Quarto Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

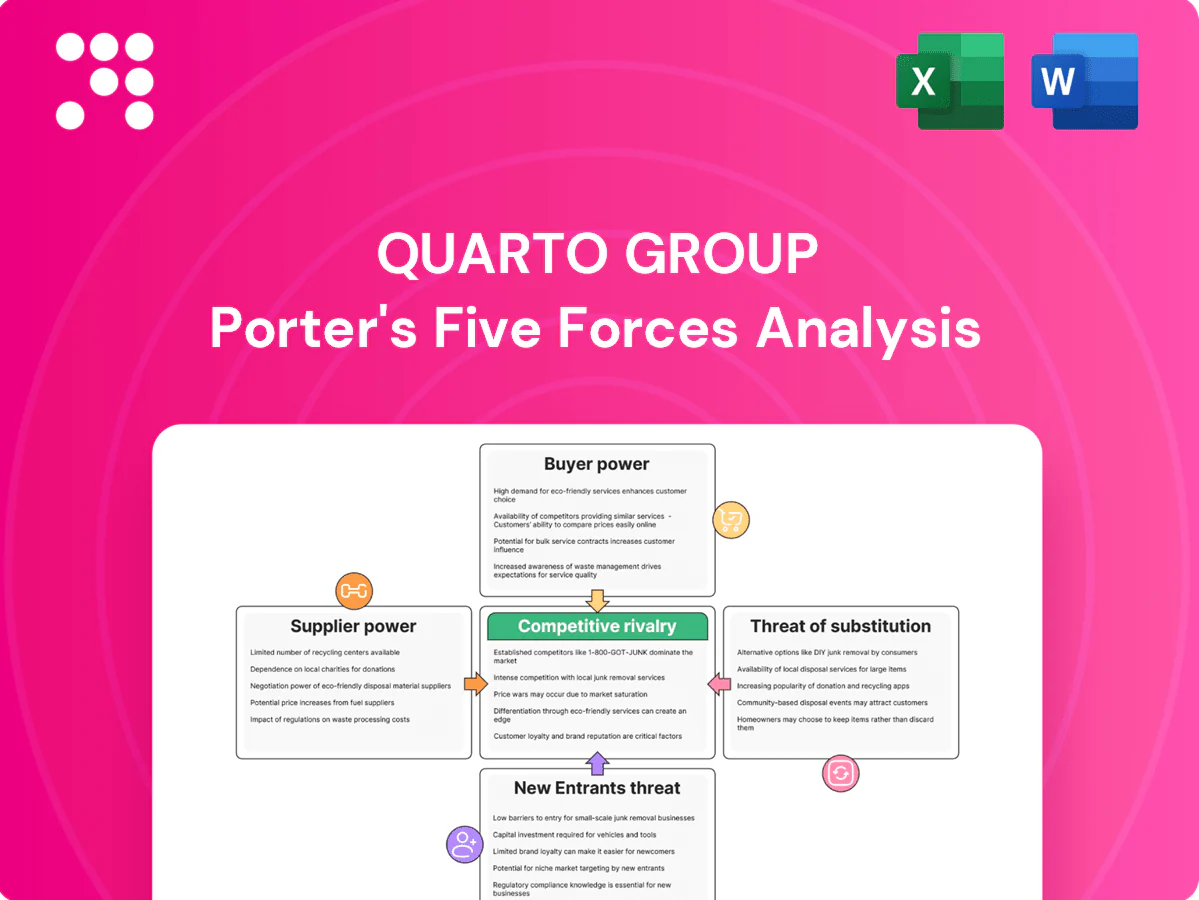

Quarto Group faces mixed pressures from concentrated buyers, moderate supplier leverage, and disruptive digital substitutes that are reshaping print-led revenues. Competitive rivalry remains intense as niche publishers and global platforms vie for shelf and online space. This brief snapshot highlights key tensions but omits force-by-force scoring. Unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Diverse creative suppliers

Quarto depends on authors, illustrators, photographers and packagers for distinctive content; star creators can command significant advances and higher royalties, pressuring margins, while the global publishing market of about $120bn in 2024 and a large international freelancer pool temper suppliers’ pricing power; long-term relationships and holding IP (rights ownership) materially reduce dependency on high-cost talent.

Printing and paper constraints

Illustrated books demand high-quality color printing and specialty papers, and premium printers are limited—top facilities often concentrate over 60% of high-end capacity—giving suppliers strong leverage amid paper price swings (paper pulp indices saw volatility of ~25% in 2023–24). Nearshoring and multi-sourcing reduce disruption risk, while larger print runs and forward paper buys (securing 20–40% lower unit costs) improve bargaining power.

Licensing and image rights

Rights holders for brands, images and datasets can extract premiums—brand licensing helped drive a global licensing market estimated at about $280 billion in 2024—creating leverage over publishers like Quarto. Niche or exclusive licenses raise switching costs and can add 10–30% cost premiums for unique imagery. Quarto can balance licensed versus owned content to limit exposure, and strong rights management reduces renegotiation and contingent liability risk.

Logistics and distribution partners

Global warehousing, freight and last-mile partners materially affect Quarto's cost and speed. Fuel surcharges averaged 5–12% in 2024 and capacity cycles caused 30–50% spot-rate swings in 2023–24, squeezing margins. Multi-3PL setups and tighter inventory dilute supplier power. Predictable contracted volumes secure preferential slots and ~1–3% better rates.

- Warehousing drives lead times/carrying cost

- Fuel surcharges 5–12% (2024)

- Spot-rate swings 30–50% (2023–24)

- Multi-3PL + inventory cuts supplier leverage

- Predictable volume → ~1–3% rate uplift

Technology and prepress tools

Design suites, color management and workflow systems are largely standardized across the industry, reducing supplier leverage; major vendors offer interoperable formats and APIs. Vendor lock-in is limited as PDFs, ICC profiles and JDF/JMF remain common exchange standards. Volume licensing and cloud subscriptions (Adobe Creative Cloud for teams listed at about 79.99 USD/month in 2024) push per-seat costs down. Process expertise and integration skills drive value more than tool differentiation.

- Standardization: interoperable formats

- Lock-in: limited by open standards

- Costs: cloud/volume pricing lowers per-seat fees

- Value: process expertise > tool choice

Publisher faces pricing risk: printers > 60% capacity, paper volatility

Quarto faces moderate supplier power: star creators and brand licensors can demand 10–30% premia; top high-end printers hold >60% capacity raising pricing risk as paper pulp volatility hit ~25% (2023–24); freight fuel surcharges averaged 5–12% (2024) but multi-sourcing, forward paper buys (20–40% unit savings) and owned IP reduce leverage.

| Supplier | Metric | 2023–24 |

|---|---|---|

| Printers | Concentration | >60% |

| Paper | Volatility | ~25% |

| Freight | Fuel surcharges | 5–12% |

| Licensing | Market size | $280bn (2024) |

What is included in the product

Comprehensive Porter's Five Forces review of Quarto Group, assessing competitive rivalry, buyer and supplier leverage, entry barriers, and substitute threats to clarify strategic risks and profit levers.

Quarto Group Porter's Five Forces Analysis condenses competitive pressures into a single, customizable one-sheet with radar visualization for instant strategic clarity; swap in current data, duplicate scenarios (pre/post regulation or new entrants), and drop directly into pitch decks or dashboards—no macros or finance expertise required.

Customers Bargaining Power

Concentrated retail channels

Large retailers and online platforms concentrate demand and press publishers on price, returns and co-op fees; Amazon accounted for roughly 40% of US book sales in 2024, amplifying buyer leverage. Their shelf placement and search algorithms materially shape discoverability and sales velocity. Heavy dependence increases exposure to policy or algorithm shifts, while diversifying direct, indie and international channels reduces that leverage.

Wholesalers and distributors

Wholesale partners can demand higher discounts—trade terms in illustrated book retail commonly sit around 40%—pressuring Quarto’s gross margins. They steer assortment and replenishment speed, prioritizing fast-selling titles and seasonal lines. Performance-based terms and chargebacks further compress margins during promotional windows. Data sharing and sell-through incentives help align interests by improving inventory turns and targeted reorders.

End-consumer price sensitivity

In 2024 end-consumer price sensitivity remains high as illustrated nonfiction competes with free or low-cost digital content, driving discretionary purchase cycles and seasonal spikes. Quarto can protect pricing through premium formats and gift positioning that command higher margins. Clear value-add in quality and curation lowers elasticity, increasing willingness to pay among niche and gift buyers.

High returns and markdown risk

Trade books carry generous return rights, with industry return rates often cited at 20–30% in 2024, increasing retailers bargaining power; over-forecasting forces markdowns and ties up working capital, amplifying margin pressure. Tighter print planning and demand forecasting have reduced buyer leverage, while a stable backlist lowers return volatility and smoothing cash flow.

- Return rate 2024: 20–30%

- Over-forecasting → markdowns, working capital drag

- Tighter print planning reduces retailer leverage

- Backlist stability lowers return volatility

Institutional and education buyers

Institutional and education buyers negotiate bulk discounts and demand durable, standards-aligned titles, driving concentrated bargaining power and multi-year renewals; budgetary cycles produce batch purchasing peaks around fiscal year-ends, while alignment to curricula increases stickiness and repeat orders. High-quality metadata raises discoverability and selection odds in procurement systems.

- bulk discounts

- durability & standards

- budget-cycle batching

- curriculum alignment

- metadata improves selection

Concentrated retail power squeezes margins: 40% market share, 40% trade discounts, 20-30% returns

Large retailers and platforms concentrate demand and push pricing and co-op fees; Amazon accounted for roughly 40% of US book sales in 2024, amplifying buyer leverage. Wholesale partners often demand ~40% trade discounts, pressuring gross margins and driving promotional markdowns. Industry return rates ran about 20–30% in 2024, increasing working capital strain and retailer bargaining power.

| Metric | 2024 Value |

|---|---|

| Amazon US market share | ~40% |

| Trade discount (illustrated) | ~40% |

| Industry return rate | 20–30% |

Same Document Delivered

Quarto Group Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis of Quarto Group you'll receive upon purchase—no samples, no placeholders. It covers supplier power, buyer power, competitive rivalry, threat of substitutes and new entrants with actionable insights. The file is fully formatted and ready for immediate download and use.

From Overview to Strategy Blueprint

Quarto Group faces mixed pressures from concentrated buyers, moderate supplier leverage, and disruptive digital substitutes that are reshaping print-led revenues. Competitive rivalry remains intense as niche publishers and global platforms vie for shelf and online space. This brief snapshot highlights key tensions but omits force-by-force scoring. Unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Diverse creative suppliers

Quarto depends on authors, illustrators, photographers and packagers for distinctive content; star creators can command significant advances and higher royalties, pressuring margins, while the global publishing market of about $120bn in 2024 and a large international freelancer pool temper suppliers’ pricing power; long-term relationships and holding IP (rights ownership) materially reduce dependency on high-cost talent.

Printing and paper constraints

Illustrated books demand high-quality color printing and specialty papers, and premium printers are limited—top facilities often concentrate over 60% of high-end capacity—giving suppliers strong leverage amid paper price swings (paper pulp indices saw volatility of ~25% in 2023–24). Nearshoring and multi-sourcing reduce disruption risk, while larger print runs and forward paper buys (securing 20–40% lower unit costs) improve bargaining power.

Licensing and image rights

Rights holders for brands, images and datasets can extract premiums—brand licensing helped drive a global licensing market estimated at about $280 billion in 2024—creating leverage over publishers like Quarto. Niche or exclusive licenses raise switching costs and can add 10–30% cost premiums for unique imagery. Quarto can balance licensed versus owned content to limit exposure, and strong rights management reduces renegotiation and contingent liability risk.

Logistics and distribution partners

Global warehousing, freight and last-mile partners materially affect Quarto's cost and speed. Fuel surcharges averaged 5–12% in 2024 and capacity cycles caused 30–50% spot-rate swings in 2023–24, squeezing margins. Multi-3PL setups and tighter inventory dilute supplier power. Predictable contracted volumes secure preferential slots and ~1–3% better rates.

- Warehousing drives lead times/carrying cost

- Fuel surcharges 5–12% (2024)

- Spot-rate swings 30–50% (2023–24)

- Multi-3PL + inventory cuts supplier leverage

- Predictable volume → ~1–3% rate uplift

Technology and prepress tools

Design suites, color management and workflow systems are largely standardized across the industry, reducing supplier leverage; major vendors offer interoperable formats and APIs. Vendor lock-in is limited as PDFs, ICC profiles and JDF/JMF remain common exchange standards. Volume licensing and cloud subscriptions (Adobe Creative Cloud for teams listed at about 79.99 USD/month in 2024) push per-seat costs down. Process expertise and integration skills drive value more than tool differentiation.

- Standardization: interoperable formats

- Lock-in: limited by open standards

- Costs: cloud/volume pricing lowers per-seat fees

- Value: process expertise > tool choice

Publisher faces pricing risk: printers > 60% capacity, paper volatility

Quarto faces moderate supplier power: star creators and brand licensors can demand 10–30% premia; top high-end printers hold >60% capacity raising pricing risk as paper pulp volatility hit ~25% (2023–24); freight fuel surcharges averaged 5–12% (2024) but multi-sourcing, forward paper buys (20–40% unit savings) and owned IP reduce leverage.

| Supplier | Metric | 2023–24 |

|---|---|---|

| Printers | Concentration | >60% |

| Paper | Volatility | ~25% |

| Freight | Fuel surcharges | 5–12% |

| Licensing | Market size | $280bn (2024) |

What is included in the product

Comprehensive Porter's Five Forces review of Quarto Group, assessing competitive rivalry, buyer and supplier leverage, entry barriers, and substitute threats to clarify strategic risks and profit levers.

Quarto Group Porter's Five Forces Analysis condenses competitive pressures into a single, customizable one-sheet with radar visualization for instant strategic clarity; swap in current data, duplicate scenarios (pre/post regulation or new entrants), and drop directly into pitch decks or dashboards—no macros or finance expertise required.

Customers Bargaining Power

Concentrated retail channels

Large retailers and online platforms concentrate demand and press publishers on price, returns and co-op fees; Amazon accounted for roughly 40% of US book sales in 2024, amplifying buyer leverage. Their shelf placement and search algorithms materially shape discoverability and sales velocity. Heavy dependence increases exposure to policy or algorithm shifts, while diversifying direct, indie and international channels reduces that leverage.

Wholesalers and distributors

Wholesale partners can demand higher discounts—trade terms in illustrated book retail commonly sit around 40%—pressuring Quarto’s gross margins. They steer assortment and replenishment speed, prioritizing fast-selling titles and seasonal lines. Performance-based terms and chargebacks further compress margins during promotional windows. Data sharing and sell-through incentives help align interests by improving inventory turns and targeted reorders.

End-consumer price sensitivity

In 2024 end-consumer price sensitivity remains high as illustrated nonfiction competes with free or low-cost digital content, driving discretionary purchase cycles and seasonal spikes. Quarto can protect pricing through premium formats and gift positioning that command higher margins. Clear value-add in quality and curation lowers elasticity, increasing willingness to pay among niche and gift buyers.

High returns and markdown risk

Trade books carry generous return rights, with industry return rates often cited at 20–30% in 2024, increasing retailers bargaining power; over-forecasting forces markdowns and ties up working capital, amplifying margin pressure. Tighter print planning and demand forecasting have reduced buyer leverage, while a stable backlist lowers return volatility and smoothing cash flow.

- Return rate 2024: 20–30%

- Over-forecasting → markdowns, working capital drag

- Tighter print planning reduces retailer leverage

- Backlist stability lowers return volatility

Institutional and education buyers

Institutional and education buyers negotiate bulk discounts and demand durable, standards-aligned titles, driving concentrated bargaining power and multi-year renewals; budgetary cycles produce batch purchasing peaks around fiscal year-ends, while alignment to curricula increases stickiness and repeat orders. High-quality metadata raises discoverability and selection odds in procurement systems.

- bulk discounts

- durability & standards

- budget-cycle batching

- curriculum alignment

- metadata improves selection

Concentrated retail power squeezes margins: 40% market share, 40% trade discounts, 20-30% returns

Large retailers and platforms concentrate demand and push pricing and co-op fees; Amazon accounted for roughly 40% of US book sales in 2024, amplifying buyer leverage. Wholesale partners often demand ~40% trade discounts, pressuring gross margins and driving promotional markdowns. Industry return rates ran about 20–30% in 2024, increasing working capital strain and retailer bargaining power.

| Metric | 2024 Value |

|---|---|

| Amazon US market share | ~40% |

| Trade discount (illustrated) | ~40% |

| Industry return rate | 20–30% |

Same Document Delivered

Quarto Group Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis of Quarto Group you'll receive upon purchase—no samples, no placeholders. It covers supplier power, buyer power, competitive rivalry, threat of substitutes and new entrants with actionable insights. The file is fully formatted and ready for immediate download and use.

Description

From Overview to Strategy Blueprint

Quarto Group faces mixed pressures from concentrated buyers, moderate supplier leverage, and disruptive digital substitutes that are reshaping print-led revenues. Competitive rivalry remains intense as niche publishers and global platforms vie for shelf and online space. This brief snapshot highlights key tensions but omits force-by-force scoring. Unlock the full Porter's Five Forces Analysis for detailed ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Diverse creative suppliers

Quarto depends on authors, illustrators, photographers and packagers for distinctive content; star creators can command significant advances and higher royalties, pressuring margins, while the global publishing market of about $120bn in 2024 and a large international freelancer pool temper suppliers’ pricing power; long-term relationships and holding IP (rights ownership) materially reduce dependency on high-cost talent.

Printing and paper constraints

Illustrated books demand high-quality color printing and specialty papers, and premium printers are limited—top facilities often concentrate over 60% of high-end capacity—giving suppliers strong leverage amid paper price swings (paper pulp indices saw volatility of ~25% in 2023–24). Nearshoring and multi-sourcing reduce disruption risk, while larger print runs and forward paper buys (securing 20–40% lower unit costs) improve bargaining power.

Licensing and image rights

Rights holders for brands, images and datasets can extract premiums—brand licensing helped drive a global licensing market estimated at about $280 billion in 2024—creating leverage over publishers like Quarto. Niche or exclusive licenses raise switching costs and can add 10–30% cost premiums for unique imagery. Quarto can balance licensed versus owned content to limit exposure, and strong rights management reduces renegotiation and contingent liability risk.

Logistics and distribution partners

Global warehousing, freight and last-mile partners materially affect Quarto's cost and speed. Fuel surcharges averaged 5–12% in 2024 and capacity cycles caused 30–50% spot-rate swings in 2023–24, squeezing margins. Multi-3PL setups and tighter inventory dilute supplier power. Predictable contracted volumes secure preferential slots and ~1–3% better rates.

- Warehousing drives lead times/carrying cost

- Fuel surcharges 5–12% (2024)

- Spot-rate swings 30–50% (2023–24)

- Multi-3PL + inventory cuts supplier leverage

- Predictable volume → ~1–3% rate uplift

Technology and prepress tools

Design suites, color management and workflow systems are largely standardized across the industry, reducing supplier leverage; major vendors offer interoperable formats and APIs. Vendor lock-in is limited as PDFs, ICC profiles and JDF/JMF remain common exchange standards. Volume licensing and cloud subscriptions (Adobe Creative Cloud for teams listed at about 79.99 USD/month in 2024) push per-seat costs down. Process expertise and integration skills drive value more than tool differentiation.

- Standardization: interoperable formats

- Lock-in: limited by open standards

- Costs: cloud/volume pricing lowers per-seat fees

- Value: process expertise > tool choice

Publisher faces pricing risk: printers > 60% capacity, paper volatility

Quarto faces moderate supplier power: star creators and brand licensors can demand 10–30% premia; top high-end printers hold >60% capacity raising pricing risk as paper pulp volatility hit ~25% (2023–24); freight fuel surcharges averaged 5–12% (2024) but multi-sourcing, forward paper buys (20–40% unit savings) and owned IP reduce leverage.

| Supplier | Metric | 2023–24 |

|---|---|---|

| Printers | Concentration | >60% |

| Paper | Volatility | ~25% |

| Freight | Fuel surcharges | 5–12% |

| Licensing | Market size | $280bn (2024) |

What is included in the product

Comprehensive Porter's Five Forces review of Quarto Group, assessing competitive rivalry, buyer and supplier leverage, entry barriers, and substitute threats to clarify strategic risks and profit levers.

Quarto Group Porter's Five Forces Analysis condenses competitive pressures into a single, customizable one-sheet with radar visualization for instant strategic clarity; swap in current data, duplicate scenarios (pre/post regulation or new entrants), and drop directly into pitch decks or dashboards—no macros or finance expertise required.

Customers Bargaining Power

Concentrated retail channels

Large retailers and online platforms concentrate demand and press publishers on price, returns and co-op fees; Amazon accounted for roughly 40% of US book sales in 2024, amplifying buyer leverage. Their shelf placement and search algorithms materially shape discoverability and sales velocity. Heavy dependence increases exposure to policy or algorithm shifts, while diversifying direct, indie and international channels reduces that leverage.

Wholesalers and distributors

Wholesale partners can demand higher discounts—trade terms in illustrated book retail commonly sit around 40%—pressuring Quarto’s gross margins. They steer assortment and replenishment speed, prioritizing fast-selling titles and seasonal lines. Performance-based terms and chargebacks further compress margins during promotional windows. Data sharing and sell-through incentives help align interests by improving inventory turns and targeted reorders.

End-consumer price sensitivity

In 2024 end-consumer price sensitivity remains high as illustrated nonfiction competes with free or low-cost digital content, driving discretionary purchase cycles and seasonal spikes. Quarto can protect pricing through premium formats and gift positioning that command higher margins. Clear value-add in quality and curation lowers elasticity, increasing willingness to pay among niche and gift buyers.

High returns and markdown risk

Trade books carry generous return rights, with industry return rates often cited at 20–30% in 2024, increasing retailers bargaining power; over-forecasting forces markdowns and ties up working capital, amplifying margin pressure. Tighter print planning and demand forecasting have reduced buyer leverage, while a stable backlist lowers return volatility and smoothing cash flow.

- Return rate 2024: 20–30%

- Over-forecasting → markdowns, working capital drag

- Tighter print planning reduces retailer leverage

- Backlist stability lowers return volatility

Institutional and education buyers

Institutional and education buyers negotiate bulk discounts and demand durable, standards-aligned titles, driving concentrated bargaining power and multi-year renewals; budgetary cycles produce batch purchasing peaks around fiscal year-ends, while alignment to curricula increases stickiness and repeat orders. High-quality metadata raises discoverability and selection odds in procurement systems.

- bulk discounts

- durability & standards

- budget-cycle batching

- curriculum alignment

- metadata improves selection

Concentrated retail power squeezes margins: 40% market share, 40% trade discounts, 20-30% returns

Large retailers and platforms concentrate demand and push pricing and co-op fees; Amazon accounted for roughly 40% of US book sales in 2024, amplifying buyer leverage. Wholesale partners often demand ~40% trade discounts, pressuring gross margins and driving promotional markdowns. Industry return rates ran about 20–30% in 2024, increasing working capital strain and retailer bargaining power.

| Metric | 2024 Value |

|---|---|

| Amazon US market share | ~40% |

| Trade discount (illustrated) | ~40% |

| Industry return rate | 20–30% |

Same Document Delivered

Quarto Group Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis of Quarto Group you'll receive upon purchase—no samples, no placeholders. It covers supplier power, buyer power, competitive rivalry, threat of substitutes and new entrants with actionable insights. The file is fully formatted and ready for immediate download and use.