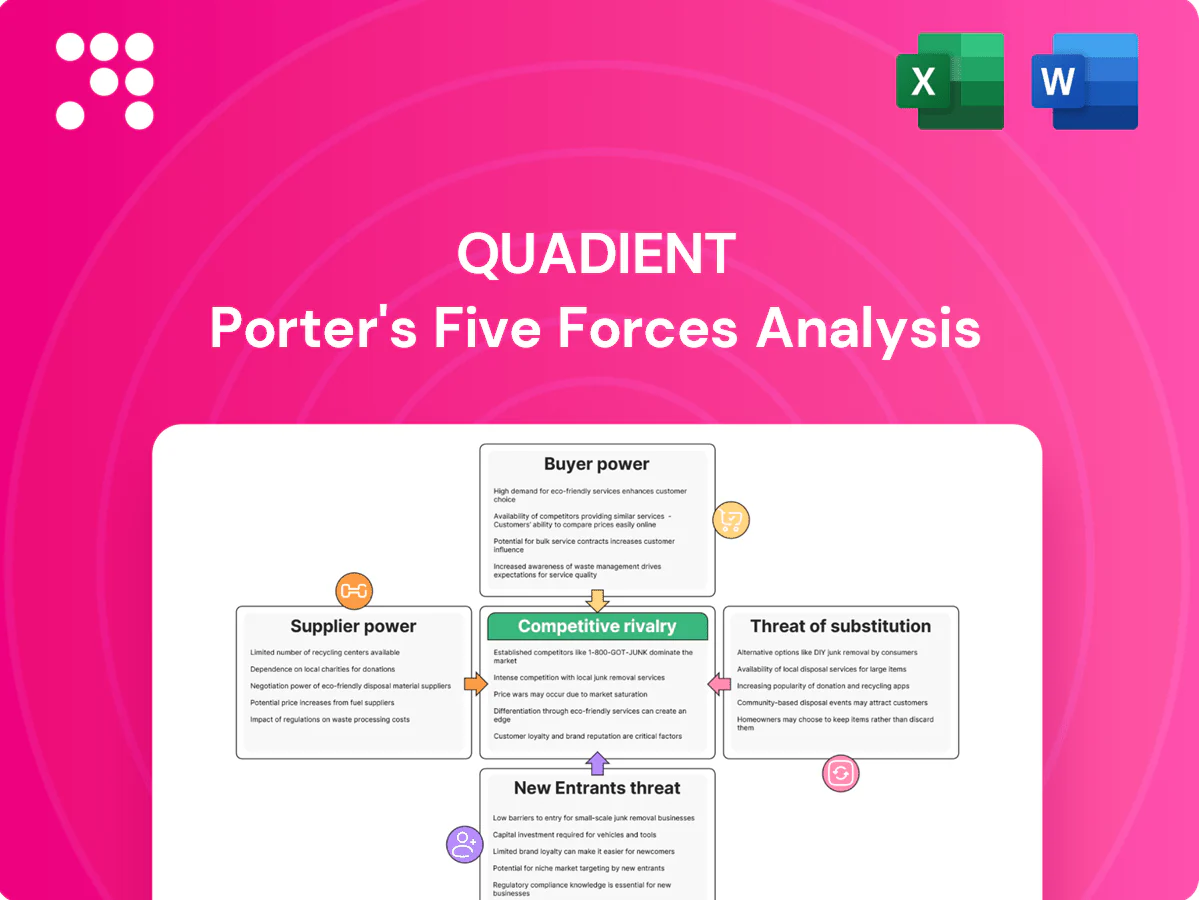

Quadient Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Quadient faces moderate buyer power, evolving substitute threats from digital workflows, and competitive pressure from niche fintech and postal automation players; supplier leverage and regulatory shifts further shape its margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Quadient’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Cloud and data center reliance

Quadient’s SaaS and CCM workloads rely on hyperscalers for compute, storage and security certifications (ISO 27001, SOC 2), concentrating power: AWS ~32%, Microsoft Azure ~24%, Google Cloud ~11% (Canalys, 2024). A small provider set drives pricing, roadmap influence and service levels. Switching clouds requires costly re-architecture and compliance revalidation, raising input costs or forcing restrictive contract terms.

Hardware and components for lockers

Parcel lockers depend on steel, electronics, IoT modules and custom firmware from specialized suppliers; electronics lead times commonly exceed 12 weeks in 2024 and steel/component price swings raise input costs. Design-specific parts and certification make qualifying alternates nontrivial, extending validation cycles by months. Suppliers can therefore delay delivery and compress margins, often impacting gross margins by roughly 5–10% in project phases.

Software tooling and IP licensors

Core Quadient platforms depend on databases, analytics engines and licensed libraries, and heavy use of security/compliance modules ties integrations to specific partners. Vendor lock-ins and usage-based pricing commonly raise COGS as volumes scale, with many SaaS companies reporting 20–40% higher variable licensing spend. Renegotiations often face take-it-or-leave-it constraints, limiting margin leverage.

Field installers and service partners

Locker deployments require certified installers, logistics and maintenance crews; in 2024 installer shortages pushed lead times in some European and North American markets to 4–8 weeks, increasing local labour rates by double digits. Variability in partner performance directly risks meeting SLAs for end clients, and this intermediation grants service partners clear negotiating leverage over pricing and scheduling.

- Certified installer scarcity: 4–8 week lead times (2024)

- Impact: double-digit local labour rate increases

- Risk: SLA breaches from performance variability

Postal equipment and consumables

Postal equipment and consumables for Quadient must use approved parts, inks and meters to meet postal regulations, which in 2024 still force re-approval cycles of roughly 3–9 months and costs commonly in the $10k–$100k range, limiting alternate sourcing and consolidating supplier influence; certified consumables carry a typical 10–30% premium, embedding supplier margin.

- Regulatory re-approval: 3–9 months, $10k–$100k

- Consumable premium: 10–30%

- Supplier leverage: high due to certification barriers

Hyperscaler lock-in causes >12wk lead times and 5–10% margin squeeze

Quadient faces concentrated supplier power: hyperscalers (AWS 32%, Azure 24%, GCP 11% in 2024) create lock-in, costly cloud re-architecture and higher COGS. Parcel/electronics suppliers have >12 week lead times and can swing input costs, squeezing project margins ~5–10%. Certified installers, long re-approval cycles (3–9 months) and consumable premiums (10–30%) add negotiating leverage.

| Item | 2024 metric |

|---|---|

| Hyperscalers share | AWS 32% / Azure 24% / GCP 11% |

| Electronics lead time | >12 weeks |

| Installer lead time | 4–8 weeks |

| Re-approval cycle | 3–9 months |

| Consumable premium | 10–30% |

| Project margin impact | ~5–10% |

What is included in the product

Concise Porter's Five Forces analysis tailored for Quadient that uncovers competitive intensity, buyer and supplier power, entry barriers and substitute threats, with strategic commentary on disruptive trends and market positioning; fully editable for reports and pitch decks.

One-sheet Porter's Five Forces for Quadient that lets you tweak force intensities by scenario, produce an instant spider chart for strategic clarity, and copy straight into decks or reports—no macros or finance expertise needed.

Customers Bargaining Power

Enterprise procurement and RFPs

Enterprise procurement in financial services, healthcare and government is driven by rigorous tenders and public procurement that represents about 12% of EU GDP (European Commission, 2024), giving buyers strong leverage. Standardized scoring and multi-vendor bids compress pricing and margin in Quadient deals. Customers demand audits, 99.9% uptime SLAs and penalty clauses that shift operational risk to vendors. Volume commitments are exchanged for discounts and bespoke SLAs to secure large contracts.

Switching costs vary by product

CCM integrations and bespoke workflows create moderate-to-high switching costs, often locking customers into multi-year contracts and integrations that can take 6–18 months to replace. Locker fleets and site build-outs deepen capital and process lock-in, with per-site CAPEX commonly in the hundreds of thousands of dollars. Conversely, basic mail solutions remain commoditized with lower stickiness. Buyers exploit this variance to negotiate pricing and service terms.

Demand for compliance and security

Customers in finance, healthcare and government increasingly require SOC 2/ISO attestations and HIPAA/GDPR features to qualify vendors. Buyers commonly use compliance gaps to extract price concessions or roadmap commitments. Ongoing audit support raises costs—SOC 2 audits typically range $20k–$200k—and non‑compliance risks (HIPAA fines up to $1.5M/yr, GDPR fines up to €20M or 4% turnover) strengthen buyer veto power.

Multi-year contracts and scalability

Large customers demand tiered pricing by volume and geography, frequently trading upsell potential for price caps; renewals and multi-year contract renegotiations repeatedly reset Quadients deal economics as buyers aggressively benchmark peers to extract value.

- Tiered pricing linked to volume/geography

- Upsell often exchanged for price caps

- Renewals reset economics

- Buyers benchmark peers to push pricing

Alternative solutions knowledge

By 2024 customers enter CCM procurements already versed in CCM, BPA and locker alternatives, running POCs with rivals to extract better pricing and features; referenceability and clear ROI proofs are treated as mandatory buying criteria, increasing negotiation leverage. Information symmetry across vendors elevates buyer power and compresses vendor margins.

- POC pressure

- ROI mandatory

- High information symmetry

Procurement leverage, compliance and lock-ins squeeze pricing while CCM drives deal stickiness

Enterprise procurement (12% of EU GDP, European Commission 2024) and standardized tenders give buyers high leverage, compressing Quadient pricing and margins. CCM integrations and locker CAPEX (per-site hundreds of thousands) create 6–18 month switching costs that raise stickiness for complex deals but leave basic mail commoditized. Compliance demands (SOC 2 $20k–$200k, GDPR fines up to €20M/4% turnover, HIPAA ~$1.5M/yr) amplify buyer veto power. Renewals and tiered-volume pricing repeatedly reset deal economics as customers use POCs and ROI proof to extract concessions.

| Metric | 2024 Value |

|---|---|

| EU public procurement share | ~12% GDP |

| SOC 2 audit cost | $20k–$200k |

| GDPR max fine | €20M or 4% turnover |

| Switching time (CCM) | 6–18 months |

| Per-site CAPEX (lockers) | hundreds of thousands |

Preview Before You Purchase

Quadient Porter's Five Forces Analysis

This preview shows the exact Quadient Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted and ready to use upon download. You're viewing the final deliverable, identical to the file you'll get after payment.

A Must-Have Tool for Decision-Makers

Quadient faces moderate buyer power, evolving substitute threats from digital workflows, and competitive pressure from niche fintech and postal automation players; supplier leverage and regulatory shifts further shape its margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Quadient’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Cloud and data center reliance

Quadient’s SaaS and CCM workloads rely on hyperscalers for compute, storage and security certifications (ISO 27001, SOC 2), concentrating power: AWS ~32%, Microsoft Azure ~24%, Google Cloud ~11% (Canalys, 2024). A small provider set drives pricing, roadmap influence and service levels. Switching clouds requires costly re-architecture and compliance revalidation, raising input costs or forcing restrictive contract terms.

Hardware and components for lockers

Parcel lockers depend on steel, electronics, IoT modules and custom firmware from specialized suppliers; electronics lead times commonly exceed 12 weeks in 2024 and steel/component price swings raise input costs. Design-specific parts and certification make qualifying alternates nontrivial, extending validation cycles by months. Suppliers can therefore delay delivery and compress margins, often impacting gross margins by roughly 5–10% in project phases.

Software tooling and IP licensors

Core Quadient platforms depend on databases, analytics engines and licensed libraries, and heavy use of security/compliance modules ties integrations to specific partners. Vendor lock-ins and usage-based pricing commonly raise COGS as volumes scale, with many SaaS companies reporting 20–40% higher variable licensing spend. Renegotiations often face take-it-or-leave-it constraints, limiting margin leverage.

Field installers and service partners

Locker deployments require certified installers, logistics and maintenance crews; in 2024 installer shortages pushed lead times in some European and North American markets to 4–8 weeks, increasing local labour rates by double digits. Variability in partner performance directly risks meeting SLAs for end clients, and this intermediation grants service partners clear negotiating leverage over pricing and scheduling.

- Certified installer scarcity: 4–8 week lead times (2024)

- Impact: double-digit local labour rate increases

- Risk: SLA breaches from performance variability

Postal equipment and consumables

Postal equipment and consumables for Quadient must use approved parts, inks and meters to meet postal regulations, which in 2024 still force re-approval cycles of roughly 3–9 months and costs commonly in the $10k–$100k range, limiting alternate sourcing and consolidating supplier influence; certified consumables carry a typical 10–30% premium, embedding supplier margin.

- Regulatory re-approval: 3–9 months, $10k–$100k

- Consumable premium: 10–30%

- Supplier leverage: high due to certification barriers

Hyperscaler lock-in causes >12wk lead times and 5–10% margin squeeze

Quadient faces concentrated supplier power: hyperscalers (AWS 32%, Azure 24%, GCP 11% in 2024) create lock-in, costly cloud re-architecture and higher COGS. Parcel/electronics suppliers have >12 week lead times and can swing input costs, squeezing project margins ~5–10%. Certified installers, long re-approval cycles (3–9 months) and consumable premiums (10–30%) add negotiating leverage.

| Item | 2024 metric |

|---|---|

| Hyperscalers share | AWS 32% / Azure 24% / GCP 11% |

| Electronics lead time | >12 weeks |

| Installer lead time | 4–8 weeks |

| Re-approval cycle | 3–9 months |

| Consumable premium | 10–30% |

| Project margin impact | ~5–10% |

What is included in the product

Concise Porter's Five Forces analysis tailored for Quadient that uncovers competitive intensity, buyer and supplier power, entry barriers and substitute threats, with strategic commentary on disruptive trends and market positioning; fully editable for reports and pitch decks.

One-sheet Porter's Five Forces for Quadient that lets you tweak force intensities by scenario, produce an instant spider chart for strategic clarity, and copy straight into decks or reports—no macros or finance expertise needed.

Customers Bargaining Power

Enterprise procurement and RFPs

Enterprise procurement in financial services, healthcare and government is driven by rigorous tenders and public procurement that represents about 12% of EU GDP (European Commission, 2024), giving buyers strong leverage. Standardized scoring and multi-vendor bids compress pricing and margin in Quadient deals. Customers demand audits, 99.9% uptime SLAs and penalty clauses that shift operational risk to vendors. Volume commitments are exchanged for discounts and bespoke SLAs to secure large contracts.

Switching costs vary by product

CCM integrations and bespoke workflows create moderate-to-high switching costs, often locking customers into multi-year contracts and integrations that can take 6–18 months to replace. Locker fleets and site build-outs deepen capital and process lock-in, with per-site CAPEX commonly in the hundreds of thousands of dollars. Conversely, basic mail solutions remain commoditized with lower stickiness. Buyers exploit this variance to negotiate pricing and service terms.

Demand for compliance and security

Customers in finance, healthcare and government increasingly require SOC 2/ISO attestations and HIPAA/GDPR features to qualify vendors. Buyers commonly use compliance gaps to extract price concessions or roadmap commitments. Ongoing audit support raises costs—SOC 2 audits typically range $20k–$200k—and non‑compliance risks (HIPAA fines up to $1.5M/yr, GDPR fines up to €20M or 4% turnover) strengthen buyer veto power.

Multi-year contracts and scalability

Large customers demand tiered pricing by volume and geography, frequently trading upsell potential for price caps; renewals and multi-year contract renegotiations repeatedly reset Quadients deal economics as buyers aggressively benchmark peers to extract value.

- Tiered pricing linked to volume/geography

- Upsell often exchanged for price caps

- Renewals reset economics

- Buyers benchmark peers to push pricing

Alternative solutions knowledge

By 2024 customers enter CCM procurements already versed in CCM, BPA and locker alternatives, running POCs with rivals to extract better pricing and features; referenceability and clear ROI proofs are treated as mandatory buying criteria, increasing negotiation leverage. Information symmetry across vendors elevates buyer power and compresses vendor margins.

- POC pressure

- ROI mandatory

- High information symmetry

Procurement leverage, compliance and lock-ins squeeze pricing while CCM drives deal stickiness

Enterprise procurement (12% of EU GDP, European Commission 2024) and standardized tenders give buyers high leverage, compressing Quadient pricing and margins. CCM integrations and locker CAPEX (per-site hundreds of thousands) create 6–18 month switching costs that raise stickiness for complex deals but leave basic mail commoditized. Compliance demands (SOC 2 $20k–$200k, GDPR fines up to €20M/4% turnover, HIPAA ~$1.5M/yr) amplify buyer veto power. Renewals and tiered-volume pricing repeatedly reset deal economics as customers use POCs and ROI proof to extract concessions.

| Metric | 2024 Value |

|---|---|

| EU public procurement share | ~12% GDP |

| SOC 2 audit cost | $20k–$200k |

| GDPR max fine | €20M or 4% turnover |

| Switching time (CCM) | 6–18 months |

| Per-site CAPEX (lockers) | hundreds of thousands |

Preview Before You Purchase

Quadient Porter's Five Forces Analysis

This preview shows the exact Quadient Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted and ready to use upon download. You're viewing the final deliverable, identical to the file you'll get after payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Quadient faces moderate buyer power, evolving substitute threats from digital workflows, and competitive pressure from niche fintech and postal automation players; supplier leverage and regulatory shifts further shape its margins. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Quadient’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Cloud and data center reliance

Quadient’s SaaS and CCM workloads rely on hyperscalers for compute, storage and security certifications (ISO 27001, SOC 2), concentrating power: AWS ~32%, Microsoft Azure ~24%, Google Cloud ~11% (Canalys, 2024). A small provider set drives pricing, roadmap influence and service levels. Switching clouds requires costly re-architecture and compliance revalidation, raising input costs or forcing restrictive contract terms.

Hardware and components for lockers

Parcel lockers depend on steel, electronics, IoT modules and custom firmware from specialized suppliers; electronics lead times commonly exceed 12 weeks in 2024 and steel/component price swings raise input costs. Design-specific parts and certification make qualifying alternates nontrivial, extending validation cycles by months. Suppliers can therefore delay delivery and compress margins, often impacting gross margins by roughly 5–10% in project phases.

Software tooling and IP licensors

Core Quadient platforms depend on databases, analytics engines and licensed libraries, and heavy use of security/compliance modules ties integrations to specific partners. Vendor lock-ins and usage-based pricing commonly raise COGS as volumes scale, with many SaaS companies reporting 20–40% higher variable licensing spend. Renegotiations often face take-it-or-leave-it constraints, limiting margin leverage.

Field installers and service partners

Locker deployments require certified installers, logistics and maintenance crews; in 2024 installer shortages pushed lead times in some European and North American markets to 4–8 weeks, increasing local labour rates by double digits. Variability in partner performance directly risks meeting SLAs for end clients, and this intermediation grants service partners clear negotiating leverage over pricing and scheduling.

- Certified installer scarcity: 4–8 week lead times (2024)

- Impact: double-digit local labour rate increases

- Risk: SLA breaches from performance variability

Postal equipment and consumables

Postal equipment and consumables for Quadient must use approved parts, inks and meters to meet postal regulations, which in 2024 still force re-approval cycles of roughly 3–9 months and costs commonly in the $10k–$100k range, limiting alternate sourcing and consolidating supplier influence; certified consumables carry a typical 10–30% premium, embedding supplier margin.

- Regulatory re-approval: 3–9 months, $10k–$100k

- Consumable premium: 10–30%

- Supplier leverage: high due to certification barriers

Hyperscaler lock-in causes >12wk lead times and 5–10% margin squeeze

Quadient faces concentrated supplier power: hyperscalers (AWS 32%, Azure 24%, GCP 11% in 2024) create lock-in, costly cloud re-architecture and higher COGS. Parcel/electronics suppliers have >12 week lead times and can swing input costs, squeezing project margins ~5–10%. Certified installers, long re-approval cycles (3–9 months) and consumable premiums (10–30%) add negotiating leverage.

| Item | 2024 metric |

|---|---|

| Hyperscalers share | AWS 32% / Azure 24% / GCP 11% |

| Electronics lead time | >12 weeks |

| Installer lead time | 4–8 weeks |

| Re-approval cycle | 3–9 months |

| Consumable premium | 10–30% |

| Project margin impact | ~5–10% |

What is included in the product

Concise Porter's Five Forces analysis tailored for Quadient that uncovers competitive intensity, buyer and supplier power, entry barriers and substitute threats, with strategic commentary on disruptive trends and market positioning; fully editable for reports and pitch decks.

One-sheet Porter's Five Forces for Quadient that lets you tweak force intensities by scenario, produce an instant spider chart for strategic clarity, and copy straight into decks or reports—no macros or finance expertise needed.

Customers Bargaining Power

Enterprise procurement and RFPs

Enterprise procurement in financial services, healthcare and government is driven by rigorous tenders and public procurement that represents about 12% of EU GDP (European Commission, 2024), giving buyers strong leverage. Standardized scoring and multi-vendor bids compress pricing and margin in Quadient deals. Customers demand audits, 99.9% uptime SLAs and penalty clauses that shift operational risk to vendors. Volume commitments are exchanged for discounts and bespoke SLAs to secure large contracts.

Switching costs vary by product

CCM integrations and bespoke workflows create moderate-to-high switching costs, often locking customers into multi-year contracts and integrations that can take 6–18 months to replace. Locker fleets and site build-outs deepen capital and process lock-in, with per-site CAPEX commonly in the hundreds of thousands of dollars. Conversely, basic mail solutions remain commoditized with lower stickiness. Buyers exploit this variance to negotiate pricing and service terms.

Demand for compliance and security

Customers in finance, healthcare and government increasingly require SOC 2/ISO attestations and HIPAA/GDPR features to qualify vendors. Buyers commonly use compliance gaps to extract price concessions or roadmap commitments. Ongoing audit support raises costs—SOC 2 audits typically range $20k–$200k—and non‑compliance risks (HIPAA fines up to $1.5M/yr, GDPR fines up to €20M or 4% turnover) strengthen buyer veto power.

Multi-year contracts and scalability

Large customers demand tiered pricing by volume and geography, frequently trading upsell potential for price caps; renewals and multi-year contract renegotiations repeatedly reset Quadients deal economics as buyers aggressively benchmark peers to extract value.

- Tiered pricing linked to volume/geography

- Upsell often exchanged for price caps

- Renewals reset economics

- Buyers benchmark peers to push pricing

Alternative solutions knowledge

By 2024 customers enter CCM procurements already versed in CCM, BPA and locker alternatives, running POCs with rivals to extract better pricing and features; referenceability and clear ROI proofs are treated as mandatory buying criteria, increasing negotiation leverage. Information symmetry across vendors elevates buyer power and compresses vendor margins.

- POC pressure

- ROI mandatory

- High information symmetry

Procurement leverage, compliance and lock-ins squeeze pricing while CCM drives deal stickiness

Enterprise procurement (12% of EU GDP, European Commission 2024) and standardized tenders give buyers high leverage, compressing Quadient pricing and margins. CCM integrations and locker CAPEX (per-site hundreds of thousands) create 6–18 month switching costs that raise stickiness for complex deals but leave basic mail commoditized. Compliance demands (SOC 2 $20k–$200k, GDPR fines up to €20M/4% turnover, HIPAA ~$1.5M/yr) amplify buyer veto power. Renewals and tiered-volume pricing repeatedly reset deal economics as customers use POCs and ROI proof to extract concessions.

| Metric | 2024 Value |

|---|---|

| EU public procurement share | ~12% GDP |

| SOC 2 audit cost | $20k–$200k |

| GDPR max fine | €20M or 4% turnover |

| Switching time (CCM) | 6–18 months |

| Per-site CAPEX (lockers) | hundreds of thousands |

Preview Before You Purchase

Quadient Porter's Five Forces Analysis

This preview shows the exact Quadient Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted and ready to use upon download. You're viewing the final deliverable, identical to the file you'll get after payment.