QuidelOrtho PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of QuidelOrtho—three to five concise sections that reveal how political, economic, social, technological, legal, and environmental forces will shape its outlook; ideal for investors and strategists. Purchase the full report to access the detailed, actionable intelligence you need to make better decisions now.

Political factors

Healthcare policy and reimbursement priorities

Government budget emphasis on preventative care and rapid diagnostics supports demand for point-of-care and lab tests, with the global POC diagnostics market ~40 billion USD in 2024. Favorable reimbursement and public screening programs can accelerate infectious and cardiometabolic assay uptake, while value-based care—covering roughly 35% of Medicare payments in 2024—rewards tests that cut downstream costs. Policy reversals or austerity can delay instrument purchases in public systems.

Global trade dynamics and supply chain geopolitics

Tariffs on electronics, reagents and plastics, including US-China measures that levy duties of up to 25% on certain product lines, elevate bill‑of‑material costs for QuidelOrtho diagnostic instruments and consumables. Export controls tightened in 2023 on advanced semiconductors and related tech constrain component sourcing and limit sales into sanctioned markets. Regionalization of manufacturing and supply hubs is increasingly pursued to de‑risk geopolitical hotspots and comply with trade controls. Customs inspections and port congestion can add multi‑day delays, disrupting just‑in‑time delivery to hospitals and reference labs.

Pandemic preparedness and public health funding cycles

QuidelOrtho, formed by the 2022 combination of Quidel and Ortho, faces outbreak-driven procurements that create sharp demand spikes for respiratory assays; after the U.S. COVID-19 national emergency ended May 11, 2023, emergency funding faded and run rates normalized, pressuring episodic revenues. Governments continue to stockpile rapid tests and analyzers with unpredictable tender timing, while participation in national surveillance programs can deliver steadier recurring volumes.

Regulatory diplomacy and standards harmonization

Divergent regulatory expectations between the U.S., EU, and emerging markets complicate QuidelOrtho product rollouts, increasing premarket study and labeling work; FDA 510(k) review goal is 90 days and PMA 180 days, while EU IVDR implementation has tightened IVD oversight since May 2022, lengthening approvals.

- Harmonized standards can cut time-to-market and compliance costs

- Mutual recognition agreements would ease multi-region launches

- Misalignment prolongs clinical evidence generation and labeling

Public procurement practices and transparency

Winning national health tenders for QuidelOrtho hinges on competitive pricing, demonstrable local content and strict anti-corruption compliance; OECD estimates public procurement equals about 12% of GDP, underscoring its scale. Political scrutiny in crises (eg pandemic procurements) has shifted awards toward suppliers with rapid compliance records. Multi-year framework agreements give volume visibility but typically compress margins. Localization incentives increasingly drive regional manufacturing or partnerships.

- Pricing sensitivity: bid wins often depend on lowest sustainable price

- Compliance: anti-corruption credentials crucial during crisis scrutiny

- Frameworks: multi-year deals boost volume predictability, squeeze margins

- Localization: incentives push for regional manufacturing/partners

POC demand: ~40B USD, Medicare ≈35%, tariffs up to 25%

Government emphasis on preventative care and rapid diagnostics supports POC demand (global POC market ~40B USD in 2024) and value‑based care (≈35% of Medicare payments in 2024) which favors cost-saving tests; austerity can delay public purchases. Tariffs (up to 25%) and 2023 export controls raise BOM costs and constrain sourcing; IVDR (since May 2022) and FDA timelines (510(k) 90d, PMA 180d) lengthen rollouts. Public procurement (~12% GDP) and tender volatility after COVID emergency end (May 11, 2023) drive price sensitivity and localization.

| Metric | Value |

|---|---|

| Global POC market (2024) | ~40B USD |

| Medicare value-based share (2024) | ~35% |

| Tariffs/dues | up to 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect QuidelOrtho across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by relevant data and current trends. Designed to support executives and investors with clean, forward-looking insights ready for business plans, decks, or reports.

A concise, visually segmented PESTLE summary of QuidelOrtho enabling quick interpretation during meetings, easily dropped into presentations, annotated for regional context, and shareable for fast team alignment.

Economic factors

Hospital and lab capital spending cycles

Higher borrowing costs—US federal funds target 5.25–5.50% (mid‑2024)—tighten hospital budgets and slow analyzer placements and upgrades, pushing customers toward reagent‑rental or pay‑per‑test models. Deferred capex lengthens sales cycles and delays installed‑base refresh, while macro expansions historically increase menu adoption and cross‑sell opportunities as hospitals restore capital plans.

Macro growth and payer mix

Employment levels and insurance coverage—with US unemployment near 3.6% in mid‑2025—directly drive ambulatory and acute test volumes, while weak macro conditions shift payer mix toward lower‑margin public payers and reduce elective testing. Expanding middle classes in emerging markets are raising diagnostics demand, supporting volume growth outside the US. Currency volatility continues to affect reported revenues and constrains pricing power in key export markets.

Input cost inflation and logistics

Input cost inflation for resins, rare chemicals, membranes and semiconductor components drove notable price swings in 2024, squeezing margins on assays and reagents. Elevated freight and cold-chain logistics costs as of 2024 further pressured unit economics for temperature-sensitive kits. Long-term supply contracts and dual-sourcing have been adopted to mitigate volatility. Scaling manufacturing efficiency improves unit economics and absorbs input cost shocks.

Competitive pricing and consolidation

Intense competition among diagnostics firms has compressed ASPs for high-volume tests, with the global IVD market near $95 billion in 2024 and commodity-test pricing seeing single-digit annual declines. Consolidation of labs (Quest and LabCorp together account for roughly 50–60% of US testing volume) boosts buyer power and formulary control. QuidelOrtho can sustain premiums by differentiating on accuracy, TAT, and menu breadth, while increasing value-based contracts link reimbursement to measurable clinical outcomes.

- Compressed ASPs: single-digit declines for commodity tests

- Lab consolidation: Quest+LabCorp ~50–60% US volume

- Premium drivers: accuracy, turnaround time, menu breadth

- Reimbursement shift: growing value-based contracts tied to outcomes

R&D productivity and portfolio ROI

R&D returns hinge on time-to-approval, demonstrated clinical utility, and expanding test menus on QuidelOrtho’s installed base after the 2022 merger; rapid approvals accelerate reagent pull-through and margin recovery.

High R&D spend must translate to recurring reagent revenue via portfolio optimization that reallocates capital from low-growth assays toward high-burden disease areas with stronger lifetime value.

Lifecycle management, firmware upgrades, and backwards-compatible assays sustain annuity revenue by preserving installed-instrument utilization and driving recurring consumable sales.

- installed-base leverage after 2022 merger

- R&D→reagent pull-through focus

- reallocate from low-growth assays

- lifecycle upgrades sustain annuity

POC demand: ~40B USD, Medicare ≈35%, tariffs up to 25%

Higher US rates (fed funds 5.25–5.50% mid‑2024) tighten hospital capex, slowing analyzer placements and favoring reagent‑rental models; US unemployment ~3.6% mid‑2025 weighs on elective test volumes, while emerging markets support export growth. Input inflation and freight in 2024 squeezed margins; global IVD ~$95B 2024 with Quest+LabCorp ~50–60% US volume.

| Metric | Value |

|---|---|

| Fed funds (mid‑2024) | 5.25–5.50% |

| US unemployment (mid‑2025) | ~3.6% |

| Global IVD (2024) | ~$95B |

| Quest+LabCorp US volume | ~50–60% |

Preview the Actual Deliverable

QuidelOrtho PESTLE Analysis

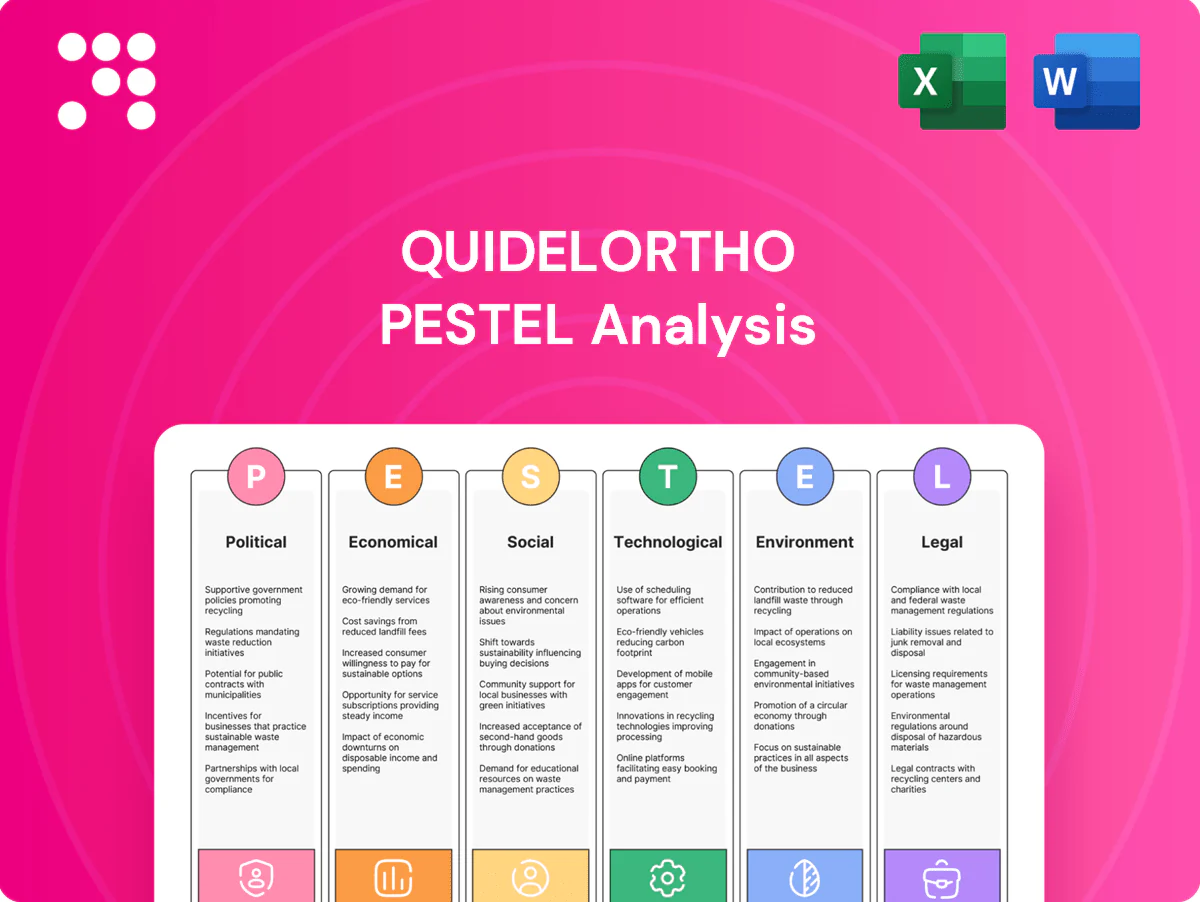

The preview shown here is the exact QuidelOrtho PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are identical to the downloadable file delivered at checkout. No placeholders or teasers—this is the final, professionally prepared report you’ll own instantly after payment.

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of QuidelOrtho—three to five concise sections that reveal how political, economic, social, technological, legal, and environmental forces will shape its outlook; ideal for investors and strategists. Purchase the full report to access the detailed, actionable intelligence you need to make better decisions now.

Political factors

Healthcare policy and reimbursement priorities

Government budget emphasis on preventative care and rapid diagnostics supports demand for point-of-care and lab tests, with the global POC diagnostics market ~40 billion USD in 2024. Favorable reimbursement and public screening programs can accelerate infectious and cardiometabolic assay uptake, while value-based care—covering roughly 35% of Medicare payments in 2024—rewards tests that cut downstream costs. Policy reversals or austerity can delay instrument purchases in public systems.

Global trade dynamics and supply chain geopolitics

Tariffs on electronics, reagents and plastics, including US-China measures that levy duties of up to 25% on certain product lines, elevate bill‑of‑material costs for QuidelOrtho diagnostic instruments and consumables. Export controls tightened in 2023 on advanced semiconductors and related tech constrain component sourcing and limit sales into sanctioned markets. Regionalization of manufacturing and supply hubs is increasingly pursued to de‑risk geopolitical hotspots and comply with trade controls. Customs inspections and port congestion can add multi‑day delays, disrupting just‑in‑time delivery to hospitals and reference labs.

Pandemic preparedness and public health funding cycles

QuidelOrtho, formed by the 2022 combination of Quidel and Ortho, faces outbreak-driven procurements that create sharp demand spikes for respiratory assays; after the U.S. COVID-19 national emergency ended May 11, 2023, emergency funding faded and run rates normalized, pressuring episodic revenues. Governments continue to stockpile rapid tests and analyzers with unpredictable tender timing, while participation in national surveillance programs can deliver steadier recurring volumes.

Regulatory diplomacy and standards harmonization

Divergent regulatory expectations between the U.S., EU, and emerging markets complicate QuidelOrtho product rollouts, increasing premarket study and labeling work; FDA 510(k) review goal is 90 days and PMA 180 days, while EU IVDR implementation has tightened IVD oversight since May 2022, lengthening approvals.

- Harmonized standards can cut time-to-market and compliance costs

- Mutual recognition agreements would ease multi-region launches

- Misalignment prolongs clinical evidence generation and labeling

Public procurement practices and transparency

Winning national health tenders for QuidelOrtho hinges on competitive pricing, demonstrable local content and strict anti-corruption compliance; OECD estimates public procurement equals about 12% of GDP, underscoring its scale. Political scrutiny in crises (eg pandemic procurements) has shifted awards toward suppliers with rapid compliance records. Multi-year framework agreements give volume visibility but typically compress margins. Localization incentives increasingly drive regional manufacturing or partnerships.

- Pricing sensitivity: bid wins often depend on lowest sustainable price

- Compliance: anti-corruption credentials crucial during crisis scrutiny

- Frameworks: multi-year deals boost volume predictability, squeeze margins

- Localization: incentives push for regional manufacturing/partners

POC demand: ~40B USD, Medicare ≈35%, tariffs up to 25%

Government emphasis on preventative care and rapid diagnostics supports POC demand (global POC market ~40B USD in 2024) and value‑based care (≈35% of Medicare payments in 2024) which favors cost-saving tests; austerity can delay public purchases. Tariffs (up to 25%) and 2023 export controls raise BOM costs and constrain sourcing; IVDR (since May 2022) and FDA timelines (510(k) 90d, PMA 180d) lengthen rollouts. Public procurement (~12% GDP) and tender volatility after COVID emergency end (May 11, 2023) drive price sensitivity and localization.

| Metric | Value |

|---|---|

| Global POC market (2024) | ~40B USD |

| Medicare value-based share (2024) | ~35% |

| Tariffs/dues | up to 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect QuidelOrtho across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by relevant data and current trends. Designed to support executives and investors with clean, forward-looking insights ready for business plans, decks, or reports.

A concise, visually segmented PESTLE summary of QuidelOrtho enabling quick interpretation during meetings, easily dropped into presentations, annotated for regional context, and shareable for fast team alignment.

Economic factors

Hospital and lab capital spending cycles

Higher borrowing costs—US federal funds target 5.25–5.50% (mid‑2024)—tighten hospital budgets and slow analyzer placements and upgrades, pushing customers toward reagent‑rental or pay‑per‑test models. Deferred capex lengthens sales cycles and delays installed‑base refresh, while macro expansions historically increase menu adoption and cross‑sell opportunities as hospitals restore capital plans.

Macro growth and payer mix

Employment levels and insurance coverage—with US unemployment near 3.6% in mid‑2025—directly drive ambulatory and acute test volumes, while weak macro conditions shift payer mix toward lower‑margin public payers and reduce elective testing. Expanding middle classes in emerging markets are raising diagnostics demand, supporting volume growth outside the US. Currency volatility continues to affect reported revenues and constrains pricing power in key export markets.

Input cost inflation and logistics

Input cost inflation for resins, rare chemicals, membranes and semiconductor components drove notable price swings in 2024, squeezing margins on assays and reagents. Elevated freight and cold-chain logistics costs as of 2024 further pressured unit economics for temperature-sensitive kits. Long-term supply contracts and dual-sourcing have been adopted to mitigate volatility. Scaling manufacturing efficiency improves unit economics and absorbs input cost shocks.

Competitive pricing and consolidation

Intense competition among diagnostics firms has compressed ASPs for high-volume tests, with the global IVD market near $95 billion in 2024 and commodity-test pricing seeing single-digit annual declines. Consolidation of labs (Quest and LabCorp together account for roughly 50–60% of US testing volume) boosts buyer power and formulary control. QuidelOrtho can sustain premiums by differentiating on accuracy, TAT, and menu breadth, while increasing value-based contracts link reimbursement to measurable clinical outcomes.

- Compressed ASPs: single-digit declines for commodity tests

- Lab consolidation: Quest+LabCorp ~50–60% US volume

- Premium drivers: accuracy, turnaround time, menu breadth

- Reimbursement shift: growing value-based contracts tied to outcomes

R&D productivity and portfolio ROI

R&D returns hinge on time-to-approval, demonstrated clinical utility, and expanding test menus on QuidelOrtho’s installed base after the 2022 merger; rapid approvals accelerate reagent pull-through and margin recovery.

High R&D spend must translate to recurring reagent revenue via portfolio optimization that reallocates capital from low-growth assays toward high-burden disease areas with stronger lifetime value.

Lifecycle management, firmware upgrades, and backwards-compatible assays sustain annuity revenue by preserving installed-instrument utilization and driving recurring consumable sales.

- installed-base leverage after 2022 merger

- R&D→reagent pull-through focus

- reallocate from low-growth assays

- lifecycle upgrades sustain annuity

POC demand: ~40B USD, Medicare ≈35%, tariffs up to 25%

Higher US rates (fed funds 5.25–5.50% mid‑2024) tighten hospital capex, slowing analyzer placements and favoring reagent‑rental models; US unemployment ~3.6% mid‑2025 weighs on elective test volumes, while emerging markets support export growth. Input inflation and freight in 2024 squeezed margins; global IVD ~$95B 2024 with Quest+LabCorp ~50–60% US volume.

| Metric | Value |

|---|---|

| Fed funds (mid‑2024) | 5.25–5.50% |

| US unemployment (mid‑2025) | ~3.6% |

| Global IVD (2024) | ~$95B |

| Quest+LabCorp US volume | ~50–60% |

Preview the Actual Deliverable

QuidelOrtho PESTLE Analysis

The preview shown here is the exact QuidelOrtho PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are identical to the downloadable file delivered at checkout. No placeholders or teasers—this is the final, professionally prepared report you’ll own instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our PESTLE Analysis of QuidelOrtho—three to five concise sections that reveal how political, economic, social, technological, legal, and environmental forces will shape its outlook; ideal for investors and strategists. Purchase the full report to access the detailed, actionable intelligence you need to make better decisions now.

Political factors

Healthcare policy and reimbursement priorities

Government budget emphasis on preventative care and rapid diagnostics supports demand for point-of-care and lab tests, with the global POC diagnostics market ~40 billion USD in 2024. Favorable reimbursement and public screening programs can accelerate infectious and cardiometabolic assay uptake, while value-based care—covering roughly 35% of Medicare payments in 2024—rewards tests that cut downstream costs. Policy reversals or austerity can delay instrument purchases in public systems.

Global trade dynamics and supply chain geopolitics

Tariffs on electronics, reagents and plastics, including US-China measures that levy duties of up to 25% on certain product lines, elevate bill‑of‑material costs for QuidelOrtho diagnostic instruments and consumables. Export controls tightened in 2023 on advanced semiconductors and related tech constrain component sourcing and limit sales into sanctioned markets. Regionalization of manufacturing and supply hubs is increasingly pursued to de‑risk geopolitical hotspots and comply with trade controls. Customs inspections and port congestion can add multi‑day delays, disrupting just‑in‑time delivery to hospitals and reference labs.

Pandemic preparedness and public health funding cycles

QuidelOrtho, formed by the 2022 combination of Quidel and Ortho, faces outbreak-driven procurements that create sharp demand spikes for respiratory assays; after the U.S. COVID-19 national emergency ended May 11, 2023, emergency funding faded and run rates normalized, pressuring episodic revenues. Governments continue to stockpile rapid tests and analyzers with unpredictable tender timing, while participation in national surveillance programs can deliver steadier recurring volumes.

Regulatory diplomacy and standards harmonization

Divergent regulatory expectations between the U.S., EU, and emerging markets complicate QuidelOrtho product rollouts, increasing premarket study and labeling work; FDA 510(k) review goal is 90 days and PMA 180 days, while EU IVDR implementation has tightened IVD oversight since May 2022, lengthening approvals.

- Harmonized standards can cut time-to-market and compliance costs

- Mutual recognition agreements would ease multi-region launches

- Misalignment prolongs clinical evidence generation and labeling

Public procurement practices and transparency

Winning national health tenders for QuidelOrtho hinges on competitive pricing, demonstrable local content and strict anti-corruption compliance; OECD estimates public procurement equals about 12% of GDP, underscoring its scale. Political scrutiny in crises (eg pandemic procurements) has shifted awards toward suppliers with rapid compliance records. Multi-year framework agreements give volume visibility but typically compress margins. Localization incentives increasingly drive regional manufacturing or partnerships.

- Pricing sensitivity: bid wins often depend on lowest sustainable price

- Compliance: anti-corruption credentials crucial during crisis scrutiny

- Frameworks: multi-year deals boost volume predictability, squeeze margins

- Localization: incentives push for regional manufacturing/partners

POC demand: ~40B USD, Medicare ≈35%, tariffs up to 25%

Government emphasis on preventative care and rapid diagnostics supports POC demand (global POC market ~40B USD in 2024) and value‑based care (≈35% of Medicare payments in 2024) which favors cost-saving tests; austerity can delay public purchases. Tariffs (up to 25%) and 2023 export controls raise BOM costs and constrain sourcing; IVDR (since May 2022) and FDA timelines (510(k) 90d, PMA 180d) lengthen rollouts. Public procurement (~12% GDP) and tender volatility after COVID emergency end (May 11, 2023) drive price sensitivity and localization.

| Metric | Value |

|---|---|

| Global POC market (2024) | ~40B USD |

| Medicare value-based share (2024) | ~35% |

| Tariffs/dues | up to 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect QuidelOrtho across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by relevant data and current trends. Designed to support executives and investors with clean, forward-looking insights ready for business plans, decks, or reports.

A concise, visually segmented PESTLE summary of QuidelOrtho enabling quick interpretation during meetings, easily dropped into presentations, annotated for regional context, and shareable for fast team alignment.

Economic factors

Hospital and lab capital spending cycles

Higher borrowing costs—US federal funds target 5.25–5.50% (mid‑2024)—tighten hospital budgets and slow analyzer placements and upgrades, pushing customers toward reagent‑rental or pay‑per‑test models. Deferred capex lengthens sales cycles and delays installed‑base refresh, while macro expansions historically increase menu adoption and cross‑sell opportunities as hospitals restore capital plans.

Macro growth and payer mix

Employment levels and insurance coverage—with US unemployment near 3.6% in mid‑2025—directly drive ambulatory and acute test volumes, while weak macro conditions shift payer mix toward lower‑margin public payers and reduce elective testing. Expanding middle classes in emerging markets are raising diagnostics demand, supporting volume growth outside the US. Currency volatility continues to affect reported revenues and constrains pricing power in key export markets.

Input cost inflation and logistics

Input cost inflation for resins, rare chemicals, membranes and semiconductor components drove notable price swings in 2024, squeezing margins on assays and reagents. Elevated freight and cold-chain logistics costs as of 2024 further pressured unit economics for temperature-sensitive kits. Long-term supply contracts and dual-sourcing have been adopted to mitigate volatility. Scaling manufacturing efficiency improves unit economics and absorbs input cost shocks.

Competitive pricing and consolidation

Intense competition among diagnostics firms has compressed ASPs for high-volume tests, with the global IVD market near $95 billion in 2024 and commodity-test pricing seeing single-digit annual declines. Consolidation of labs (Quest and LabCorp together account for roughly 50–60% of US testing volume) boosts buyer power and formulary control. QuidelOrtho can sustain premiums by differentiating on accuracy, TAT, and menu breadth, while increasing value-based contracts link reimbursement to measurable clinical outcomes.

- Compressed ASPs: single-digit declines for commodity tests

- Lab consolidation: Quest+LabCorp ~50–60% US volume

- Premium drivers: accuracy, turnaround time, menu breadth

- Reimbursement shift: growing value-based contracts tied to outcomes

R&D productivity and portfolio ROI

R&D returns hinge on time-to-approval, demonstrated clinical utility, and expanding test menus on QuidelOrtho’s installed base after the 2022 merger; rapid approvals accelerate reagent pull-through and margin recovery.

High R&D spend must translate to recurring reagent revenue via portfolio optimization that reallocates capital from low-growth assays toward high-burden disease areas with stronger lifetime value.

Lifecycle management, firmware upgrades, and backwards-compatible assays sustain annuity revenue by preserving installed-instrument utilization and driving recurring consumable sales.

- installed-base leverage after 2022 merger

- R&D→reagent pull-through focus

- reallocate from low-growth assays

- lifecycle upgrades sustain annuity

POC demand: ~40B USD, Medicare ≈35%, tariffs up to 25%

Higher US rates (fed funds 5.25–5.50% mid‑2024) tighten hospital capex, slowing analyzer placements and favoring reagent‑rental models; US unemployment ~3.6% mid‑2025 weighs on elective test volumes, while emerging markets support export growth. Input inflation and freight in 2024 squeezed margins; global IVD ~$95B 2024 with Quest+LabCorp ~50–60% US volume.

| Metric | Value |

|---|---|

| Fed funds (mid‑2024) | 5.25–5.50% |

| US unemployment (mid‑2025) | ~3.6% |

| Global IVD (2024) | ~$95B |

| Quest+LabCorp US volume | ~50–60% |

Preview the Actual Deliverable

QuidelOrtho PESTLE Analysis

The preview shown here is the exact QuidelOrtho PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are identical to the downloadable file delivered at checkout. No placeholders or teasers—this is the final, professionally prepared report you’ll own instantly after payment.