Quanta Services PESTLE Analysis

Your Shortcut to Market Insight Starts Here

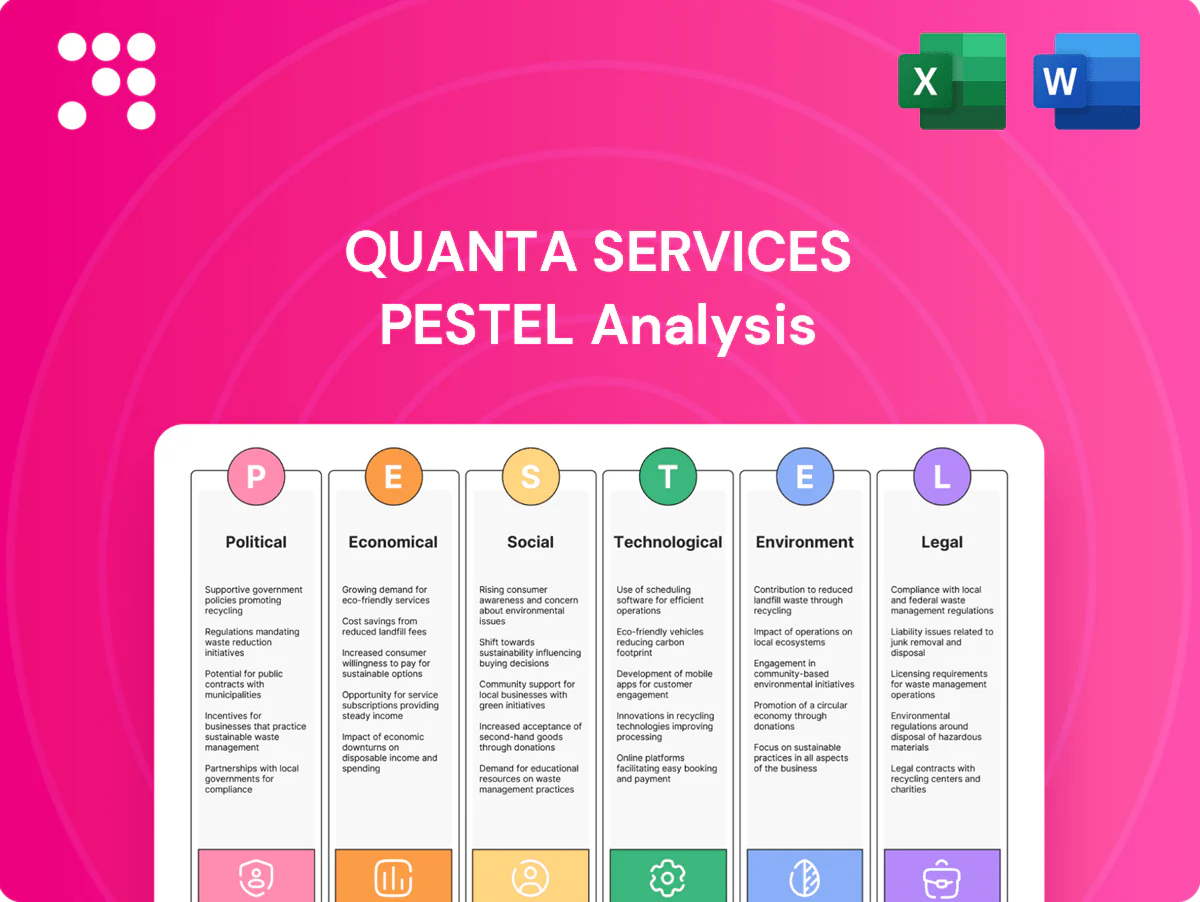

Gain a competitive edge with our PESTLE analysis of Quanta Services. Explore how political, economic, social, technological, legal, and environmental forces reshape its strategy and risk profile. Purchase the full, ready-to-use report for actionable insights, editable files, and instant download to power investment or strategic decisions.

Political factors

Infrastructure funding and public policy

Federal infrastructure law totals about 1.2 trillion dollars with roughly 550 billion in new spending, and the BEAD program earmarks 42.45 billion for broadband, driving multi-year utility and broadband demand. Federal and state grants for grid hardening and rural broadband expand Quanta’s addressable market. Shifts in administration priorities can reallocate funds among electric, communications and pipeline projects, while appropriations stability and grant timing directly affect backlog visibility.

Energy transition and grid modernization mandates

State renewable portfolio standards in over 30 states plus federal incentives (IRA, BIL) are accelerating T&D upgrades, feeding a US interconnection queue exceeding 2,000 GW and driving demand for EPC work by firms like Quanta. Policies easing interconnection of renewables, storage and EVs force expanded EPC capabilities across transmission, substation and distribution scopes. Rollbacks or delays in clean‑energy policy would directly throttle project pipelines. Regional politics remain decisive for siting of the ~60,000 miles of new transmission NREL estimates needed by 2030.

Permitting and right‑of‑way governance

Federal, state, tribal and municipal permitting regimes materially affect schedule and cost, with transmission and corridor projects commonly facing 2–5 year permitting delays that raise capital and carrying costs. Streamlined federal approvals under post‑2021 infrastructure policy can unlock multi‑billion‑dollar corridors, while political pushes to reform NEPA‑type processes aim to shorten timelines. Increasingly, community‑benefit agreements serve as political conditions of approval, adding negotiated cost or schedule obligations.

Telecom and broadband initiatives

- BEAD 42.45B

- C‑band 80.9B

- Pole/make‑ready impacts timelines/costs

- Funding shifts reprioritize areas/tech

Trade, immigration, and labor mobility

Visas and the H-2B cap of 66,000, plus prevailing‑wage enforcement, limit Quanta’s access to skilled linemen and technicians, affecting project staffing and margins. Tariffs such as the Section 232 steel levy (25%) and duties on transformers/electronics raise material costs and pressure bids. Expanded Buy America rules from the Bipartisan Infrastructure Law (about $550 billion new investment) force reshoring of supply chains. Political scrutiny of pipelines curtails some fossil projects while DOE estimates ~97 billion dollars needed for transmission to 2030, boosting electrification work.

- Visas/H-2B: 66,000 cap

- Prevailing wage: higher labor costs, compliance risk

- Tariffs: 25% steel Section 232

- Buy America: driven by $550B BIL spend

- Energy politics: pipeline limits vs ~$97B transmission need

BEAD 42.45B, BIL ~550B drive T&D + broadband buildout

Federal BEAD 42.45B and BIL ~$550B drive multi‑year utility and broadband demand while state RPS and IRA incentives push T&D and interconnection work (>2,000 GW queue). Permitting, pole/make‑ready and Buy America rules reshape schedules and supply chains; visas/H‑2B (66,000 cap), prevailing wage and tariffs (steel 25%) constrain labor and material costs.

| Metric | Value |

|---|---|

| BEAD | 42.45B |

| BIL new spend | ~550B |

| C‑band auction | 80.9B |

| H‑2B cap | 66,000 |

| Steel tariff (Sec232) | 25% |

| US transmission need | ~97B to 2030 |

| Interconnection queue | >2,000 GW |

What is included in the product

Provides a concise PESTLE evaluation of Quanta Services across Political, Economic, Social, Technological, Environmental, and Legal dimensions, grounded in current data and industry trends to reveal key risks and opportunities. Designed for executives and investors, the analysis is region- and sector-specific, forward-looking, and formatted for direct inclusion in reports, plans, or decks.

Clean, visually segmented PESTLE summary tailored to Quanta Services that’s easily dropped into presentations or shared across teams to streamline external risk discussions and alignment during planning sessions.

Economic factors

Utility and carrier capex cycles

Client spending by electric utilities, pipelines and communications providers underpins Quanta Services revenue, with U.S. T&D investment running above $50 billion annually and pipeline/comms capex rising alongside electrification and fiber builds. Grid reliability needs and surging data demand (IP traffic ~30% y/y in 2023) support sustained investment, though cycles can pause in macro slowdowns that defer discretionary upgrades. Visibility into demand improves through multi‑year frameworks and master service agreements that lock in work and margins.

Interest rates and financing costs

Higher benchmark rates — US Fed funds near 5.25–5.50% and the 10‑yr Treasury around 4.2% in mid‑2025 — raise utilities’ cost of capital and can delay transmission and fiber projects; easing would reaccelerate builds. Quanta’s bonding and working‑capital costs fluctuate with credit spreads and market rates, squeezing margins when rates climb. Long‑dated EPC contracts perform best in stable rate environments.

Inflation and input costs

Rising labor (wage growth ~4–5% Y/Y in 2024), steel (HRC volatility ±15–25% since 2022), diesel and equipment inflation have compressed Quanta margins. Escalation clauses and cost‑plus contracts have mitigated pass‑through risk on large projects. Transformer and cable lead times stretched to ~30–52 weeks, heightening schedule risk. Proactive procurement, supplier diversification and fuel/commodity hedges preserve project profitability.

Labor market tightness

Skilled craft labor scarcity constrains Quanta Services growth and elevates wage bills amid tight U.S. labor conditions (national unemployment ~3.9% in 2024), making training pipelines and apprenticeships key talent differentiators. Competition from mega-projects raises turnover risk, while productivity tools and strict scheduling discipline help offset cost pressures and preserve margins.

- Skilled labor shortage raises wages

- Apprenticeships improve retention

- Mega-project competition increases churn

- Productivity tools cut cost impact

Commodity and energy price dynamics

Oil and gas price swings (Brent ranged roughly $60–120/bbl since 2022, averaging near $86/bbl in 2024) directly affect pipeline maintenance and integrity budgets, while power price signals and rising ERCOT/CAISO volatility drive renewed transmission and renewable build‑outs. Fuel cost swings (U.S. diesel ~4.10/gal in 2024) raise fleet and equipment operating expenses; Quanta’s diversified 2024 revenue (~$14.7B) helps smooth segment volatility.

- Impact: pipeline OPEX capex sensitivity

- Signal: power prices influence T&D and renewables

- Cost: diesel volatility uplifts fleet expenses

- Mitigation: segment diversification reduces revenue swings

BEAD 42.45B, BIL ~550B drive T&D + broadband buildout

Quanta revenue depends on utility, pipeline and comms capex (U.S. T&D >$50B/yr) with 2024 revenue ~$14.7B; macro slowdowns can defer projects. Higher rates (Fed funds ~5.25–5.50%, 10‑yr ~4.2% mid‑2025) and rising input costs (wage growth 4–5% Y/Y, Brent ~$86/bbl, diesel ~$4.10/gal) pressure margins; contract terms and diversification mitigate risk.

| Metric | 2024/2025 |

|---|---|

| Quanta revenue | $14.7B (2024) |

| U.S. T&D spend | >$50B/yr |

| Fed funds | 5.25–5.50% (mid‑2025) |

| 10‑yr Treasury | ~4.2% (mid‑2025) |

| Wage growth | 4–5% Y/Y (2024) |

| Brent | ~$86/bbl (2024) |

| Diesel | ~$4.10/gal (2024) |

Full Version Awaits

Quanta Services PESTLE Analysis

The preview shown here is the exact Quanta Services PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with actionable insights. No placeholders or teasers—this is the finished, download-ready file.

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our PESTLE analysis of Quanta Services. Explore how political, economic, social, technological, legal, and environmental forces reshape its strategy and risk profile. Purchase the full, ready-to-use report for actionable insights, editable files, and instant download to power investment or strategic decisions.

Political factors

Infrastructure funding and public policy

Federal infrastructure law totals about 1.2 trillion dollars with roughly 550 billion in new spending, and the BEAD program earmarks 42.45 billion for broadband, driving multi-year utility and broadband demand. Federal and state grants for grid hardening and rural broadband expand Quanta’s addressable market. Shifts in administration priorities can reallocate funds among electric, communications and pipeline projects, while appropriations stability and grant timing directly affect backlog visibility.

Energy transition and grid modernization mandates

State renewable portfolio standards in over 30 states plus federal incentives (IRA, BIL) are accelerating T&D upgrades, feeding a US interconnection queue exceeding 2,000 GW and driving demand for EPC work by firms like Quanta. Policies easing interconnection of renewables, storage and EVs force expanded EPC capabilities across transmission, substation and distribution scopes. Rollbacks or delays in clean‑energy policy would directly throttle project pipelines. Regional politics remain decisive for siting of the ~60,000 miles of new transmission NREL estimates needed by 2030.

Permitting and right‑of‑way governance

Federal, state, tribal and municipal permitting regimes materially affect schedule and cost, with transmission and corridor projects commonly facing 2–5 year permitting delays that raise capital and carrying costs. Streamlined federal approvals under post‑2021 infrastructure policy can unlock multi‑billion‑dollar corridors, while political pushes to reform NEPA‑type processes aim to shorten timelines. Increasingly, community‑benefit agreements serve as political conditions of approval, adding negotiated cost or schedule obligations.

Telecom and broadband initiatives

- BEAD 42.45B

- C‑band 80.9B

- Pole/make‑ready impacts timelines/costs

- Funding shifts reprioritize areas/tech

Trade, immigration, and labor mobility

Visas and the H-2B cap of 66,000, plus prevailing‑wage enforcement, limit Quanta’s access to skilled linemen and technicians, affecting project staffing and margins. Tariffs such as the Section 232 steel levy (25%) and duties on transformers/electronics raise material costs and pressure bids. Expanded Buy America rules from the Bipartisan Infrastructure Law (about $550 billion new investment) force reshoring of supply chains. Political scrutiny of pipelines curtails some fossil projects while DOE estimates ~97 billion dollars needed for transmission to 2030, boosting electrification work.

- Visas/H-2B: 66,000 cap

- Prevailing wage: higher labor costs, compliance risk

- Tariffs: 25% steel Section 232

- Buy America: driven by $550B BIL spend

- Energy politics: pipeline limits vs ~$97B transmission need

BEAD 42.45B, BIL ~550B drive T&D + broadband buildout

Federal BEAD 42.45B and BIL ~$550B drive multi‑year utility and broadband demand while state RPS and IRA incentives push T&D and interconnection work (>2,000 GW queue). Permitting, pole/make‑ready and Buy America rules reshape schedules and supply chains; visas/H‑2B (66,000 cap), prevailing wage and tariffs (steel 25%) constrain labor and material costs.

| Metric | Value |

|---|---|

| BEAD | 42.45B |

| BIL new spend | ~550B |

| C‑band auction | 80.9B |

| H‑2B cap | 66,000 |

| Steel tariff (Sec232) | 25% |

| US transmission need | ~97B to 2030 |

| Interconnection queue | >2,000 GW |

What is included in the product

Provides a concise PESTLE evaluation of Quanta Services across Political, Economic, Social, Technological, Environmental, and Legal dimensions, grounded in current data and industry trends to reveal key risks and opportunities. Designed for executives and investors, the analysis is region- and sector-specific, forward-looking, and formatted for direct inclusion in reports, plans, or decks.

Clean, visually segmented PESTLE summary tailored to Quanta Services that’s easily dropped into presentations or shared across teams to streamline external risk discussions and alignment during planning sessions.

Economic factors

Utility and carrier capex cycles

Client spending by electric utilities, pipelines and communications providers underpins Quanta Services revenue, with U.S. T&D investment running above $50 billion annually and pipeline/comms capex rising alongside electrification and fiber builds. Grid reliability needs and surging data demand (IP traffic ~30% y/y in 2023) support sustained investment, though cycles can pause in macro slowdowns that defer discretionary upgrades. Visibility into demand improves through multi‑year frameworks and master service agreements that lock in work and margins.

Interest rates and financing costs

Higher benchmark rates — US Fed funds near 5.25–5.50% and the 10‑yr Treasury around 4.2% in mid‑2025 — raise utilities’ cost of capital and can delay transmission and fiber projects; easing would reaccelerate builds. Quanta’s bonding and working‑capital costs fluctuate with credit spreads and market rates, squeezing margins when rates climb. Long‑dated EPC contracts perform best in stable rate environments.

Inflation and input costs

Rising labor (wage growth ~4–5% Y/Y in 2024), steel (HRC volatility ±15–25% since 2022), diesel and equipment inflation have compressed Quanta margins. Escalation clauses and cost‑plus contracts have mitigated pass‑through risk on large projects. Transformer and cable lead times stretched to ~30–52 weeks, heightening schedule risk. Proactive procurement, supplier diversification and fuel/commodity hedges preserve project profitability.

Labor market tightness

Skilled craft labor scarcity constrains Quanta Services growth and elevates wage bills amid tight U.S. labor conditions (national unemployment ~3.9% in 2024), making training pipelines and apprenticeships key talent differentiators. Competition from mega-projects raises turnover risk, while productivity tools and strict scheduling discipline help offset cost pressures and preserve margins.

- Skilled labor shortage raises wages

- Apprenticeships improve retention

- Mega-project competition increases churn

- Productivity tools cut cost impact

Commodity and energy price dynamics

Oil and gas price swings (Brent ranged roughly $60–120/bbl since 2022, averaging near $86/bbl in 2024) directly affect pipeline maintenance and integrity budgets, while power price signals and rising ERCOT/CAISO volatility drive renewed transmission and renewable build‑outs. Fuel cost swings (U.S. diesel ~4.10/gal in 2024) raise fleet and equipment operating expenses; Quanta’s diversified 2024 revenue (~$14.7B) helps smooth segment volatility.

- Impact: pipeline OPEX capex sensitivity

- Signal: power prices influence T&D and renewables

- Cost: diesel volatility uplifts fleet expenses

- Mitigation: segment diversification reduces revenue swings

BEAD 42.45B, BIL ~550B drive T&D + broadband buildout

Quanta revenue depends on utility, pipeline and comms capex (U.S. T&D >$50B/yr) with 2024 revenue ~$14.7B; macro slowdowns can defer projects. Higher rates (Fed funds ~5.25–5.50%, 10‑yr ~4.2% mid‑2025) and rising input costs (wage growth 4–5% Y/Y, Brent ~$86/bbl, diesel ~$4.10/gal) pressure margins; contract terms and diversification mitigate risk.

| Metric | 2024/2025 |

|---|---|

| Quanta revenue | $14.7B (2024) |

| U.S. T&D spend | >$50B/yr |

| Fed funds | 5.25–5.50% (mid‑2025) |

| 10‑yr Treasury | ~4.2% (mid‑2025) |

| Wage growth | 4–5% Y/Y (2024) |

| Brent | ~$86/bbl (2024) |

| Diesel | ~$4.10/gal (2024) |

Full Version Awaits

Quanta Services PESTLE Analysis

The preview shown here is the exact Quanta Services PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with actionable insights. No placeholders or teasers—this is the finished, download-ready file.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our PESTLE analysis of Quanta Services. Explore how political, economic, social, technological, legal, and environmental forces reshape its strategy and risk profile. Purchase the full, ready-to-use report for actionable insights, editable files, and instant download to power investment or strategic decisions.

Political factors

Infrastructure funding and public policy

Federal infrastructure law totals about 1.2 trillion dollars with roughly 550 billion in new spending, and the BEAD program earmarks 42.45 billion for broadband, driving multi-year utility and broadband demand. Federal and state grants for grid hardening and rural broadband expand Quanta’s addressable market. Shifts in administration priorities can reallocate funds among electric, communications and pipeline projects, while appropriations stability and grant timing directly affect backlog visibility.

Energy transition and grid modernization mandates

State renewable portfolio standards in over 30 states plus federal incentives (IRA, BIL) are accelerating T&D upgrades, feeding a US interconnection queue exceeding 2,000 GW and driving demand for EPC work by firms like Quanta. Policies easing interconnection of renewables, storage and EVs force expanded EPC capabilities across transmission, substation and distribution scopes. Rollbacks or delays in clean‑energy policy would directly throttle project pipelines. Regional politics remain decisive for siting of the ~60,000 miles of new transmission NREL estimates needed by 2030.

Permitting and right‑of‑way governance

Federal, state, tribal and municipal permitting regimes materially affect schedule and cost, with transmission and corridor projects commonly facing 2–5 year permitting delays that raise capital and carrying costs. Streamlined federal approvals under post‑2021 infrastructure policy can unlock multi‑billion‑dollar corridors, while political pushes to reform NEPA‑type processes aim to shorten timelines. Increasingly, community‑benefit agreements serve as political conditions of approval, adding negotiated cost or schedule obligations.

Telecom and broadband initiatives

- BEAD 42.45B

- C‑band 80.9B

- Pole/make‑ready impacts timelines/costs

- Funding shifts reprioritize areas/tech

Trade, immigration, and labor mobility

Visas and the H-2B cap of 66,000, plus prevailing‑wage enforcement, limit Quanta’s access to skilled linemen and technicians, affecting project staffing and margins. Tariffs such as the Section 232 steel levy (25%) and duties on transformers/electronics raise material costs and pressure bids. Expanded Buy America rules from the Bipartisan Infrastructure Law (about $550 billion new investment) force reshoring of supply chains. Political scrutiny of pipelines curtails some fossil projects while DOE estimates ~97 billion dollars needed for transmission to 2030, boosting electrification work.

- Visas/H-2B: 66,000 cap

- Prevailing wage: higher labor costs, compliance risk

- Tariffs: 25% steel Section 232

- Buy America: driven by $550B BIL spend

- Energy politics: pipeline limits vs ~$97B transmission need

BEAD 42.45B, BIL ~550B drive T&D + broadband buildout

Federal BEAD 42.45B and BIL ~$550B drive multi‑year utility and broadband demand while state RPS and IRA incentives push T&D and interconnection work (>2,000 GW queue). Permitting, pole/make‑ready and Buy America rules reshape schedules and supply chains; visas/H‑2B (66,000 cap), prevailing wage and tariffs (steel 25%) constrain labor and material costs.

| Metric | Value |

|---|---|

| BEAD | 42.45B |

| BIL new spend | ~550B |

| C‑band auction | 80.9B |

| H‑2B cap | 66,000 |

| Steel tariff (Sec232) | 25% |

| US transmission need | ~97B to 2030 |

| Interconnection queue | >2,000 GW |

What is included in the product

Provides a concise PESTLE evaluation of Quanta Services across Political, Economic, Social, Technological, Environmental, and Legal dimensions, grounded in current data and industry trends to reveal key risks and opportunities. Designed for executives and investors, the analysis is region- and sector-specific, forward-looking, and formatted for direct inclusion in reports, plans, or decks.

Clean, visually segmented PESTLE summary tailored to Quanta Services that’s easily dropped into presentations or shared across teams to streamline external risk discussions and alignment during planning sessions.

Economic factors

Utility and carrier capex cycles

Client spending by electric utilities, pipelines and communications providers underpins Quanta Services revenue, with U.S. T&D investment running above $50 billion annually and pipeline/comms capex rising alongside electrification and fiber builds. Grid reliability needs and surging data demand (IP traffic ~30% y/y in 2023) support sustained investment, though cycles can pause in macro slowdowns that defer discretionary upgrades. Visibility into demand improves through multi‑year frameworks and master service agreements that lock in work and margins.

Interest rates and financing costs

Higher benchmark rates — US Fed funds near 5.25–5.50% and the 10‑yr Treasury around 4.2% in mid‑2025 — raise utilities’ cost of capital and can delay transmission and fiber projects; easing would reaccelerate builds. Quanta’s bonding and working‑capital costs fluctuate with credit spreads and market rates, squeezing margins when rates climb. Long‑dated EPC contracts perform best in stable rate environments.

Inflation and input costs

Rising labor (wage growth ~4–5% Y/Y in 2024), steel (HRC volatility ±15–25% since 2022), diesel and equipment inflation have compressed Quanta margins. Escalation clauses and cost‑plus contracts have mitigated pass‑through risk on large projects. Transformer and cable lead times stretched to ~30–52 weeks, heightening schedule risk. Proactive procurement, supplier diversification and fuel/commodity hedges preserve project profitability.

Labor market tightness

Skilled craft labor scarcity constrains Quanta Services growth and elevates wage bills amid tight U.S. labor conditions (national unemployment ~3.9% in 2024), making training pipelines and apprenticeships key talent differentiators. Competition from mega-projects raises turnover risk, while productivity tools and strict scheduling discipline help offset cost pressures and preserve margins.

- Skilled labor shortage raises wages

- Apprenticeships improve retention

- Mega-project competition increases churn

- Productivity tools cut cost impact

Commodity and energy price dynamics

Oil and gas price swings (Brent ranged roughly $60–120/bbl since 2022, averaging near $86/bbl in 2024) directly affect pipeline maintenance and integrity budgets, while power price signals and rising ERCOT/CAISO volatility drive renewed transmission and renewable build‑outs. Fuel cost swings (U.S. diesel ~4.10/gal in 2024) raise fleet and equipment operating expenses; Quanta’s diversified 2024 revenue (~$14.7B) helps smooth segment volatility.

- Impact: pipeline OPEX capex sensitivity

- Signal: power prices influence T&D and renewables

- Cost: diesel volatility uplifts fleet expenses

- Mitigation: segment diversification reduces revenue swings

BEAD 42.45B, BIL ~550B drive T&D + broadband buildout

Quanta revenue depends on utility, pipeline and comms capex (U.S. T&D >$50B/yr) with 2024 revenue ~$14.7B; macro slowdowns can defer projects. Higher rates (Fed funds ~5.25–5.50%, 10‑yr ~4.2% mid‑2025) and rising input costs (wage growth 4–5% Y/Y, Brent ~$86/bbl, diesel ~$4.10/gal) pressure margins; contract terms and diversification mitigate risk.

| Metric | 2024/2025 |

|---|---|

| Quanta revenue | $14.7B (2024) |

| U.S. T&D spend | >$50B/yr |

| Fed funds | 5.25–5.50% (mid‑2025) |

| 10‑yr Treasury | ~4.2% (mid‑2025) |

| Wage growth | 4–5% Y/Y (2024) |

| Brent | ~$86/bbl (2024) |

| Diesel | ~$4.10/gal (2024) |

Full Version Awaits

Quanta Services PESTLE Analysis

The preview shown here is the exact Quanta Services PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with actionable insights. No placeholders or teasers—this is the finished, download-ready file.