Rallye Porter's Five Forces Analysis

From Overview to Strategy Blueprint

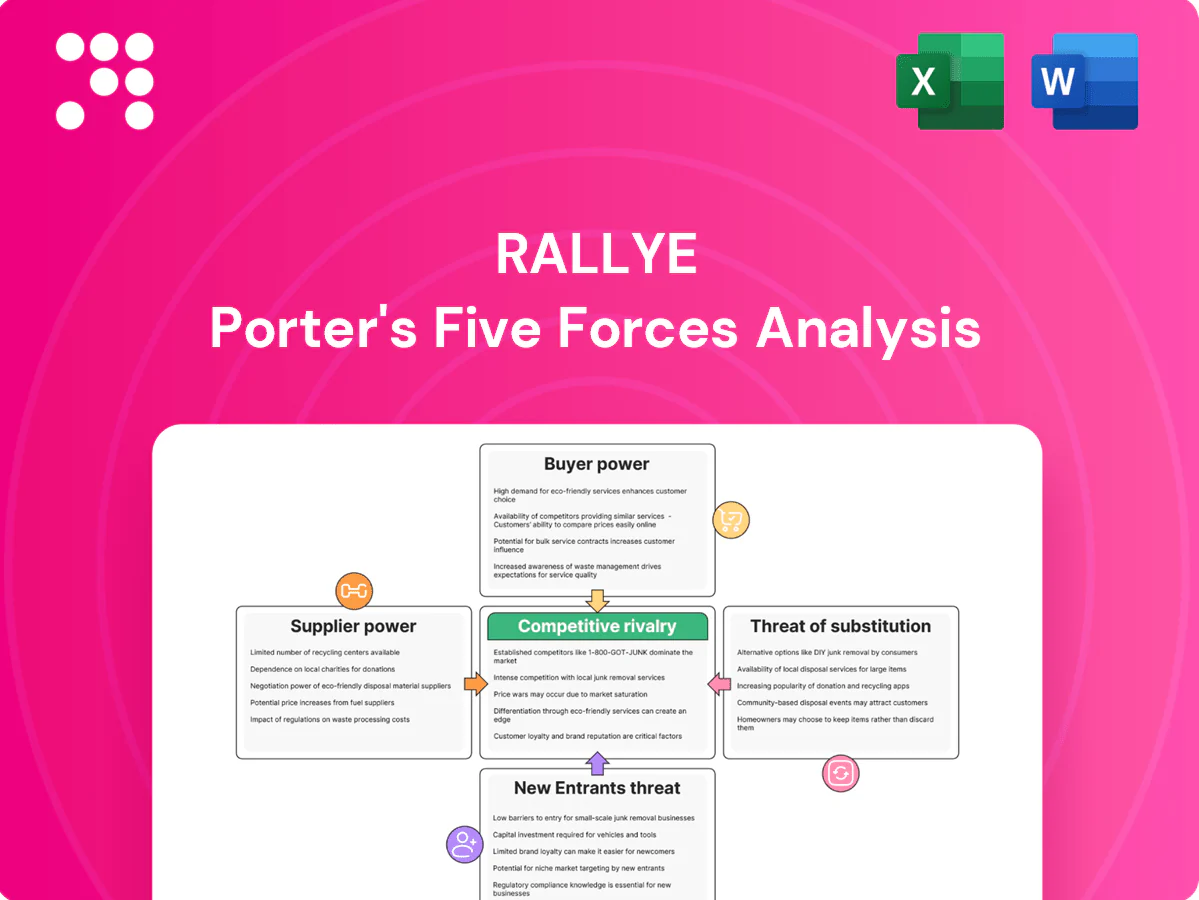

Rallye’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, and competitive intensity shaping its retail-conglomerate position. It surfaces key threats from new entrants and substitutes and flags strategic levers to defend margins. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Fragmented FMCG base

Most food and CPG categories are sourced from a fragmented supplier base, limiting individual vendors' leverage against Casino’s scale, while centralized procurement and private labels materially enhance bargaining clout. Category captains in beverages, hygiene and baby care still retain pricing power and can push tougher terms. Rallye’s net influence hinges on Casino’s purchasing alliances and volume commitments.

Private label leverage

Casino’s private brands substitute for national brands, lowering dependence on powerful suppliers and shifting category leverage toward the retailer. Improved margin mix and deliberate dual-sourcing strengthen negotiating power with national suppliers. Sustained consumer trust depends on rigorous quality controls and reliable supply chains. Switching costs for packaging and specifications create moderate stickiness for suppliers and co-manufacturers.

Fresh and local producers

Fruits, vegetables and meats often come from regional suppliers with limited scale, giving episodic leverage due to seasonality and perishability; roughly one-third of produced food is lost or wasted globally, amplifying supply sensitivity. Casino’s integrated logistics, forecasting and cold-chain investments reduce this volatility and buffer buying power. Certification and sustainability demands further narrow supplier pools, increasing supplier bargaining in peak seasons.

Non-merch suppliers (rent, IT, logistics)

Landlords, payment providers and logistics/IT vendors exert leverage via contract lock-ins: multi-year store leases and DC commitments create switching frictions, tech-stack dependencies raise integration costs, and payment fees (typically 1–3% of transaction value) and logistics (often 5–10% of sales) inflate operating leverage; competitive bidding and shared services can rebalance terms.

- Lease lock-ins: multi-year commitments

- Payment fees: 1–3% of transactions

- Logistics/IT: ~5–10% of sales

- Mitigants: competitive bidding, shared services

Regulatory and ESG constraints

French fair-trading reforms (EGalim, 2018) and EU sustainability rules such as the Corporate Sustainability Reporting Directive, which extends reporting to roughly 50,000 companies from 2024, constrain Rallye’s procurement tactics by enforcing transparency and fair pricing with agricultural suppliers. ESG sourcing standards limit rapid supplier substitution, often narrowing choice and increasing input cost pressure for food retailers. Long-term supplier partnerships partially offset these constraints by securing volumes and shared-compliance investments.

- EGalim: strengthens farmer-retailer pricing rules in France

- CSRD ~50,000 companies from 2024: greater disclosure burden

- ESG sourcing: reduces substitution, can raise input costs

- Long-term contracts: mitigate supplier power, enable joint ESG investments

Fragmented suppliers vs centralized buyers: logistics, payments and ESG squeeze margins

Supplier power is limited by fragmented food/CPG supply and Casino’s centralized procurement and private-label leverage, though category captains (beverages, hygiene) retain pricing power. Landlords, payments and logistics exert measurable leverage (leases multi-year; payment fees 1–3%; logistics 5–10% of sales). Regulations (EGalim, CSRD ~50,000 firms from 2024) and ESG sourcing narrow supplier pools seasonally.

| Metric | Value | Implication |

|---|---|---|

| Payment fees | 1–3% | Operating cost pressure |

| Logistics | 5–10% of sales | Negotiation leverage |

| CSRD scope | ~50,000 firms (from 2024) | Greater disclosure, sourcing constraints |

| Food waste | ~33% | Supply sensitivity/seasonality |

What is included in the product

Tailored Porter’s Five Forces analysis for Rallye that pinpoints competitive intensity, supplier and buyer bargaining power, threat of entrants and substitutes, and identifies disruptive risks and strategic levers to protect market share and improve profitability.

Rallye Porter's Five Forces Analysis delivers a clean, one-sheet summary with adjustable pressure levels and an instant radar chart visualization, so teams can quickly assess competitive threats and opportunities without coding. Drop-ready for decks or dashboards, it simplifies scenario comparisons (pre/post events or new entrants) and speeds strategic decision-making.

Customers Bargaining Power

Price-sensitive consumers

French grocery shoppers are highly price-focused, giving buyers strong leverage; discounters held about 25% of the market in 2024 and set reference prices that squeeze margins. Heavy promotional intensity—around 30% of transactions in 2024 involved discounts—has trained consumers to wait for deals. Loyalty schemes (Carrefour ~22 million cardholders in 2024) and private labels (≈40% penetration by units) help retain baskets despite price sensitivity.

Omnichannel transparency

Omnichannel transparency accelerates switching: global online retail reached about 23.5% of total retail sales in 2024 and 58% of consumers used price‑comparison tools, making price differences easy to find. Click‑and‑collect and delivery are table stakes, offered by roughly 70% of major retailers in 2024. High transparency compressed price dispersion, while delivery and service reliability—cited by 35% of shoppers as top loyalty drivers—become key differentiators.

Limited B2B share

Retail at Rallye is overwhelmingly B2C, which reduces bulk-buyer concentration risk; corporate catering and resellers account for a low single-digit share of volumes according to industry estimates. These niche accounts exert higher bargaining power per contract but are small in aggregate. Tailored pricing, minimum order sizes and service tiers can preserve margins while serving resellers profitably.

Low switching costs

Consumers can readily switch among banners, formats and channels, keeping bargaining power high; European e‑grocery penetration reached about 10% in 2024, raising channel fluidity. Proximity and convenience reduce but do not eliminate churn for urban shoppers. Deep assortments and unique private labels create soft lock‑in, while delivery subscriptions (global paid delivery memberships >200 million in 2024) add incremental stickiness.

- High channel fluidity

- Proximity moderates churn

- Private label = soft lock‑in

- Delivery subs increase retention

Quality and ESG expectations

Rising demand for organic, fair-trade and local origin lets buyers push Rallye to tailor assortments; in Western Europe organic penetration exceeded 6% of food retail in 2024, enabling customers to dictate ranges. Failure to meet ESG or quality standards risks basket shifts to competitors and discounters.

Premiumization can lift gross margins (organic/fair-trade price premiums often 20–40%) but narrows the addressable base; clear labeling and traceability are essential to sustain trust and avoid churn.

- Buyers: demand-driven assortment

- Risk: basket shifts if standards fail

- Opportunity: 20–40% premiums

- Mitigation: labeling & traceability

Discounters 25% share, online 23.5% sales boost switching

Buyers hold strong leverage: discounters 25% market share (2024), 30% of transactions promoted and Carrefour ~22M cardholders; private labels ≈40% unit penetration soften price pressure.

Omnichannel transparency (online retail 23.5% of retail sales 2024; 58% use price tools) and 10% e‑grocery penetration raise switching; delivery subs (>200M global) add retention.

Organic >6% penetration (2024) supports 20–40% premiums but raises churn risk if ESG/traceability fail.

| Metric | 2024 |

|---|---|

| Discounters share | 25% |

| Promoted txns | 30% |

| Carrefour cardholders | 22M |

| Private label units | ≈40% |

Same Document Delivered

Rallye Porter's Five Forces Analysis

This preview shows the exact Rallye Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The file is fully formatted, professionally written, and ready to download and use. What you see is the deliverable, available instantly after payment.

From Overview to Strategy Blueprint

Rallye’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, and competitive intensity shaping its retail-conglomerate position. It surfaces key threats from new entrants and substitutes and flags strategic levers to defend margins. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Fragmented FMCG base

Most food and CPG categories are sourced from a fragmented supplier base, limiting individual vendors' leverage against Casino’s scale, while centralized procurement and private labels materially enhance bargaining clout. Category captains in beverages, hygiene and baby care still retain pricing power and can push tougher terms. Rallye’s net influence hinges on Casino’s purchasing alliances and volume commitments.

Private label leverage

Casino’s private brands substitute for national brands, lowering dependence on powerful suppliers and shifting category leverage toward the retailer. Improved margin mix and deliberate dual-sourcing strengthen negotiating power with national suppliers. Sustained consumer trust depends on rigorous quality controls and reliable supply chains. Switching costs for packaging and specifications create moderate stickiness for suppliers and co-manufacturers.

Fresh and local producers

Fruits, vegetables and meats often come from regional suppliers with limited scale, giving episodic leverage due to seasonality and perishability; roughly one-third of produced food is lost or wasted globally, amplifying supply sensitivity. Casino’s integrated logistics, forecasting and cold-chain investments reduce this volatility and buffer buying power. Certification and sustainability demands further narrow supplier pools, increasing supplier bargaining in peak seasons.

Non-merch suppliers (rent, IT, logistics)

Landlords, payment providers and logistics/IT vendors exert leverage via contract lock-ins: multi-year store leases and DC commitments create switching frictions, tech-stack dependencies raise integration costs, and payment fees (typically 1–3% of transaction value) and logistics (often 5–10% of sales) inflate operating leverage; competitive bidding and shared services can rebalance terms.

- Lease lock-ins: multi-year commitments

- Payment fees: 1–3% of transactions

- Logistics/IT: ~5–10% of sales

- Mitigants: competitive bidding, shared services

Regulatory and ESG constraints

French fair-trading reforms (EGalim, 2018) and EU sustainability rules such as the Corporate Sustainability Reporting Directive, which extends reporting to roughly 50,000 companies from 2024, constrain Rallye’s procurement tactics by enforcing transparency and fair pricing with agricultural suppliers. ESG sourcing standards limit rapid supplier substitution, often narrowing choice and increasing input cost pressure for food retailers. Long-term supplier partnerships partially offset these constraints by securing volumes and shared-compliance investments.

- EGalim: strengthens farmer-retailer pricing rules in France

- CSRD ~50,000 companies from 2024: greater disclosure burden

- ESG sourcing: reduces substitution, can raise input costs

- Long-term contracts: mitigate supplier power, enable joint ESG investments

Fragmented suppliers vs centralized buyers: logistics, payments and ESG squeeze margins

Supplier power is limited by fragmented food/CPG supply and Casino’s centralized procurement and private-label leverage, though category captains (beverages, hygiene) retain pricing power. Landlords, payments and logistics exert measurable leverage (leases multi-year; payment fees 1–3%; logistics 5–10% of sales). Regulations (EGalim, CSRD ~50,000 firms from 2024) and ESG sourcing narrow supplier pools seasonally.

| Metric | Value | Implication |

|---|---|---|

| Payment fees | 1–3% | Operating cost pressure |

| Logistics | 5–10% of sales | Negotiation leverage |

| CSRD scope | ~50,000 firms (from 2024) | Greater disclosure, sourcing constraints |

| Food waste | ~33% | Supply sensitivity/seasonality |

What is included in the product

Tailored Porter’s Five Forces analysis for Rallye that pinpoints competitive intensity, supplier and buyer bargaining power, threat of entrants and substitutes, and identifies disruptive risks and strategic levers to protect market share and improve profitability.

Rallye Porter's Five Forces Analysis delivers a clean, one-sheet summary with adjustable pressure levels and an instant radar chart visualization, so teams can quickly assess competitive threats and opportunities without coding. Drop-ready for decks or dashboards, it simplifies scenario comparisons (pre/post events or new entrants) and speeds strategic decision-making.

Customers Bargaining Power

Price-sensitive consumers

French grocery shoppers are highly price-focused, giving buyers strong leverage; discounters held about 25% of the market in 2024 and set reference prices that squeeze margins. Heavy promotional intensity—around 30% of transactions in 2024 involved discounts—has trained consumers to wait for deals. Loyalty schemes (Carrefour ~22 million cardholders in 2024) and private labels (≈40% penetration by units) help retain baskets despite price sensitivity.

Omnichannel transparency

Omnichannel transparency accelerates switching: global online retail reached about 23.5% of total retail sales in 2024 and 58% of consumers used price‑comparison tools, making price differences easy to find. Click‑and‑collect and delivery are table stakes, offered by roughly 70% of major retailers in 2024. High transparency compressed price dispersion, while delivery and service reliability—cited by 35% of shoppers as top loyalty drivers—become key differentiators.

Limited B2B share

Retail at Rallye is overwhelmingly B2C, which reduces bulk-buyer concentration risk; corporate catering and resellers account for a low single-digit share of volumes according to industry estimates. These niche accounts exert higher bargaining power per contract but are small in aggregate. Tailored pricing, minimum order sizes and service tiers can preserve margins while serving resellers profitably.

Low switching costs

Consumers can readily switch among banners, formats and channels, keeping bargaining power high; European e‑grocery penetration reached about 10% in 2024, raising channel fluidity. Proximity and convenience reduce but do not eliminate churn for urban shoppers. Deep assortments and unique private labels create soft lock‑in, while delivery subscriptions (global paid delivery memberships >200 million in 2024) add incremental stickiness.

- High channel fluidity

- Proximity moderates churn

- Private label = soft lock‑in

- Delivery subs increase retention

Quality and ESG expectations

Rising demand for organic, fair-trade and local origin lets buyers push Rallye to tailor assortments; in Western Europe organic penetration exceeded 6% of food retail in 2024, enabling customers to dictate ranges. Failure to meet ESG or quality standards risks basket shifts to competitors and discounters.

Premiumization can lift gross margins (organic/fair-trade price premiums often 20–40%) but narrows the addressable base; clear labeling and traceability are essential to sustain trust and avoid churn.

- Buyers: demand-driven assortment

- Risk: basket shifts if standards fail

- Opportunity: 20–40% premiums

- Mitigation: labeling & traceability

Discounters 25% share, online 23.5% sales boost switching

Buyers hold strong leverage: discounters 25% market share (2024), 30% of transactions promoted and Carrefour ~22M cardholders; private labels ≈40% unit penetration soften price pressure.

Omnichannel transparency (online retail 23.5% of retail sales 2024; 58% use price tools) and 10% e‑grocery penetration raise switching; delivery subs (>200M global) add retention.

Organic >6% penetration (2024) supports 20–40% premiums but raises churn risk if ESG/traceability fail.

| Metric | 2024 |

|---|---|

| Discounters share | 25% |

| Promoted txns | 30% |

| Carrefour cardholders | 22M |

| Private label units | ≈40% |

Same Document Delivered

Rallye Porter's Five Forces Analysis

This preview shows the exact Rallye Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The file is fully formatted, professionally written, and ready to download and use. What you see is the deliverable, available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Rallye’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, and competitive intensity shaping its retail-conglomerate position. It surfaces key threats from new entrants and substitutes and flags strategic levers to defend margins. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Fragmented FMCG base

Most food and CPG categories are sourced from a fragmented supplier base, limiting individual vendors' leverage against Casino’s scale, while centralized procurement and private labels materially enhance bargaining clout. Category captains in beverages, hygiene and baby care still retain pricing power and can push tougher terms. Rallye’s net influence hinges on Casino’s purchasing alliances and volume commitments.

Private label leverage

Casino’s private brands substitute for national brands, lowering dependence on powerful suppliers and shifting category leverage toward the retailer. Improved margin mix and deliberate dual-sourcing strengthen negotiating power with national suppliers. Sustained consumer trust depends on rigorous quality controls and reliable supply chains. Switching costs for packaging and specifications create moderate stickiness for suppliers and co-manufacturers.

Fresh and local producers

Fruits, vegetables and meats often come from regional suppliers with limited scale, giving episodic leverage due to seasonality and perishability; roughly one-third of produced food is lost or wasted globally, amplifying supply sensitivity. Casino’s integrated logistics, forecasting and cold-chain investments reduce this volatility and buffer buying power. Certification and sustainability demands further narrow supplier pools, increasing supplier bargaining in peak seasons.

Non-merch suppliers (rent, IT, logistics)

Landlords, payment providers and logistics/IT vendors exert leverage via contract lock-ins: multi-year store leases and DC commitments create switching frictions, tech-stack dependencies raise integration costs, and payment fees (typically 1–3% of transaction value) and logistics (often 5–10% of sales) inflate operating leverage; competitive bidding and shared services can rebalance terms.

- Lease lock-ins: multi-year commitments

- Payment fees: 1–3% of transactions

- Logistics/IT: ~5–10% of sales

- Mitigants: competitive bidding, shared services

Regulatory and ESG constraints

French fair-trading reforms (EGalim, 2018) and EU sustainability rules such as the Corporate Sustainability Reporting Directive, which extends reporting to roughly 50,000 companies from 2024, constrain Rallye’s procurement tactics by enforcing transparency and fair pricing with agricultural suppliers. ESG sourcing standards limit rapid supplier substitution, often narrowing choice and increasing input cost pressure for food retailers. Long-term supplier partnerships partially offset these constraints by securing volumes and shared-compliance investments.

- EGalim: strengthens farmer-retailer pricing rules in France

- CSRD ~50,000 companies from 2024: greater disclosure burden

- ESG sourcing: reduces substitution, can raise input costs

- Long-term contracts: mitigate supplier power, enable joint ESG investments

Fragmented suppliers vs centralized buyers: logistics, payments and ESG squeeze margins

Supplier power is limited by fragmented food/CPG supply and Casino’s centralized procurement and private-label leverage, though category captains (beverages, hygiene) retain pricing power. Landlords, payments and logistics exert measurable leverage (leases multi-year; payment fees 1–3%; logistics 5–10% of sales). Regulations (EGalim, CSRD ~50,000 firms from 2024) and ESG sourcing narrow supplier pools seasonally.

| Metric | Value | Implication |

|---|---|---|

| Payment fees | 1–3% | Operating cost pressure |

| Logistics | 5–10% of sales | Negotiation leverage |

| CSRD scope | ~50,000 firms (from 2024) | Greater disclosure, sourcing constraints |

| Food waste | ~33% | Supply sensitivity/seasonality |

What is included in the product

Tailored Porter’s Five Forces analysis for Rallye that pinpoints competitive intensity, supplier and buyer bargaining power, threat of entrants and substitutes, and identifies disruptive risks and strategic levers to protect market share and improve profitability.

Rallye Porter's Five Forces Analysis delivers a clean, one-sheet summary with adjustable pressure levels and an instant radar chart visualization, so teams can quickly assess competitive threats and opportunities without coding. Drop-ready for decks or dashboards, it simplifies scenario comparisons (pre/post events or new entrants) and speeds strategic decision-making.

Customers Bargaining Power

Price-sensitive consumers

French grocery shoppers are highly price-focused, giving buyers strong leverage; discounters held about 25% of the market in 2024 and set reference prices that squeeze margins. Heavy promotional intensity—around 30% of transactions in 2024 involved discounts—has trained consumers to wait for deals. Loyalty schemes (Carrefour ~22 million cardholders in 2024) and private labels (≈40% penetration by units) help retain baskets despite price sensitivity.

Omnichannel transparency

Omnichannel transparency accelerates switching: global online retail reached about 23.5% of total retail sales in 2024 and 58% of consumers used price‑comparison tools, making price differences easy to find. Click‑and‑collect and delivery are table stakes, offered by roughly 70% of major retailers in 2024. High transparency compressed price dispersion, while delivery and service reliability—cited by 35% of shoppers as top loyalty drivers—become key differentiators.

Limited B2B share

Retail at Rallye is overwhelmingly B2C, which reduces bulk-buyer concentration risk; corporate catering and resellers account for a low single-digit share of volumes according to industry estimates. These niche accounts exert higher bargaining power per contract but are small in aggregate. Tailored pricing, minimum order sizes and service tiers can preserve margins while serving resellers profitably.

Low switching costs

Consumers can readily switch among banners, formats and channels, keeping bargaining power high; European e‑grocery penetration reached about 10% in 2024, raising channel fluidity. Proximity and convenience reduce but do not eliminate churn for urban shoppers. Deep assortments and unique private labels create soft lock‑in, while delivery subscriptions (global paid delivery memberships >200 million in 2024) add incremental stickiness.

- High channel fluidity

- Proximity moderates churn

- Private label = soft lock‑in

- Delivery subs increase retention

Quality and ESG expectations

Rising demand for organic, fair-trade and local origin lets buyers push Rallye to tailor assortments; in Western Europe organic penetration exceeded 6% of food retail in 2024, enabling customers to dictate ranges. Failure to meet ESG or quality standards risks basket shifts to competitors and discounters.

Premiumization can lift gross margins (organic/fair-trade price premiums often 20–40%) but narrows the addressable base; clear labeling and traceability are essential to sustain trust and avoid churn.

- Buyers: demand-driven assortment

- Risk: basket shifts if standards fail

- Opportunity: 20–40% premiums

- Mitigation: labeling & traceability

Discounters 25% share, online 23.5% sales boost switching

Buyers hold strong leverage: discounters 25% market share (2024), 30% of transactions promoted and Carrefour ~22M cardholders; private labels ≈40% unit penetration soften price pressure.

Omnichannel transparency (online retail 23.5% of retail sales 2024; 58% use price tools) and 10% e‑grocery penetration raise switching; delivery subs (>200M global) add retention.

Organic >6% penetration (2024) supports 20–40% premiums but raises churn risk if ESG/traceability fail.

| Metric | 2024 |

|---|---|

| Discounters share | 25% |

| Promoted txns | 30% |

| Carrefour cardholders | 22M |

| Private label units | ≈40% |

Same Document Delivered

Rallye Porter's Five Forces Analysis

This preview shows the exact Rallye Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders. The file is fully formatted, professionally written, and ready to download and use. What you see is the deliverable, available instantly after payment.