Quadient PESTLE Analysis

Skip the Research. Get the Strategy.

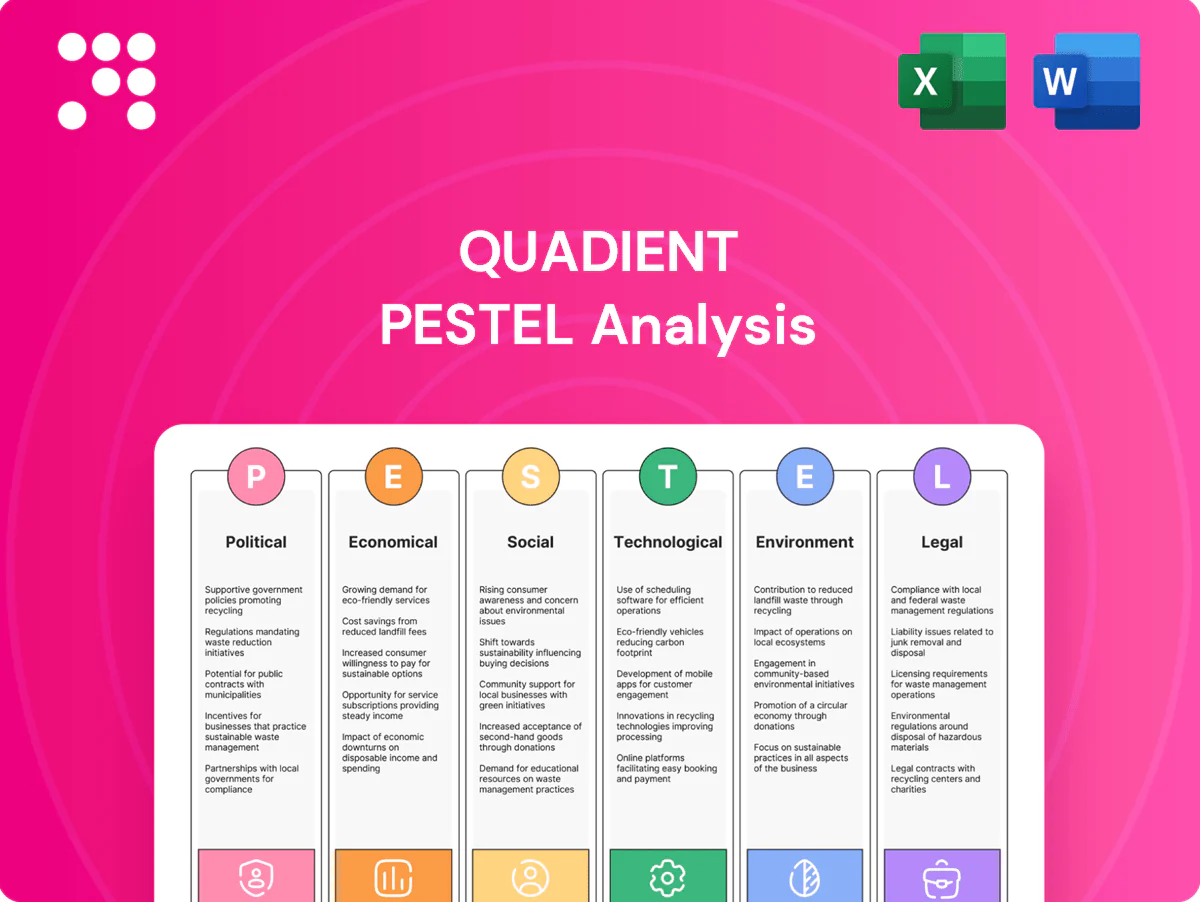

Our PESTLE analysis of Quadient reveals how political regulation, digital transformation, economic cycles, social trends, legal compliance, and environmental pressures converge to shape its strategy and risk profile. Ideal for investors and strategists, this concise overview highlights key external threats and opportunities. Download the full, editable PESTLE now to get the complete, actionable intelligence you need.

Political factors

Public-sector digital transformation agendas

Governments are prioritizing citizen experience, e-invoicing and digitized correspondence, driving demand for CCM and automation; Quadient can align offerings with the EU eIDAS framework (Regulation (EU) No 910/2014) and national digital mail initiatives. EU recovery funding via NextGenerationEU (€750 billion) supports digitization projects and procurement pipelines. Public tenders often take 12–24 months but deliver sticky, multi-year contracts; budget cycles and election outcomes can rephase priorities or timelines.

Data sovereignty and localization policies

With over 60 countries enacting data localization or strict cross-border transfer rules, EU and UK regimes plus regional laws increasingly demand local storage and processing; Quadient’s CCM and parcel‑locker telemetry must offer EU/UK/region hosting options to remain eligible. This drives multi-region cloud architecture, higher infrastructure and compliance costs and narrower vendor choice, and non-compliance can disqualify bids for government or regulated-sector contracts.

Postal sector regulation and modernization

Reforms of national postal services—after letter post volumes have fallen roughly 40% globally since 2000 (UPU)—reshape franking standards and machine certification, forcing Quadient to update mail systems and testing. Quadient (≈€1.04bn revenue in 2024) must track changing tariffs, indicia formats and compliance tests across markets. Government incentives for hybrid mail (subsidies or integration pilots in EU member states) can soften physical-mail decline, while stricter de-mail mandates accelerate substitution.

Trade policy and supply-chain geopolitics

Tariffs on electronics (notably US Section 301 levies of roughly 7.5–25% on many Chinese-made components) raise Quadient parcel-locker BOM costs and compress margins; 2023–24 export controls on advanced semiconductors and sanctions complicate multinational deployments and certifications; political tensions and chokepoint risks have extended logistics lead times by several weeks; diversifying suppliers and nearshoring mitigates exposure.

- Tariff impact: 7.5–25% on many components

- Export controls: 2023–24 semiconductor restrictions

- Logistics: lead times +weeks, higher freight volatility

- Mitigation: supplier diversification, nearshoring

Cybersecurity directives for critical infrastructure

Public and regulated buyers are bound by frameworks such as NIS2 across the 27 EU member states and FedRAMP-style requirements for US federal procurements (FedRAMP mandatory for cloud services since 2014). Quadient must deliver heightened security assurance for CCM platforms and locker networks; achieving certifications often lengthens sales cycles by several months but expands addressable markets. Failure to meet standards can exclude the company from key public procurements.

- Compliance: NIS2 (EU) and FedRAMP (US)

- Impact: longer sales cycles, larger market access

- Risk: exclusion from public tenders if noncompliant

EU €750bn e‑procurement boosts tenders; data localization (60+ countries), tariffs raise costs

Governments push e‑delivery and e‑invoicing (NextGenerationEU €750bn), creating public procurement opportunities; Quadient (≈€1.04bn revenue 2024) benefits from CCM alignment but faces 12–24 month tender cycles. Data localization in 60+ countries forces multi‑region hosting and higher costs; NIS2/FedRAMP raise security certification burdens. Tariffs (7.5–25%) and 2023–24 export controls increase BOM and lead times (~weeks), prompting nearshoring.

| Factor | Impact | 2023–25 data |

|---|---|---|

| Digital govt | Procurement pipelines | NextGenerationEU €750bn; tenders 12–24m |

| Data rules | Hosting cost, bid eligibility | 60+ countries |

| Tariffs/controls | BOM↑, lead times | Tariffs 7.5–25%; lead times +weeks |

| Security regs | Longer sales cycles | NIS2, FedRAMP |

What is included in the product

Explores how external macro-environmental factors uniquely affect Quadient across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section is data-backed, region- and industry-specific, and offers forward-looking insights with actionable implications for executives, investors and strategists.

A concise, visually segmented PESTLE summary of Quadient that’s easy to drop into presentations, share across teams, and annotate for region- or product-specific risks—supporting faster alignment and clearer discussions on external threats and market positioning.

Economic factors

Interest rates and capital spending

Higher policy rates—Fed funds around 5.25–5.50% and the ECB deposit rate near 4% in 2024—have dampened capex for hardware such as parcel lockers and mail equipment, prompting some customers to defer large purchases. Many clients are shifting to SaaS, subscription and leasing models to avoid upfront spend. If rates fall, large rollout programs can restart, and flexible financing solutions help sustain Quadient’s sales pipeline through cycles.

Macro growth and enterprise IT budgets

Economic slowdowns curb discretionary CX and automation budgets, with Gartner estimating global IT spending near $4.9 trillion in 2024 and enterprise software growth around 5% y/y, tightening approvals. Mission-critical compliance communications remain resilient, often prioritized during cuts. Demonstrable ROI—reduced cost-to-serve and faster cash conversion—drives signoffs; land-and-expand sales models preserve growth by converting smaller deployments into broader contracts.

E-commerce parcel volumes and last-mile economics

Rising online retail—global e‑commerce sales estimated at about 6.3 trillion USD in 2024—boosts demand for secure, efficient parcel lockers. Locker networks can cut failed home deliveries by up to 70% and lower last‑mile cost per parcel by roughly 30–50%, improving throughput valued by retailers and multifamily owners. Retail cyclicality can slow or accelerate locker rollouts depending on seasonal and macro retail swings.

Declining traditional mail volumes

Declining traditional mail volumes have eroded legacy franking revenues for Quadient, yet the same digital shift fuels demand for customer communications management and hybrid mail solutions; industry data show letter volumes in many developed markets have fallen roughly 40–50% since the early 2000s, accelerating CCM adoption and managed services purchases.

- Cross-sell automation to existing mail customers offsets revenue decline

- Pricing and service bundling defend margins

- CCM and hybrid mail growth captures digital migration

Currency fluctuations and global footprint

Quadient's multinational footprint exposes reported revenue and component costs to FX swings; in FY2024 (≈€1.1bn revenue) currency translation materially shifted reported growth by an estimated 2–4 percentage points. Dispersion of sourcing and manufacturing across Europe and Asia provides natural hedges and supports pricing localization to reduce volatility. Active hedging programs and centralized treasury policies help stabilize cash flows and limit FX margin erosion.

- FY2024 revenue ≈€1.1bn

- FX translation impact ~2–4 pp

- Sourcing in Europe/Asia = natural hedge

- Pricing localization + hedging = lower volatility

EU €750bn e‑procurement boosts tenders; data localization (60+ countries), tariffs raise costs

Higher policy rates (Fed 5.25–5.50%, ECB ~4% in 2024) depress capex for parcel lockers and mail hardware, shifting customers to SaaS, leasing and deferred purchases. Global e‑commerce (~$6.3T) and IT spend (~$4.9T) sustain locker and CCM demand, while falling letter volumes (down ~40–50% since early 2000s) drive hybrid mail adoption. Quadient FY2024 revenue ≈€1.1bn; FX translation impacted growth ~2–4 pp.

| Metric | Value |

|---|---|

| Fed/ECB rates (2024) | 5.25–5.50% / ~4% |

| Global e‑commerce (2024) | $6.3T |

| Global IT spend (2024) | $4.9T |

| Quadient FY2024 rev | ≈€1.1bn |

| FX impact on growth | ~2–4 pp |

What You See Is What You Get

Quadient PESTLE Analysis

The Quadient PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The preview displays the complete content, structure, and layout with no placeholders. After checkout you’ll instantly download this same professional file.

Skip the Research. Get the Strategy.

Our PESTLE analysis of Quadient reveals how political regulation, digital transformation, economic cycles, social trends, legal compliance, and environmental pressures converge to shape its strategy and risk profile. Ideal for investors and strategists, this concise overview highlights key external threats and opportunities. Download the full, editable PESTLE now to get the complete, actionable intelligence you need.

Political factors

Public-sector digital transformation agendas

Governments are prioritizing citizen experience, e-invoicing and digitized correspondence, driving demand for CCM and automation; Quadient can align offerings with the EU eIDAS framework (Regulation (EU) No 910/2014) and national digital mail initiatives. EU recovery funding via NextGenerationEU (€750 billion) supports digitization projects and procurement pipelines. Public tenders often take 12–24 months but deliver sticky, multi-year contracts; budget cycles and election outcomes can rephase priorities or timelines.

Data sovereignty and localization policies

With over 60 countries enacting data localization or strict cross-border transfer rules, EU and UK regimes plus regional laws increasingly demand local storage and processing; Quadient’s CCM and parcel‑locker telemetry must offer EU/UK/region hosting options to remain eligible. This drives multi-region cloud architecture, higher infrastructure and compliance costs and narrower vendor choice, and non-compliance can disqualify bids for government or regulated-sector contracts.

Postal sector regulation and modernization

Reforms of national postal services—after letter post volumes have fallen roughly 40% globally since 2000 (UPU)—reshape franking standards and machine certification, forcing Quadient to update mail systems and testing. Quadient (≈€1.04bn revenue in 2024) must track changing tariffs, indicia formats and compliance tests across markets. Government incentives for hybrid mail (subsidies or integration pilots in EU member states) can soften physical-mail decline, while stricter de-mail mandates accelerate substitution.

Trade policy and supply-chain geopolitics

Tariffs on electronics (notably US Section 301 levies of roughly 7.5–25% on many Chinese-made components) raise Quadient parcel-locker BOM costs and compress margins; 2023–24 export controls on advanced semiconductors and sanctions complicate multinational deployments and certifications; political tensions and chokepoint risks have extended logistics lead times by several weeks; diversifying suppliers and nearshoring mitigates exposure.

- Tariff impact: 7.5–25% on many components

- Export controls: 2023–24 semiconductor restrictions

- Logistics: lead times +weeks, higher freight volatility

- Mitigation: supplier diversification, nearshoring

Cybersecurity directives for critical infrastructure

Public and regulated buyers are bound by frameworks such as NIS2 across the 27 EU member states and FedRAMP-style requirements for US federal procurements (FedRAMP mandatory for cloud services since 2014). Quadient must deliver heightened security assurance for CCM platforms and locker networks; achieving certifications often lengthens sales cycles by several months but expands addressable markets. Failure to meet standards can exclude the company from key public procurements.

- Compliance: NIS2 (EU) and FedRAMP (US)

- Impact: longer sales cycles, larger market access

- Risk: exclusion from public tenders if noncompliant

EU €750bn e‑procurement boosts tenders; data localization (60+ countries), tariffs raise costs

Governments push e‑delivery and e‑invoicing (NextGenerationEU €750bn), creating public procurement opportunities; Quadient (≈€1.04bn revenue 2024) benefits from CCM alignment but faces 12–24 month tender cycles. Data localization in 60+ countries forces multi‑region hosting and higher costs; NIS2/FedRAMP raise security certification burdens. Tariffs (7.5–25%) and 2023–24 export controls increase BOM and lead times (~weeks), prompting nearshoring.

| Factor | Impact | 2023–25 data |

|---|---|---|

| Digital govt | Procurement pipelines | NextGenerationEU €750bn; tenders 12–24m |

| Data rules | Hosting cost, bid eligibility | 60+ countries |

| Tariffs/controls | BOM↑, lead times | Tariffs 7.5–25%; lead times +weeks |

| Security regs | Longer sales cycles | NIS2, FedRAMP |

What is included in the product

Explores how external macro-environmental factors uniquely affect Quadient across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section is data-backed, region- and industry-specific, and offers forward-looking insights with actionable implications for executives, investors and strategists.

A concise, visually segmented PESTLE summary of Quadient that’s easy to drop into presentations, share across teams, and annotate for region- or product-specific risks—supporting faster alignment and clearer discussions on external threats and market positioning.

Economic factors

Interest rates and capital spending

Higher policy rates—Fed funds around 5.25–5.50% and the ECB deposit rate near 4% in 2024—have dampened capex for hardware such as parcel lockers and mail equipment, prompting some customers to defer large purchases. Many clients are shifting to SaaS, subscription and leasing models to avoid upfront spend. If rates fall, large rollout programs can restart, and flexible financing solutions help sustain Quadient’s sales pipeline through cycles.

Macro growth and enterprise IT budgets

Economic slowdowns curb discretionary CX and automation budgets, with Gartner estimating global IT spending near $4.9 trillion in 2024 and enterprise software growth around 5% y/y, tightening approvals. Mission-critical compliance communications remain resilient, often prioritized during cuts. Demonstrable ROI—reduced cost-to-serve and faster cash conversion—drives signoffs; land-and-expand sales models preserve growth by converting smaller deployments into broader contracts.

E-commerce parcel volumes and last-mile economics

Rising online retail—global e‑commerce sales estimated at about 6.3 trillion USD in 2024—boosts demand for secure, efficient parcel lockers. Locker networks can cut failed home deliveries by up to 70% and lower last‑mile cost per parcel by roughly 30–50%, improving throughput valued by retailers and multifamily owners. Retail cyclicality can slow or accelerate locker rollouts depending on seasonal and macro retail swings.

Declining traditional mail volumes

Declining traditional mail volumes have eroded legacy franking revenues for Quadient, yet the same digital shift fuels demand for customer communications management and hybrid mail solutions; industry data show letter volumes in many developed markets have fallen roughly 40–50% since the early 2000s, accelerating CCM adoption and managed services purchases.

- Cross-sell automation to existing mail customers offsets revenue decline

- Pricing and service bundling defend margins

- CCM and hybrid mail growth captures digital migration

Currency fluctuations and global footprint

Quadient's multinational footprint exposes reported revenue and component costs to FX swings; in FY2024 (≈€1.1bn revenue) currency translation materially shifted reported growth by an estimated 2–4 percentage points. Dispersion of sourcing and manufacturing across Europe and Asia provides natural hedges and supports pricing localization to reduce volatility. Active hedging programs and centralized treasury policies help stabilize cash flows and limit FX margin erosion.

- FY2024 revenue ≈€1.1bn

- FX translation impact ~2–4 pp

- Sourcing in Europe/Asia = natural hedge

- Pricing localization + hedging = lower volatility

EU €750bn e‑procurement boosts tenders; data localization (60+ countries), tariffs raise costs

Higher policy rates (Fed 5.25–5.50%, ECB ~4% in 2024) depress capex for parcel lockers and mail hardware, shifting customers to SaaS, leasing and deferred purchases. Global e‑commerce (~$6.3T) and IT spend (~$4.9T) sustain locker and CCM demand, while falling letter volumes (down ~40–50% since early 2000s) drive hybrid mail adoption. Quadient FY2024 revenue ≈€1.1bn; FX translation impacted growth ~2–4 pp.

| Metric | Value |

|---|---|

| Fed/ECB rates (2024) | 5.25–5.50% / ~4% |

| Global e‑commerce (2024) | $6.3T |

| Global IT spend (2024) | $4.9T |

| Quadient FY2024 rev | ≈€1.1bn |

| FX impact on growth | ~2–4 pp |

What You See Is What You Get

Quadient PESTLE Analysis

The Quadient PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The preview displays the complete content, structure, and layout with no placeholders. After checkout you’ll instantly download this same professional file.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Our PESTLE analysis of Quadient reveals how political regulation, digital transformation, economic cycles, social trends, legal compliance, and environmental pressures converge to shape its strategy and risk profile. Ideal for investors and strategists, this concise overview highlights key external threats and opportunities. Download the full, editable PESTLE now to get the complete, actionable intelligence you need.

Political factors

Public-sector digital transformation agendas

Governments are prioritizing citizen experience, e-invoicing and digitized correspondence, driving demand for CCM and automation; Quadient can align offerings with the EU eIDAS framework (Regulation (EU) No 910/2014) and national digital mail initiatives. EU recovery funding via NextGenerationEU (€750 billion) supports digitization projects and procurement pipelines. Public tenders often take 12–24 months but deliver sticky, multi-year contracts; budget cycles and election outcomes can rephase priorities or timelines.

Data sovereignty and localization policies

With over 60 countries enacting data localization or strict cross-border transfer rules, EU and UK regimes plus regional laws increasingly demand local storage and processing; Quadient’s CCM and parcel‑locker telemetry must offer EU/UK/region hosting options to remain eligible. This drives multi-region cloud architecture, higher infrastructure and compliance costs and narrower vendor choice, and non-compliance can disqualify bids for government or regulated-sector contracts.

Postal sector regulation and modernization

Reforms of national postal services—after letter post volumes have fallen roughly 40% globally since 2000 (UPU)—reshape franking standards and machine certification, forcing Quadient to update mail systems and testing. Quadient (≈€1.04bn revenue in 2024) must track changing tariffs, indicia formats and compliance tests across markets. Government incentives for hybrid mail (subsidies or integration pilots in EU member states) can soften physical-mail decline, while stricter de-mail mandates accelerate substitution.

Trade policy and supply-chain geopolitics

Tariffs on electronics (notably US Section 301 levies of roughly 7.5–25% on many Chinese-made components) raise Quadient parcel-locker BOM costs and compress margins; 2023–24 export controls on advanced semiconductors and sanctions complicate multinational deployments and certifications; political tensions and chokepoint risks have extended logistics lead times by several weeks; diversifying suppliers and nearshoring mitigates exposure.

- Tariff impact: 7.5–25% on many components

- Export controls: 2023–24 semiconductor restrictions

- Logistics: lead times +weeks, higher freight volatility

- Mitigation: supplier diversification, nearshoring

Cybersecurity directives for critical infrastructure

Public and regulated buyers are bound by frameworks such as NIS2 across the 27 EU member states and FedRAMP-style requirements for US federal procurements (FedRAMP mandatory for cloud services since 2014). Quadient must deliver heightened security assurance for CCM platforms and locker networks; achieving certifications often lengthens sales cycles by several months but expands addressable markets. Failure to meet standards can exclude the company from key public procurements.

- Compliance: NIS2 (EU) and FedRAMP (US)

- Impact: longer sales cycles, larger market access

- Risk: exclusion from public tenders if noncompliant

EU €750bn e‑procurement boosts tenders; data localization (60+ countries), tariffs raise costs

Governments push e‑delivery and e‑invoicing (NextGenerationEU €750bn), creating public procurement opportunities; Quadient (≈€1.04bn revenue 2024) benefits from CCM alignment but faces 12–24 month tender cycles. Data localization in 60+ countries forces multi‑region hosting and higher costs; NIS2/FedRAMP raise security certification burdens. Tariffs (7.5–25%) and 2023–24 export controls increase BOM and lead times (~weeks), prompting nearshoring.

| Factor | Impact | 2023–25 data |

|---|---|---|

| Digital govt | Procurement pipelines | NextGenerationEU €750bn; tenders 12–24m |

| Data rules | Hosting cost, bid eligibility | 60+ countries |

| Tariffs/controls | BOM↑, lead times | Tariffs 7.5–25%; lead times +weeks |

| Security regs | Longer sales cycles | NIS2, FedRAMP |

What is included in the product

Explores how external macro-environmental factors uniquely affect Quadient across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section is data-backed, region- and industry-specific, and offers forward-looking insights with actionable implications for executives, investors and strategists.

A concise, visually segmented PESTLE summary of Quadient that’s easy to drop into presentations, share across teams, and annotate for region- or product-specific risks—supporting faster alignment and clearer discussions on external threats and market positioning.

Economic factors

Interest rates and capital spending

Higher policy rates—Fed funds around 5.25–5.50% and the ECB deposit rate near 4% in 2024—have dampened capex for hardware such as parcel lockers and mail equipment, prompting some customers to defer large purchases. Many clients are shifting to SaaS, subscription and leasing models to avoid upfront spend. If rates fall, large rollout programs can restart, and flexible financing solutions help sustain Quadient’s sales pipeline through cycles.

Macro growth and enterprise IT budgets

Economic slowdowns curb discretionary CX and automation budgets, with Gartner estimating global IT spending near $4.9 trillion in 2024 and enterprise software growth around 5% y/y, tightening approvals. Mission-critical compliance communications remain resilient, often prioritized during cuts. Demonstrable ROI—reduced cost-to-serve and faster cash conversion—drives signoffs; land-and-expand sales models preserve growth by converting smaller deployments into broader contracts.

E-commerce parcel volumes and last-mile economics

Rising online retail—global e‑commerce sales estimated at about 6.3 trillion USD in 2024—boosts demand for secure, efficient parcel lockers. Locker networks can cut failed home deliveries by up to 70% and lower last‑mile cost per parcel by roughly 30–50%, improving throughput valued by retailers and multifamily owners. Retail cyclicality can slow or accelerate locker rollouts depending on seasonal and macro retail swings.

Declining traditional mail volumes

Declining traditional mail volumes have eroded legacy franking revenues for Quadient, yet the same digital shift fuels demand for customer communications management and hybrid mail solutions; industry data show letter volumes in many developed markets have fallen roughly 40–50% since the early 2000s, accelerating CCM adoption and managed services purchases.

- Cross-sell automation to existing mail customers offsets revenue decline

- Pricing and service bundling defend margins

- CCM and hybrid mail growth captures digital migration

Currency fluctuations and global footprint

Quadient's multinational footprint exposes reported revenue and component costs to FX swings; in FY2024 (≈€1.1bn revenue) currency translation materially shifted reported growth by an estimated 2–4 percentage points. Dispersion of sourcing and manufacturing across Europe and Asia provides natural hedges and supports pricing localization to reduce volatility. Active hedging programs and centralized treasury policies help stabilize cash flows and limit FX margin erosion.

- FY2024 revenue ≈€1.1bn

- FX translation impact ~2–4 pp

- Sourcing in Europe/Asia = natural hedge

- Pricing localization + hedging = lower volatility

EU €750bn e‑procurement boosts tenders; data localization (60+ countries), tariffs raise costs

Higher policy rates (Fed 5.25–5.50%, ECB ~4% in 2024) depress capex for parcel lockers and mail hardware, shifting customers to SaaS, leasing and deferred purchases. Global e‑commerce (~$6.3T) and IT spend (~$4.9T) sustain locker and CCM demand, while falling letter volumes (down ~40–50% since early 2000s) drive hybrid mail adoption. Quadient FY2024 revenue ≈€1.1bn; FX translation impacted growth ~2–4 pp.

| Metric | Value |

|---|---|

| Fed/ECB rates (2024) | 5.25–5.50% / ~4% |

| Global e‑commerce (2024) | $6.3T |

| Global IT spend (2024) | $4.9T |

| Quadient FY2024 rev | ≈€1.1bn |

| FX impact on growth | ~2–4 pp |

What You See Is What You Get

Quadient PESTLE Analysis

The Quadient PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The preview displays the complete content, structure, and layout with no placeholders. After checkout you’ll instantly download this same professional file.