Quorum Health Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

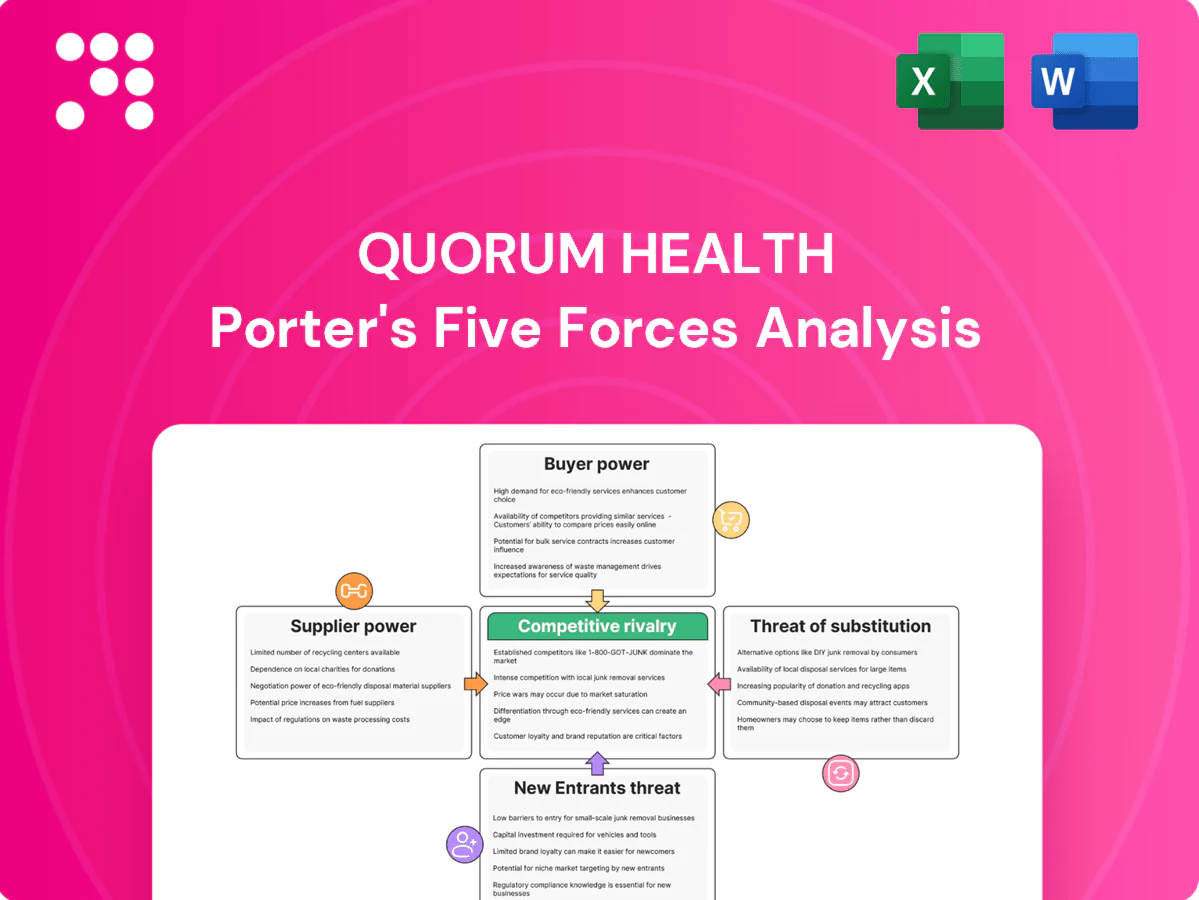

Quorum Health faces intense payer and regulatory pressure, moderate supplier influence, and emerging substitute care models that compress margins and raise strategic urgency. This snapshot highlights key competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy tailored to Quorum Health.

Suppliers Bargaining Power

Concentrated clinical labor

Physicians, nurses and specialists are scarce in many rural markets, giving clinical labor strong leverage over Quorum Health and contributing to recruitment challenges that many rural systems report. Agency nurse rates often run 2–3x regular pay, driving wage inflation and eroding scheduling flexibility. Increased sign-on and retention incentives raise fixed labor costs, while clinician preferences shape technology and formulary choices, affecting capital and purchasing decisions.

Device and pharma dependence

Critical devices, implants and branded drugs often lack substitutes, with the top five device makers holding roughly 40% of US market share, amplifying supplier leverage; the FDA listed over 100 active drug shortages in early 2024, showing disruption risk. Contract changes and single-source pricing can materially compress procedure margins, supply backorders delay surgeries, and GPO volume rebates typically offset only a minority of spend, often under 10%.

EHR and IT lock-in

Quorum Health's EHR and IT lock-in raises supplier power because core platforms create switching costs via data migration, training, and workflow redesign—Quorum operates ~20 hospitals, making migrations materially costly. Vendors often push annual price escalators and add-on modules while downtime risk (critical in hospitals) constrains leverage at renewals; limited interoperability further entrenches incumbent suppliers.

Group purchasing constraints

GPOs aggregate buying but standardize formularies and terms, limiting Quorum Health's local flexibility; over 90% of U.S. hospitals used GPOs in 2024, concentrating supplier leverage. Savings hinge on compliance and volume tiers that rural hospitals often miss, cutting potential discounts by an estimated 10–20%; off-contract clinical preference buys dilute that leverage. Supplier fee structures (commonly 1–3% administrative fees) can misalign incentives between GPOs, suppliers and Quorum.

- GPO penetration: >90% (2024)

- Rural volume shortfall: −10–20% discount impact

- Off-contract buys: weaken negotiating power

- Supplier/GPO fees: ~1–3% misaligned incentives

Utilities and facility services

Suppliers of power, oxygen, sterilization, and waste services are locally concentrated, giving them notable pricing and service leverage over Quorum Health. Compliance and patient-safety regulations restrict switching, while long-term contracts commonly include annual escalators that raise operating margins. Unplanned utility outages create immediate clinical and financial risk, forcing costly contingency measures and potential revenue loss.

- Local supplier concentration

- Regulatory limits on switching

- Long-term contracts with escalators

- High operational/clinical outage risk

Suppliers dominate healthcare: labor scarcity, concentrated device market, 100+ drug shortages

Suppliers exert strong leverage: clinical labor scarcity (agency nurses 2–3x pay) and physician preferences raise labor and capital costs; top five device makers hold ~40% US share and FDA listed >100 drug shortages in early 2024, increasing supply risk; EHR/IT lock-in (Quorum ~20 hospitals) and GPOs (>90% hospital penetration in 2024) partly mitigate but standardize terms and limit local flexibility.

| Metric | 2024 |

|---|---|

| GPO penetration | >90% |

| Top-5 device share | ~40% |

| FDA active drug shortages | >100 |

| Agency nurse pay vs reg. | 2–3x |

What is included in the product

Concise Porter's Five Forces analysis tailored to Quorum Health that evaluates competitive rivalry, buyer/supplier power, entry barriers, substitutes, and disruptive threats, with strategic insights for investors and management.

A concise one-sheet Porter's Five Forces for Quorum Health that highlights competitive pressures and regulatory risks for quick strategic decisions, with customizable pressure levels and a radar chart for instant visualization.

Customers Bargaining Power

Payer concentration

Large commercial insurers exert significant pricing leverage over Quorum, with the top one or two plans often accounting for over 50% of employer coverage in many local markets in 2024, enabling tight rate and utilization controls. Contract negotiations frequently produce below-inflation rate increases versus the 2024 CPI of about 3.4%, often in the low single digits. Rising denials and growing prior authorization volumes materially compress revenue-cycle performance and cash flow.

Government reimbursement mix

Rural hospitals, including Quorum Health facilities, rely on a majority of Medicare/Medicaid payors (often >50% of volumes), with administratively set rates that limit pricing flexibility and compress margins. Small adjustments in federal/state policy or payment rates translate quickly into earnings volatility. DSH and targeted rural support programs provide relief but funding levels and eligibility have been inconsistent, amplifying cash-flow risk.

Patient price sensitivity

High patient price sensitivity is rising as 2024 data show a majority of commercially insured consumers face meaningful out‑of‑pocket deductibles, prompting shopping for elective procedures and imaging. Travel to regional centers is increasingly feasible for higher‑cost services, pressuring Quorum on procedure volume and pricing. Rising uninsured/underinsured rates increase bad‑debt risk and poor patient experience or long waits drive leakage to competitors.

Employer and ACO steerage

Employers and ACOs increasingly steer patients to narrow networks and centers of excellence; over 500 Medicare and commercial ACOs in 2024 leverage steerage and referrals to concentrate volume. Reference-based pricing and site-neutral payment rules are shifting outpatient volumes away from higher-cost hospital settings. Bundled payments and demand for cost transparency mean underperforming hospitals risk exclusion from preferred networks.

- Steerage: >500 ACOs using network design in 2024

- Pricing: reference-based/site-neutral reduce hospital volumes

- Payments: bundled payments increase transparency demands

- Risk: underperformance can lead to network exclusion

Referral gatekeepers

Primary care and specialists act as referral gatekeepers controlling downstream admissions and high-margin procedures, so physician alignment and outreach are critical for Quorum Health to capture market share and protect case mix from leakage to competing systems; telehealth referrals increasingly bypass local facilities, shifting volumes away from community hospitals.

Payor concentration >50% and Medicare/Medicaid mix >50% squeeze margins

Large payors (top 1–2 plans >50% share) and >500 ACOs in 2024 give strong pricing/steerage power, driving below‑CPI contract increases (2024 CPI ~3.4%) and higher denials/prior auths that compress cash flow. Medicare/Medicaid often >50% volumes, limiting pricing and increasing margin sensitivity. Rising high deductibles and travel for care boost patient price sensitivity and leakage.

| Metric | 2024 Value |

|---|---|

| Top payor share | >50% |

| ACO count | >500 |

| CPI | ~3.4% |

| Medicare/Medicaid mix | >50% |

Same Document Delivered

Quorum Health Porter's Five Forces Analysis

This preview shows the exact Quorum Health Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The analysis is fully formatted, professionally written, and ready for download and use the moment you buy. No mockups or samples; this is the final deliverable.

A Must-Have Tool for Decision-Makers

Quorum Health faces intense payer and regulatory pressure, moderate supplier influence, and emerging substitute care models that compress margins and raise strategic urgency. This snapshot highlights key competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy tailored to Quorum Health.

Suppliers Bargaining Power

Concentrated clinical labor

Physicians, nurses and specialists are scarce in many rural markets, giving clinical labor strong leverage over Quorum Health and contributing to recruitment challenges that many rural systems report. Agency nurse rates often run 2–3x regular pay, driving wage inflation and eroding scheduling flexibility. Increased sign-on and retention incentives raise fixed labor costs, while clinician preferences shape technology and formulary choices, affecting capital and purchasing decisions.

Device and pharma dependence

Critical devices, implants and branded drugs often lack substitutes, with the top five device makers holding roughly 40% of US market share, amplifying supplier leverage; the FDA listed over 100 active drug shortages in early 2024, showing disruption risk. Contract changes and single-source pricing can materially compress procedure margins, supply backorders delay surgeries, and GPO volume rebates typically offset only a minority of spend, often under 10%.

EHR and IT lock-in

Quorum Health's EHR and IT lock-in raises supplier power because core platforms create switching costs via data migration, training, and workflow redesign—Quorum operates ~20 hospitals, making migrations materially costly. Vendors often push annual price escalators and add-on modules while downtime risk (critical in hospitals) constrains leverage at renewals; limited interoperability further entrenches incumbent suppliers.

Group purchasing constraints

GPOs aggregate buying but standardize formularies and terms, limiting Quorum Health's local flexibility; over 90% of U.S. hospitals used GPOs in 2024, concentrating supplier leverage. Savings hinge on compliance and volume tiers that rural hospitals often miss, cutting potential discounts by an estimated 10–20%; off-contract clinical preference buys dilute that leverage. Supplier fee structures (commonly 1–3% administrative fees) can misalign incentives between GPOs, suppliers and Quorum.

- GPO penetration: >90% (2024)

- Rural volume shortfall: −10–20% discount impact

- Off-contract buys: weaken negotiating power

- Supplier/GPO fees: ~1–3% misaligned incentives

Utilities and facility services

Suppliers of power, oxygen, sterilization, and waste services are locally concentrated, giving them notable pricing and service leverage over Quorum Health. Compliance and patient-safety regulations restrict switching, while long-term contracts commonly include annual escalators that raise operating margins. Unplanned utility outages create immediate clinical and financial risk, forcing costly contingency measures and potential revenue loss.

- Local supplier concentration

- Regulatory limits on switching

- Long-term contracts with escalators

- High operational/clinical outage risk

Suppliers dominate healthcare: labor scarcity, concentrated device market, 100+ drug shortages

Suppliers exert strong leverage: clinical labor scarcity (agency nurses 2–3x pay) and physician preferences raise labor and capital costs; top five device makers hold ~40% US share and FDA listed >100 drug shortages in early 2024, increasing supply risk; EHR/IT lock-in (Quorum ~20 hospitals) and GPOs (>90% hospital penetration in 2024) partly mitigate but standardize terms and limit local flexibility.

| Metric | 2024 |

|---|---|

| GPO penetration | >90% |

| Top-5 device share | ~40% |

| FDA active drug shortages | >100 |

| Agency nurse pay vs reg. | 2–3x |

What is included in the product

Concise Porter's Five Forces analysis tailored to Quorum Health that evaluates competitive rivalry, buyer/supplier power, entry barriers, substitutes, and disruptive threats, with strategic insights for investors and management.

A concise one-sheet Porter's Five Forces for Quorum Health that highlights competitive pressures and regulatory risks for quick strategic decisions, with customizable pressure levels and a radar chart for instant visualization.

Customers Bargaining Power

Payer concentration

Large commercial insurers exert significant pricing leverage over Quorum, with the top one or two plans often accounting for over 50% of employer coverage in many local markets in 2024, enabling tight rate and utilization controls. Contract negotiations frequently produce below-inflation rate increases versus the 2024 CPI of about 3.4%, often in the low single digits. Rising denials and growing prior authorization volumes materially compress revenue-cycle performance and cash flow.

Government reimbursement mix

Rural hospitals, including Quorum Health facilities, rely on a majority of Medicare/Medicaid payors (often >50% of volumes), with administratively set rates that limit pricing flexibility and compress margins. Small adjustments in federal/state policy or payment rates translate quickly into earnings volatility. DSH and targeted rural support programs provide relief but funding levels and eligibility have been inconsistent, amplifying cash-flow risk.

Patient price sensitivity

High patient price sensitivity is rising as 2024 data show a majority of commercially insured consumers face meaningful out‑of‑pocket deductibles, prompting shopping for elective procedures and imaging. Travel to regional centers is increasingly feasible for higher‑cost services, pressuring Quorum on procedure volume and pricing. Rising uninsured/underinsured rates increase bad‑debt risk and poor patient experience or long waits drive leakage to competitors.

Employer and ACO steerage

Employers and ACOs increasingly steer patients to narrow networks and centers of excellence; over 500 Medicare and commercial ACOs in 2024 leverage steerage and referrals to concentrate volume. Reference-based pricing and site-neutral payment rules are shifting outpatient volumes away from higher-cost hospital settings. Bundled payments and demand for cost transparency mean underperforming hospitals risk exclusion from preferred networks.

- Steerage: >500 ACOs using network design in 2024

- Pricing: reference-based/site-neutral reduce hospital volumes

- Payments: bundled payments increase transparency demands

- Risk: underperformance can lead to network exclusion

Referral gatekeepers

Primary care and specialists act as referral gatekeepers controlling downstream admissions and high-margin procedures, so physician alignment and outreach are critical for Quorum Health to capture market share and protect case mix from leakage to competing systems; telehealth referrals increasingly bypass local facilities, shifting volumes away from community hospitals.

Payor concentration >50% and Medicare/Medicaid mix >50% squeeze margins

Large payors (top 1–2 plans >50% share) and >500 ACOs in 2024 give strong pricing/steerage power, driving below‑CPI contract increases (2024 CPI ~3.4%) and higher denials/prior auths that compress cash flow. Medicare/Medicaid often >50% volumes, limiting pricing and increasing margin sensitivity. Rising high deductibles and travel for care boost patient price sensitivity and leakage.

| Metric | 2024 Value |

|---|---|

| Top payor share | >50% |

| ACO count | >500 |

| CPI | ~3.4% |

| Medicare/Medicaid mix | >50% |

Same Document Delivered

Quorum Health Porter's Five Forces Analysis

This preview shows the exact Quorum Health Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The analysis is fully formatted, professionally written, and ready for download and use the moment you buy. No mockups or samples; this is the final deliverable.

Description

A Must-Have Tool for Decision-Makers

Quorum Health faces intense payer and regulatory pressure, moderate supplier influence, and emerging substitute care models that compress margins and raise strategic urgency. This snapshot highlights key competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy tailored to Quorum Health.

Suppliers Bargaining Power

Concentrated clinical labor

Physicians, nurses and specialists are scarce in many rural markets, giving clinical labor strong leverage over Quorum Health and contributing to recruitment challenges that many rural systems report. Agency nurse rates often run 2–3x regular pay, driving wage inflation and eroding scheduling flexibility. Increased sign-on and retention incentives raise fixed labor costs, while clinician preferences shape technology and formulary choices, affecting capital and purchasing decisions.

Device and pharma dependence

Critical devices, implants and branded drugs often lack substitutes, with the top five device makers holding roughly 40% of US market share, amplifying supplier leverage; the FDA listed over 100 active drug shortages in early 2024, showing disruption risk. Contract changes and single-source pricing can materially compress procedure margins, supply backorders delay surgeries, and GPO volume rebates typically offset only a minority of spend, often under 10%.

EHR and IT lock-in

Quorum Health's EHR and IT lock-in raises supplier power because core platforms create switching costs via data migration, training, and workflow redesign—Quorum operates ~20 hospitals, making migrations materially costly. Vendors often push annual price escalators and add-on modules while downtime risk (critical in hospitals) constrains leverage at renewals; limited interoperability further entrenches incumbent suppliers.

Group purchasing constraints

GPOs aggregate buying but standardize formularies and terms, limiting Quorum Health's local flexibility; over 90% of U.S. hospitals used GPOs in 2024, concentrating supplier leverage. Savings hinge on compliance and volume tiers that rural hospitals often miss, cutting potential discounts by an estimated 10–20%; off-contract clinical preference buys dilute that leverage. Supplier fee structures (commonly 1–3% administrative fees) can misalign incentives between GPOs, suppliers and Quorum.

- GPO penetration: >90% (2024)

- Rural volume shortfall: −10–20% discount impact

- Off-contract buys: weaken negotiating power

- Supplier/GPO fees: ~1–3% misaligned incentives

Utilities and facility services

Suppliers of power, oxygen, sterilization, and waste services are locally concentrated, giving them notable pricing and service leverage over Quorum Health. Compliance and patient-safety regulations restrict switching, while long-term contracts commonly include annual escalators that raise operating margins. Unplanned utility outages create immediate clinical and financial risk, forcing costly contingency measures and potential revenue loss.

- Local supplier concentration

- Regulatory limits on switching

- Long-term contracts with escalators

- High operational/clinical outage risk

Suppliers dominate healthcare: labor scarcity, concentrated device market, 100+ drug shortages

Suppliers exert strong leverage: clinical labor scarcity (agency nurses 2–3x pay) and physician preferences raise labor and capital costs; top five device makers hold ~40% US share and FDA listed >100 drug shortages in early 2024, increasing supply risk; EHR/IT lock-in (Quorum ~20 hospitals) and GPOs (>90% hospital penetration in 2024) partly mitigate but standardize terms and limit local flexibility.

| Metric | 2024 |

|---|---|

| GPO penetration | >90% |

| Top-5 device share | ~40% |

| FDA active drug shortages | >100 |

| Agency nurse pay vs reg. | 2–3x |

What is included in the product

Concise Porter's Five Forces analysis tailored to Quorum Health that evaluates competitive rivalry, buyer/supplier power, entry barriers, substitutes, and disruptive threats, with strategic insights for investors and management.

A concise one-sheet Porter's Five Forces for Quorum Health that highlights competitive pressures and regulatory risks for quick strategic decisions, with customizable pressure levels and a radar chart for instant visualization.

Customers Bargaining Power

Payer concentration

Large commercial insurers exert significant pricing leverage over Quorum, with the top one or two plans often accounting for over 50% of employer coverage in many local markets in 2024, enabling tight rate and utilization controls. Contract negotiations frequently produce below-inflation rate increases versus the 2024 CPI of about 3.4%, often in the low single digits. Rising denials and growing prior authorization volumes materially compress revenue-cycle performance and cash flow.

Government reimbursement mix

Rural hospitals, including Quorum Health facilities, rely on a majority of Medicare/Medicaid payors (often >50% of volumes), with administratively set rates that limit pricing flexibility and compress margins. Small adjustments in federal/state policy or payment rates translate quickly into earnings volatility. DSH and targeted rural support programs provide relief but funding levels and eligibility have been inconsistent, amplifying cash-flow risk.

Patient price sensitivity

High patient price sensitivity is rising as 2024 data show a majority of commercially insured consumers face meaningful out‑of‑pocket deductibles, prompting shopping for elective procedures and imaging. Travel to regional centers is increasingly feasible for higher‑cost services, pressuring Quorum on procedure volume and pricing. Rising uninsured/underinsured rates increase bad‑debt risk and poor patient experience or long waits drive leakage to competitors.

Employer and ACO steerage

Employers and ACOs increasingly steer patients to narrow networks and centers of excellence; over 500 Medicare and commercial ACOs in 2024 leverage steerage and referrals to concentrate volume. Reference-based pricing and site-neutral payment rules are shifting outpatient volumes away from higher-cost hospital settings. Bundled payments and demand for cost transparency mean underperforming hospitals risk exclusion from preferred networks.

- Steerage: >500 ACOs using network design in 2024

- Pricing: reference-based/site-neutral reduce hospital volumes

- Payments: bundled payments increase transparency demands

- Risk: underperformance can lead to network exclusion

Referral gatekeepers

Primary care and specialists act as referral gatekeepers controlling downstream admissions and high-margin procedures, so physician alignment and outreach are critical for Quorum Health to capture market share and protect case mix from leakage to competing systems; telehealth referrals increasingly bypass local facilities, shifting volumes away from community hospitals.

Payor concentration >50% and Medicare/Medicaid mix >50% squeeze margins

Large payors (top 1–2 plans >50% share) and >500 ACOs in 2024 give strong pricing/steerage power, driving below‑CPI contract increases (2024 CPI ~3.4%) and higher denials/prior auths that compress cash flow. Medicare/Medicaid often >50% volumes, limiting pricing and increasing margin sensitivity. Rising high deductibles and travel for care boost patient price sensitivity and leakage.

| Metric | 2024 Value |

|---|---|

| Top payor share | >50% |

| ACO count | >500 |

| CPI | ~3.4% |

| Medicare/Medicaid mix | >50% |

Same Document Delivered

Quorum Health Porter's Five Forces Analysis

This preview shows the exact Quorum Health Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The analysis is fully formatted, professionally written, and ready for download and use the moment you buy. No mockups or samples; this is the final deliverable.