Ramsay Health Care Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

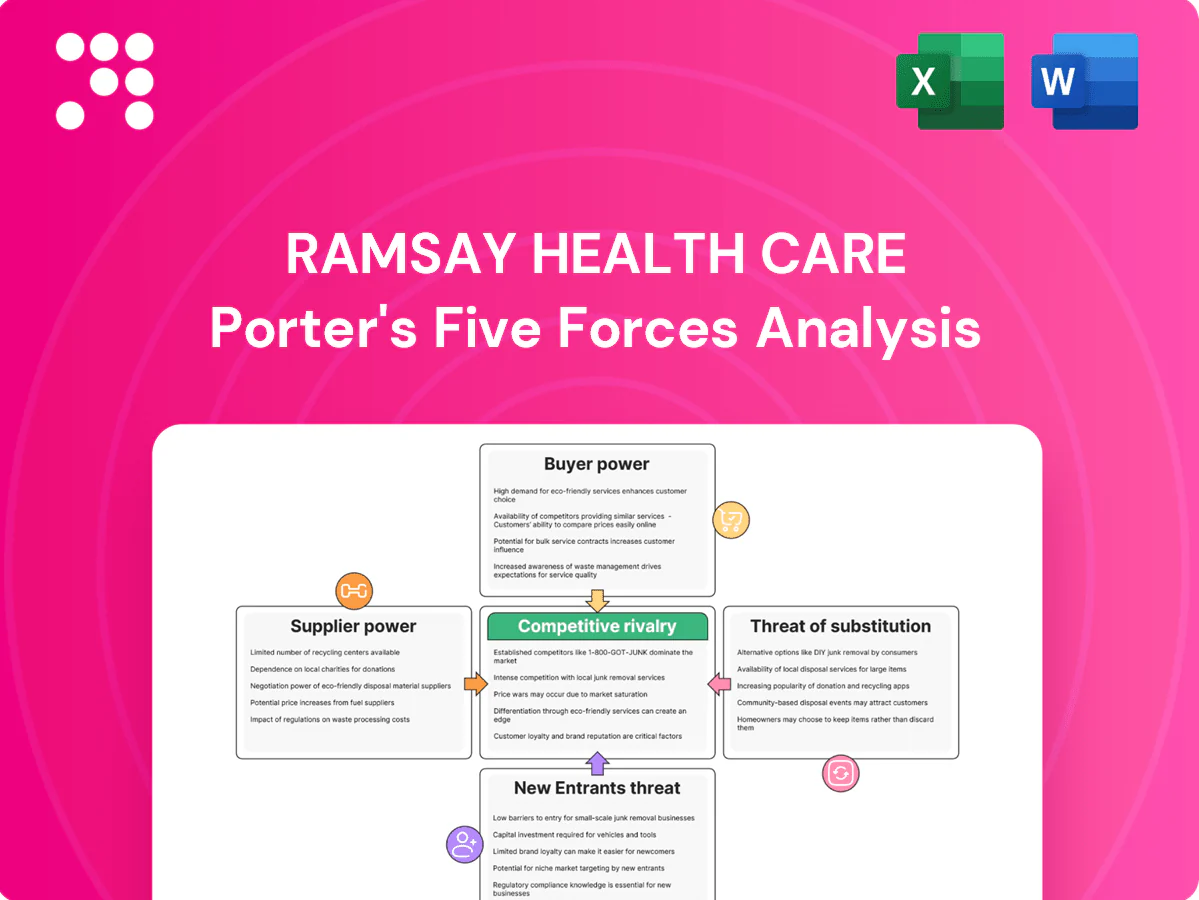

Ramsay Health Care's Porter's Five Forces analysis highlights strong buyer power, moderate supplier influence, and high rivalry driven by consolidation and regulatory pressures, while barriers to entry and substitute threats remain mixed; these dynamics shape margins and growth outlook. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ramsay Health Care’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Supplier Power 1

Medical device and pharma vendors exert moderate power over Ramsay Health Care: product differentiation and regulation make switching critical implants, biologics and imaging platforms costly and risky, potentially disrupting care. Long-term supply contracts mitigate price pressure but lock in technology standards. Ramsay’s global sourcing and scale across over 480 facilities in 11 countries and FY2024 revenue above AUD12bn reduce single-vendor leverage.

Supplier Power 2

Specialist clinicians are pivotal suppliers with high scarcity in key disciplines; credentialed surgeons and psychiatrists can shift cases to competing facilities, elevating their bargaining power. Ramsay in 2024 must offer attractive theatres, dedicated support staff and competitive revenue-sharing to retain them. Ongoing 2024 workforce shortages amplify wage inflation and roster pressure across hospitals.

Supplier Power 3

IT and digital infrastructure vendors create high switching frictions for Ramsay as EHRs, imaging PACS and cybersecurity platforms require deep integration and staff training. Vendor lock-in and certification requirements raise supplier power by increasing migration costs and regulatory hurdles. Ramsay’s scale—about 480 facilities globally in 2024—enables negotiation of enterprise licences and stronger interoperability clauses.

Supplier Power 4

Supplier Power 4: Utilities, facilities and consumables suppliers exert low-to-moderate power for Ramsay Health Care given commoditised lines are contestable via tenders and group purchasing; Ramsay operates ~480 hospitals and clinics (2024), enabling scale. Critical sterile supplies, medical oxygen and reliable energy force dual-sourcing and stock buffers, and inflation/supply-chain shocks can transiently raise supplier leverage.

- Commoditised supplies: tenderable

- Scale: ~480 facilities (2024)

- Critical inputs: dual-sourcing essential

- Risk: inflation & disruptions raise short-term leverage

Supplier Power 5

Regulators act as non-traditional suppliers by controlling licenses and approvals, with accreditation (eg NSQHS) dictating equipment, staffing ratios and processes, raising compliance costs that limit substitution and boost supplier power. Ramsay operates in 11 countries with ~500 facilities, and its strong compliance track record reduces approval risk over time.

- Regulatory approvals drive capital and OPEX

- Accreditation enforces staffing/equipment standards

- Compliance costs increase switching barriers

- Ramsay scale and track record lower approval risk

Supplier leverage grows despite scale: ≈480 sites, AUD12.3bn

Medical vendors, specialist clinicians and IT suppliers exert moderate-to-high power over Ramsay due to product differentiation, credential scarcity and integration lock-in; long-term contracts and scale (≈480 facilities across 11 countries; FY2024 revenue AUD12.3bn) mitigate but don’t eliminate leverage. Commoditised consumables and utilities show low power, regulators raise switching costs.

| Metric | 2024 |

|---|---|

| Facilities | ≈480 |

| Countries | 11 |

| Revenue | AUD12.3bn |

What is included in the product

Tailored Porter's Five Forces analysis for Ramsay Health Care, uncovering competitive drivers, supplier and buyer influence, entry barriers, substitutes and emerging threats to market share.

A clear, one-sheet Porter's Five Forces summary for Ramsay Health Care—instantly highlight competitive pressures and pain points to speed strategic decisions and boardroom action.

Customers Bargaining Power

Buyer Power 1

Private insurers exert high power via network design and tariff negotiations, steering patient volumes through prior authorizations and differential co-pays. Multi-year contracts trade price for guaranteed volume and quality metrics. Ramsay’s ~480 facilities across 11 countries in 2024 strengthen its negotiating stance by offering scale and geographic coverage.

Buyer Power 2

Public payers and procurement agencies materially influence Ramsay Health Care pricing where contracts exist, with fixed DRG-style rates and competitive tenders compressing margins. Political scrutiny in key markets increases requirements for transparency and outcome reporting. Diversification across 11 countries and around 500 facilities helps balance payer-concentration risk.

Buyer Power 3

Self-pay patients show moderate price and experience sensitivity, comparing wait times, surgeon reputation and amenities; Ramsay operates over 480 hospitals across 11 countries, enhancing brand-driven retention. Bundled pricing and financing options reduce perceived cost and accelerate elective uptake. Strong clinical outcomes and brand recognition lower switching and support pricing power.

Buyer Power 4

Corporate and workers’ comp buyers negotiate preferential rates and demand fast access, predictable costs and return-to-work outcomes; in FY2024 Ramsay reported A$13.6bn revenue and leverages scale to meet volume contracts. Ramsay differentiates via standardized care pathways and case management, improving RTT and reducing length of stay. Contracted volumes across 480+ facilities partially offset pricing pressure and stabilize margins.

- Buyers: corporate/workers comp

- Needs: fast access, predictable cost, RTW

- Ramsay levers: care pathways, case management

- Scale: 480+ facilities; FY2024 revenue A$13.6bn

Buyer Power 5

Referring physicians and GPs are major intermediaries for Ramsay, shaping demand for elective procedures and directing patients to facilities; in Australia in 2024 GP/referrer pathways accounted for about 70% of private elective admissions. Preferences on outreach, theatre availability and patient feedback drive facility choice and sustain referral flows, while weak referral relationships raise buyer power through referral leakage.

High payer leverage drives pricing; referrals and scale limit buyer power

Private insurers and public payers exert high pricing leverage via networks, DRG rates and tenders; multi-year contracts trade price for volume. Corporate and self-pay segments show moderate negotiating power; referrals (≈70% Australian elective admissions) and Ramsay scale (~480 facilities, 11 countries; FY2024 revenue A$13.6bn) mitigate buyer power.

| Buyer | Influence | Metric |

|---|---|---|

| Private insurers | High | Network/tariff negotiation |

| Public payers | High | DRG/tenders |

| Referrals | Moderate | ≈70% AU elective |

| Corporate/self-pay | Moderate | Price/RTW demands |

Preview Before You Purchase

Ramsay Health Care Porter's Five Forces Analysis

This preview is the exact Ramsay Health Care Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. It's the final, fully formatted document covering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants. Purchase grants instant access to this same downloadable file, ready for immediate use.

Go Beyond the Preview—Access the Full Strategic Report

Ramsay Health Care's Porter's Five Forces analysis highlights strong buyer power, moderate supplier influence, and high rivalry driven by consolidation and regulatory pressures, while barriers to entry and substitute threats remain mixed; these dynamics shape margins and growth outlook. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ramsay Health Care’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Supplier Power 1

Medical device and pharma vendors exert moderate power over Ramsay Health Care: product differentiation and regulation make switching critical implants, biologics and imaging platforms costly and risky, potentially disrupting care. Long-term supply contracts mitigate price pressure but lock in technology standards. Ramsay’s global sourcing and scale across over 480 facilities in 11 countries and FY2024 revenue above AUD12bn reduce single-vendor leverage.

Supplier Power 2

Specialist clinicians are pivotal suppliers with high scarcity in key disciplines; credentialed surgeons and psychiatrists can shift cases to competing facilities, elevating their bargaining power. Ramsay in 2024 must offer attractive theatres, dedicated support staff and competitive revenue-sharing to retain them. Ongoing 2024 workforce shortages amplify wage inflation and roster pressure across hospitals.

Supplier Power 3

IT and digital infrastructure vendors create high switching frictions for Ramsay as EHRs, imaging PACS and cybersecurity platforms require deep integration and staff training. Vendor lock-in and certification requirements raise supplier power by increasing migration costs and regulatory hurdles. Ramsay’s scale—about 480 facilities globally in 2024—enables negotiation of enterprise licences and stronger interoperability clauses.

Supplier Power 4

Supplier Power 4: Utilities, facilities and consumables suppliers exert low-to-moderate power for Ramsay Health Care given commoditised lines are contestable via tenders and group purchasing; Ramsay operates ~480 hospitals and clinics (2024), enabling scale. Critical sterile supplies, medical oxygen and reliable energy force dual-sourcing and stock buffers, and inflation/supply-chain shocks can transiently raise supplier leverage.

- Commoditised supplies: tenderable

- Scale: ~480 facilities (2024)

- Critical inputs: dual-sourcing essential

- Risk: inflation & disruptions raise short-term leverage

Supplier Power 5

Regulators act as non-traditional suppliers by controlling licenses and approvals, with accreditation (eg NSQHS) dictating equipment, staffing ratios and processes, raising compliance costs that limit substitution and boost supplier power. Ramsay operates in 11 countries with ~500 facilities, and its strong compliance track record reduces approval risk over time.

- Regulatory approvals drive capital and OPEX

- Accreditation enforces staffing/equipment standards

- Compliance costs increase switching barriers

- Ramsay scale and track record lower approval risk

Supplier leverage grows despite scale: ≈480 sites, AUD12.3bn

Medical vendors, specialist clinicians and IT suppliers exert moderate-to-high power over Ramsay due to product differentiation, credential scarcity and integration lock-in; long-term contracts and scale (≈480 facilities across 11 countries; FY2024 revenue AUD12.3bn) mitigate but don’t eliminate leverage. Commoditised consumables and utilities show low power, regulators raise switching costs.

| Metric | 2024 |

|---|---|

| Facilities | ≈480 |

| Countries | 11 |

| Revenue | AUD12.3bn |

What is included in the product

Tailored Porter's Five Forces analysis for Ramsay Health Care, uncovering competitive drivers, supplier and buyer influence, entry barriers, substitutes and emerging threats to market share.

A clear, one-sheet Porter's Five Forces summary for Ramsay Health Care—instantly highlight competitive pressures and pain points to speed strategic decisions and boardroom action.

Customers Bargaining Power

Buyer Power 1

Private insurers exert high power via network design and tariff negotiations, steering patient volumes through prior authorizations and differential co-pays. Multi-year contracts trade price for guaranteed volume and quality metrics. Ramsay’s ~480 facilities across 11 countries in 2024 strengthen its negotiating stance by offering scale and geographic coverage.

Buyer Power 2

Public payers and procurement agencies materially influence Ramsay Health Care pricing where contracts exist, with fixed DRG-style rates and competitive tenders compressing margins. Political scrutiny in key markets increases requirements for transparency and outcome reporting. Diversification across 11 countries and around 500 facilities helps balance payer-concentration risk.

Buyer Power 3

Self-pay patients show moderate price and experience sensitivity, comparing wait times, surgeon reputation and amenities; Ramsay operates over 480 hospitals across 11 countries, enhancing brand-driven retention. Bundled pricing and financing options reduce perceived cost and accelerate elective uptake. Strong clinical outcomes and brand recognition lower switching and support pricing power.

Buyer Power 4

Corporate and workers’ comp buyers negotiate preferential rates and demand fast access, predictable costs and return-to-work outcomes; in FY2024 Ramsay reported A$13.6bn revenue and leverages scale to meet volume contracts. Ramsay differentiates via standardized care pathways and case management, improving RTT and reducing length of stay. Contracted volumes across 480+ facilities partially offset pricing pressure and stabilize margins.

- Buyers: corporate/workers comp

- Needs: fast access, predictable cost, RTW

- Ramsay levers: care pathways, case management

- Scale: 480+ facilities; FY2024 revenue A$13.6bn

Buyer Power 5

Referring physicians and GPs are major intermediaries for Ramsay, shaping demand for elective procedures and directing patients to facilities; in Australia in 2024 GP/referrer pathways accounted for about 70% of private elective admissions. Preferences on outreach, theatre availability and patient feedback drive facility choice and sustain referral flows, while weak referral relationships raise buyer power through referral leakage.

High payer leverage drives pricing; referrals and scale limit buyer power

Private insurers and public payers exert high pricing leverage via networks, DRG rates and tenders; multi-year contracts trade price for volume. Corporate and self-pay segments show moderate negotiating power; referrals (≈70% Australian elective admissions) and Ramsay scale (~480 facilities, 11 countries; FY2024 revenue A$13.6bn) mitigate buyer power.

| Buyer | Influence | Metric |

|---|---|---|

| Private insurers | High | Network/tariff negotiation |

| Public payers | High | DRG/tenders |

| Referrals | Moderate | ≈70% AU elective |

| Corporate/self-pay | Moderate | Price/RTW demands |

Preview Before You Purchase

Ramsay Health Care Porter's Five Forces Analysis

This preview is the exact Ramsay Health Care Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. It's the final, fully formatted document covering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants. Purchase grants instant access to this same downloadable file, ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Ramsay Health Care's Porter's Five Forces analysis highlights strong buyer power, moderate supplier influence, and high rivalry driven by consolidation and regulatory pressures, while barriers to entry and substitute threats remain mixed; these dynamics shape margins and growth outlook. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ramsay Health Care’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Supplier Power 1

Medical device and pharma vendors exert moderate power over Ramsay Health Care: product differentiation and regulation make switching critical implants, biologics and imaging platforms costly and risky, potentially disrupting care. Long-term supply contracts mitigate price pressure but lock in technology standards. Ramsay’s global sourcing and scale across over 480 facilities in 11 countries and FY2024 revenue above AUD12bn reduce single-vendor leverage.

Supplier Power 2

Specialist clinicians are pivotal suppliers with high scarcity in key disciplines; credentialed surgeons and psychiatrists can shift cases to competing facilities, elevating their bargaining power. Ramsay in 2024 must offer attractive theatres, dedicated support staff and competitive revenue-sharing to retain them. Ongoing 2024 workforce shortages amplify wage inflation and roster pressure across hospitals.

Supplier Power 3

IT and digital infrastructure vendors create high switching frictions for Ramsay as EHRs, imaging PACS and cybersecurity platforms require deep integration and staff training. Vendor lock-in and certification requirements raise supplier power by increasing migration costs and regulatory hurdles. Ramsay’s scale—about 480 facilities globally in 2024—enables negotiation of enterprise licences and stronger interoperability clauses.

Supplier Power 4

Supplier Power 4: Utilities, facilities and consumables suppliers exert low-to-moderate power for Ramsay Health Care given commoditised lines are contestable via tenders and group purchasing; Ramsay operates ~480 hospitals and clinics (2024), enabling scale. Critical sterile supplies, medical oxygen and reliable energy force dual-sourcing and stock buffers, and inflation/supply-chain shocks can transiently raise supplier leverage.

- Commoditised supplies: tenderable

- Scale: ~480 facilities (2024)

- Critical inputs: dual-sourcing essential

- Risk: inflation & disruptions raise short-term leverage

Supplier Power 5

Regulators act as non-traditional suppliers by controlling licenses and approvals, with accreditation (eg NSQHS) dictating equipment, staffing ratios and processes, raising compliance costs that limit substitution and boost supplier power. Ramsay operates in 11 countries with ~500 facilities, and its strong compliance track record reduces approval risk over time.

- Regulatory approvals drive capital and OPEX

- Accreditation enforces staffing/equipment standards

- Compliance costs increase switching barriers

- Ramsay scale and track record lower approval risk

Supplier leverage grows despite scale: ≈480 sites, AUD12.3bn

Medical vendors, specialist clinicians and IT suppliers exert moderate-to-high power over Ramsay due to product differentiation, credential scarcity and integration lock-in; long-term contracts and scale (≈480 facilities across 11 countries; FY2024 revenue AUD12.3bn) mitigate but don’t eliminate leverage. Commoditised consumables and utilities show low power, regulators raise switching costs.

| Metric | 2024 |

|---|---|

| Facilities | ≈480 |

| Countries | 11 |

| Revenue | AUD12.3bn |

What is included in the product

Tailored Porter's Five Forces analysis for Ramsay Health Care, uncovering competitive drivers, supplier and buyer influence, entry barriers, substitutes and emerging threats to market share.

A clear, one-sheet Porter's Five Forces summary for Ramsay Health Care—instantly highlight competitive pressures and pain points to speed strategic decisions and boardroom action.

Customers Bargaining Power

Buyer Power 1

Private insurers exert high power via network design and tariff negotiations, steering patient volumes through prior authorizations and differential co-pays. Multi-year contracts trade price for guaranteed volume and quality metrics. Ramsay’s ~480 facilities across 11 countries in 2024 strengthen its negotiating stance by offering scale and geographic coverage.

Buyer Power 2

Public payers and procurement agencies materially influence Ramsay Health Care pricing where contracts exist, with fixed DRG-style rates and competitive tenders compressing margins. Political scrutiny in key markets increases requirements for transparency and outcome reporting. Diversification across 11 countries and around 500 facilities helps balance payer-concentration risk.

Buyer Power 3

Self-pay patients show moderate price and experience sensitivity, comparing wait times, surgeon reputation and amenities; Ramsay operates over 480 hospitals across 11 countries, enhancing brand-driven retention. Bundled pricing and financing options reduce perceived cost and accelerate elective uptake. Strong clinical outcomes and brand recognition lower switching and support pricing power.

Buyer Power 4

Corporate and workers’ comp buyers negotiate preferential rates and demand fast access, predictable costs and return-to-work outcomes; in FY2024 Ramsay reported A$13.6bn revenue and leverages scale to meet volume contracts. Ramsay differentiates via standardized care pathways and case management, improving RTT and reducing length of stay. Contracted volumes across 480+ facilities partially offset pricing pressure and stabilize margins.

- Buyers: corporate/workers comp

- Needs: fast access, predictable cost, RTW

- Ramsay levers: care pathways, case management

- Scale: 480+ facilities; FY2024 revenue A$13.6bn

Buyer Power 5

Referring physicians and GPs are major intermediaries for Ramsay, shaping demand for elective procedures and directing patients to facilities; in Australia in 2024 GP/referrer pathways accounted for about 70% of private elective admissions. Preferences on outreach, theatre availability and patient feedback drive facility choice and sustain referral flows, while weak referral relationships raise buyer power through referral leakage.

High payer leverage drives pricing; referrals and scale limit buyer power

Private insurers and public payers exert high pricing leverage via networks, DRG rates and tenders; multi-year contracts trade price for volume. Corporate and self-pay segments show moderate negotiating power; referrals (≈70% Australian elective admissions) and Ramsay scale (~480 facilities, 11 countries; FY2024 revenue A$13.6bn) mitigate buyer power.

| Buyer | Influence | Metric |

|---|---|---|

| Private insurers | High | Network/tariff negotiation |

| Public payers | High | DRG/tenders |

| Referrals | Moderate | ≈70% AU elective |

| Corporate/self-pay | Moderate | Price/RTW demands |

Preview Before You Purchase

Ramsay Health Care Porter's Five Forces Analysis

This preview is the exact Ramsay Health Care Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples. It's the final, fully formatted document covering competitive rivalry, supplier and buyer power, threat of substitutes and new entrants. Purchase grants instant access to this same downloadable file, ready for immediate use.