Quaker Chemical Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Quaker Chemical faces moderate supplier power, specialized customer demands, steady rivalry, manageable new-entry barriers, and evolving substitute threats shaping margins and strategy. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Quaker Chemical’s competitive dynamics, market pressures, and strategic advantages in detail. Get the consultant-grade report with visuals, force ratings, and actionable implications for investment or strategy.

Suppliers Bargaining Power

Concentrated specialty additive base

Quaker Houghton depends on a finite set of global suppliers (typically fewer than 10) for base oils, esters, corrosion inhibitors and EP/AW additives; in 2024 upstream consolidation among refiners and petrochemical majors accelerated, concentrating feedstock sources. That consolidation provides suppliers greater pricing discipline and margin resilience. Any disruption can force costly reformulation or allocation, elevating supplier bargaining leverage.

Qualification and switching frictions

Industrial fluids for Quaker are tightly specified and on-line validated, so changing ingredients typically requires months of requalification and performance trials, making reformulation slow and risky; these frictions materially raise switching costs to alternate suppliers and enable suppliers to extract price or supply concessions during tight markets, as seen in 2024 global specialty-chemical supply constraints.

Energy and logistics volatility passthrough

Input costs for Quaker track Brent crude (~85 USD/bbl in 2024), natural gas (~3 USD/MMBtu) and freight, with suppliers imposing surcharges; contracts often include pass-through clauses but timing gaps compress margins. Shipping constraints and sudden port congestion (container freight up ~20% in parts of 2024) tighten supply and temporarily elevate supplier bargaining power.

Regulatory and ESG constraints

Mitigations via scale and dual sourcing

Quaker Houghton leverages scale—roughly $2.2 billion revenue in 2024—to secure multi-sourcing and long-term contracts, while collaborative forecasting and vendor-managed inventory (VMI) lower disruption risk; private‑label and custom blends lock supply at negotiated margins, tempering but not eliminating supplier power.

- Scale: $2.2B revenue (2024)

- Operational levers: multi‑sourcing, VMI, collaborative forecasting

- Commercial levers: private‑label/custom blends, long‑term agreements

Concentrated suppliers tighten pricing; Brent 85 USD/bbl, freight +20%

Supplier base is concentrated (<10 core feedstock providers), raising pricing leverage after 2024 upstream consolidation. High switching costs from on-line validation and REACH/TSCA/PFAS constraints amplify supplier power; Brent-linked feedstock (≈85 USD/bbl) and container freight spikes (~+20% in 2024) compress margins. Quaker Houghton scale (≈$2.2B revenue in 2024) and long-term contracts mitigate but do not eliminate supplier leverage.

| Metric | 2024 value |

|---|---|

| Core suppliers | <10 |

| Brent crude | ≈85 USD/bbl |

| Revenue | ≈$2.2B |

| REACH | ≈22,500 substances |

| TSCA | ≈86,000 |

| Freight change | ≈+20% |

What is included in the product

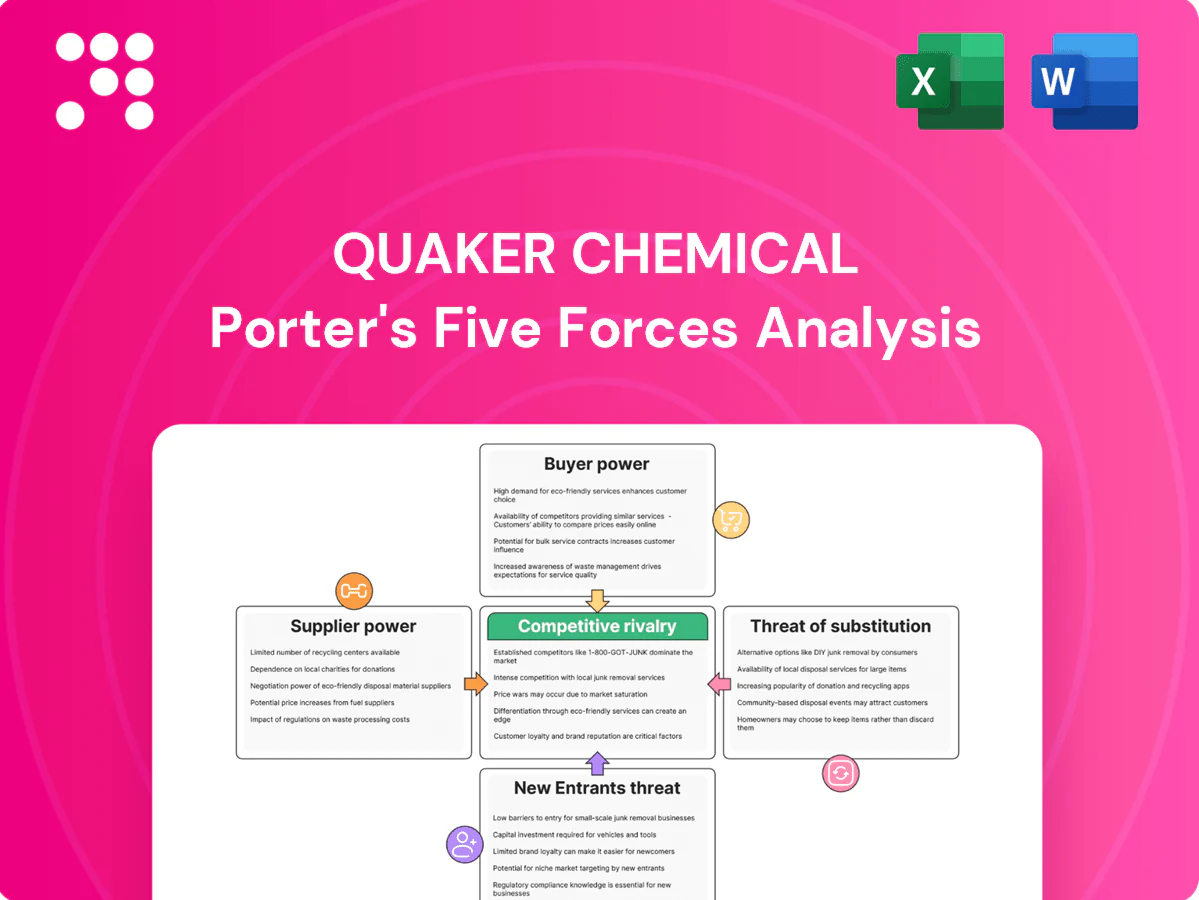

Tailored Porter's Five Forces analysis for Quaker Chemical uncovering competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers—highlighting how raw‑material concentration, technical service differentiation, and regulatory/innovation threats shape pricing power and profitability.

One-sheet Porter’s Five Forces for Quaker Chemical that condenses competitive pressure into a customizable spider chart—perfect for quick strategic decisions, slide-ready summaries, and seamless integration into reports or dashboards to instantly relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated heavy-industry customers

Steel, aluminum, automotive and aerospace buyers are large, organized customers that run competitive tenders and use volume to extract price concessions; in 2024 the top 10 steel producers account for roughly 50% of global crude steel, while the top 10 automakers represent about 60% of light-vehicle sales. Consolidation among OEMs and mills—Boeing and Airbus controlling ~90% of large commercial jet deliveries—heightens purchasing clout. This concentration materially elevates buyer power versus Quaker Chemical.

High switching costs and embedded service

Process fluids are tightly integrated with equipment, tooling and quality specs, so switching requires line trials, downtime risk and retraining. Quaker Houghton, with reported 2023 net sales of about $1.7 billion, embeds technical service into account relationships, creating operational stickiness. These factors materially reduce buyer willingness to switch solely on price.

Cyclic demand and price sensitivity

End markets for Quaker Chemical are highly cyclical, driving customers to demand cost-outs during downturns; FY2024 sales of about $1.02 billion heightened focus on rebates, indexation and extended payment terms. Buyers push rebates and indexation to protect margins, while volume variability — often ±10-20% in industrial end markets — becomes leverage. Price sensitivity rises sharply as plant utilization falls, compressing mix and margins.

Performance and compliance requirements

Global support expectations

Global customers demand consistent formulations and service across plants, requiring vendors like Quaker Chemical to deliver rapid technical response and high supply reliability to retain multinational contracts.

Because only a handful of suppliers can meet global scale and regulatory consistency, the pool of credible alternatives is small, which limits buyer leverage despite large account size.

- Consistent formulations across sites

- Rapid technical response required

- High supply reliability narrows suppliers

- Few credible alternatives reduces buyer power

Large buyers (~50% steel, ~60% autos) press supplier

Large consolidated buyers (top10 steel ~50% crude steel; top10 automakers ~60% light-vehicle sales) exert strong price pressure on Quaker Chemical (FY2024 sales ~1.02B). Technical integration, approved-vendor lists and HSE/ESG raise switching costs, reducing buyer leverage despite cyclical cost demands.

| Metric | Value |

|---|---|

| Quaker FY2024 sales | $1.02B |

| Top10 steel share | ~50% |

Full Version Awaits

Quaker Chemical Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Quaker Chemical you'll receive—no placeholders or mockups. The document is the final, professionally formatted file covering supplier power, buyer power, competitive rivalry, threat of entry and substitutes, and strategic implications. Once you purchase, you get immediate access to this same ready-to-use file.

From Overview to Strategy Blueprint

Quaker Chemical faces moderate supplier power, specialized customer demands, steady rivalry, manageable new-entry barriers, and evolving substitute threats shaping margins and strategy. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Quaker Chemical’s competitive dynamics, market pressures, and strategic advantages in detail. Get the consultant-grade report with visuals, force ratings, and actionable implications for investment or strategy.

Suppliers Bargaining Power

Concentrated specialty additive base

Quaker Houghton depends on a finite set of global suppliers (typically fewer than 10) for base oils, esters, corrosion inhibitors and EP/AW additives; in 2024 upstream consolidation among refiners and petrochemical majors accelerated, concentrating feedstock sources. That consolidation provides suppliers greater pricing discipline and margin resilience. Any disruption can force costly reformulation or allocation, elevating supplier bargaining leverage.

Qualification and switching frictions

Industrial fluids for Quaker are tightly specified and on-line validated, so changing ingredients typically requires months of requalification and performance trials, making reformulation slow and risky; these frictions materially raise switching costs to alternate suppliers and enable suppliers to extract price or supply concessions during tight markets, as seen in 2024 global specialty-chemical supply constraints.

Energy and logistics volatility passthrough

Input costs for Quaker track Brent crude (~85 USD/bbl in 2024), natural gas (~3 USD/MMBtu) and freight, with suppliers imposing surcharges; contracts often include pass-through clauses but timing gaps compress margins. Shipping constraints and sudden port congestion (container freight up ~20% in parts of 2024) tighten supply and temporarily elevate supplier bargaining power.

Regulatory and ESG constraints

Mitigations via scale and dual sourcing

Quaker Houghton leverages scale—roughly $2.2 billion revenue in 2024—to secure multi-sourcing and long-term contracts, while collaborative forecasting and vendor-managed inventory (VMI) lower disruption risk; private‑label and custom blends lock supply at negotiated margins, tempering but not eliminating supplier power.

- Scale: $2.2B revenue (2024)

- Operational levers: multi‑sourcing, VMI, collaborative forecasting

- Commercial levers: private‑label/custom blends, long‑term agreements

Concentrated suppliers tighten pricing; Brent 85 USD/bbl, freight +20%

Supplier base is concentrated (<10 core feedstock providers), raising pricing leverage after 2024 upstream consolidation. High switching costs from on-line validation and REACH/TSCA/PFAS constraints amplify supplier power; Brent-linked feedstock (≈85 USD/bbl) and container freight spikes (~+20% in 2024) compress margins. Quaker Houghton scale (≈$2.2B revenue in 2024) and long-term contracts mitigate but do not eliminate supplier leverage.

| Metric | 2024 value |

|---|---|

| Core suppliers | <10 |

| Brent crude | ≈85 USD/bbl |

| Revenue | ≈$2.2B |

| REACH | ≈22,500 substances |

| TSCA | ≈86,000 |

| Freight change | ≈+20% |

What is included in the product

Tailored Porter's Five Forces analysis for Quaker Chemical uncovering competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers—highlighting how raw‑material concentration, technical service differentiation, and regulatory/innovation threats shape pricing power and profitability.

One-sheet Porter’s Five Forces for Quaker Chemical that condenses competitive pressure into a customizable spider chart—perfect for quick strategic decisions, slide-ready summaries, and seamless integration into reports or dashboards to instantly relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated heavy-industry customers

Steel, aluminum, automotive and aerospace buyers are large, organized customers that run competitive tenders and use volume to extract price concessions; in 2024 the top 10 steel producers account for roughly 50% of global crude steel, while the top 10 automakers represent about 60% of light-vehicle sales. Consolidation among OEMs and mills—Boeing and Airbus controlling ~90% of large commercial jet deliveries—heightens purchasing clout. This concentration materially elevates buyer power versus Quaker Chemical.

High switching costs and embedded service

Process fluids are tightly integrated with equipment, tooling and quality specs, so switching requires line trials, downtime risk and retraining. Quaker Houghton, with reported 2023 net sales of about $1.7 billion, embeds technical service into account relationships, creating operational stickiness. These factors materially reduce buyer willingness to switch solely on price.

Cyclic demand and price sensitivity

End markets for Quaker Chemical are highly cyclical, driving customers to demand cost-outs during downturns; FY2024 sales of about $1.02 billion heightened focus on rebates, indexation and extended payment terms. Buyers push rebates and indexation to protect margins, while volume variability — often ±10-20% in industrial end markets — becomes leverage. Price sensitivity rises sharply as plant utilization falls, compressing mix and margins.

Performance and compliance requirements

Global support expectations

Global customers demand consistent formulations and service across plants, requiring vendors like Quaker Chemical to deliver rapid technical response and high supply reliability to retain multinational contracts.

Because only a handful of suppliers can meet global scale and regulatory consistency, the pool of credible alternatives is small, which limits buyer leverage despite large account size.

- Consistent formulations across sites

- Rapid technical response required

- High supply reliability narrows suppliers

- Few credible alternatives reduces buyer power

Large buyers (~50% steel, ~60% autos) press supplier

Large consolidated buyers (top10 steel ~50% crude steel; top10 automakers ~60% light-vehicle sales) exert strong price pressure on Quaker Chemical (FY2024 sales ~1.02B). Technical integration, approved-vendor lists and HSE/ESG raise switching costs, reducing buyer leverage despite cyclical cost demands.

| Metric | Value |

|---|---|

| Quaker FY2024 sales | $1.02B |

| Top10 steel share | ~50% |

Full Version Awaits

Quaker Chemical Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Quaker Chemical you'll receive—no placeholders or mockups. The document is the final, professionally formatted file covering supplier power, buyer power, competitive rivalry, threat of entry and substitutes, and strategic implications. Once you purchase, you get immediate access to this same ready-to-use file.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Quaker Chemical faces moderate supplier power, specialized customer demands, steady rivalry, manageable new-entry barriers, and evolving substitute threats shaping margins and strategy. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Quaker Chemical’s competitive dynamics, market pressures, and strategic advantages in detail. Get the consultant-grade report with visuals, force ratings, and actionable implications for investment or strategy.

Suppliers Bargaining Power

Concentrated specialty additive base

Quaker Houghton depends on a finite set of global suppliers (typically fewer than 10) for base oils, esters, corrosion inhibitors and EP/AW additives; in 2024 upstream consolidation among refiners and petrochemical majors accelerated, concentrating feedstock sources. That consolidation provides suppliers greater pricing discipline and margin resilience. Any disruption can force costly reformulation or allocation, elevating supplier bargaining leverage.

Qualification and switching frictions

Industrial fluids for Quaker are tightly specified and on-line validated, so changing ingredients typically requires months of requalification and performance trials, making reformulation slow and risky; these frictions materially raise switching costs to alternate suppliers and enable suppliers to extract price or supply concessions during tight markets, as seen in 2024 global specialty-chemical supply constraints.

Energy and logistics volatility passthrough

Input costs for Quaker track Brent crude (~85 USD/bbl in 2024), natural gas (~3 USD/MMBtu) and freight, with suppliers imposing surcharges; contracts often include pass-through clauses but timing gaps compress margins. Shipping constraints and sudden port congestion (container freight up ~20% in parts of 2024) tighten supply and temporarily elevate supplier bargaining power.

Regulatory and ESG constraints

Mitigations via scale and dual sourcing

Quaker Houghton leverages scale—roughly $2.2 billion revenue in 2024—to secure multi-sourcing and long-term contracts, while collaborative forecasting and vendor-managed inventory (VMI) lower disruption risk; private‑label and custom blends lock supply at negotiated margins, tempering but not eliminating supplier power.

- Scale: $2.2B revenue (2024)

- Operational levers: multi‑sourcing, VMI, collaborative forecasting

- Commercial levers: private‑label/custom blends, long‑term agreements

Concentrated suppliers tighten pricing; Brent 85 USD/bbl, freight +20%

Supplier base is concentrated (<10 core feedstock providers), raising pricing leverage after 2024 upstream consolidation. High switching costs from on-line validation and REACH/TSCA/PFAS constraints amplify supplier power; Brent-linked feedstock (≈85 USD/bbl) and container freight spikes (~+20% in 2024) compress margins. Quaker Houghton scale (≈$2.2B revenue in 2024) and long-term contracts mitigate but do not eliminate supplier leverage.

| Metric | 2024 value |

|---|---|

| Core suppliers | <10 |

| Brent crude | ≈85 USD/bbl |

| Revenue | ≈$2.2B |

| REACH | ≈22,500 substances |

| TSCA | ≈86,000 |

| Freight change | ≈+20% |

What is included in the product

Tailored Porter's Five Forces analysis for Quaker Chemical uncovering competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers—highlighting how raw‑material concentration, technical service differentiation, and regulatory/innovation threats shape pricing power and profitability.

One-sheet Porter’s Five Forces for Quaker Chemical that condenses competitive pressure into a customizable spider chart—perfect for quick strategic decisions, slide-ready summaries, and seamless integration into reports or dashboards to instantly relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated heavy-industry customers

Steel, aluminum, automotive and aerospace buyers are large, organized customers that run competitive tenders and use volume to extract price concessions; in 2024 the top 10 steel producers account for roughly 50% of global crude steel, while the top 10 automakers represent about 60% of light-vehicle sales. Consolidation among OEMs and mills—Boeing and Airbus controlling ~90% of large commercial jet deliveries—heightens purchasing clout. This concentration materially elevates buyer power versus Quaker Chemical.

High switching costs and embedded service

Process fluids are tightly integrated with equipment, tooling and quality specs, so switching requires line trials, downtime risk and retraining. Quaker Houghton, with reported 2023 net sales of about $1.7 billion, embeds technical service into account relationships, creating operational stickiness. These factors materially reduce buyer willingness to switch solely on price.

Cyclic demand and price sensitivity

End markets for Quaker Chemical are highly cyclical, driving customers to demand cost-outs during downturns; FY2024 sales of about $1.02 billion heightened focus on rebates, indexation and extended payment terms. Buyers push rebates and indexation to protect margins, while volume variability — often ±10-20% in industrial end markets — becomes leverage. Price sensitivity rises sharply as plant utilization falls, compressing mix and margins.

Performance and compliance requirements

Global support expectations

Global customers demand consistent formulations and service across plants, requiring vendors like Quaker Chemical to deliver rapid technical response and high supply reliability to retain multinational contracts.

Because only a handful of suppliers can meet global scale and regulatory consistency, the pool of credible alternatives is small, which limits buyer leverage despite large account size.

- Consistent formulations across sites

- Rapid technical response required

- High supply reliability narrows suppliers

- Few credible alternatives reduces buyer power

Large buyers (~50% steel, ~60% autos) press supplier

Large consolidated buyers (top10 steel ~50% crude steel; top10 automakers ~60% light-vehicle sales) exert strong price pressure on Quaker Chemical (FY2024 sales ~1.02B). Technical integration, approved-vendor lists and HSE/ESG raise switching costs, reducing buyer leverage despite cyclical cost demands.

| Metric | Value |

|---|---|

| Quaker FY2024 sales | $1.02B |

| Top10 steel share | ~50% |

Full Version Awaits

Quaker Chemical Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Quaker Chemical you'll receive—no placeholders or mockups. The document is the final, professionally formatted file covering supplier power, buyer power, competitive rivalry, threat of entry and substitutes, and strategic implications. Once you purchase, you get immediate access to this same ready-to-use file.