

| Cost as top factor | ~65% | Price pressure |

| PoC adoption | ~70% | Low‑risk switching |

| Managed services market | $250B+ | More suppliers |

Same Document Delivered

QS Communications Porter's Five Forces Analysis

This preview displays the exact QS Communications Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is complete, professionally formatted, and ready for download and use the moment you buy. What you see here is precisely the deliverable you'll get.