Quero-Quero PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

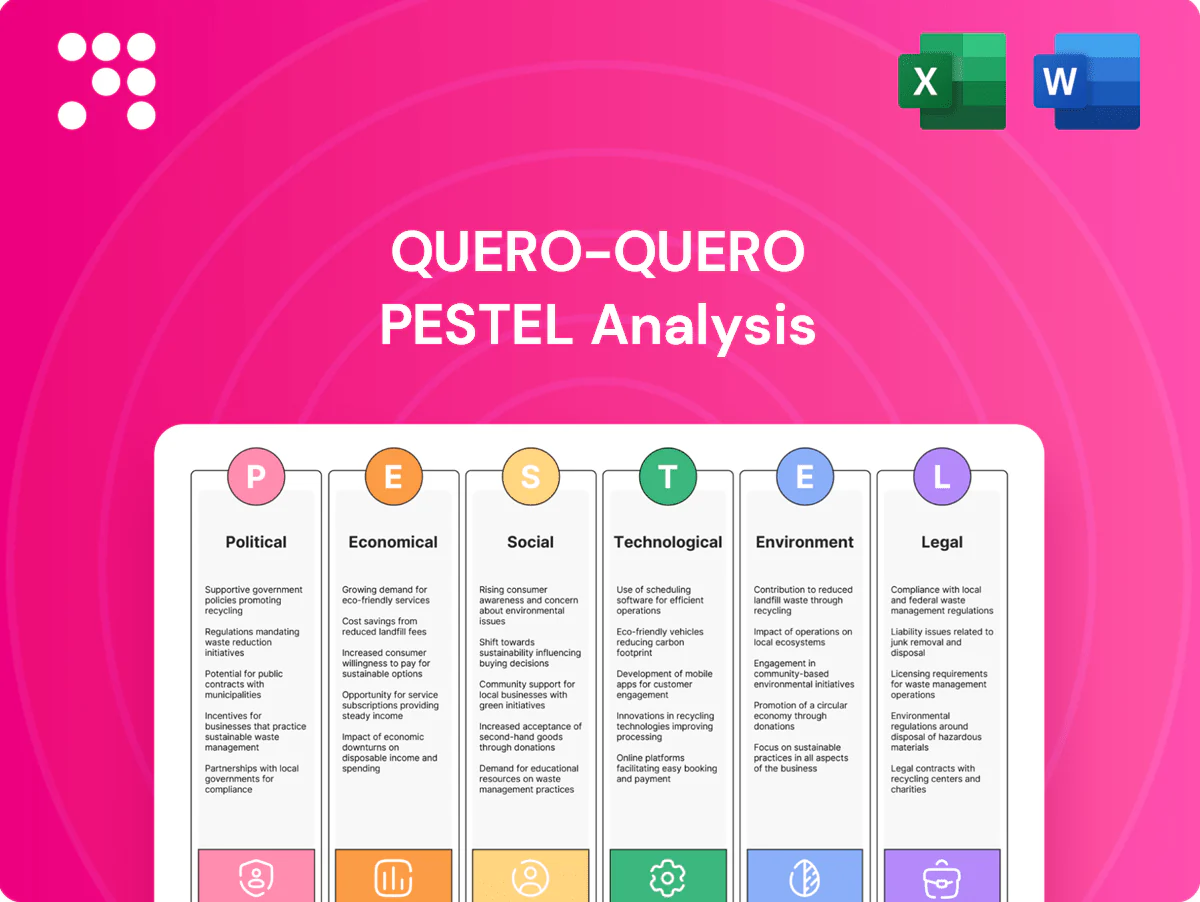

Discover how political, economic, social, technological, legal, and environmental forces are shaping Quero-Quero's future in our concise PESTLE snapshot. Gain actionable insights to anticipate risks and spot growth opportunities. Ideal for investors, consultants, and planners. Purchase the full PESTLE for the complete, ready-to-use analysis.

Political factors

Housing programs and subsidies

Federal housing initiatives such as Minha Casa Minha Vida (now Casa Verde e Amarela) and municipal programs like Habite Seguro drive upstream demand for construction materials and home appliances, making alignment with program specifications and accredited financing partners essential to unlock volume sales; policy pauses or budget cuts have historically slowed footfall and procurement cycles, so active monitoring of federal budget releases and municipal tendering portals is critical to capture B2B contracts.

Tax policy and fiscal reform

Brazil’s complex tax regime—ICMS (state VAT commonly 12–18% across states), PIS/COFINS (combined effective rates often exceeding 9%) and IPI (varies by product)—materially affects Quero-Quero pricing and margins across states. Ongoing national tax reform debates (aiming at rate, credit and compliance shifts) could alter cash flow and compliance costs. Scenario planning is needed to reprice and reroute supply quickly, while leveraging southern-state incentives (reduced ICMS/credit programs in Rio Grande do Sul and Santa Catarina) for logistics and store expansion.

Infrastructure and regional development

Public investments in roads, ports and energy in the South can cut Quero-Quero logistics costs—Brazil’s logistics bill was about 12% of GDP in 2023—reducing delivery times and inventory carrying costs. Municipal zoning and store permitting, often taking around 150–180 days on average, shape expansion pace and capex scheduling. State political shifts can re-prioritize projects, creating redistribution or delays in 2024–25 works; proactive engagement with local authorities helps de-risk timelines.

Trade policy and import duties

Tariffs on appliances and inputs shape Quero-Quero vendor mix and shelf prices; the Mercosur common external tariff averages about 14% in 2025, directly affecting landed costs and retail margins.

Anti-dumping measures, recently applied in metals and electronics, can spike sourcing costs and reduce supplier options, forcing pricier domestic or alternative imports.

Currency-sensitive import rules and BRL volatility (around ±12% y/y in 2024) make hedging and supplier diversification essential; strict customs compliance prevents delays and fines.

- Tariffs ~14%: higher landed costs

- Anti-dumping: reduced supplier availability

- BRL volatility ~±12% (2024): hedge/diversify

- Customs compliance: avoids delays/fines

Security and public policy environment

Public safety initiatives shape Quero-Quero store shrinkage, insurance premiums and operating hours by altering theft risk and response times; stronger municipal patrols and CCTV programs reduce in-store losses and lower insurance costs. Political commitment to combat organized retail crime—through dedicated task forces and harsher penalties—can materially lower loss rates, while election cycles often create enforcement variability that affects short-term security. Collaboration with local policing to protect high-turnover SKUs and peak-shift shifts improves inventory turnover and reduces stockouts.

- Public safety initiatives affect shrinkage, insurance, hours

- Dedicated anti-organized retail crime policies reduce losses

- Election cycles cause enforcement variability

- Police collaboration secures high-turnover SKUs

Federal housing tenders boost demand; taxes, tariffs, logistics and BRL volatility squeeze margins

Federal housing programs and municipal tenders drive bulk demand—budget shifts slow procurement; municipal permits average 150–180 days. Tax mix (ICMS 12–18%, PIS/COFINS >9%, IPI variable) and Mercosur tariff ~14% materially squeeze margins. Logistics spend ~12% of GDP (2023) and BRL volatility ±12% (2024) require hedging and supplier diversification. Anti-dumping and safety policy shifts affect sourcing and shrinkage.

| Factor | Key Metric |

|---|---|

| ICMS | 12–18% |

| PIS/COFINS | >9% |

| Tariff | ~14% |

| Logistics | ~12% GDP (2023) |

| BRL vol | ±12% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact the Quero-Quero, with each category backed by data and trend-based insights to reveal risks and opportunities for strategy and investment. Delivered in clean, region-specific format ready for plans and decks.

The Quero-Quero PESTLE Analysis delivers a clean, visually segmented summary that relieves planning pain points by offering editable notes, concise PowerPoint-ready content, and an easily shareable format in clear language for quick alignment across teams.

Economic factors

Interest rates and credit cycle

Movements in the Selic directly affect Quero-Quero: recent easing from 13.75% in 2023 to 11.25% by mid‑2025 expanded appliance and furniture ticket sizes and conversion, while prior hikes compressed demand. Private‑label credit and BNPL boost sales but increased portfolio delinquency—90‑120 day NPLs rose in retail during rate spikes. Risk‑based pricing and tighter underwriting are crucial to contain losses.

Construction and renovation activity

New builds and reforms drive core materials volume, with Brazil cement production near 64 million tonnes in 2023, underpinning demand for finishes and tools. Public and private capex cycles ripple through margins and sales velocity, so Quero-Quero must align procurement with multi-year infrastructure budgets. Seasonal peaks (rainy vs dry cycles) require tighter working-capital planning and inventory buffers, while strong contractor partnerships can stabilize B2B flow.

Inflation and cost pass-through

Input and wage inflation eroded margins on low-ticket, high-volume SKUs, with Brazil's IPCA at 4.23% in 2024 (IBGE) increasing per-unit costs and compressing typical retail gross margins around single digits. Dynamic pricing and intensified vendor negotiations enabled partial pass-through, while trading-down favored Quero-Quero store brands, boosting private-label share. Tight logistics cost control (inventory turns, route optimization) preserved competitiveness.

Currency volatility (BRL)

BRL volatility (roughly 15–20% swings vs USD in 2023–2024) raises costs for imported appliances and components, driving margin pressure for Quero-Quero; active hedging and multi-currency sourcing can smooth cost pass-through and limit repricing shocks.

Transparent price communication preserves customer trust during necessary adjustments, and FX-linked promotions should be strictly time-bound to avoid long-term margin leakage.

- FX impact: 15–20% BRL/USD swings (2023–2024)

- Mitigation: hedging, multi-currency sourcing

- Customer: clear repricing communication

- Promotions: time-bound FX-linked offers

Regional income dynamics in the South

Household income dispersion across RS (pop ~11.4M), SC (~7.5M) and PR (~11.5M) shapes assortment depth and price tiers, with SC/PR skewing toward higher-priced SKUs while RS needs broader value ranges; agribusiness cycles (soy/maize/wheat) drive 10–20% seasonal rural sales swings; tailored cluster strategies in pilots improved sell-through 5–12%; local unemployment (~6–8%) and employment growth guide new-store placement.

- income-levels

- agribusiness-cycles

- cluster-strategies

- employment-trends

Federal housing tenders boost demand; taxes, tariffs, logistics and BRL volatility squeeze margins

Selic easing to 11.25% by mid‑2025 lifted ticket sizes and conversion; prior 2023 hikes tightened demand. IPCA 2024 at 4.23% pressured margins; private‑label gains offset some pass‑through. BRL swung ~15–20% vs USD (2023–24), raising import costs. Regional income and agribusiness seasonality (10–20% rural sales swings) shape assortment and store placement.

| Metric | Value |

|---|---|

| Selic | 11.25% (mid‑2025) |

| IPCA 2024 | 4.23% |

| BRL/USD vol | 15–20% |

| Rural sales swing | 10–20% |

Same Document Delivered

Quero-Quero PESTLE Analysis

The preview shown here is the exact Quero-Quero PESTLE Analysis you’ll receive after purchase — fully formatted, professionally structured, and ready to use. This is the real file, delivered exactly as displayed with no placeholders or teasers. After checkout you can download the same complete document immediately, with the same layout, content, and structure visible here.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are shaping Quero-Quero's future in our concise PESTLE snapshot. Gain actionable insights to anticipate risks and spot growth opportunities. Ideal for investors, consultants, and planners. Purchase the full PESTLE for the complete, ready-to-use analysis.

Political factors

Housing programs and subsidies

Federal housing initiatives such as Minha Casa Minha Vida (now Casa Verde e Amarela) and municipal programs like Habite Seguro drive upstream demand for construction materials and home appliances, making alignment with program specifications and accredited financing partners essential to unlock volume sales; policy pauses or budget cuts have historically slowed footfall and procurement cycles, so active monitoring of federal budget releases and municipal tendering portals is critical to capture B2B contracts.

Tax policy and fiscal reform

Brazil’s complex tax regime—ICMS (state VAT commonly 12–18% across states), PIS/COFINS (combined effective rates often exceeding 9%) and IPI (varies by product)—materially affects Quero-Quero pricing and margins across states. Ongoing national tax reform debates (aiming at rate, credit and compliance shifts) could alter cash flow and compliance costs. Scenario planning is needed to reprice and reroute supply quickly, while leveraging southern-state incentives (reduced ICMS/credit programs in Rio Grande do Sul and Santa Catarina) for logistics and store expansion.

Infrastructure and regional development

Public investments in roads, ports and energy in the South can cut Quero-Quero logistics costs—Brazil’s logistics bill was about 12% of GDP in 2023—reducing delivery times and inventory carrying costs. Municipal zoning and store permitting, often taking around 150–180 days on average, shape expansion pace and capex scheduling. State political shifts can re-prioritize projects, creating redistribution or delays in 2024–25 works; proactive engagement with local authorities helps de-risk timelines.

Trade policy and import duties

Tariffs on appliances and inputs shape Quero-Quero vendor mix and shelf prices; the Mercosur common external tariff averages about 14% in 2025, directly affecting landed costs and retail margins.

Anti-dumping measures, recently applied in metals and electronics, can spike sourcing costs and reduce supplier options, forcing pricier domestic or alternative imports.

Currency-sensitive import rules and BRL volatility (around ±12% y/y in 2024) make hedging and supplier diversification essential; strict customs compliance prevents delays and fines.

- Tariffs ~14%: higher landed costs

- Anti-dumping: reduced supplier availability

- BRL volatility ~±12% (2024): hedge/diversify

- Customs compliance: avoids delays/fines

Security and public policy environment

Public safety initiatives shape Quero-Quero store shrinkage, insurance premiums and operating hours by altering theft risk and response times; stronger municipal patrols and CCTV programs reduce in-store losses and lower insurance costs. Political commitment to combat organized retail crime—through dedicated task forces and harsher penalties—can materially lower loss rates, while election cycles often create enforcement variability that affects short-term security. Collaboration with local policing to protect high-turnover SKUs and peak-shift shifts improves inventory turnover and reduces stockouts.

- Public safety initiatives affect shrinkage, insurance, hours

- Dedicated anti-organized retail crime policies reduce losses

- Election cycles cause enforcement variability

- Police collaboration secures high-turnover SKUs

Federal housing tenders boost demand; taxes, tariffs, logistics and BRL volatility squeeze margins

Federal housing programs and municipal tenders drive bulk demand—budget shifts slow procurement; municipal permits average 150–180 days. Tax mix (ICMS 12–18%, PIS/COFINS >9%, IPI variable) and Mercosur tariff ~14% materially squeeze margins. Logistics spend ~12% of GDP (2023) and BRL volatility ±12% (2024) require hedging and supplier diversification. Anti-dumping and safety policy shifts affect sourcing and shrinkage.

| Factor | Key Metric |

|---|---|

| ICMS | 12–18% |

| PIS/COFINS | >9% |

| Tariff | ~14% |

| Logistics | ~12% GDP (2023) |

| BRL vol | ±12% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact the Quero-Quero, with each category backed by data and trend-based insights to reveal risks and opportunities for strategy and investment. Delivered in clean, region-specific format ready for plans and decks.

The Quero-Quero PESTLE Analysis delivers a clean, visually segmented summary that relieves planning pain points by offering editable notes, concise PowerPoint-ready content, and an easily shareable format in clear language for quick alignment across teams.

Economic factors

Interest rates and credit cycle

Movements in the Selic directly affect Quero-Quero: recent easing from 13.75% in 2023 to 11.25% by mid‑2025 expanded appliance and furniture ticket sizes and conversion, while prior hikes compressed demand. Private‑label credit and BNPL boost sales but increased portfolio delinquency—90‑120 day NPLs rose in retail during rate spikes. Risk‑based pricing and tighter underwriting are crucial to contain losses.

Construction and renovation activity

New builds and reforms drive core materials volume, with Brazil cement production near 64 million tonnes in 2023, underpinning demand for finishes and tools. Public and private capex cycles ripple through margins and sales velocity, so Quero-Quero must align procurement with multi-year infrastructure budgets. Seasonal peaks (rainy vs dry cycles) require tighter working-capital planning and inventory buffers, while strong contractor partnerships can stabilize B2B flow.

Inflation and cost pass-through

Input and wage inflation eroded margins on low-ticket, high-volume SKUs, with Brazil's IPCA at 4.23% in 2024 (IBGE) increasing per-unit costs and compressing typical retail gross margins around single digits. Dynamic pricing and intensified vendor negotiations enabled partial pass-through, while trading-down favored Quero-Quero store brands, boosting private-label share. Tight logistics cost control (inventory turns, route optimization) preserved competitiveness.

Currency volatility (BRL)

BRL volatility (roughly 15–20% swings vs USD in 2023–2024) raises costs for imported appliances and components, driving margin pressure for Quero-Quero; active hedging and multi-currency sourcing can smooth cost pass-through and limit repricing shocks.

Transparent price communication preserves customer trust during necessary adjustments, and FX-linked promotions should be strictly time-bound to avoid long-term margin leakage.

- FX impact: 15–20% BRL/USD swings (2023–2024)

- Mitigation: hedging, multi-currency sourcing

- Customer: clear repricing communication

- Promotions: time-bound FX-linked offers

Regional income dynamics in the South

Household income dispersion across RS (pop ~11.4M), SC (~7.5M) and PR (~11.5M) shapes assortment depth and price tiers, with SC/PR skewing toward higher-priced SKUs while RS needs broader value ranges; agribusiness cycles (soy/maize/wheat) drive 10–20% seasonal rural sales swings; tailored cluster strategies in pilots improved sell-through 5–12%; local unemployment (~6–8%) and employment growth guide new-store placement.

- income-levels

- agribusiness-cycles

- cluster-strategies

- employment-trends

Federal housing tenders boost demand; taxes, tariffs, logistics and BRL volatility squeeze margins

Selic easing to 11.25% by mid‑2025 lifted ticket sizes and conversion; prior 2023 hikes tightened demand. IPCA 2024 at 4.23% pressured margins; private‑label gains offset some pass‑through. BRL swung ~15–20% vs USD (2023–24), raising import costs. Regional income and agribusiness seasonality (10–20% rural sales swings) shape assortment and store placement.

| Metric | Value |

|---|---|

| Selic | 11.25% (mid‑2025) |

| IPCA 2024 | 4.23% |

| BRL/USD vol | 15–20% |

| Rural sales swing | 10–20% |

Same Document Delivered

Quero-Quero PESTLE Analysis

The preview shown here is the exact Quero-Quero PESTLE Analysis you’ll receive after purchase — fully formatted, professionally structured, and ready to use. This is the real file, delivered exactly as displayed with no placeholders or teasers. After checkout you can download the same complete document immediately, with the same layout, content, and structure visible here.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are shaping Quero-Quero's future in our concise PESTLE snapshot. Gain actionable insights to anticipate risks and spot growth opportunities. Ideal for investors, consultants, and planners. Purchase the full PESTLE for the complete, ready-to-use analysis.

Political factors

Housing programs and subsidies

Federal housing initiatives such as Minha Casa Minha Vida (now Casa Verde e Amarela) and municipal programs like Habite Seguro drive upstream demand for construction materials and home appliances, making alignment with program specifications and accredited financing partners essential to unlock volume sales; policy pauses or budget cuts have historically slowed footfall and procurement cycles, so active monitoring of federal budget releases and municipal tendering portals is critical to capture B2B contracts.

Tax policy and fiscal reform

Brazil’s complex tax regime—ICMS (state VAT commonly 12–18% across states), PIS/COFINS (combined effective rates often exceeding 9%) and IPI (varies by product)—materially affects Quero-Quero pricing and margins across states. Ongoing national tax reform debates (aiming at rate, credit and compliance shifts) could alter cash flow and compliance costs. Scenario planning is needed to reprice and reroute supply quickly, while leveraging southern-state incentives (reduced ICMS/credit programs in Rio Grande do Sul and Santa Catarina) for logistics and store expansion.

Infrastructure and regional development

Public investments in roads, ports and energy in the South can cut Quero-Quero logistics costs—Brazil’s logistics bill was about 12% of GDP in 2023—reducing delivery times and inventory carrying costs. Municipal zoning and store permitting, often taking around 150–180 days on average, shape expansion pace and capex scheduling. State political shifts can re-prioritize projects, creating redistribution or delays in 2024–25 works; proactive engagement with local authorities helps de-risk timelines.

Trade policy and import duties

Tariffs on appliances and inputs shape Quero-Quero vendor mix and shelf prices; the Mercosur common external tariff averages about 14% in 2025, directly affecting landed costs and retail margins.

Anti-dumping measures, recently applied in metals and electronics, can spike sourcing costs and reduce supplier options, forcing pricier domestic or alternative imports.

Currency-sensitive import rules and BRL volatility (around ±12% y/y in 2024) make hedging and supplier diversification essential; strict customs compliance prevents delays and fines.

- Tariffs ~14%: higher landed costs

- Anti-dumping: reduced supplier availability

- BRL volatility ~±12% (2024): hedge/diversify

- Customs compliance: avoids delays/fines

Security and public policy environment

Public safety initiatives shape Quero-Quero store shrinkage, insurance premiums and operating hours by altering theft risk and response times; stronger municipal patrols and CCTV programs reduce in-store losses and lower insurance costs. Political commitment to combat organized retail crime—through dedicated task forces and harsher penalties—can materially lower loss rates, while election cycles often create enforcement variability that affects short-term security. Collaboration with local policing to protect high-turnover SKUs and peak-shift shifts improves inventory turnover and reduces stockouts.

- Public safety initiatives affect shrinkage, insurance, hours

- Dedicated anti-organized retail crime policies reduce losses

- Election cycles cause enforcement variability

- Police collaboration secures high-turnover SKUs

Federal housing tenders boost demand; taxes, tariffs, logistics and BRL volatility squeeze margins

Federal housing programs and municipal tenders drive bulk demand—budget shifts slow procurement; municipal permits average 150–180 days. Tax mix (ICMS 12–18%, PIS/COFINS >9%, IPI variable) and Mercosur tariff ~14% materially squeeze margins. Logistics spend ~12% of GDP (2023) and BRL volatility ±12% (2024) require hedging and supplier diversification. Anti-dumping and safety policy shifts affect sourcing and shrinkage.

| Factor | Key Metric |

|---|---|

| ICMS | 12–18% |

| PIS/COFINS | >9% |

| Tariff | ~14% |

| Logistics | ~12% GDP (2023) |

| BRL vol | ±12% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact the Quero-Quero, with each category backed by data and trend-based insights to reveal risks and opportunities for strategy and investment. Delivered in clean, region-specific format ready for plans and decks.

The Quero-Quero PESTLE Analysis delivers a clean, visually segmented summary that relieves planning pain points by offering editable notes, concise PowerPoint-ready content, and an easily shareable format in clear language for quick alignment across teams.

Economic factors

Interest rates and credit cycle

Movements in the Selic directly affect Quero-Quero: recent easing from 13.75% in 2023 to 11.25% by mid‑2025 expanded appliance and furniture ticket sizes and conversion, while prior hikes compressed demand. Private‑label credit and BNPL boost sales but increased portfolio delinquency—90‑120 day NPLs rose in retail during rate spikes. Risk‑based pricing and tighter underwriting are crucial to contain losses.

Construction and renovation activity

New builds and reforms drive core materials volume, with Brazil cement production near 64 million tonnes in 2023, underpinning demand for finishes and tools. Public and private capex cycles ripple through margins and sales velocity, so Quero-Quero must align procurement with multi-year infrastructure budgets. Seasonal peaks (rainy vs dry cycles) require tighter working-capital planning and inventory buffers, while strong contractor partnerships can stabilize B2B flow.

Inflation and cost pass-through

Input and wage inflation eroded margins on low-ticket, high-volume SKUs, with Brazil's IPCA at 4.23% in 2024 (IBGE) increasing per-unit costs and compressing typical retail gross margins around single digits. Dynamic pricing and intensified vendor negotiations enabled partial pass-through, while trading-down favored Quero-Quero store brands, boosting private-label share. Tight logistics cost control (inventory turns, route optimization) preserved competitiveness.

Currency volatility (BRL)

BRL volatility (roughly 15–20% swings vs USD in 2023–2024) raises costs for imported appliances and components, driving margin pressure for Quero-Quero; active hedging and multi-currency sourcing can smooth cost pass-through and limit repricing shocks.

Transparent price communication preserves customer trust during necessary adjustments, and FX-linked promotions should be strictly time-bound to avoid long-term margin leakage.

- FX impact: 15–20% BRL/USD swings (2023–2024)

- Mitigation: hedging, multi-currency sourcing

- Customer: clear repricing communication

- Promotions: time-bound FX-linked offers

Regional income dynamics in the South

Household income dispersion across RS (pop ~11.4M), SC (~7.5M) and PR (~11.5M) shapes assortment depth and price tiers, with SC/PR skewing toward higher-priced SKUs while RS needs broader value ranges; agribusiness cycles (soy/maize/wheat) drive 10–20% seasonal rural sales swings; tailored cluster strategies in pilots improved sell-through 5–12%; local unemployment (~6–8%) and employment growth guide new-store placement.

- income-levels

- agribusiness-cycles

- cluster-strategies

- employment-trends

Federal housing tenders boost demand; taxes, tariffs, logistics and BRL volatility squeeze margins

Selic easing to 11.25% by mid‑2025 lifted ticket sizes and conversion; prior 2023 hikes tightened demand. IPCA 2024 at 4.23% pressured margins; private‑label gains offset some pass‑through. BRL swung ~15–20% vs USD (2023–24), raising import costs. Regional income and agribusiness seasonality (10–20% rural sales swings) shape assortment and store placement.

| Metric | Value |

|---|---|

| Selic | 11.25% (mid‑2025) |

| IPCA 2024 | 4.23% |

| BRL/USD vol | 15–20% |

| Rural sales swing | 10–20% |

Same Document Delivered

Quero-Quero PESTLE Analysis

The preview shown here is the exact Quero-Quero PESTLE Analysis you’ll receive after purchase — fully formatted, professionally structured, and ready to use. This is the real file, delivered exactly as displayed with no placeholders or teasers. After checkout you can download the same complete document immediately, with the same layout, content, and structure visible here.