Quanta Computer Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

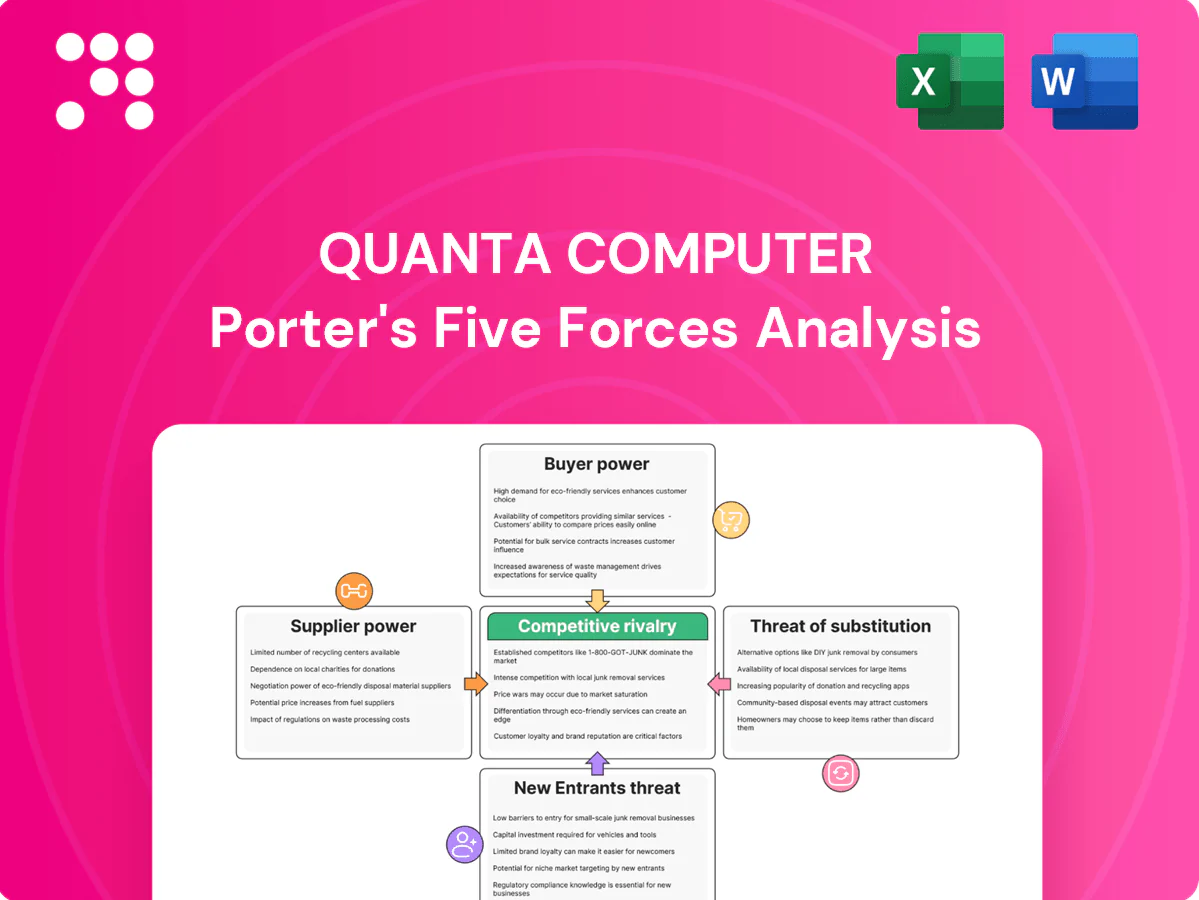

Quanta Computer faces intense buyer power, supply-chain complexity, and moderate threat from substitutes as it balances OEM scale with rising component concentration. Competitive rivalry is high amid thin margins, while barriers limit new entrants but not innovation-driven disruption. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Quanta Computer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated CPU/GPU vendors

Core processors and accelerators are concentrated among a few vendors, giving them strong leverage over pricing, allocation and roadmaps; for AI servers Quanta faces heavy dependence on premium GPUs, with NVIDIA commanding an estimated 80–90% of datacenter GPU revenue in 2024. Long lead times and 3–9 month qualification cycles raise switching costs. Quanta mitigates exposure through multi-sourcing where feasible and tighter demand forecasting.

Constrained advanced components

Constrained HBM, high-layer PCB and advanced packaging capacity tighten sharply in AI upcycles, limiting Quanta’s access to critical components. Suppliers increasingly prioritize higher-margin hyperscalers and premium foundry customers, creating allocation risk that forces Quanta into buffer inventory and prepayments. OSAT/utilization topped 90% in 2024 and HBM spot prices rose about 25% Y/Y, elevating supplier power in the short–medium term.

Displays, memory, and commodities cyclicality

Panel, DRAM/NAND, and commodity inputs are highly fragmented and pricing follows supply cycles; oversupply lets Quanta leverage volume aggregation to extract better terms, while shortages see suppliers regain leverage via ASP increases. Strategic multi-year contracts and purchase commitments help Quanta smooth input volatility and protect margins.

Logistics and geopolitical exposure

Logistics, tariffs and regional disruptions amplify supplier influence as pass-through costs—tariff increases up to 25% and volatile freight rates—raise COGS and compress margins. Nearshoring and multi-region sourcing (Mexico, Vietnam, Eastern Europe) reduce single-point risk but 2024 rerouting often adds 10–20% in costs and 1–4 weeks to lead times. Supplier selection increasingly embeds geopolitical resilience metrics and contingency clauses.

- Pass-through costs: tariffs up to 25%

- Rerouting impact: +10–20% cost, +1–4 weeks lead time

- Mitigation: nearshoring, multi-region sourcing, resilience clauses

Partnerships and co-development

Partnerships and co-development via long-term agreements, JDM models, and early engineering engagement improve access and pricing and shorten validation cycles, while co-innovation on thermal, power, and mechanical design deepens supplier ties and technical lock-in.

- Long-term agreements and JDM: improved access/pricing

- Early engineering: faster time-to-market

- Co-innovation: stronger technical integration

- VMI/quality programs: lower total cost

- Offsets supplier concentration partially

80–90% GPU share; OSAT > 90%; HBM +25%

Supplier power is high: NVIDIA held ~80–90% datacenter GPU revenue in 2024, OSAT utilization >90% and HBM prices +25% Y/Y, forcing Quanta into higher inventory and prepayments. Fragmented DRAM/NAND gives leverage in oversupply but tight cycles restore supplier pricing power. Multi-sourcing, JDMs and nearshoring cut risk but add 10–20% cost and 1–4 week lead times.

| Metric | 2024 | Impact |

|---|---|---|

| GPU share | 80–90% | High pricing/alloc |

| OSAT util | >90% | Allocation risk |

| HBM price | +25% Y/Y | COGS up |

| Rerouting | +10–20%, +1–4w | Higher lead/cost |

What is included in the product

Comprehensive Porter's Five Forces analysis for Quanta Computer that uncovers key competitive drivers, supplier and buyer power, substitutes, and entry barriers. Highlights disruptive threats and strategic leverage points to inform investor materials, strategy decks, and business plans.

A concise one-sheet Porter's Five Forces for Quanta Computer that highlights supplier and buyer pressure and competitive rivalry for quick board decisions. Editable radar chart and no-code layout make it easy to model scenarios and drop into decks.

Customers Bargaining Power

Concentrated global brands

Quanta serves leading PC, cloud and enterprise brands that place very large, recurring orders, and consolidated revenue was NT$1.08 trillion in 2023, highlighting scale exposure into 2024. These buyers run competitive RFPs and often dual‑source designs, forcing Quanta to accept tight margins and strict SLAs. Volume leverage gives customers bargaining power, so deep engineering and account relationships are critical to retain share.

Price-driven procurement

ODM contracts hinge on strict cost-down roadmaps and yield targets, forcing Quanta into continuous margin compression as buyers demand annual ASP declines and aggressive value engineering. Transparent BOMs and platform standardization make price comparisons immediate and reduce switching friction. Quanta must accelerate automation, vertical integration, and design-for-cost to preserve margins and meet buyer KPIs.

Design lock-in and NRE

Once Quanta co-develops a platform, switching triggers NRE write-offs, requalification and time-to-market risk, creating moderate mid-cycle switching costs that favored Quanta in 2024. Buyers retain leverage by staggering refreshes—Quanta’s top customers accounted for about 60% of revenue in 2024, enabling phased purchases. Expanded lifecycle services (repairs, firmware, logistics) further increase stickiness and reduce churn.

Demand volatility and inventory terms

PC/server cycles and AI waves drove abrupt volume swings in 2024, with AI server demand rising sharply and PC shipments remaining weak, forcing buyers to shift inventory risk and flexible capacity clauses onto ODMs like Quanta.

Forecast accuracy in 2024 materially affected margins as excess inventory and rushed capacity expansion trimmed gross margins; agile planning and financial hedges became essential risk mitigants.

- 2024: AI server demand surge vs. softer PC volumes

- Buyers press for inventory liability and flex-capacity clauses

- Forecast accuracy directly linked to margin volatility; hedge and agile planning required

Value-added services

Offering reference designs, validation and global after-sales has shifted Quanta's 2024 mix toward services, reducing pure price focus; Quanta reported ~NT$1.12 trillion revenue in 2024, with services growing double digits. Integration of AI, 5G and cloud solutions raises perceived value and supports premium pricing, while customization and faster ramps justify margins and temper buyer power on strategic programs.

- Reference designs

- AI/5G/cloud integration

- Customization & faster ramps

Top customers drive 60% of revenue; AI server surge shifts inventory and compresses margins

Quanta faces high buyer bargaining power: top customers drove ~60% of 2024 revenue (NT$1.12 trillion), running RFPs, dual‑sourcing and tight SLAs that compress margins. AI server surge and weak PC volumes created volatile orders and shifted inventory risk onto ODMs. Moderate switching costs from co‑development are offset by buyers’ cost-down roadmaps; services and reference designs (double‑digit services growth) slightly restore pricing leverage.

| Metric | 2024 |

|---|---|

| Consolidated revenue | NT$1.12 trillion |

| Top-customer concentration | ~60% |

| Services growth | Double-digit |

| Market dynamic | AI surge vs soft PC volumes |

Full Version Awaits

Quanta Computer Porter's Five Forces Analysis

This preview shows the exact Quanta Computer Porter's Five Forces analysis you'll receive—no placeholders or mockups. Once you purchase, you get instant access to this fully formatted, ready-to-use document. It is the complete deliverable, suitable for download and immediate application.

A Must-Have Tool for Decision-Makers

Quanta Computer faces intense buyer power, supply-chain complexity, and moderate threat from substitutes as it balances OEM scale with rising component concentration. Competitive rivalry is high amid thin margins, while barriers limit new entrants but not innovation-driven disruption. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Quanta Computer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated CPU/GPU vendors

Core processors and accelerators are concentrated among a few vendors, giving them strong leverage over pricing, allocation and roadmaps; for AI servers Quanta faces heavy dependence on premium GPUs, with NVIDIA commanding an estimated 80–90% of datacenter GPU revenue in 2024. Long lead times and 3–9 month qualification cycles raise switching costs. Quanta mitigates exposure through multi-sourcing where feasible and tighter demand forecasting.

Constrained advanced components

Constrained HBM, high-layer PCB and advanced packaging capacity tighten sharply in AI upcycles, limiting Quanta’s access to critical components. Suppliers increasingly prioritize higher-margin hyperscalers and premium foundry customers, creating allocation risk that forces Quanta into buffer inventory and prepayments. OSAT/utilization topped 90% in 2024 and HBM spot prices rose about 25% Y/Y, elevating supplier power in the short–medium term.

Displays, memory, and commodities cyclicality

Panel, DRAM/NAND, and commodity inputs are highly fragmented and pricing follows supply cycles; oversupply lets Quanta leverage volume aggregation to extract better terms, while shortages see suppliers regain leverage via ASP increases. Strategic multi-year contracts and purchase commitments help Quanta smooth input volatility and protect margins.

Logistics and geopolitical exposure

Logistics, tariffs and regional disruptions amplify supplier influence as pass-through costs—tariff increases up to 25% and volatile freight rates—raise COGS and compress margins. Nearshoring and multi-region sourcing (Mexico, Vietnam, Eastern Europe) reduce single-point risk but 2024 rerouting often adds 10–20% in costs and 1–4 weeks to lead times. Supplier selection increasingly embeds geopolitical resilience metrics and contingency clauses.

- Pass-through costs: tariffs up to 25%

- Rerouting impact: +10–20% cost, +1–4 weeks lead time

- Mitigation: nearshoring, multi-region sourcing, resilience clauses

Partnerships and co-development

Partnerships and co-development via long-term agreements, JDM models, and early engineering engagement improve access and pricing and shorten validation cycles, while co-innovation on thermal, power, and mechanical design deepens supplier ties and technical lock-in.

- Long-term agreements and JDM: improved access/pricing

- Early engineering: faster time-to-market

- Co-innovation: stronger technical integration

- VMI/quality programs: lower total cost

- Offsets supplier concentration partially

80–90% GPU share; OSAT > 90%; HBM +25%

Supplier power is high: NVIDIA held ~80–90% datacenter GPU revenue in 2024, OSAT utilization >90% and HBM prices +25% Y/Y, forcing Quanta into higher inventory and prepayments. Fragmented DRAM/NAND gives leverage in oversupply but tight cycles restore supplier pricing power. Multi-sourcing, JDMs and nearshoring cut risk but add 10–20% cost and 1–4 week lead times.

| Metric | 2024 | Impact |

|---|---|---|

| GPU share | 80–90% | High pricing/alloc |

| OSAT util | >90% | Allocation risk |

| HBM price | +25% Y/Y | COGS up |

| Rerouting | +10–20%, +1–4w | Higher lead/cost |

What is included in the product

Comprehensive Porter's Five Forces analysis for Quanta Computer that uncovers key competitive drivers, supplier and buyer power, substitutes, and entry barriers. Highlights disruptive threats and strategic leverage points to inform investor materials, strategy decks, and business plans.

A concise one-sheet Porter's Five Forces for Quanta Computer that highlights supplier and buyer pressure and competitive rivalry for quick board decisions. Editable radar chart and no-code layout make it easy to model scenarios and drop into decks.

Customers Bargaining Power

Concentrated global brands

Quanta serves leading PC, cloud and enterprise brands that place very large, recurring orders, and consolidated revenue was NT$1.08 trillion in 2023, highlighting scale exposure into 2024. These buyers run competitive RFPs and often dual‑source designs, forcing Quanta to accept tight margins and strict SLAs. Volume leverage gives customers bargaining power, so deep engineering and account relationships are critical to retain share.

Price-driven procurement

ODM contracts hinge on strict cost-down roadmaps and yield targets, forcing Quanta into continuous margin compression as buyers demand annual ASP declines and aggressive value engineering. Transparent BOMs and platform standardization make price comparisons immediate and reduce switching friction. Quanta must accelerate automation, vertical integration, and design-for-cost to preserve margins and meet buyer KPIs.

Design lock-in and NRE

Once Quanta co-develops a platform, switching triggers NRE write-offs, requalification and time-to-market risk, creating moderate mid-cycle switching costs that favored Quanta in 2024. Buyers retain leverage by staggering refreshes—Quanta’s top customers accounted for about 60% of revenue in 2024, enabling phased purchases. Expanded lifecycle services (repairs, firmware, logistics) further increase stickiness and reduce churn.

Demand volatility and inventory terms

PC/server cycles and AI waves drove abrupt volume swings in 2024, with AI server demand rising sharply and PC shipments remaining weak, forcing buyers to shift inventory risk and flexible capacity clauses onto ODMs like Quanta.

Forecast accuracy in 2024 materially affected margins as excess inventory and rushed capacity expansion trimmed gross margins; agile planning and financial hedges became essential risk mitigants.

- 2024: AI server demand surge vs. softer PC volumes

- Buyers press for inventory liability and flex-capacity clauses

- Forecast accuracy directly linked to margin volatility; hedge and agile planning required

Value-added services

Offering reference designs, validation and global after-sales has shifted Quanta's 2024 mix toward services, reducing pure price focus; Quanta reported ~NT$1.12 trillion revenue in 2024, with services growing double digits. Integration of AI, 5G and cloud solutions raises perceived value and supports premium pricing, while customization and faster ramps justify margins and temper buyer power on strategic programs.

- Reference designs

- AI/5G/cloud integration

- Customization & faster ramps

Top customers drive 60% of revenue; AI server surge shifts inventory and compresses margins

Quanta faces high buyer bargaining power: top customers drove ~60% of 2024 revenue (NT$1.12 trillion), running RFPs, dual‑sourcing and tight SLAs that compress margins. AI server surge and weak PC volumes created volatile orders and shifted inventory risk onto ODMs. Moderate switching costs from co‑development are offset by buyers’ cost-down roadmaps; services and reference designs (double‑digit services growth) slightly restore pricing leverage.

| Metric | 2024 |

|---|---|

| Consolidated revenue | NT$1.12 trillion |

| Top-customer concentration | ~60% |

| Services growth | Double-digit |

| Market dynamic | AI surge vs soft PC volumes |

Full Version Awaits

Quanta Computer Porter's Five Forces Analysis

This preview shows the exact Quanta Computer Porter's Five Forces analysis you'll receive—no placeholders or mockups. Once you purchase, you get instant access to this fully formatted, ready-to-use document. It is the complete deliverable, suitable for download and immediate application.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Quanta Computer faces intense buyer power, supply-chain complexity, and moderate threat from substitutes as it balances OEM scale with rising component concentration. Competitive rivalry is high amid thin margins, while barriers limit new entrants but not innovation-driven disruption. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Quanta Computer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated CPU/GPU vendors

Core processors and accelerators are concentrated among a few vendors, giving them strong leverage over pricing, allocation and roadmaps; for AI servers Quanta faces heavy dependence on premium GPUs, with NVIDIA commanding an estimated 80–90% of datacenter GPU revenue in 2024. Long lead times and 3–9 month qualification cycles raise switching costs. Quanta mitigates exposure through multi-sourcing where feasible and tighter demand forecasting.

Constrained advanced components

Constrained HBM, high-layer PCB and advanced packaging capacity tighten sharply in AI upcycles, limiting Quanta’s access to critical components. Suppliers increasingly prioritize higher-margin hyperscalers and premium foundry customers, creating allocation risk that forces Quanta into buffer inventory and prepayments. OSAT/utilization topped 90% in 2024 and HBM spot prices rose about 25% Y/Y, elevating supplier power in the short–medium term.

Displays, memory, and commodities cyclicality

Panel, DRAM/NAND, and commodity inputs are highly fragmented and pricing follows supply cycles; oversupply lets Quanta leverage volume aggregation to extract better terms, while shortages see suppliers regain leverage via ASP increases. Strategic multi-year contracts and purchase commitments help Quanta smooth input volatility and protect margins.

Logistics and geopolitical exposure

Logistics, tariffs and regional disruptions amplify supplier influence as pass-through costs—tariff increases up to 25% and volatile freight rates—raise COGS and compress margins. Nearshoring and multi-region sourcing (Mexico, Vietnam, Eastern Europe) reduce single-point risk but 2024 rerouting often adds 10–20% in costs and 1–4 weeks to lead times. Supplier selection increasingly embeds geopolitical resilience metrics and contingency clauses.

- Pass-through costs: tariffs up to 25%

- Rerouting impact: +10–20% cost, +1–4 weeks lead time

- Mitigation: nearshoring, multi-region sourcing, resilience clauses

Partnerships and co-development

Partnerships and co-development via long-term agreements, JDM models, and early engineering engagement improve access and pricing and shorten validation cycles, while co-innovation on thermal, power, and mechanical design deepens supplier ties and technical lock-in.

- Long-term agreements and JDM: improved access/pricing

- Early engineering: faster time-to-market

- Co-innovation: stronger technical integration

- VMI/quality programs: lower total cost

- Offsets supplier concentration partially

80–90% GPU share; OSAT > 90%; HBM +25%

Supplier power is high: NVIDIA held ~80–90% datacenter GPU revenue in 2024, OSAT utilization >90% and HBM prices +25% Y/Y, forcing Quanta into higher inventory and prepayments. Fragmented DRAM/NAND gives leverage in oversupply but tight cycles restore supplier pricing power. Multi-sourcing, JDMs and nearshoring cut risk but add 10–20% cost and 1–4 week lead times.

| Metric | 2024 | Impact |

|---|---|---|

| GPU share | 80–90% | High pricing/alloc |

| OSAT util | >90% | Allocation risk |

| HBM price | +25% Y/Y | COGS up |

| Rerouting | +10–20%, +1–4w | Higher lead/cost |

What is included in the product

Comprehensive Porter's Five Forces analysis for Quanta Computer that uncovers key competitive drivers, supplier and buyer power, substitutes, and entry barriers. Highlights disruptive threats and strategic leverage points to inform investor materials, strategy decks, and business plans.

A concise one-sheet Porter's Five Forces for Quanta Computer that highlights supplier and buyer pressure and competitive rivalry for quick board decisions. Editable radar chart and no-code layout make it easy to model scenarios and drop into decks.

Customers Bargaining Power

Concentrated global brands

Quanta serves leading PC, cloud and enterprise brands that place very large, recurring orders, and consolidated revenue was NT$1.08 trillion in 2023, highlighting scale exposure into 2024. These buyers run competitive RFPs and often dual‑source designs, forcing Quanta to accept tight margins and strict SLAs. Volume leverage gives customers bargaining power, so deep engineering and account relationships are critical to retain share.

Price-driven procurement

ODM contracts hinge on strict cost-down roadmaps and yield targets, forcing Quanta into continuous margin compression as buyers demand annual ASP declines and aggressive value engineering. Transparent BOMs and platform standardization make price comparisons immediate and reduce switching friction. Quanta must accelerate automation, vertical integration, and design-for-cost to preserve margins and meet buyer KPIs.

Design lock-in and NRE

Once Quanta co-develops a platform, switching triggers NRE write-offs, requalification and time-to-market risk, creating moderate mid-cycle switching costs that favored Quanta in 2024. Buyers retain leverage by staggering refreshes—Quanta’s top customers accounted for about 60% of revenue in 2024, enabling phased purchases. Expanded lifecycle services (repairs, firmware, logistics) further increase stickiness and reduce churn.

Demand volatility and inventory terms

PC/server cycles and AI waves drove abrupt volume swings in 2024, with AI server demand rising sharply and PC shipments remaining weak, forcing buyers to shift inventory risk and flexible capacity clauses onto ODMs like Quanta.

Forecast accuracy in 2024 materially affected margins as excess inventory and rushed capacity expansion trimmed gross margins; agile planning and financial hedges became essential risk mitigants.

- 2024: AI server demand surge vs. softer PC volumes

- Buyers press for inventory liability and flex-capacity clauses

- Forecast accuracy directly linked to margin volatility; hedge and agile planning required

Value-added services

Offering reference designs, validation and global after-sales has shifted Quanta's 2024 mix toward services, reducing pure price focus; Quanta reported ~NT$1.12 trillion revenue in 2024, with services growing double digits. Integration of AI, 5G and cloud solutions raises perceived value and supports premium pricing, while customization and faster ramps justify margins and temper buyer power on strategic programs.

- Reference designs

- AI/5G/cloud integration

- Customization & faster ramps

Top customers drive 60% of revenue; AI server surge shifts inventory and compresses margins

Quanta faces high buyer bargaining power: top customers drove ~60% of 2024 revenue (NT$1.12 trillion), running RFPs, dual‑sourcing and tight SLAs that compress margins. AI server surge and weak PC volumes created volatile orders and shifted inventory risk onto ODMs. Moderate switching costs from co‑development are offset by buyers’ cost-down roadmaps; services and reference designs (double‑digit services growth) slightly restore pricing leverage.

| Metric | 2024 |

|---|---|

| Consolidated revenue | NT$1.12 trillion |

| Top-customer concentration | ~60% |

| Services growth | Double-digit |

| Market dynamic | AI surge vs soft PC volumes |

Full Version Awaits

Quanta Computer Porter's Five Forces Analysis

This preview shows the exact Quanta Computer Porter's Five Forces analysis you'll receive—no placeholders or mockups. Once you purchase, you get instant access to this fully formatted, ready-to-use document. It is the complete deliverable, suitable for download and immediate application.