RAND Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

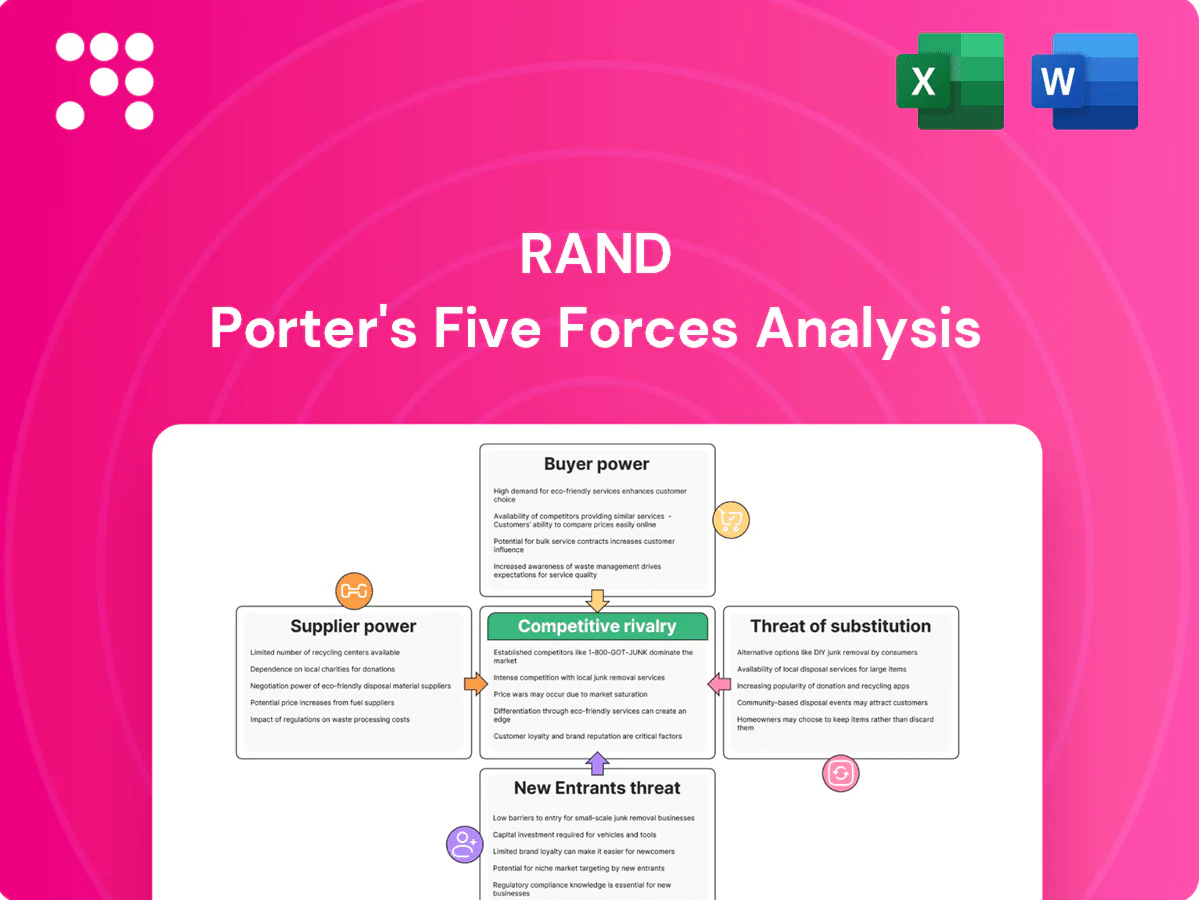

RAND’s Porter's Five Forces distills competitive pressure across suppliers, buyers, entrants, substitutes, and rivalry to reveal where strategic risks and advantages lie. This brief snapshot highlights key dynamics but leaves force-by-force ratings, visuals, and actionable implications unexplored. Unlock the full analysis for a consultant-grade, data-driven breakdown to inform investment and strategic decisions.

Suppliers Bargaining Power

Specialized talent

RAND depends on PhD-level researchers and cleared subject-matter experts drawn from a US annual pool of about 55,703 research doctorates (NCSES 2022); this scarcity lifts wage expectations and raises switching costs. RAND employs roughly 1,800 staff worldwide, but its mission, reputation and intrinsic-motivation appeal temper supplier power. Long tenures and internal development reduce volatility.

Proprietary data

In 2024, access to restricted government datasets and licensed private data remained key bottlenecks for RAND-style analytics, with many projects delaying timelines for permissions.

Exclusive or hard-to-replicate datasets gave suppliers meaningful leverage on price and terms, often commanding premiums above 30% in licensing deals.

Multi-source strategies, open-data alternatives and negotiated data-use agreements or long-term partnerships reduced dependence and stabilized access.

Field access

Survey panels, clinical sites, and operational theaters depend on gatekeepers who set conditions, timelines, and fees, and as of 2024 these intermediaries remain primary chokepoints for field access. RAND mitigates supplier power by cultivating diverse site networks and maintaining IRB standards that attract participation. Maintaining redundant site options reduces single-point exposure and activation risk.

Tech stack

Cloud platforms, secure enclaves and niche software vendors create significant switching costs; security and compliance needs further amplify vendor lock-in. In 2024, 92% of enterprises report multi-cloud use and 87% run Kubernetes in production, prompting RAND to use multi-cloud, open-source and containerization for portability. Volume pricing and consortia buying can cut procurement costs by ~15%.

- suppliers: hyperscalers, enclave vendors

- lock-in drivers: security, compliance

- mitigation: multi-cloud, OSS, containers

- 2024 stats: 92% multi-cloud, 87% k8s

- cost leverage: ~15% via consortia

Subcontractors

Subcontractors supply niche local expertise and surge capacity, with 2024 industry surveys showing regional partners staffed 30–35% of major infrastructure project hours; specialized firms raised rates about 15–20% during 2023–24 demand spikes, increasing supplier leverage. Long-term framework agreements and prequalified benches cut price volatility and lead times, while knowledge-transfer clauses reduce dependency over 2–4 years.

- Supplier share: 30–35%

- Price spike: 15–20%

- Dependency horizon: 2–4 years

- Mitigants: frameworks, prequalification, transfer clauses

PhD shortage (55,703) lifts licensing premiums >30%; multi-cloud cuts ~15%

RAND depends on scarce PhD talent (55,703 US research doctorates, NCSES 2022), raising wage and switching costs; exclusive datasets and gatekeepers command premiums >30% and delay timelines. Multi-cloud (92%) and Kubernetes (87%) trends push RAND to multi-cloud/OSS to cut procurement ~15%. Subcontractors supply 30–35% of hours with 15–20% rate spikes, mitigated by frameworks and knowledge-transfer.

| Metric | Value |

|---|---|

| US research doctorates | 55,703 (NCSES 2022) |

| Licensing premium | >30% |

| Multi-cloud | 92% (2024) |

| Kubernetes | 87% (2024) |

| Consortia savings | ~15% |

| Subcontractor share | 30–35% |

| Subcontractor rate spike | 15–20% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to RAND, with detailed evaluation of supplier and buyer power, substitutes, and disruptive threats. Fully editable Word format—ready for inclusion in investor materials, strategy decks, or academic projects.

A concise RAND Porter's Five Forces one-sheet with adjustable pressure sliders and an instant radar chart—clean, no-macro layout that’s ready for pitch decks, dashboards, and quick scenario updates as market conditions evolve.

Customers Bargaining Power

Government sponsors

Federal, state and defense agencies control large budgets—federal contracting exceeds $700B annually and the FY2024 DoD budget was about $858B—giving buyers strong leverage. RFPs, fixed-fee awards and audit rights constrain margins and shift risk. Past-performance scoring forces aggressive pricing and on-time delivery. Multi-year IDIQs provide stability but intensify competition over terms.

Foundations/NGOs

Philanthropic funders shape research agendas through thematic grants and milestone-driven contracts; Giving USA 2024 reports US charitable giving at $499.3B in 2023, concentrating leverage in large donors who often push for lower overhead and faster timelines. RAND’s long-standing credibility and measurable impact mitigate pricing pressure, while broad portfolio diversification reduces dependence on any single donor.

International bodies

As of 2024, multilaterals enforce stringent compliance and public disclosure regimes that compress negotiation levers around pricing and scope. Currency, jurisdiction, and political risk add contractual complexity that sophisticated buyers exploit in negotiation and payment terms. RAND’s global experience improves bid win rates but does not translate into greater fee flexibility. Consortium bids in multilateral tenders slightly dilute individual buyer leverage.

Outcome accountability

Buyers demand actionable, measurable policy impact and in 2024 roughly 40% of major grants incorporate performance-linked payments, increasing buyer leverage. Performance-linked payments and deliverable gates strengthen buyer hand, but RAND counters with clear methodologies, staged deliverables and rigorous baselines. Transparent impact evaluation and documented outcomes boost repeat business and reduce pure price competition.

- Performance mandates: ~40% of grants in 2024

- Risk shift: more payments tied to delivery gates

- RAND defense: staged deliverables + clear methodology

- Outcome proof: repeat business lowers price pressure

Information symmetry

Buyers increasingly deploy internal analytics and open data; by 2024 over 50% of enterprises maintain analytics teams, strengthening BATNA to insource or rebid. RAND differentiates through independence, cross-domain breadth and methodological rigor, reducing client capture risk. Co-creation models preserve value while allocating ownership and limiting commoditization.

- 2024: >50% enterprises with analytics

- RAND: independence + breadth + rigor

- Co-creation: shared ownership, protected margin

>700B buyers, 499B donors; ~40% grants pay

Large public buyers (US federal procurement >700B, DoD FY2024 ~858B) and major donors (US giving $499.3B in 2023) exert strong price and scope leverage; ~40% of major grants tie payments to performance. Over 50% of enterprises have analytics teams, raising insourcing BATNA. RAND’s credibility, diversified portfolio and staged deliverables mitigate but do not eliminate buyer pressure.

| Buyer | 2023/24 |

|---|---|

| US federal procurement | >700B |

| DoD budget FY2024 | ~858B |

| US charitable giving 2023 | 499.3B |

| Grants performance-linked | ~40% |

| Enterprises with analytics | >50% |

Same Document Delivered

RAND Porter's Five Forces Analysis

This preview shows the exact RAND Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is the complete, professionally formatted analysis, ready for download and use the moment you buy. You’ll get instant access to this identical file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

RAND’s Porter's Five Forces distills competitive pressure across suppliers, buyers, entrants, substitutes, and rivalry to reveal where strategic risks and advantages lie. This brief snapshot highlights key dynamics but leaves force-by-force ratings, visuals, and actionable implications unexplored. Unlock the full analysis for a consultant-grade, data-driven breakdown to inform investment and strategic decisions.

Suppliers Bargaining Power

Specialized talent

RAND depends on PhD-level researchers and cleared subject-matter experts drawn from a US annual pool of about 55,703 research doctorates (NCSES 2022); this scarcity lifts wage expectations and raises switching costs. RAND employs roughly 1,800 staff worldwide, but its mission, reputation and intrinsic-motivation appeal temper supplier power. Long tenures and internal development reduce volatility.

Proprietary data

In 2024, access to restricted government datasets and licensed private data remained key bottlenecks for RAND-style analytics, with many projects delaying timelines for permissions.

Exclusive or hard-to-replicate datasets gave suppliers meaningful leverage on price and terms, often commanding premiums above 30% in licensing deals.

Multi-source strategies, open-data alternatives and negotiated data-use agreements or long-term partnerships reduced dependence and stabilized access.

Field access

Survey panels, clinical sites, and operational theaters depend on gatekeepers who set conditions, timelines, and fees, and as of 2024 these intermediaries remain primary chokepoints for field access. RAND mitigates supplier power by cultivating diverse site networks and maintaining IRB standards that attract participation. Maintaining redundant site options reduces single-point exposure and activation risk.

Tech stack

Cloud platforms, secure enclaves and niche software vendors create significant switching costs; security and compliance needs further amplify vendor lock-in. In 2024, 92% of enterprises report multi-cloud use and 87% run Kubernetes in production, prompting RAND to use multi-cloud, open-source and containerization for portability. Volume pricing and consortia buying can cut procurement costs by ~15%.

- suppliers: hyperscalers, enclave vendors

- lock-in drivers: security, compliance

- mitigation: multi-cloud, OSS, containers

- 2024 stats: 92% multi-cloud, 87% k8s

- cost leverage: ~15% via consortia

Subcontractors

Subcontractors supply niche local expertise and surge capacity, with 2024 industry surveys showing regional partners staffed 30–35% of major infrastructure project hours; specialized firms raised rates about 15–20% during 2023–24 demand spikes, increasing supplier leverage. Long-term framework agreements and prequalified benches cut price volatility and lead times, while knowledge-transfer clauses reduce dependency over 2–4 years.

- Supplier share: 30–35%

- Price spike: 15–20%

- Dependency horizon: 2–4 years

- Mitigants: frameworks, prequalification, transfer clauses

PhD shortage (55,703) lifts licensing premiums >30%; multi-cloud cuts ~15%

RAND depends on scarce PhD talent (55,703 US research doctorates, NCSES 2022), raising wage and switching costs; exclusive datasets and gatekeepers command premiums >30% and delay timelines. Multi-cloud (92%) and Kubernetes (87%) trends push RAND to multi-cloud/OSS to cut procurement ~15%. Subcontractors supply 30–35% of hours with 15–20% rate spikes, mitigated by frameworks and knowledge-transfer.

| Metric | Value |

|---|---|

| US research doctorates | 55,703 (NCSES 2022) |

| Licensing premium | >30% |

| Multi-cloud | 92% (2024) |

| Kubernetes | 87% (2024) |

| Consortia savings | ~15% |

| Subcontractor share | 30–35% |

| Subcontractor rate spike | 15–20% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to RAND, with detailed evaluation of supplier and buyer power, substitutes, and disruptive threats. Fully editable Word format—ready for inclusion in investor materials, strategy decks, or academic projects.

A concise RAND Porter's Five Forces one-sheet with adjustable pressure sliders and an instant radar chart—clean, no-macro layout that’s ready for pitch decks, dashboards, and quick scenario updates as market conditions evolve.

Customers Bargaining Power

Government sponsors

Federal, state and defense agencies control large budgets—federal contracting exceeds $700B annually and the FY2024 DoD budget was about $858B—giving buyers strong leverage. RFPs, fixed-fee awards and audit rights constrain margins and shift risk. Past-performance scoring forces aggressive pricing and on-time delivery. Multi-year IDIQs provide stability but intensify competition over terms.

Foundations/NGOs

Philanthropic funders shape research agendas through thematic grants and milestone-driven contracts; Giving USA 2024 reports US charitable giving at $499.3B in 2023, concentrating leverage in large donors who often push for lower overhead and faster timelines. RAND’s long-standing credibility and measurable impact mitigate pricing pressure, while broad portfolio diversification reduces dependence on any single donor.

International bodies

As of 2024, multilaterals enforce stringent compliance and public disclosure regimes that compress negotiation levers around pricing and scope. Currency, jurisdiction, and political risk add contractual complexity that sophisticated buyers exploit in negotiation and payment terms. RAND’s global experience improves bid win rates but does not translate into greater fee flexibility. Consortium bids in multilateral tenders slightly dilute individual buyer leverage.

Outcome accountability

Buyers demand actionable, measurable policy impact and in 2024 roughly 40% of major grants incorporate performance-linked payments, increasing buyer leverage. Performance-linked payments and deliverable gates strengthen buyer hand, but RAND counters with clear methodologies, staged deliverables and rigorous baselines. Transparent impact evaluation and documented outcomes boost repeat business and reduce pure price competition.

- Performance mandates: ~40% of grants in 2024

- Risk shift: more payments tied to delivery gates

- RAND defense: staged deliverables + clear methodology

- Outcome proof: repeat business lowers price pressure

Information symmetry

Buyers increasingly deploy internal analytics and open data; by 2024 over 50% of enterprises maintain analytics teams, strengthening BATNA to insource or rebid. RAND differentiates through independence, cross-domain breadth and methodological rigor, reducing client capture risk. Co-creation models preserve value while allocating ownership and limiting commoditization.

- 2024: >50% enterprises with analytics

- RAND: independence + breadth + rigor

- Co-creation: shared ownership, protected margin

>700B buyers, 499B donors; ~40% grants pay

Large public buyers (US federal procurement >700B, DoD FY2024 ~858B) and major donors (US giving $499.3B in 2023) exert strong price and scope leverage; ~40% of major grants tie payments to performance. Over 50% of enterprises have analytics teams, raising insourcing BATNA. RAND’s credibility, diversified portfolio and staged deliverables mitigate but do not eliminate buyer pressure.

| Buyer | 2023/24 |

|---|---|

| US federal procurement | >700B |

| DoD budget FY2024 | ~858B |

| US charitable giving 2023 | 499.3B |

| Grants performance-linked | ~40% |

| Enterprises with analytics | >50% |

Same Document Delivered

RAND Porter's Five Forces Analysis

This preview shows the exact RAND Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is the complete, professionally formatted analysis, ready for download and use the moment you buy. You’ll get instant access to this identical file.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

RAND’s Porter's Five Forces distills competitive pressure across suppliers, buyers, entrants, substitutes, and rivalry to reveal where strategic risks and advantages lie. This brief snapshot highlights key dynamics but leaves force-by-force ratings, visuals, and actionable implications unexplored. Unlock the full analysis for a consultant-grade, data-driven breakdown to inform investment and strategic decisions.

Suppliers Bargaining Power

Specialized talent

RAND depends on PhD-level researchers and cleared subject-matter experts drawn from a US annual pool of about 55,703 research doctorates (NCSES 2022); this scarcity lifts wage expectations and raises switching costs. RAND employs roughly 1,800 staff worldwide, but its mission, reputation and intrinsic-motivation appeal temper supplier power. Long tenures and internal development reduce volatility.

Proprietary data

In 2024, access to restricted government datasets and licensed private data remained key bottlenecks for RAND-style analytics, with many projects delaying timelines for permissions.

Exclusive or hard-to-replicate datasets gave suppliers meaningful leverage on price and terms, often commanding premiums above 30% in licensing deals.

Multi-source strategies, open-data alternatives and negotiated data-use agreements or long-term partnerships reduced dependence and stabilized access.

Field access

Survey panels, clinical sites, and operational theaters depend on gatekeepers who set conditions, timelines, and fees, and as of 2024 these intermediaries remain primary chokepoints for field access. RAND mitigates supplier power by cultivating diverse site networks and maintaining IRB standards that attract participation. Maintaining redundant site options reduces single-point exposure and activation risk.

Tech stack

Cloud platforms, secure enclaves and niche software vendors create significant switching costs; security and compliance needs further amplify vendor lock-in. In 2024, 92% of enterprises report multi-cloud use and 87% run Kubernetes in production, prompting RAND to use multi-cloud, open-source and containerization for portability. Volume pricing and consortia buying can cut procurement costs by ~15%.

- suppliers: hyperscalers, enclave vendors

- lock-in drivers: security, compliance

- mitigation: multi-cloud, OSS, containers

- 2024 stats: 92% multi-cloud, 87% k8s

- cost leverage: ~15% via consortia

Subcontractors

Subcontractors supply niche local expertise and surge capacity, with 2024 industry surveys showing regional partners staffed 30–35% of major infrastructure project hours; specialized firms raised rates about 15–20% during 2023–24 demand spikes, increasing supplier leverage. Long-term framework agreements and prequalified benches cut price volatility and lead times, while knowledge-transfer clauses reduce dependency over 2–4 years.

- Supplier share: 30–35%

- Price spike: 15–20%

- Dependency horizon: 2–4 years

- Mitigants: frameworks, prequalification, transfer clauses

PhD shortage (55,703) lifts licensing premiums >30%; multi-cloud cuts ~15%

RAND depends on scarce PhD talent (55,703 US research doctorates, NCSES 2022), raising wage and switching costs; exclusive datasets and gatekeepers command premiums >30% and delay timelines. Multi-cloud (92%) and Kubernetes (87%) trends push RAND to multi-cloud/OSS to cut procurement ~15%. Subcontractors supply 30–35% of hours with 15–20% rate spikes, mitigated by frameworks and knowledge-transfer.

| Metric | Value |

|---|---|

| US research doctorates | 55,703 (NCSES 2022) |

| Licensing premium | >30% |

| Multi-cloud | 92% (2024) |

| Kubernetes | 87% (2024) |

| Consortia savings | ~15% |

| Subcontractor share | 30–35% |

| Subcontractor rate spike | 15–20% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks specific to RAND, with detailed evaluation of supplier and buyer power, substitutes, and disruptive threats. Fully editable Word format—ready for inclusion in investor materials, strategy decks, or academic projects.

A concise RAND Porter's Five Forces one-sheet with adjustable pressure sliders and an instant radar chart—clean, no-macro layout that’s ready for pitch decks, dashboards, and quick scenario updates as market conditions evolve.

Customers Bargaining Power

Government sponsors

Federal, state and defense agencies control large budgets—federal contracting exceeds $700B annually and the FY2024 DoD budget was about $858B—giving buyers strong leverage. RFPs, fixed-fee awards and audit rights constrain margins and shift risk. Past-performance scoring forces aggressive pricing and on-time delivery. Multi-year IDIQs provide stability but intensify competition over terms.

Foundations/NGOs

Philanthropic funders shape research agendas through thematic grants and milestone-driven contracts; Giving USA 2024 reports US charitable giving at $499.3B in 2023, concentrating leverage in large donors who often push for lower overhead and faster timelines. RAND’s long-standing credibility and measurable impact mitigate pricing pressure, while broad portfolio diversification reduces dependence on any single donor.

International bodies

As of 2024, multilaterals enforce stringent compliance and public disclosure regimes that compress negotiation levers around pricing and scope. Currency, jurisdiction, and political risk add contractual complexity that sophisticated buyers exploit in negotiation and payment terms. RAND’s global experience improves bid win rates but does not translate into greater fee flexibility. Consortium bids in multilateral tenders slightly dilute individual buyer leverage.

Outcome accountability

Buyers demand actionable, measurable policy impact and in 2024 roughly 40% of major grants incorporate performance-linked payments, increasing buyer leverage. Performance-linked payments and deliverable gates strengthen buyer hand, but RAND counters with clear methodologies, staged deliverables and rigorous baselines. Transparent impact evaluation and documented outcomes boost repeat business and reduce pure price competition.

- Performance mandates: ~40% of grants in 2024

- Risk shift: more payments tied to delivery gates

- RAND defense: staged deliverables + clear methodology

- Outcome proof: repeat business lowers price pressure

Information symmetry

Buyers increasingly deploy internal analytics and open data; by 2024 over 50% of enterprises maintain analytics teams, strengthening BATNA to insource or rebid. RAND differentiates through independence, cross-domain breadth and methodological rigor, reducing client capture risk. Co-creation models preserve value while allocating ownership and limiting commoditization.

- 2024: >50% enterprises with analytics

- RAND: independence + breadth + rigor

- Co-creation: shared ownership, protected margin

>700B buyers, 499B donors; ~40% grants pay

Large public buyers (US federal procurement >700B, DoD FY2024 ~858B) and major donors (US giving $499.3B in 2023) exert strong price and scope leverage; ~40% of major grants tie payments to performance. Over 50% of enterprises have analytics teams, raising insourcing BATNA. RAND’s credibility, diversified portfolio and staged deliverables mitigate but do not eliminate buyer pressure.

| Buyer | 2023/24 |

|---|---|

| US federal procurement | >700B |

| DoD budget FY2024 | ~858B |

| US charitable giving 2023 | 499.3B |

| Grants performance-linked | ~40% |

| Enterprises with analytics | >50% |

Same Document Delivered

RAND Porter's Five Forces Analysis

This preview shows the exact RAND Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is the complete, professionally formatted analysis, ready for download and use the moment you buy. You’ll get instant access to this identical file.