RadNet Porter's Five Forces Analysis

From Overview to Strategy Blueprint

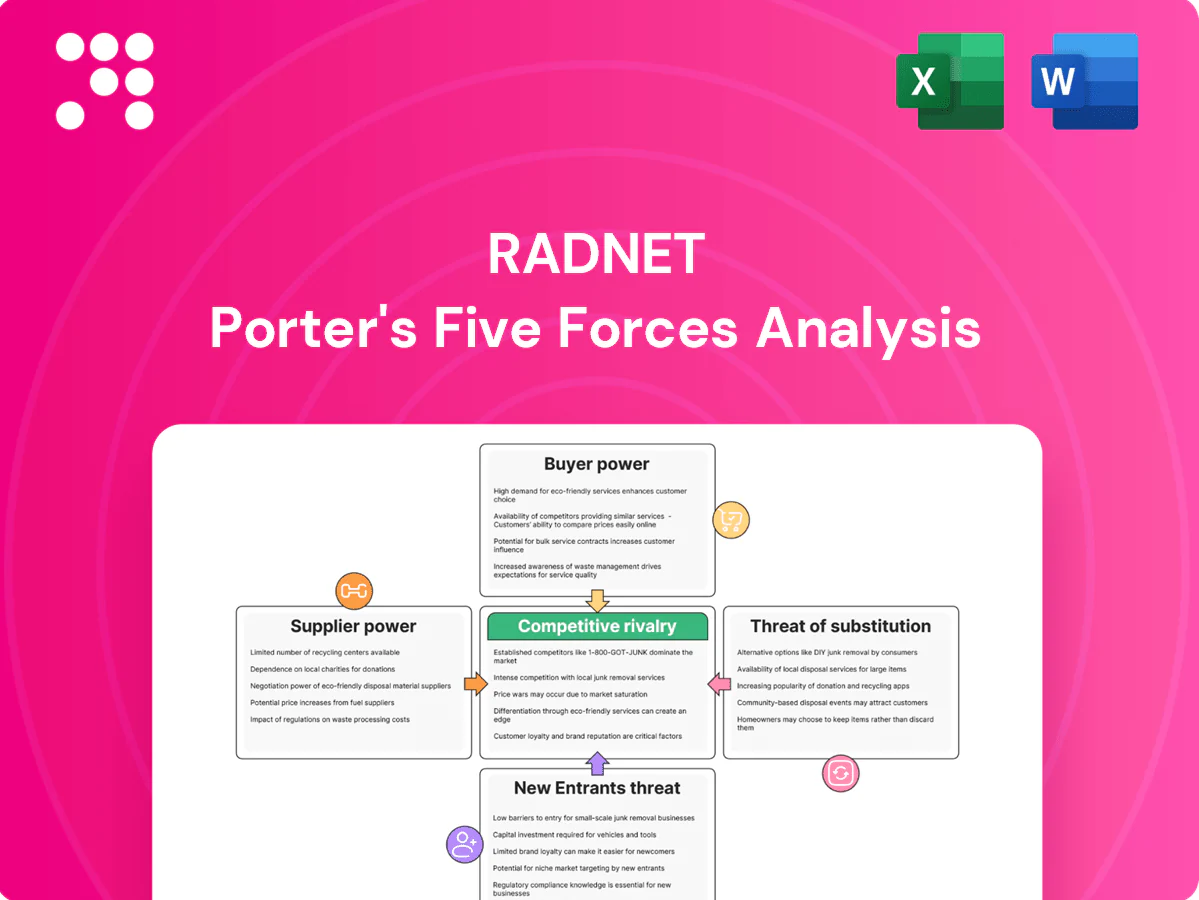

RadNet faces mixed pressures—strong buyer bargaining from payers and consolidation-driven supplier leverage, moderate threat of new entrants, and rising substitute risks from outpatient imaging centers; strategic positioning hinges on scale and payer relationships. This brief scratches the surface—unlock the full Porter’s Five Forces for detailed ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated OEM imaging vendors

Major MRI/CT OEMs (Siemens, GE, Philips) control roughly three-quarters of the global market, giving them pricing and terms leverage over buyers. Multi-year service contracts (commonly 5–10 years) and proprietary parts create high switching costs for RadNet, which operates approximately 350 outpatient imaging sites. RadNet mitigates this via volume purchasing and multi-vendor portfolios, but new modalities and frequent upgrades keep dependence elevated.

Maintenance and service agreements

Uptime is mission-critical for RadNet, which operates more than 300 outpatient imaging centers, making OEMs and third-party service providers influential in availability. Long-term service agreements commonly include escalation clauses and 99%+ uptime SLAs that shift negotiation power to suppliers. Investment in predictive maintenance and in-house biomedical teams can reduce service leverage. Downtime penalties and multi-source SLAs improve RadNet’s bargaining position.

Skilled radiologist and technologist labor

Skilled radiologists and specialized technologists are scarce in many U.S. markets, with BLS projecting 6% employment growth for diagnostic medical sonographers and related technologists 2022–32, tightening supply and driving wage pressure in 2024. Tight labor markets and growing subspecialty demand push compensation up; RadNet’s national scale and teleradiology capacity let it distribute case load and lower marginal staffing costs. Investment in training pipelines, retention programs and flexible scheduling further reduces supplier leverage by improving throughput and lowering turnover.

AI/software and PACS/RIS vendors

Best-in-class AI, PACS, and RIS capabilities remain concentrated: top 4 vendors hold about 70% of the PACS/RIS market in 2024, creating integration lock-in and per-study fees that elevate unit costs; API-first stacks and negotiated enterprise licenses (often reducing per-study spend 20–40% in 2024) mitigate this, while internal AI development has cut vendor dependency and related spend by roughly 20–30% among peers in 2024.

- Concentration: top-4 ≈70% (2024)

- Per-study fees raise marginal cost; enterprise licenses save 20–40% (2024)

- API-first reduces switching costs

- Internal AI lowers vendor leverage ~20–30% (2024)

Contrast agents and disposables

Contrast media and single-use disposables exert intermittent supplier power due to periodic shortages and price volatility driven by manufacturing recalls and supply-chain shocks, which can sharply raise imaging costs and margins pressure for providers like RadNet.

- Dual-sourcing reduces single-vendor exposure

- Inventory management cushions stock-outs

- Standardization across centers increases purchasing scale

Suppliers ~75% share; 99%+ uptime, long service lock

OEMs (Siemens/GE/Philips) hold ~75% MRI/CT share, creating price/parts leverage; long 5–10y service contracts and proprietary parts raise switching costs. Critical uptime (99%+ SLAs) and concentrated PACS/RIS (top‑4 ≈70% in 2024) shift power to suppliers, though RadNet scale, multi-vendor sourcing, in‑house AI (cuts vendor spend ~20–30%) and dual‑sourcing reduce it.

| Metric | Value (2024) |

|---|---|

| MRI/CT OEM share | ~75% |

| PACS/RIS top‑4 | ~70% |

| Service length | 5–10 years |

| Uptime SLA | 99%+ |

| AI vendor spend cut | 20–30% |

What is included in the product

Comprehensive Porter's Five Forces for RadNet that dissects competitive rivalry, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic insights and editable formatting for investor or internal use.

A clear, one-sheet Porter's Five Forces for RadNet that pinpoints competitive pain points and accelerates strategic decisions, with customizable pressure levels and a radar view for instant, board-ready insights.

Customers Bargaining Power

Commercial payers and Medicare

Reimbursement rates are largely set or negotiated, giving commercial payers and Medicare substantial leverage over RadNet pricing and margins. Site-neutral payment rules and expanding prior-authorization policies in 2023–2024 have compressed price and volume for outpatient imaging. Scale-based contracts and quality metrics enable RadNet to secure better terms with payers when negotiating managed-care and Medicare Advantage deals. Medicare Advantage enrollment exceeded 30 million in 2024, underscoring payer influence.

Physician groups and referral networks

Referrals drive volumes and power concentrates with large physician groups and IDNs; RadNet operated about 324 outpatient imaging centers in 2024, making relationships with big referrers critical. Preferred‑provider lists and ACO alignment (covering roughly 12 million Medicare lives in 2024) steer patient flow away from independents. RadNet counters with facility access, faster turnaround, subspecialty reads, co‑marketing and EMR integration to deepen stickiness.

Price-sensitive patients

By 2024 roughly one-third of privately insured Americans were enrolled in high-deductible health plans, heightening out-of-pocket sensitivity among imaging patients. Patients increasingly compare price and convenience across centers, driving demand for transparent pricing. Easy online scheduling and clear fees reduce switching barriers, while a retail-like experience and faster results strengthen loyalty.

Self-insured employers and TPAs

Self-insured employers and TPAs actively steer employees to lower-cost outpatient imaging, often mandating bundled rates and centers of excellence; in 2024 direct-to-employer contracts accelerated, shifting meaningful MRI/CT volume away from hospital outpatient departments and pressuring RadNet pricing and utilization.

- Steerage-driven volume shift

- Bundled rates mandated

- Performance guarantees strengthen ties

- Navigation tools increase retention

Government and policy influence

Government policy shifts can reset reimbursement across imaging, with Medicare Advantage enrollment reaching about 30 million in 2024, increasing payer leverage over rates. Prior authorization, appropriate-use criteria and intensified audits have already reduced utilization in several markets, pressuring margins. Excellence in compliance preserves access and revenue while advocacy and data-sharing shape payer policies and coverage decisions.

- Policy reset risk: higher payer leverage

- Utilization controls: prior auth, AUC, audits

- Compliance: protects access/revenue

- Advocacy/data: influences payer rules

Payer Leverage, Medicare Advantage, and HDHPs Compress Imaging Margins; Referral Risk

Payers and Medicare (Medicare Advantage ~30M in 2024) exert strong pricing leverage through negotiated rates, site-neutral rules and prior authorization, compressing margins. Referrals from large IDNs/physician groups (RadNet ~324 centers in 2024) concentrate volume risk. Rising HDHP prevalence (~33% privately insured in 2024) and employer steering increase price sensitivity and bundled-rate pressure.

| Metric | 2024 |

|---|---|

| RadNet centers | ~324 |

| Medicare Advantage enrollees | ~30M |

| HDHP privately insured | ~33% |

Full Version Awaits

RadNet Porter's Five Forces Analysis

This preview shows the exact RadNet Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the professionally written, fully formatted file ready for download and use the moment you buy. You're looking at the actual deliverable and will get instant access to this same complete analysis upon payment.

From Overview to Strategy Blueprint

RadNet faces mixed pressures—strong buyer bargaining from payers and consolidation-driven supplier leverage, moderate threat of new entrants, and rising substitute risks from outpatient imaging centers; strategic positioning hinges on scale and payer relationships. This brief scratches the surface—unlock the full Porter’s Five Forces for detailed ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated OEM imaging vendors

Major MRI/CT OEMs (Siemens, GE, Philips) control roughly three-quarters of the global market, giving them pricing and terms leverage over buyers. Multi-year service contracts (commonly 5–10 years) and proprietary parts create high switching costs for RadNet, which operates approximately 350 outpatient imaging sites. RadNet mitigates this via volume purchasing and multi-vendor portfolios, but new modalities and frequent upgrades keep dependence elevated.

Maintenance and service agreements

Uptime is mission-critical for RadNet, which operates more than 300 outpatient imaging centers, making OEMs and third-party service providers influential in availability. Long-term service agreements commonly include escalation clauses and 99%+ uptime SLAs that shift negotiation power to suppliers. Investment in predictive maintenance and in-house biomedical teams can reduce service leverage. Downtime penalties and multi-source SLAs improve RadNet’s bargaining position.

Skilled radiologist and technologist labor

Skilled radiologists and specialized technologists are scarce in many U.S. markets, with BLS projecting 6% employment growth for diagnostic medical sonographers and related technologists 2022–32, tightening supply and driving wage pressure in 2024. Tight labor markets and growing subspecialty demand push compensation up; RadNet’s national scale and teleradiology capacity let it distribute case load and lower marginal staffing costs. Investment in training pipelines, retention programs and flexible scheduling further reduces supplier leverage by improving throughput and lowering turnover.

AI/software and PACS/RIS vendors

Best-in-class AI, PACS, and RIS capabilities remain concentrated: top 4 vendors hold about 70% of the PACS/RIS market in 2024, creating integration lock-in and per-study fees that elevate unit costs; API-first stacks and negotiated enterprise licenses (often reducing per-study spend 20–40% in 2024) mitigate this, while internal AI development has cut vendor dependency and related spend by roughly 20–30% among peers in 2024.

- Concentration: top-4 ≈70% (2024)

- Per-study fees raise marginal cost; enterprise licenses save 20–40% (2024)

- API-first reduces switching costs

- Internal AI lowers vendor leverage ~20–30% (2024)

Contrast agents and disposables

Contrast media and single-use disposables exert intermittent supplier power due to periodic shortages and price volatility driven by manufacturing recalls and supply-chain shocks, which can sharply raise imaging costs and margins pressure for providers like RadNet.

- Dual-sourcing reduces single-vendor exposure

- Inventory management cushions stock-outs

- Standardization across centers increases purchasing scale

Suppliers ~75% share; 99%+ uptime, long service lock

OEMs (Siemens/GE/Philips) hold ~75% MRI/CT share, creating price/parts leverage; long 5–10y service contracts and proprietary parts raise switching costs. Critical uptime (99%+ SLAs) and concentrated PACS/RIS (top‑4 ≈70% in 2024) shift power to suppliers, though RadNet scale, multi-vendor sourcing, in‑house AI (cuts vendor spend ~20–30%) and dual‑sourcing reduce it.

| Metric | Value (2024) |

|---|---|

| MRI/CT OEM share | ~75% |

| PACS/RIS top‑4 | ~70% |

| Service length | 5–10 years |

| Uptime SLA | 99%+ |

| AI vendor spend cut | 20–30% |

What is included in the product

Comprehensive Porter's Five Forces for RadNet that dissects competitive rivalry, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic insights and editable formatting for investor or internal use.

A clear, one-sheet Porter's Five Forces for RadNet that pinpoints competitive pain points and accelerates strategic decisions, with customizable pressure levels and a radar view for instant, board-ready insights.

Customers Bargaining Power

Commercial payers and Medicare

Reimbursement rates are largely set or negotiated, giving commercial payers and Medicare substantial leverage over RadNet pricing and margins. Site-neutral payment rules and expanding prior-authorization policies in 2023–2024 have compressed price and volume for outpatient imaging. Scale-based contracts and quality metrics enable RadNet to secure better terms with payers when negotiating managed-care and Medicare Advantage deals. Medicare Advantage enrollment exceeded 30 million in 2024, underscoring payer influence.

Physician groups and referral networks

Referrals drive volumes and power concentrates with large physician groups and IDNs; RadNet operated about 324 outpatient imaging centers in 2024, making relationships with big referrers critical. Preferred‑provider lists and ACO alignment (covering roughly 12 million Medicare lives in 2024) steer patient flow away from independents. RadNet counters with facility access, faster turnaround, subspecialty reads, co‑marketing and EMR integration to deepen stickiness.

Price-sensitive patients

By 2024 roughly one-third of privately insured Americans were enrolled in high-deductible health plans, heightening out-of-pocket sensitivity among imaging patients. Patients increasingly compare price and convenience across centers, driving demand for transparent pricing. Easy online scheduling and clear fees reduce switching barriers, while a retail-like experience and faster results strengthen loyalty.

Self-insured employers and TPAs

Self-insured employers and TPAs actively steer employees to lower-cost outpatient imaging, often mandating bundled rates and centers of excellence; in 2024 direct-to-employer contracts accelerated, shifting meaningful MRI/CT volume away from hospital outpatient departments and pressuring RadNet pricing and utilization.

- Steerage-driven volume shift

- Bundled rates mandated

- Performance guarantees strengthen ties

- Navigation tools increase retention

Government and policy influence

Government policy shifts can reset reimbursement across imaging, with Medicare Advantage enrollment reaching about 30 million in 2024, increasing payer leverage over rates. Prior authorization, appropriate-use criteria and intensified audits have already reduced utilization in several markets, pressuring margins. Excellence in compliance preserves access and revenue while advocacy and data-sharing shape payer policies and coverage decisions.

- Policy reset risk: higher payer leverage

- Utilization controls: prior auth, AUC, audits

- Compliance: protects access/revenue

- Advocacy/data: influences payer rules

Payer Leverage, Medicare Advantage, and HDHPs Compress Imaging Margins; Referral Risk

Payers and Medicare (Medicare Advantage ~30M in 2024) exert strong pricing leverage through negotiated rates, site-neutral rules and prior authorization, compressing margins. Referrals from large IDNs/physician groups (RadNet ~324 centers in 2024) concentrate volume risk. Rising HDHP prevalence (~33% privately insured in 2024) and employer steering increase price sensitivity and bundled-rate pressure.

| Metric | 2024 |

|---|---|

| RadNet centers | ~324 |

| Medicare Advantage enrollees | ~30M |

| HDHP privately insured | ~33% |

Full Version Awaits

RadNet Porter's Five Forces Analysis

This preview shows the exact RadNet Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the professionally written, fully formatted file ready for download and use the moment you buy. You're looking at the actual deliverable and will get instant access to this same complete analysis upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

RadNet faces mixed pressures—strong buyer bargaining from payers and consolidation-driven supplier leverage, moderate threat of new entrants, and rising substitute risks from outpatient imaging centers; strategic positioning hinges on scale and payer relationships. This brief scratches the surface—unlock the full Porter’s Five Forces for detailed ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated OEM imaging vendors

Major MRI/CT OEMs (Siemens, GE, Philips) control roughly three-quarters of the global market, giving them pricing and terms leverage over buyers. Multi-year service contracts (commonly 5–10 years) and proprietary parts create high switching costs for RadNet, which operates approximately 350 outpatient imaging sites. RadNet mitigates this via volume purchasing and multi-vendor portfolios, but new modalities and frequent upgrades keep dependence elevated.

Maintenance and service agreements

Uptime is mission-critical for RadNet, which operates more than 300 outpatient imaging centers, making OEMs and third-party service providers influential in availability. Long-term service agreements commonly include escalation clauses and 99%+ uptime SLAs that shift negotiation power to suppliers. Investment in predictive maintenance and in-house biomedical teams can reduce service leverage. Downtime penalties and multi-source SLAs improve RadNet’s bargaining position.

Skilled radiologist and technologist labor

Skilled radiologists and specialized technologists are scarce in many U.S. markets, with BLS projecting 6% employment growth for diagnostic medical sonographers and related technologists 2022–32, tightening supply and driving wage pressure in 2024. Tight labor markets and growing subspecialty demand push compensation up; RadNet’s national scale and teleradiology capacity let it distribute case load and lower marginal staffing costs. Investment in training pipelines, retention programs and flexible scheduling further reduces supplier leverage by improving throughput and lowering turnover.

AI/software and PACS/RIS vendors

Best-in-class AI, PACS, and RIS capabilities remain concentrated: top 4 vendors hold about 70% of the PACS/RIS market in 2024, creating integration lock-in and per-study fees that elevate unit costs; API-first stacks and negotiated enterprise licenses (often reducing per-study spend 20–40% in 2024) mitigate this, while internal AI development has cut vendor dependency and related spend by roughly 20–30% among peers in 2024.

- Concentration: top-4 ≈70% (2024)

- Per-study fees raise marginal cost; enterprise licenses save 20–40% (2024)

- API-first reduces switching costs

- Internal AI lowers vendor leverage ~20–30% (2024)

Contrast agents and disposables

Contrast media and single-use disposables exert intermittent supplier power due to periodic shortages and price volatility driven by manufacturing recalls and supply-chain shocks, which can sharply raise imaging costs and margins pressure for providers like RadNet.

- Dual-sourcing reduces single-vendor exposure

- Inventory management cushions stock-outs

- Standardization across centers increases purchasing scale

Suppliers ~75% share; 99%+ uptime, long service lock

OEMs (Siemens/GE/Philips) hold ~75% MRI/CT share, creating price/parts leverage; long 5–10y service contracts and proprietary parts raise switching costs. Critical uptime (99%+ SLAs) and concentrated PACS/RIS (top‑4 ≈70% in 2024) shift power to suppliers, though RadNet scale, multi-vendor sourcing, in‑house AI (cuts vendor spend ~20–30%) and dual‑sourcing reduce it.

| Metric | Value (2024) |

|---|---|

| MRI/CT OEM share | ~75% |

| PACS/RIS top‑4 | ~70% |

| Service length | 5–10 years |

| Uptime SLA | 99%+ |

| AI vendor spend cut | 20–30% |

What is included in the product

Comprehensive Porter's Five Forces for RadNet that dissects competitive rivalry, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic insights and editable formatting for investor or internal use.

A clear, one-sheet Porter's Five Forces for RadNet that pinpoints competitive pain points and accelerates strategic decisions, with customizable pressure levels and a radar view for instant, board-ready insights.

Customers Bargaining Power

Commercial payers and Medicare

Reimbursement rates are largely set or negotiated, giving commercial payers and Medicare substantial leverage over RadNet pricing and margins. Site-neutral payment rules and expanding prior-authorization policies in 2023–2024 have compressed price and volume for outpatient imaging. Scale-based contracts and quality metrics enable RadNet to secure better terms with payers when negotiating managed-care and Medicare Advantage deals. Medicare Advantage enrollment exceeded 30 million in 2024, underscoring payer influence.

Physician groups and referral networks

Referrals drive volumes and power concentrates with large physician groups and IDNs; RadNet operated about 324 outpatient imaging centers in 2024, making relationships with big referrers critical. Preferred‑provider lists and ACO alignment (covering roughly 12 million Medicare lives in 2024) steer patient flow away from independents. RadNet counters with facility access, faster turnaround, subspecialty reads, co‑marketing and EMR integration to deepen stickiness.

Price-sensitive patients

By 2024 roughly one-third of privately insured Americans were enrolled in high-deductible health plans, heightening out-of-pocket sensitivity among imaging patients. Patients increasingly compare price and convenience across centers, driving demand for transparent pricing. Easy online scheduling and clear fees reduce switching barriers, while a retail-like experience and faster results strengthen loyalty.

Self-insured employers and TPAs

Self-insured employers and TPAs actively steer employees to lower-cost outpatient imaging, often mandating bundled rates and centers of excellence; in 2024 direct-to-employer contracts accelerated, shifting meaningful MRI/CT volume away from hospital outpatient departments and pressuring RadNet pricing and utilization.

- Steerage-driven volume shift

- Bundled rates mandated

- Performance guarantees strengthen ties

- Navigation tools increase retention

Government and policy influence

Government policy shifts can reset reimbursement across imaging, with Medicare Advantage enrollment reaching about 30 million in 2024, increasing payer leverage over rates. Prior authorization, appropriate-use criteria and intensified audits have already reduced utilization in several markets, pressuring margins. Excellence in compliance preserves access and revenue while advocacy and data-sharing shape payer policies and coverage decisions.

- Policy reset risk: higher payer leverage

- Utilization controls: prior auth, AUC, audits

- Compliance: protects access/revenue

- Advocacy/data: influences payer rules

Payer Leverage, Medicare Advantage, and HDHPs Compress Imaging Margins; Referral Risk

Payers and Medicare (Medicare Advantage ~30M in 2024) exert strong pricing leverage through negotiated rates, site-neutral rules and prior authorization, compressing margins. Referrals from large IDNs/physician groups (RadNet ~324 centers in 2024) concentrate volume risk. Rising HDHP prevalence (~33% privately insured in 2024) and employer steering increase price sensitivity and bundled-rate pressure.

| Metric | 2024 |

|---|---|

| RadNet centers | ~324 |

| Medicare Advantage enrollees | ~30M |

| HDHP privately insured | ~33% |

Full Version Awaits

RadNet Porter's Five Forces Analysis

This preview shows the exact RadNet Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the professionally written, fully formatted file ready for download and use the moment you buy. You're looking at the actual deliverable and will get instant access to this same complete analysis upon payment.