Qualcomm SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Qualcomm’s chipset leadership and strong patent portfolio drive margins, while dependence on smartphone OEMs and legal/regulatory risks pressure growth. 5G expansion and AI at the edge present major opportunities, but fierce competition and supply-chain exposure are clear threats. Want full strategic detail and editable tools? Purchase the complete SWOT analysis for an investor-ready, research-backed report.

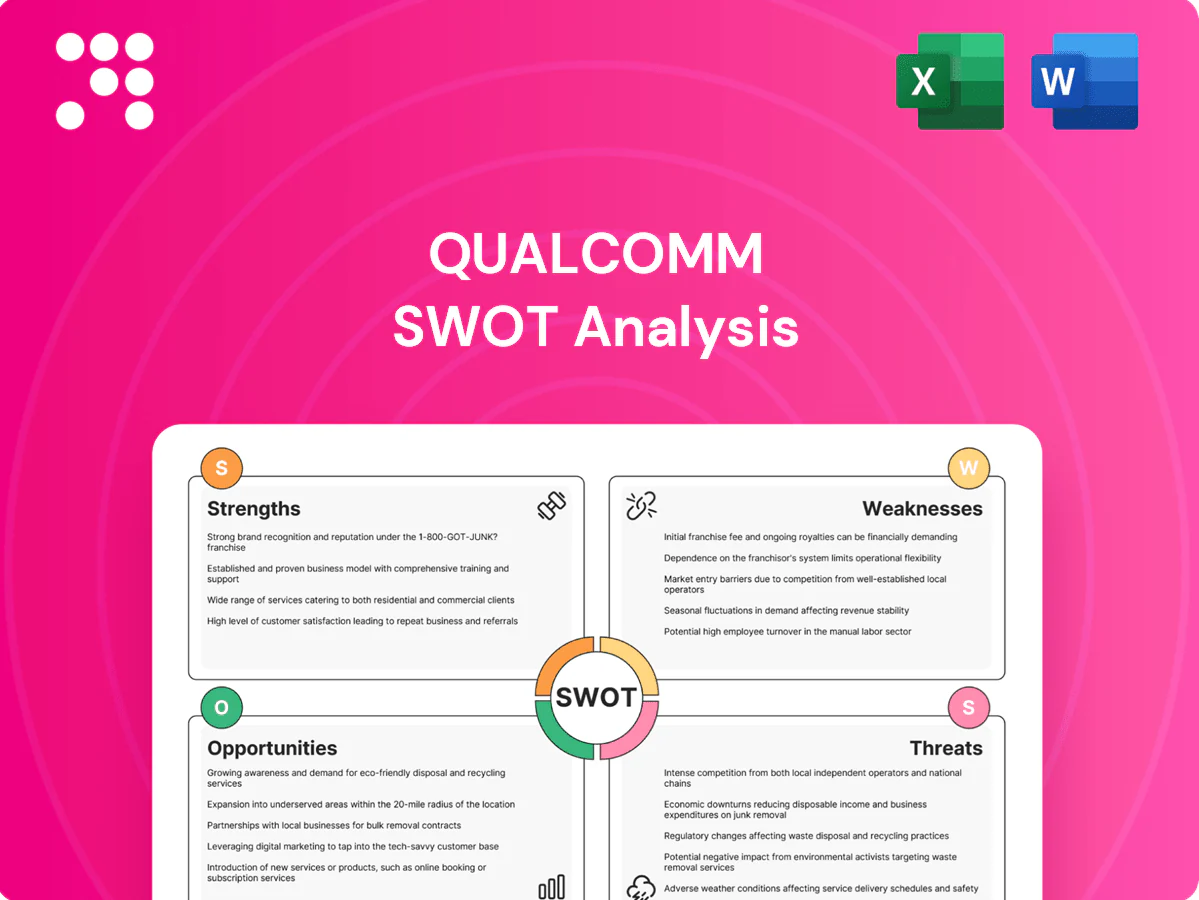

Strengths

Dominant 5G IP

Qualcomm holds one of the deepest cellular patent portfolios with more than 20,000 patents and applications spanning 3G through 5G Advanced, underpinning high-margin licensing streams. Its licensing business has generated over $100 billion in cumulative royalties, giving strategic leverage across device makers and carriers. The IP depth enables broad cross-licensing, raises rivals’ entry barriers and positions Qualcomm strongly for 6G standard-setting.

Snapdragon platform leadership

Snapdragon processors and modems power the majority of premium and high-tier Android devices, shipping in hundreds of millions of handsets annually; integrated CPU, GPU, NPU and modem deliver measurable gains in performance and power efficiency that shorten OEM time-to-market. Strong brand pull with top OEMs such as Samsung and Xiaomi sustains design-win momentum and recurring royalty and chipset revenue streams. Consistent flagship wins reinforce developer support and ecosystem stickiness, boosting app optimization and long-term platform value.

Diversified growth engines

Beyond handsets, Qualcomm leverages diversified growth engines—RF front-end, IoT, automotive, PC and XR—anchored by FY2024 revenue of about $44.2 billion; RF modules and advanced 5G/Wi‑Fi increase dollar content per device, while Automotive Digital Chassis wins have built a multi-year backlog near $9 billion, reducing reliance on cyclical smartphone demand.

Fabless scalability

Qualcomm's fabless model leverages world-class foundries such as TSMC and Samsung (TSMC held roughly 54% of global foundry revenue in 2024) to access leading nodes (5nm/3nm), enabling rapid node migration without capex-heavy fabs, faster product refreshes and shorter time-to-market while optimizing cost and yield through flexible multi-sourcing.

- Foundry partners: TSMC, Samsung

- Leading nodes: 5nm/3nm

- 2024 foundry share: ~54% TSMC

- Benefits: lower capex, faster refresh, cost/yield optimization

Heavy R&D and standards role

Qualcomm's sustained R&D intensity (FY2024 R&D ~$7.5B on revenue ~$44.3B) keeps it at the frontier of wireless, AI-at-the-edge and connectivity; deep 3GPP and IEEE engagement gives early sight on standards adoption and customer needs, enabling differentiated silicon and firmware that command premium ASPs and create durable moats.

- R&D spend ~7.5B (FY2024)

- Revenue context ~$44.3B (FY2024)

- Active in 3GPP/IEEE = earlier roadmap influence

- Result: premium ASPs, defensible moats

Mobile-chip leader: >20,000, >$100B royalties, FY24 ~$44B

Qualcomm’s >20,000-patent portfolio and >$100B cumulative royalties underpin high-margin licensing and 6G positioning. Snapdragon chips dominate premium Android, shipping hundreds of millions yearly and securing flagship design wins. FY2024 revenue ~$44.2B with R&D ~$7.5B sustains wireless/AI leadership; automotive backlog ~$9B and TSMC ~54% foundry access diversify dollar content.

| Metric | Value |

|---|---|

| Patents | >20,000 |

| Cumulative royalties | >$100B |

| FY2024 revenue | ~$44.2B |

| FY2024 R&D | ~$7.5B |

| Automotive backlog | ~$9B |

| TSMC foundry share | ~54% |

What is included in the product

Provides a clear SWOT framework for analyzing Qualcomm’s business strategy, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and future growth.

Provides a concise Qualcomm SWOT matrix for fast strategic alignment, quick executive snapshots, and easy integration into reports and presentations.

Weaknesses

Handset concentration

Smartphones still drive a large share of Qualcomm’s revenue and profits, leaving results highly exposed to handset demand cycles and FY2024/FY2025 seasonal shifts. Inventory corrections and upgrade lulls have compressed chipset margins in recent quarters, increasing cost pressure. This handset dependence heightens quarterly volatility and limits pricing power during down-cycles, forcing promotional or concessionary pricing to maintain volumes.

Customer concentration risk

A meaningful portion of Qualcomm sales remains concentrated with a handful of major Android OEMs and China-based customers, with China accounting for roughly one-third of FY2024 revenue; shifts in market share, in-sourcing or financial stress at those OEMs could materially dent top-line performance. Large buyers command negotiating leverage on pricing and terms, compressing margins, while replacement design-wins typically take 12–24 months to materialize, delaying revenue recovery.

Third-party foundry reliance

Qualcomm's heavy reliance on external fabs, primarily TSMC and Samsung, exposes it to capacity constraints and node allocations—TSMC held about 54% of global foundry revenue in 2024. Yield problems or supply disruptions can delay product launches and increase COGS; large customers like Apple and NVIDIA often secure node priority, limiting Qualcomm's control over manufacturing roadmaps and timing.

Regulatory and legal overhang

Qualcomm faces sustained antitrust scrutiny over licensing practices across multiple jurisdictions; past regulatory actions have led to remedies and fines totaling hundreds of millions of dollars in prior cases, and new probes could force lower royalty rates. Ongoing global litigation consumes management time and cash, with outcomes able to set precedents that constrain future licensing leverage.

- Antitrust probes: multi-jurisdictional

- Financial impact: prior fines in the hundreds of millions

- Operational drag: management focus and legal spend

- Precedent risk: could reduce future royalties

Apple modem exposure

Apple’s push for in‑house modems, announced in 2020 and reported in 2023 to target 2025–2026 deployment, creates a tangible revenue risk to Qualcomm’s premium modem segment and scale economics tied to high‑end iPhone volumes (~223 million iPhones shipped in 2023 per IDC).

Loss of a marquee customer could compress margins and shift market perception of Qualcomm’s technology leadership.

- Apple modem roadmap: 2020 announcement; 2023 reports targeting 2025–26

- iPhone volume reference: ~223M units in 2023 (IDC)

- Impacts: revenue, scale economics, brand/tech perception

Smartphone concentration and foundry reliance squeeze chipset margins, raise supply risk

Smartphone dependence (≈33% FY2024 revenue from China) and OEM concentration raise volatility and compress chipset margins across FY2024–FY2025 cycles. Heavy reliance on external fabs (TSMC ≈54% foundry share in 2024) risks node priority and supply squeezes. Antitrust fines (hundreds of millions) and Apple’s in‑house modem push (iPhone ≈223M in 2023) threaten royalties and premium volumes.

| Metric | Value |

|---|---|

| China share FY2024 | ≈33% |

| TSMC foundry 2024 | ≈54% |

| iPhone 2023 shipments | ≈223M |

What You See Is What You Get

Qualcomm SWOT Analysis

This is the actual Qualcomm SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after checkout. Buy now to unlock the entire in-depth report.

Make Insightful Decisions Backed by Expert Research

Qualcomm’s chipset leadership and strong patent portfolio drive margins, while dependence on smartphone OEMs and legal/regulatory risks pressure growth. 5G expansion and AI at the edge present major opportunities, but fierce competition and supply-chain exposure are clear threats. Want full strategic detail and editable tools? Purchase the complete SWOT analysis for an investor-ready, research-backed report.

Strengths

Dominant 5G IP

Qualcomm holds one of the deepest cellular patent portfolios with more than 20,000 patents and applications spanning 3G through 5G Advanced, underpinning high-margin licensing streams. Its licensing business has generated over $100 billion in cumulative royalties, giving strategic leverage across device makers and carriers. The IP depth enables broad cross-licensing, raises rivals’ entry barriers and positions Qualcomm strongly for 6G standard-setting.

Snapdragon platform leadership

Snapdragon processors and modems power the majority of premium and high-tier Android devices, shipping in hundreds of millions of handsets annually; integrated CPU, GPU, NPU and modem deliver measurable gains in performance and power efficiency that shorten OEM time-to-market. Strong brand pull with top OEMs such as Samsung and Xiaomi sustains design-win momentum and recurring royalty and chipset revenue streams. Consistent flagship wins reinforce developer support and ecosystem stickiness, boosting app optimization and long-term platform value.

Diversified growth engines

Beyond handsets, Qualcomm leverages diversified growth engines—RF front-end, IoT, automotive, PC and XR—anchored by FY2024 revenue of about $44.2 billion; RF modules and advanced 5G/Wi‑Fi increase dollar content per device, while Automotive Digital Chassis wins have built a multi-year backlog near $9 billion, reducing reliance on cyclical smartphone demand.

Fabless scalability

Qualcomm's fabless model leverages world-class foundries such as TSMC and Samsung (TSMC held roughly 54% of global foundry revenue in 2024) to access leading nodes (5nm/3nm), enabling rapid node migration without capex-heavy fabs, faster product refreshes and shorter time-to-market while optimizing cost and yield through flexible multi-sourcing.

- Foundry partners: TSMC, Samsung

- Leading nodes: 5nm/3nm

- 2024 foundry share: ~54% TSMC

- Benefits: lower capex, faster refresh, cost/yield optimization

Heavy R&D and standards role

Qualcomm's sustained R&D intensity (FY2024 R&D ~$7.5B on revenue ~$44.3B) keeps it at the frontier of wireless, AI-at-the-edge and connectivity; deep 3GPP and IEEE engagement gives early sight on standards adoption and customer needs, enabling differentiated silicon and firmware that command premium ASPs and create durable moats.

- R&D spend ~7.5B (FY2024)

- Revenue context ~$44.3B (FY2024)

- Active in 3GPP/IEEE = earlier roadmap influence

- Result: premium ASPs, defensible moats

Mobile-chip leader: >20,000, >$100B royalties, FY24 ~$44B

Qualcomm’s >20,000-patent portfolio and >$100B cumulative royalties underpin high-margin licensing and 6G positioning. Snapdragon chips dominate premium Android, shipping hundreds of millions yearly and securing flagship design wins. FY2024 revenue ~$44.2B with R&D ~$7.5B sustains wireless/AI leadership; automotive backlog ~$9B and TSMC ~54% foundry access diversify dollar content.

| Metric | Value |

|---|---|

| Patents | >20,000 |

| Cumulative royalties | >$100B |

| FY2024 revenue | ~$44.2B |

| FY2024 R&D | ~$7.5B |

| Automotive backlog | ~$9B |

| TSMC foundry share | ~54% |

What is included in the product

Provides a clear SWOT framework for analyzing Qualcomm’s business strategy, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and future growth.

Provides a concise Qualcomm SWOT matrix for fast strategic alignment, quick executive snapshots, and easy integration into reports and presentations.

Weaknesses

Handset concentration

Smartphones still drive a large share of Qualcomm’s revenue and profits, leaving results highly exposed to handset demand cycles and FY2024/FY2025 seasonal shifts. Inventory corrections and upgrade lulls have compressed chipset margins in recent quarters, increasing cost pressure. This handset dependence heightens quarterly volatility and limits pricing power during down-cycles, forcing promotional or concessionary pricing to maintain volumes.

Customer concentration risk

A meaningful portion of Qualcomm sales remains concentrated with a handful of major Android OEMs and China-based customers, with China accounting for roughly one-third of FY2024 revenue; shifts in market share, in-sourcing or financial stress at those OEMs could materially dent top-line performance. Large buyers command negotiating leverage on pricing and terms, compressing margins, while replacement design-wins typically take 12–24 months to materialize, delaying revenue recovery.

Third-party foundry reliance

Qualcomm's heavy reliance on external fabs, primarily TSMC and Samsung, exposes it to capacity constraints and node allocations—TSMC held about 54% of global foundry revenue in 2024. Yield problems or supply disruptions can delay product launches and increase COGS; large customers like Apple and NVIDIA often secure node priority, limiting Qualcomm's control over manufacturing roadmaps and timing.

Regulatory and legal overhang

Qualcomm faces sustained antitrust scrutiny over licensing practices across multiple jurisdictions; past regulatory actions have led to remedies and fines totaling hundreds of millions of dollars in prior cases, and new probes could force lower royalty rates. Ongoing global litigation consumes management time and cash, with outcomes able to set precedents that constrain future licensing leverage.

- Antitrust probes: multi-jurisdictional

- Financial impact: prior fines in the hundreds of millions

- Operational drag: management focus and legal spend

- Precedent risk: could reduce future royalties

Apple modem exposure

Apple’s push for in‑house modems, announced in 2020 and reported in 2023 to target 2025–2026 deployment, creates a tangible revenue risk to Qualcomm’s premium modem segment and scale economics tied to high‑end iPhone volumes (~223 million iPhones shipped in 2023 per IDC).

Loss of a marquee customer could compress margins and shift market perception of Qualcomm’s technology leadership.

- Apple modem roadmap: 2020 announcement; 2023 reports targeting 2025–26

- iPhone volume reference: ~223M units in 2023 (IDC)

- Impacts: revenue, scale economics, brand/tech perception

Smartphone concentration and foundry reliance squeeze chipset margins, raise supply risk

Smartphone dependence (≈33% FY2024 revenue from China) and OEM concentration raise volatility and compress chipset margins across FY2024–FY2025 cycles. Heavy reliance on external fabs (TSMC ≈54% foundry share in 2024) risks node priority and supply squeezes. Antitrust fines (hundreds of millions) and Apple’s in‑house modem push (iPhone ≈223M in 2023) threaten royalties and premium volumes.

| Metric | Value |

|---|---|

| China share FY2024 | ≈33% |

| TSMC foundry 2024 | ≈54% |

| iPhone 2023 shipments | ≈223M |

What You See Is What You Get

Qualcomm SWOT Analysis

This is the actual Qualcomm SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after checkout. Buy now to unlock the entire in-depth report.

Description

Make Insightful Decisions Backed by Expert Research

Qualcomm’s chipset leadership and strong patent portfolio drive margins, while dependence on smartphone OEMs and legal/regulatory risks pressure growth. 5G expansion and AI at the edge present major opportunities, but fierce competition and supply-chain exposure are clear threats. Want full strategic detail and editable tools? Purchase the complete SWOT analysis for an investor-ready, research-backed report.

Strengths

Dominant 5G IP

Qualcomm holds one of the deepest cellular patent portfolios with more than 20,000 patents and applications spanning 3G through 5G Advanced, underpinning high-margin licensing streams. Its licensing business has generated over $100 billion in cumulative royalties, giving strategic leverage across device makers and carriers. The IP depth enables broad cross-licensing, raises rivals’ entry barriers and positions Qualcomm strongly for 6G standard-setting.

Snapdragon platform leadership

Snapdragon processors and modems power the majority of premium and high-tier Android devices, shipping in hundreds of millions of handsets annually; integrated CPU, GPU, NPU and modem deliver measurable gains in performance and power efficiency that shorten OEM time-to-market. Strong brand pull with top OEMs such as Samsung and Xiaomi sustains design-win momentum and recurring royalty and chipset revenue streams. Consistent flagship wins reinforce developer support and ecosystem stickiness, boosting app optimization and long-term platform value.

Diversified growth engines

Beyond handsets, Qualcomm leverages diversified growth engines—RF front-end, IoT, automotive, PC and XR—anchored by FY2024 revenue of about $44.2 billion; RF modules and advanced 5G/Wi‑Fi increase dollar content per device, while Automotive Digital Chassis wins have built a multi-year backlog near $9 billion, reducing reliance on cyclical smartphone demand.

Fabless scalability

Qualcomm's fabless model leverages world-class foundries such as TSMC and Samsung (TSMC held roughly 54% of global foundry revenue in 2024) to access leading nodes (5nm/3nm), enabling rapid node migration without capex-heavy fabs, faster product refreshes and shorter time-to-market while optimizing cost and yield through flexible multi-sourcing.

- Foundry partners: TSMC, Samsung

- Leading nodes: 5nm/3nm

- 2024 foundry share: ~54% TSMC

- Benefits: lower capex, faster refresh, cost/yield optimization

Heavy R&D and standards role

Qualcomm's sustained R&D intensity (FY2024 R&D ~$7.5B on revenue ~$44.3B) keeps it at the frontier of wireless, AI-at-the-edge and connectivity; deep 3GPP and IEEE engagement gives early sight on standards adoption and customer needs, enabling differentiated silicon and firmware that command premium ASPs and create durable moats.

- R&D spend ~7.5B (FY2024)

- Revenue context ~$44.3B (FY2024)

- Active in 3GPP/IEEE = earlier roadmap influence

- Result: premium ASPs, defensible moats

Mobile-chip leader: >20,000, >$100B royalties, FY24 ~$44B

Qualcomm’s >20,000-patent portfolio and >$100B cumulative royalties underpin high-margin licensing and 6G positioning. Snapdragon chips dominate premium Android, shipping hundreds of millions yearly and securing flagship design wins. FY2024 revenue ~$44.2B with R&D ~$7.5B sustains wireless/AI leadership; automotive backlog ~$9B and TSMC ~54% foundry access diversify dollar content.

| Metric | Value |

|---|---|

| Patents | >20,000 |

| Cumulative royalties | >$100B |

| FY2024 revenue | ~$44.2B |

| FY2024 R&D | ~$7.5B |

| Automotive backlog | ~$9B |

| TSMC foundry share | ~54% |

What is included in the product

Provides a clear SWOT framework for analyzing Qualcomm’s business strategy, highlighting internal strengths and weaknesses and external opportunities and threats shaping its competitive position and future growth.

Provides a concise Qualcomm SWOT matrix for fast strategic alignment, quick executive snapshots, and easy integration into reports and presentations.

Weaknesses

Handset concentration

Smartphones still drive a large share of Qualcomm’s revenue and profits, leaving results highly exposed to handset demand cycles and FY2024/FY2025 seasonal shifts. Inventory corrections and upgrade lulls have compressed chipset margins in recent quarters, increasing cost pressure. This handset dependence heightens quarterly volatility and limits pricing power during down-cycles, forcing promotional or concessionary pricing to maintain volumes.

Customer concentration risk

A meaningful portion of Qualcomm sales remains concentrated with a handful of major Android OEMs and China-based customers, with China accounting for roughly one-third of FY2024 revenue; shifts in market share, in-sourcing or financial stress at those OEMs could materially dent top-line performance. Large buyers command negotiating leverage on pricing and terms, compressing margins, while replacement design-wins typically take 12–24 months to materialize, delaying revenue recovery.

Third-party foundry reliance

Qualcomm's heavy reliance on external fabs, primarily TSMC and Samsung, exposes it to capacity constraints and node allocations—TSMC held about 54% of global foundry revenue in 2024. Yield problems or supply disruptions can delay product launches and increase COGS; large customers like Apple and NVIDIA often secure node priority, limiting Qualcomm's control over manufacturing roadmaps and timing.

Regulatory and legal overhang

Qualcomm faces sustained antitrust scrutiny over licensing practices across multiple jurisdictions; past regulatory actions have led to remedies and fines totaling hundreds of millions of dollars in prior cases, and new probes could force lower royalty rates. Ongoing global litigation consumes management time and cash, with outcomes able to set precedents that constrain future licensing leverage.

- Antitrust probes: multi-jurisdictional

- Financial impact: prior fines in the hundreds of millions

- Operational drag: management focus and legal spend

- Precedent risk: could reduce future royalties

Apple modem exposure

Apple’s push for in‑house modems, announced in 2020 and reported in 2023 to target 2025–2026 deployment, creates a tangible revenue risk to Qualcomm’s premium modem segment and scale economics tied to high‑end iPhone volumes (~223 million iPhones shipped in 2023 per IDC).

Loss of a marquee customer could compress margins and shift market perception of Qualcomm’s technology leadership.

- Apple modem roadmap: 2020 announcement; 2023 reports targeting 2025–26

- iPhone volume reference: ~223M units in 2023 (IDC)

- Impacts: revenue, scale economics, brand/tech perception

Smartphone concentration and foundry reliance squeeze chipset margins, raise supply risk

Smartphone dependence (≈33% FY2024 revenue from China) and OEM concentration raise volatility and compress chipset margins across FY2024–FY2025 cycles. Heavy reliance on external fabs (TSMC ≈54% foundry share in 2024) risks node priority and supply squeezes. Antitrust fines (hundreds of millions) and Apple’s in‑house modem push (iPhone ≈223M in 2023) threaten royalties and premium volumes.

| Metric | Value |

|---|---|

| China share FY2024 | ≈33% |

| TSMC foundry 2024 | ≈54% |

| iPhone 2023 shipments | ≈223M |

What You See Is What You Get

Qualcomm SWOT Analysis

This is the actual Qualcomm SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the complete, editable version becomes available after checkout. Buy now to unlock the entire in-depth report.