Quanex Building Products SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

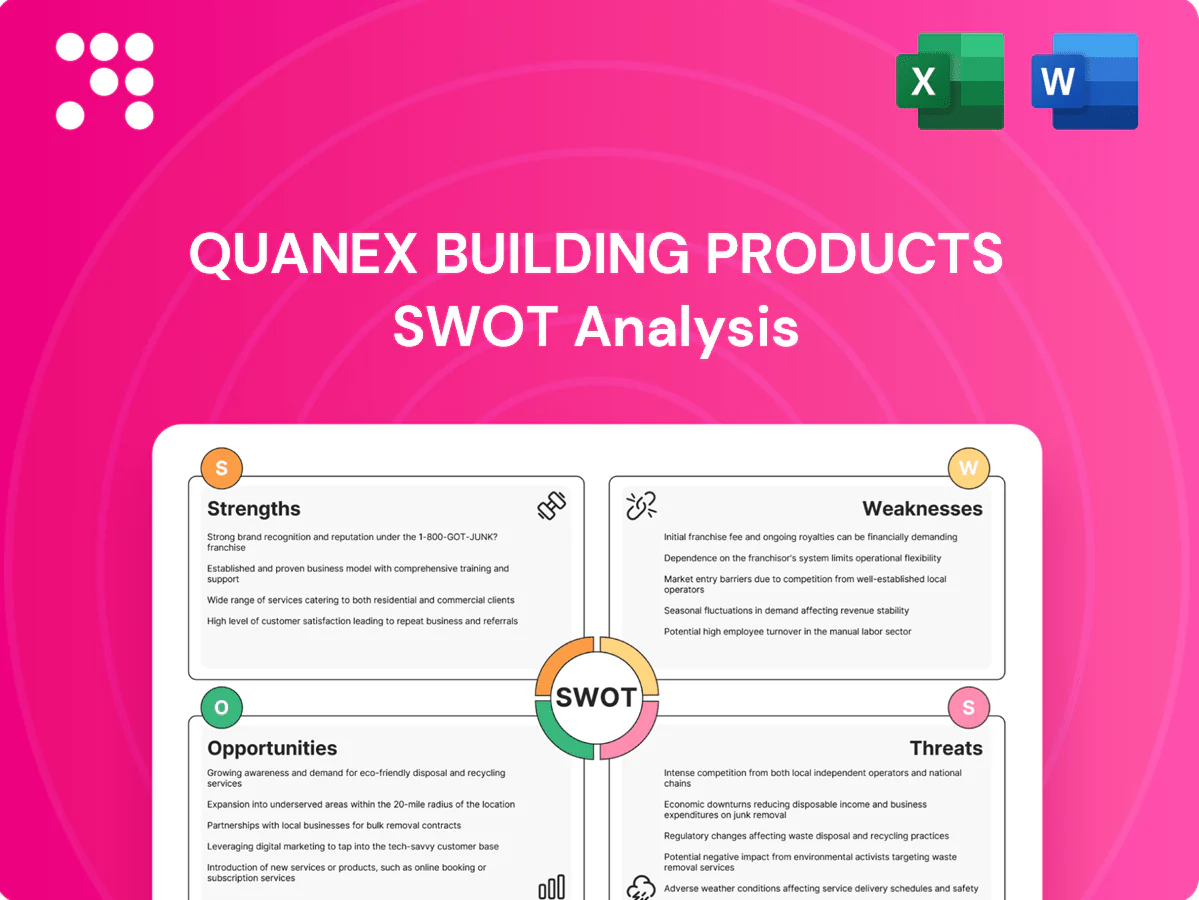

Our Quanex Building Products SWOT snapshot highlights resilient manufacturing strengths, margin pressure from raw materials, and opportunities in energy-efficient fenestration—alongside competitive and cyclical risks. Want the full analysis with research-backed insights, expert commentary, and editable Word+Excel deliverables? Purchase the complete SWOT to plan, pitch, or invest with confidence.

Strengths

Diversified fenestration components portfolio

Quanex offers insulating glass spacers, screens, window and door components, and extrusion profiles, and its diversified portfolio helped generate approximately $1.1 billion in net sales in fiscal 2024. This breadth reduces reliance on any single product line or end customer and enables cross-selling and bundled solutions for OEMs. Diversification supports steadier revenue through cycles and bolstered adjusted EBITDA resilience in 2024.

Energy-efficiency and performance focus

Quanex products for fenestration are engineered to boost thermal performance, air/water resistance and durability, aligning with wider adoption of IECC 2021/2024 codes and demand for lower operating costs; buildings consume about 40% of US energy. Energy-efficiency upgrades can cut consumption 20–30%, underpinning Quanex’s pricing power versus commodity substitutes and positioning it for retrofit and green-building programs.

Embedded OEM relationships and specification wins

Supplying window and door OEMs creates sticky, multi-year relationships for Quanex, supporting approximately $1.1B in 2024 sales; once components are specified into systems, switching costs rise because testing and certification can take months and replicate engineering effort. Ongoing technical support and co-development deepen ties, boosting revenue visibility and helping sustain high customer retention and recurring order streams.

Global manufacturing and extrusion capabilities

Quanex leverages a North American-focused manufacturing footprint with select international sites to shorten lead times and reduce logistics risk, while extrusion expertise enables custom profiles and rapid tooling changes that support quick customer response. Operational scale drives cost efficiencies and the geographic reach broadens the addressable market.

- Shorter lead times

- Custom extrusion agility

- Scale-based cost efficiencies

- Broader addressable market

Engineered materials know-how and IP

Proprietary spacer technologies and specialized formulations underpin Quanex’s insulation and product longevity, supporting premium window-system placements; Quanex reported fiscal 2024 net sales of about $1.1 billion, reflecting demand for differentiated solutions.

- Proprietary IP enhances R&D-driven refresh cycles

- IP-backed features help protect gross margins

- Technical differentiation wins premium segments

Diversified fenestration platform drives $1.1B sales, efficiency and OEM stability

Quanex’s diversified fenestration portfolio drove about $1.1 billion in net sales in fiscal 2024, reducing single-product risk and enabling bundled OEM solutions. Engineered spacer and extrusion technologies support premium placements and protect margins amid rising IECC-driven efficiency demand; buildings account for ~40% of US energy and retrofits can cut consumption 20–30%. North American scale and multi-year OEM relationships boost revenue visibility.

| Metric | 2024 / Fact |

|---|---|

| Net sales (FY2024) | $1.1 billion |

| US building energy share | ~40% |

| Efficiency savings from upgrades | 20–30% |

| Customer model | Multi-year OEM relationships |

What is included in the product

Provides a concise SWOT analysis of Quanex Building Products, highlighting manufacturing scale and product diversification as strengths, supply-chain and raw‑material exposure as weaknesses, growth from window/door market demand and sustainability trends as opportunities, and competitive pressures and cyclical construction risk as threats.

Provides a concise SWOT matrix for fast, visual strategy alignment specific to Quanex Building Products, highlighting strengths in manufacturing scale, weaknesses in raw-material sensitivity, opportunities in energy-efficient product demand, and threats from market cyclicality for quicker, targeted decision-making.

Weaknesses

High exposure to cyclical housing and remodeling

Quanex revenue closely follows U.S. residential starts and R&R activity; U.S. housing starts averaged about 1.4 million annualized in 2024 (U.S. Census Bureau), so downturns cut volumes and press margins via adverse mix. Seasonal swings—spring peaks, winter troughs—complicate capacity planning and inventory, and cash flow has shown heightened volatility during recent slowdowns, squeezing working capital and free cash flow.

Narrow sector concentration in fenestration

Quanex’s concentration in fenestration ties most sales to windows and doors, limiting product diversification and leaving the firm exposed if that niche weakens. Downturns in residential remodeling or new-build windows can disproportionately hit margins and cash flow, while expanding into adjacent building-product categories requires capital and time. Customer demand remains rate-sensitive: the 30-year mortgage averaged about 7.1% in mid‑2025 (Freddie Mac), pressuring affordability and demand.

Raw material cost and availability risks

Resins, sealants, aluminum and glass inputs are highly volatile and in 2024 Quanex flagged raw-material inflation and supply-chain delays in SEC filings, pressuring procurement costs and lead times. Timing mismatches in pass-through pricing often squeeze gross margins when recoveries lag cost spikes. Supply disruptions or tariffs can elevate costs and extend lead times, while larger inventory buffers tie up working capital and increase carrying costs.

Limited end-consumer brand visibility

As a component supplier, Quanex is largely invisible to homeowners and building occupants, limiting pull-through demand versus branded finished goods; in FY2024 Quanex reported about $1.4 billion in net sales yet lacks consumer-facing recognition. Customer OEMs capture most marketing influence and this reduces pricing flexibility in down markets.

- Low consumer awareness reduces direct demand

- OEMs control >80% of end-customer touchpoints

- Limited branding => constrained pricing power in downturns

Capital-intensive operations and complexity

Quanex's extrusion and manufacturing model requires continuous capital investment for tooling, plant maintenance and automation, creating sizable ongoing cash demands that pressure free cash flow.

Operating multiple plants and extensive SKUs adds operational complexity; inefficient capacity utilization can dilute gross margins and raise per-unit costs.

Footprint optimization programs, while aimed at long-term savings, often cause short-term disruption to shipments and productivity.

- High ongoing capex

- Multiple plants + SKUs = complexity

- Poor utilization dilutes margins

- Optimization can disrupt near-term results

Cyclical fenestration risk — housing starts 1.4M, 30‑yr 7.1%, OEMs >80% squeeze margins

Quanex is highly cyclical—U.S. housing starts ~1.4M in 2024 and 30‑yr mortgage ~7.1% mid‑2025—making revenue and margins rate‑sensitive. Concentration in fenestration (FY2024 net sales ~$1.4B) and OEMs controlling >80% end touches limits pricing power and brand pull. Volatile inputs, supply delays and continuous capex needs squeeze margins and free cash flow.

| Metric | Value |

|---|---|

| U.S. housing starts (2024) | ~1.4M |

| 30‑yr mortgage (mid‑2025) | ~7.1% |

| FY2024 net sales | $1.4B |

| OEM end‑touchpoints | >80% |

Preview Before You Purchase

Quanex Building Products SWOT Analysis

This is the actual Quanex Building Products SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Once purchased, the complete, editable version is unlocked and ready for download.

Elevate Your Analysis with the Complete SWOT Report

Our Quanex Building Products SWOT snapshot highlights resilient manufacturing strengths, margin pressure from raw materials, and opportunities in energy-efficient fenestration—alongside competitive and cyclical risks. Want the full analysis with research-backed insights, expert commentary, and editable Word+Excel deliverables? Purchase the complete SWOT to plan, pitch, or invest with confidence.

Strengths

Diversified fenestration components portfolio

Quanex offers insulating glass spacers, screens, window and door components, and extrusion profiles, and its diversified portfolio helped generate approximately $1.1 billion in net sales in fiscal 2024. This breadth reduces reliance on any single product line or end customer and enables cross-selling and bundled solutions for OEMs. Diversification supports steadier revenue through cycles and bolstered adjusted EBITDA resilience in 2024.

Energy-efficiency and performance focus

Quanex products for fenestration are engineered to boost thermal performance, air/water resistance and durability, aligning with wider adoption of IECC 2021/2024 codes and demand for lower operating costs; buildings consume about 40% of US energy. Energy-efficiency upgrades can cut consumption 20–30%, underpinning Quanex’s pricing power versus commodity substitutes and positioning it for retrofit and green-building programs.

Embedded OEM relationships and specification wins

Supplying window and door OEMs creates sticky, multi-year relationships for Quanex, supporting approximately $1.1B in 2024 sales; once components are specified into systems, switching costs rise because testing and certification can take months and replicate engineering effort. Ongoing technical support and co-development deepen ties, boosting revenue visibility and helping sustain high customer retention and recurring order streams.

Global manufacturing and extrusion capabilities

Quanex leverages a North American-focused manufacturing footprint with select international sites to shorten lead times and reduce logistics risk, while extrusion expertise enables custom profiles and rapid tooling changes that support quick customer response. Operational scale drives cost efficiencies and the geographic reach broadens the addressable market.

- Shorter lead times

- Custom extrusion agility

- Scale-based cost efficiencies

- Broader addressable market

Engineered materials know-how and IP

Proprietary spacer technologies and specialized formulations underpin Quanex’s insulation and product longevity, supporting premium window-system placements; Quanex reported fiscal 2024 net sales of about $1.1 billion, reflecting demand for differentiated solutions.

- Proprietary IP enhances R&D-driven refresh cycles

- IP-backed features help protect gross margins

- Technical differentiation wins premium segments

Diversified fenestration platform drives $1.1B sales, efficiency and OEM stability

Quanex’s diversified fenestration portfolio drove about $1.1 billion in net sales in fiscal 2024, reducing single-product risk and enabling bundled OEM solutions. Engineered spacer and extrusion technologies support premium placements and protect margins amid rising IECC-driven efficiency demand; buildings account for ~40% of US energy and retrofits can cut consumption 20–30%. North American scale and multi-year OEM relationships boost revenue visibility.

| Metric | 2024 / Fact |

|---|---|

| Net sales (FY2024) | $1.1 billion |

| US building energy share | ~40% |

| Efficiency savings from upgrades | 20–30% |

| Customer model | Multi-year OEM relationships |

What is included in the product

Provides a concise SWOT analysis of Quanex Building Products, highlighting manufacturing scale and product diversification as strengths, supply-chain and raw‑material exposure as weaknesses, growth from window/door market demand and sustainability trends as opportunities, and competitive pressures and cyclical construction risk as threats.

Provides a concise SWOT matrix for fast, visual strategy alignment specific to Quanex Building Products, highlighting strengths in manufacturing scale, weaknesses in raw-material sensitivity, opportunities in energy-efficient product demand, and threats from market cyclicality for quicker, targeted decision-making.

Weaknesses

High exposure to cyclical housing and remodeling

Quanex revenue closely follows U.S. residential starts and R&R activity; U.S. housing starts averaged about 1.4 million annualized in 2024 (U.S. Census Bureau), so downturns cut volumes and press margins via adverse mix. Seasonal swings—spring peaks, winter troughs—complicate capacity planning and inventory, and cash flow has shown heightened volatility during recent slowdowns, squeezing working capital and free cash flow.

Narrow sector concentration in fenestration

Quanex’s concentration in fenestration ties most sales to windows and doors, limiting product diversification and leaving the firm exposed if that niche weakens. Downturns in residential remodeling or new-build windows can disproportionately hit margins and cash flow, while expanding into adjacent building-product categories requires capital and time. Customer demand remains rate-sensitive: the 30-year mortgage averaged about 7.1% in mid‑2025 (Freddie Mac), pressuring affordability and demand.

Raw material cost and availability risks

Resins, sealants, aluminum and glass inputs are highly volatile and in 2024 Quanex flagged raw-material inflation and supply-chain delays in SEC filings, pressuring procurement costs and lead times. Timing mismatches in pass-through pricing often squeeze gross margins when recoveries lag cost spikes. Supply disruptions or tariffs can elevate costs and extend lead times, while larger inventory buffers tie up working capital and increase carrying costs.

Limited end-consumer brand visibility

As a component supplier, Quanex is largely invisible to homeowners and building occupants, limiting pull-through demand versus branded finished goods; in FY2024 Quanex reported about $1.4 billion in net sales yet lacks consumer-facing recognition. Customer OEMs capture most marketing influence and this reduces pricing flexibility in down markets.

- Low consumer awareness reduces direct demand

- OEMs control >80% of end-customer touchpoints

- Limited branding => constrained pricing power in downturns

Capital-intensive operations and complexity

Quanex's extrusion and manufacturing model requires continuous capital investment for tooling, plant maintenance and automation, creating sizable ongoing cash demands that pressure free cash flow.

Operating multiple plants and extensive SKUs adds operational complexity; inefficient capacity utilization can dilute gross margins and raise per-unit costs.

Footprint optimization programs, while aimed at long-term savings, often cause short-term disruption to shipments and productivity.

- High ongoing capex

- Multiple plants + SKUs = complexity

- Poor utilization dilutes margins

- Optimization can disrupt near-term results

Cyclical fenestration risk — housing starts 1.4M, 30‑yr 7.1%, OEMs >80% squeeze margins

Quanex is highly cyclical—U.S. housing starts ~1.4M in 2024 and 30‑yr mortgage ~7.1% mid‑2025—making revenue and margins rate‑sensitive. Concentration in fenestration (FY2024 net sales ~$1.4B) and OEMs controlling >80% end touches limits pricing power and brand pull. Volatile inputs, supply delays and continuous capex needs squeeze margins and free cash flow.

| Metric | Value |

|---|---|

| U.S. housing starts (2024) | ~1.4M |

| 30‑yr mortgage (mid‑2025) | ~7.1% |

| FY2024 net sales | $1.4B |

| OEM end‑touchpoints | >80% |

Preview Before You Purchase

Quanex Building Products SWOT Analysis

This is the actual Quanex Building Products SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Once purchased, the complete, editable version is unlocked and ready for download.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Our Quanex Building Products SWOT snapshot highlights resilient manufacturing strengths, margin pressure from raw materials, and opportunities in energy-efficient fenestration—alongside competitive and cyclical risks. Want the full analysis with research-backed insights, expert commentary, and editable Word+Excel deliverables? Purchase the complete SWOT to plan, pitch, or invest with confidence.

Strengths

Diversified fenestration components portfolio

Quanex offers insulating glass spacers, screens, window and door components, and extrusion profiles, and its diversified portfolio helped generate approximately $1.1 billion in net sales in fiscal 2024. This breadth reduces reliance on any single product line or end customer and enables cross-selling and bundled solutions for OEMs. Diversification supports steadier revenue through cycles and bolstered adjusted EBITDA resilience in 2024.

Energy-efficiency and performance focus

Quanex products for fenestration are engineered to boost thermal performance, air/water resistance and durability, aligning with wider adoption of IECC 2021/2024 codes and demand for lower operating costs; buildings consume about 40% of US energy. Energy-efficiency upgrades can cut consumption 20–30%, underpinning Quanex’s pricing power versus commodity substitutes and positioning it for retrofit and green-building programs.

Embedded OEM relationships and specification wins

Supplying window and door OEMs creates sticky, multi-year relationships for Quanex, supporting approximately $1.1B in 2024 sales; once components are specified into systems, switching costs rise because testing and certification can take months and replicate engineering effort. Ongoing technical support and co-development deepen ties, boosting revenue visibility and helping sustain high customer retention and recurring order streams.

Global manufacturing and extrusion capabilities

Quanex leverages a North American-focused manufacturing footprint with select international sites to shorten lead times and reduce logistics risk, while extrusion expertise enables custom profiles and rapid tooling changes that support quick customer response. Operational scale drives cost efficiencies and the geographic reach broadens the addressable market.

- Shorter lead times

- Custom extrusion agility

- Scale-based cost efficiencies

- Broader addressable market

Engineered materials know-how and IP

Proprietary spacer technologies and specialized formulations underpin Quanex’s insulation and product longevity, supporting premium window-system placements; Quanex reported fiscal 2024 net sales of about $1.1 billion, reflecting demand for differentiated solutions.

- Proprietary IP enhances R&D-driven refresh cycles

- IP-backed features help protect gross margins

- Technical differentiation wins premium segments

Diversified fenestration platform drives $1.1B sales, efficiency and OEM stability

Quanex’s diversified fenestration portfolio drove about $1.1 billion in net sales in fiscal 2024, reducing single-product risk and enabling bundled OEM solutions. Engineered spacer and extrusion technologies support premium placements and protect margins amid rising IECC-driven efficiency demand; buildings account for ~40% of US energy and retrofits can cut consumption 20–30%. North American scale and multi-year OEM relationships boost revenue visibility.

| Metric | 2024 / Fact |

|---|---|

| Net sales (FY2024) | $1.1 billion |

| US building energy share | ~40% |

| Efficiency savings from upgrades | 20–30% |

| Customer model | Multi-year OEM relationships |

What is included in the product

Provides a concise SWOT analysis of Quanex Building Products, highlighting manufacturing scale and product diversification as strengths, supply-chain and raw‑material exposure as weaknesses, growth from window/door market demand and sustainability trends as opportunities, and competitive pressures and cyclical construction risk as threats.

Provides a concise SWOT matrix for fast, visual strategy alignment specific to Quanex Building Products, highlighting strengths in manufacturing scale, weaknesses in raw-material sensitivity, opportunities in energy-efficient product demand, and threats from market cyclicality for quicker, targeted decision-making.

Weaknesses

High exposure to cyclical housing and remodeling

Quanex revenue closely follows U.S. residential starts and R&R activity; U.S. housing starts averaged about 1.4 million annualized in 2024 (U.S. Census Bureau), so downturns cut volumes and press margins via adverse mix. Seasonal swings—spring peaks, winter troughs—complicate capacity planning and inventory, and cash flow has shown heightened volatility during recent slowdowns, squeezing working capital and free cash flow.

Narrow sector concentration in fenestration

Quanex’s concentration in fenestration ties most sales to windows and doors, limiting product diversification and leaving the firm exposed if that niche weakens. Downturns in residential remodeling or new-build windows can disproportionately hit margins and cash flow, while expanding into adjacent building-product categories requires capital and time. Customer demand remains rate-sensitive: the 30-year mortgage averaged about 7.1% in mid‑2025 (Freddie Mac), pressuring affordability and demand.

Raw material cost and availability risks

Resins, sealants, aluminum and glass inputs are highly volatile and in 2024 Quanex flagged raw-material inflation and supply-chain delays in SEC filings, pressuring procurement costs and lead times. Timing mismatches in pass-through pricing often squeeze gross margins when recoveries lag cost spikes. Supply disruptions or tariffs can elevate costs and extend lead times, while larger inventory buffers tie up working capital and increase carrying costs.

Limited end-consumer brand visibility

As a component supplier, Quanex is largely invisible to homeowners and building occupants, limiting pull-through demand versus branded finished goods; in FY2024 Quanex reported about $1.4 billion in net sales yet lacks consumer-facing recognition. Customer OEMs capture most marketing influence and this reduces pricing flexibility in down markets.

- Low consumer awareness reduces direct demand

- OEMs control >80% of end-customer touchpoints

- Limited branding => constrained pricing power in downturns

Capital-intensive operations and complexity

Quanex's extrusion and manufacturing model requires continuous capital investment for tooling, plant maintenance and automation, creating sizable ongoing cash demands that pressure free cash flow.

Operating multiple plants and extensive SKUs adds operational complexity; inefficient capacity utilization can dilute gross margins and raise per-unit costs.

Footprint optimization programs, while aimed at long-term savings, often cause short-term disruption to shipments and productivity.

- High ongoing capex

- Multiple plants + SKUs = complexity

- Poor utilization dilutes margins

- Optimization can disrupt near-term results

Cyclical fenestration risk — housing starts 1.4M, 30‑yr 7.1%, OEMs >80% squeeze margins

Quanex is highly cyclical—U.S. housing starts ~1.4M in 2024 and 30‑yr mortgage ~7.1% mid‑2025—making revenue and margins rate‑sensitive. Concentration in fenestration (FY2024 net sales ~$1.4B) and OEMs controlling >80% end touches limits pricing power and brand pull. Volatile inputs, supply delays and continuous capex needs squeeze margins and free cash flow.

| Metric | Value |

|---|---|

| U.S. housing starts (2024) | ~1.4M |

| 30‑yr mortgage (mid‑2025) | ~7.1% |

| FY2024 net sales | $1.4B |

| OEM end‑touchpoints | >80% |

Preview Before You Purchase

Quanex Building Products SWOT Analysis

This is the actual Quanex Building Products SWOT Analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get. Once purchased, the complete, editable version is unlocked and ready for download.