RATCH Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

RATCH Group faces high capital intensity and regulatory scrutiny that shape supplier and buyer power, while limited substitute energy sources and strong incumbent scale keep competitive rivalry moderate; renewables growth and policy shifts are key threat vectors. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore RATCH Group’s competitive dynamics, market pressures, and strategic advantages in detail.

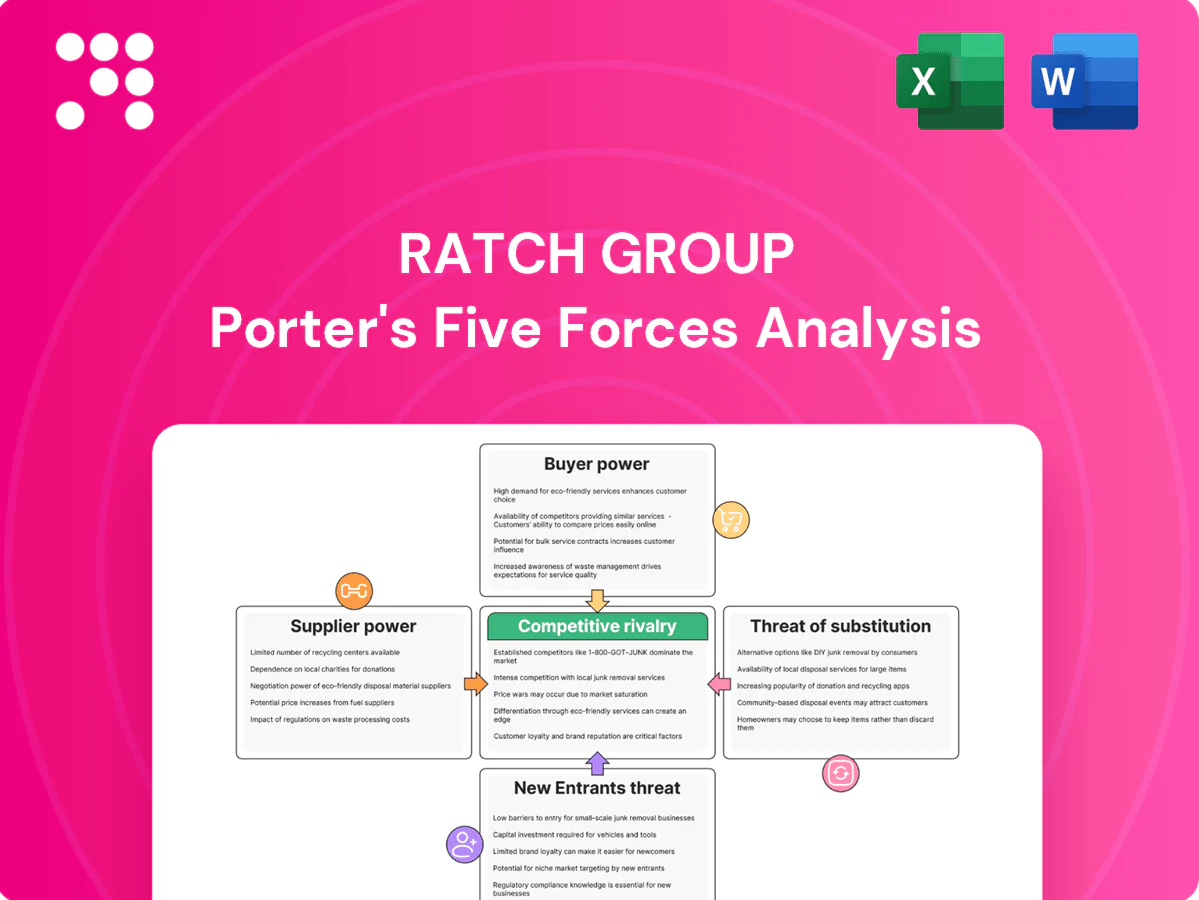

Suppliers Bargaining Power

Fuel concentration risk

Gas supply in Thailand is dominated by state-linked players such as PTT, and long-term gas contracts tie IPPs to a small set of upstream and midstream providers, concentrating supplier leverage. LNG price and supply volatility has increased suppliers’ pricing and delivery power. RATCH’s conventional, largely gas-fired fleet faces limited fuel alternatives, elevating supplier bargaining power. Expansion into renewables reduces but does not eliminate this dependency.

OEM and turbine lock-in

Large thermal units rely on OEM-specific parts and services, creating technical lock-in and high switching costs for operators; long-term service agreements (LTSAs) commonly span 5–15 years and can represent 20–30% of lifecycle O&M expenditure. Maintenance schedules and LTSA terms often favor OEM pricing power, limiting short-term negotiation flexibility. RATCH must balance reliability with multi-sourcing where feasible, and scale plus fleet standardization improves bargaining leverage.

EPC and construction capacity cycles

EPC contractor pricing tightens in boom cycles and loosens in downturns, with tender premiums often moving materially and increasing developer exposure to higher capital costs. Delays or cost escalations typically shift risk back to developers through liquidated damages and contingency drawdowns, pressuring returns. RATCH, with >5 GW operating capacity, mitigates this via competitive bidding and phased pipelines. Local partnerships help stabilize timelines and unit costs.

Renewables component volatility

Renewables component volatility raises supplier power for RATCH as solar modules, inverters and wind turbines face periodic bottlenecks and trade-policy swings; 2024 saw module lead times and tariff actions that tightened supply globally. Commodity inputs—polysilicon, copper and steel—continued to drive cost swings (polysilicon averaging near $12–15/kg in 2024, copper up ~6% year-on-year), while logistics disruptions intermittently raised supplier leverage. Framework agreements and price hedges have tempered procurement risk, and RATCH’s multi-market sourcing reduces single-point exposure and mitigates supplier bargaining power.

- Supply: module/inverter/turbine bottlenecks; trade-policy risk

- Commodities: polysilicon ~$12–15/kg (2024); copper +6% YoY (2024)

- Mitigation: framework agreements, hedging

- RATCH: multi-market sourcing lowers single-point supplier risk

Financing providers’ terms

- lenders: set covenants, pricing, security

- rates: Fed 5.25–5.50% (2024) raises capital costs

- PPA/credit enhancements: tighten spreads for RATCH

- green/SLL: ~10–25 bps cost reduction (2023–24)

Supplier power high: concentrated gas, LTSAs restrict IPPs; polysilicon $12-15/kg, copper +6%

Supplier power is high: gas market concentrated (PTT-dominant), long-term contracts limit IPP options and RATCH’s >5 GW gas fleet has few fuel substitutes. OEM LTSAs (5–15 yrs) raise switching costs and O&M share (~20–30%). Renewables face module/inverter bottlenecks; polysilicon ~$12–15/kg and copper +6% YoY (2024) tightened supplier leverage.

| Factor | 2024 datapoint |

|---|---|

| Gas concentration | PTT-dominant |

| RATCH capacity | >5 GW |

| Polysilicon | $12–15/kg |

| Copper YoY | +6% |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and rivalry specific to RATCH Group—highlighting regulatory/grid access barriers, PPAs and fuel supply dynamics, and emerging renewable competitors as key disruptive threats to market share and profitability.

A clear, one-sheet summary of all five forces for RATCH Group—perfect for quick strategic decisions on generation mix, regulatory exposure and market-entry risks.

Customers Bargaining Power

Single-buyer utility structure

Thai IPPs predominantly sell to EGAT under a single-buyer, regulated framework, concentrating buyer power and leaving little room for price negotiation; standardized PPAs impose strict performance, availability and fuel clauses. RATCH gains predictable offtake and stable revenue visibility but faces constrained pricing flexibility and margin upside. Creditworthy counterparties like EGAT and state utilities reduce payment and counterparty risk.

Long-term PPAs dampen leverage

Take-or-pay and availability-based PPAs, typically 20–25 year contracts in Thailand, limit buyers’ day-to-day negotiating power and lock in volumes. Indexed fuel pass-throughs for conventional plants largely protect RATCH’s margins against spot fuel swings. RATCH reports a high share of capacity under long-term contracts, giving multi-year revenue visibility. Repricing generally happens only at contract renewal or via regulatory changes.

Merchant and C&I exposure abroad

Merchant and C&I exposure abroad increases RATCHs sensitivity to wholesale price swings and negotiators among savvy commercial customers. Large C&I buyers can insist on bespoke pricing, offtake flexibility and greener power, raising bargaining power. Effective contract structuring and hedging are critical to lock margins and transfer risk. The portfolio mix—merchant versus contracted assets—shapes the net buyer power effect.

Quality and reliability expectations

Buyers prioritize grid stability and dispatch reliability, raising performance accountability for RATCH and driving stricter availability and response-time requirements.

Penalties and curtailment clauses in PPAs shift bargaining power toward buyers, so RATCH must sustain high availability and fast ramping to avoid revenue loss.

Digital O&M and predictive maintenance platforms are deployed to defend service levels and reduce unplanned outages.

- Focus: grid stability

- Risk: PPA penalties

- Requirement: high availability

- Defense: digital O&M

ESG-driven preferences

Buyers increasingly favor lower-carbon power, shaping contract awards and renewals and pressuring thermal pricing; corporate and utility buyers in 2024 prioritized renewables in procurement cycles. RATCH’s balanced portfolio (c.5 GW total capacity in 2024) aligns with evolving demand, while certification and attribute-tracking (I-REC/GS) strengthen its contracting position.

- Buyer emphasis: lower-carbon procurement

- Pressure: downward on thermal margins

- RATCH 2024: c.5 GW portfolio

- Advantage: certified clean attributes

Single-buyer PPAs lock stable offtake but cap margin; renewables demand boosts attribute play

Buyers wield limited day-to-day price leverage under Thailand’s single-buyer EGAT framework and 20–25 year PPAs, giving RATCH predictable offtake but capped margin upside. Merchant and C&I contracts abroad raise customer bargaining on price and green attributes; 2024 corporate procurement favored renewables. RATCH reported c.5 GW capacity in 2024, using attribute certification to compete on green procurement.

| Metric | Value |

|---|---|

| RATCH capacity (2024) | c.5 GW |

| PPA length (Thailand) | 20–25 years |

| Major buyer | EGAT (single-buyer) |

| 2024 buyer trend | Renewables preference |

Preview Before You Purchase

RATCH Group Porter's Five Forces Analysis

This preview shows the exact RATCH Group Porter's Five Forces Analysis you'll receive after purchase—no samples, no placeholders. It contains the full, professionally formatted evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitution, and concluding implications for RATCH. Once you buy, this identical file is available for immediate download and use.

Don't Miss the Bigger Picture

RATCH Group faces high capital intensity and regulatory scrutiny that shape supplier and buyer power, while limited substitute energy sources and strong incumbent scale keep competitive rivalry moderate; renewables growth and policy shifts are key threat vectors. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore RATCH Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel concentration risk

Gas supply in Thailand is dominated by state-linked players such as PTT, and long-term gas contracts tie IPPs to a small set of upstream and midstream providers, concentrating supplier leverage. LNG price and supply volatility has increased suppliers’ pricing and delivery power. RATCH’s conventional, largely gas-fired fleet faces limited fuel alternatives, elevating supplier bargaining power. Expansion into renewables reduces but does not eliminate this dependency.

OEM and turbine lock-in

Large thermal units rely on OEM-specific parts and services, creating technical lock-in and high switching costs for operators; long-term service agreements (LTSAs) commonly span 5–15 years and can represent 20–30% of lifecycle O&M expenditure. Maintenance schedules and LTSA terms often favor OEM pricing power, limiting short-term negotiation flexibility. RATCH must balance reliability with multi-sourcing where feasible, and scale plus fleet standardization improves bargaining leverage.

EPC and construction capacity cycles

EPC contractor pricing tightens in boom cycles and loosens in downturns, with tender premiums often moving materially and increasing developer exposure to higher capital costs. Delays or cost escalations typically shift risk back to developers through liquidated damages and contingency drawdowns, pressuring returns. RATCH, with >5 GW operating capacity, mitigates this via competitive bidding and phased pipelines. Local partnerships help stabilize timelines and unit costs.

Renewables component volatility

Renewables component volatility raises supplier power for RATCH as solar modules, inverters and wind turbines face periodic bottlenecks and trade-policy swings; 2024 saw module lead times and tariff actions that tightened supply globally. Commodity inputs—polysilicon, copper and steel—continued to drive cost swings (polysilicon averaging near $12–15/kg in 2024, copper up ~6% year-on-year), while logistics disruptions intermittently raised supplier leverage. Framework agreements and price hedges have tempered procurement risk, and RATCH’s multi-market sourcing reduces single-point exposure and mitigates supplier bargaining power.

- Supply: module/inverter/turbine bottlenecks; trade-policy risk

- Commodities: polysilicon ~$12–15/kg (2024); copper +6% YoY (2024)

- Mitigation: framework agreements, hedging

- RATCH: multi-market sourcing lowers single-point supplier risk

Financing providers’ terms

- lenders: set covenants, pricing, security

- rates: Fed 5.25–5.50% (2024) raises capital costs

- PPA/credit enhancements: tighten spreads for RATCH

- green/SLL: ~10–25 bps cost reduction (2023–24)

Supplier power high: concentrated gas, LTSAs restrict IPPs; polysilicon $12-15/kg, copper +6%

Supplier power is high: gas market concentrated (PTT-dominant), long-term contracts limit IPP options and RATCH’s >5 GW gas fleet has few fuel substitutes. OEM LTSAs (5–15 yrs) raise switching costs and O&M share (~20–30%). Renewables face module/inverter bottlenecks; polysilicon ~$12–15/kg and copper +6% YoY (2024) tightened supplier leverage.

| Factor | 2024 datapoint |

|---|---|

| Gas concentration | PTT-dominant |

| RATCH capacity | >5 GW |

| Polysilicon | $12–15/kg |

| Copper YoY | +6% |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and rivalry specific to RATCH Group—highlighting regulatory/grid access barriers, PPAs and fuel supply dynamics, and emerging renewable competitors as key disruptive threats to market share and profitability.

A clear, one-sheet summary of all five forces for RATCH Group—perfect for quick strategic decisions on generation mix, regulatory exposure and market-entry risks.

Customers Bargaining Power

Single-buyer utility structure

Thai IPPs predominantly sell to EGAT under a single-buyer, regulated framework, concentrating buyer power and leaving little room for price negotiation; standardized PPAs impose strict performance, availability and fuel clauses. RATCH gains predictable offtake and stable revenue visibility but faces constrained pricing flexibility and margin upside. Creditworthy counterparties like EGAT and state utilities reduce payment and counterparty risk.

Long-term PPAs dampen leverage

Take-or-pay and availability-based PPAs, typically 20–25 year contracts in Thailand, limit buyers’ day-to-day negotiating power and lock in volumes. Indexed fuel pass-throughs for conventional plants largely protect RATCH’s margins against spot fuel swings. RATCH reports a high share of capacity under long-term contracts, giving multi-year revenue visibility. Repricing generally happens only at contract renewal or via regulatory changes.

Merchant and C&I exposure abroad

Merchant and C&I exposure abroad increases RATCHs sensitivity to wholesale price swings and negotiators among savvy commercial customers. Large C&I buyers can insist on bespoke pricing, offtake flexibility and greener power, raising bargaining power. Effective contract structuring and hedging are critical to lock margins and transfer risk. The portfolio mix—merchant versus contracted assets—shapes the net buyer power effect.

Quality and reliability expectations

Buyers prioritize grid stability and dispatch reliability, raising performance accountability for RATCH and driving stricter availability and response-time requirements.

Penalties and curtailment clauses in PPAs shift bargaining power toward buyers, so RATCH must sustain high availability and fast ramping to avoid revenue loss.

Digital O&M and predictive maintenance platforms are deployed to defend service levels and reduce unplanned outages.

- Focus: grid stability

- Risk: PPA penalties

- Requirement: high availability

- Defense: digital O&M

ESG-driven preferences

Buyers increasingly favor lower-carbon power, shaping contract awards and renewals and pressuring thermal pricing; corporate and utility buyers in 2024 prioritized renewables in procurement cycles. RATCH’s balanced portfolio (c.5 GW total capacity in 2024) aligns with evolving demand, while certification and attribute-tracking (I-REC/GS) strengthen its contracting position.

- Buyer emphasis: lower-carbon procurement

- Pressure: downward on thermal margins

- RATCH 2024: c.5 GW portfolio

- Advantage: certified clean attributes

Single-buyer PPAs lock stable offtake but cap margin; renewables demand boosts attribute play

Buyers wield limited day-to-day price leverage under Thailand’s single-buyer EGAT framework and 20–25 year PPAs, giving RATCH predictable offtake but capped margin upside. Merchant and C&I contracts abroad raise customer bargaining on price and green attributes; 2024 corporate procurement favored renewables. RATCH reported c.5 GW capacity in 2024, using attribute certification to compete on green procurement.

| Metric | Value |

|---|---|

| RATCH capacity (2024) | c.5 GW |

| PPA length (Thailand) | 20–25 years |

| Major buyer | EGAT (single-buyer) |

| 2024 buyer trend | Renewables preference |

Preview Before You Purchase

RATCH Group Porter's Five Forces Analysis

This preview shows the exact RATCH Group Porter's Five Forces Analysis you'll receive after purchase—no samples, no placeholders. It contains the full, professionally formatted evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitution, and concluding implications for RATCH. Once you buy, this identical file is available for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

RATCH Group faces high capital intensity and regulatory scrutiny that shape supplier and buyer power, while limited substitute energy sources and strong incumbent scale keep competitive rivalry moderate; renewables growth and policy shifts are key threat vectors. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore RATCH Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fuel concentration risk

Gas supply in Thailand is dominated by state-linked players such as PTT, and long-term gas contracts tie IPPs to a small set of upstream and midstream providers, concentrating supplier leverage. LNG price and supply volatility has increased suppliers’ pricing and delivery power. RATCH’s conventional, largely gas-fired fleet faces limited fuel alternatives, elevating supplier bargaining power. Expansion into renewables reduces but does not eliminate this dependency.

OEM and turbine lock-in

Large thermal units rely on OEM-specific parts and services, creating technical lock-in and high switching costs for operators; long-term service agreements (LTSAs) commonly span 5–15 years and can represent 20–30% of lifecycle O&M expenditure. Maintenance schedules and LTSA terms often favor OEM pricing power, limiting short-term negotiation flexibility. RATCH must balance reliability with multi-sourcing where feasible, and scale plus fleet standardization improves bargaining leverage.

EPC and construction capacity cycles

EPC contractor pricing tightens in boom cycles and loosens in downturns, with tender premiums often moving materially and increasing developer exposure to higher capital costs. Delays or cost escalations typically shift risk back to developers through liquidated damages and contingency drawdowns, pressuring returns. RATCH, with >5 GW operating capacity, mitigates this via competitive bidding and phased pipelines. Local partnerships help stabilize timelines and unit costs.

Renewables component volatility

Renewables component volatility raises supplier power for RATCH as solar modules, inverters and wind turbines face periodic bottlenecks and trade-policy swings; 2024 saw module lead times and tariff actions that tightened supply globally. Commodity inputs—polysilicon, copper and steel—continued to drive cost swings (polysilicon averaging near $12–15/kg in 2024, copper up ~6% year-on-year), while logistics disruptions intermittently raised supplier leverage. Framework agreements and price hedges have tempered procurement risk, and RATCH’s multi-market sourcing reduces single-point exposure and mitigates supplier bargaining power.

- Supply: module/inverter/turbine bottlenecks; trade-policy risk

- Commodities: polysilicon ~$12–15/kg (2024); copper +6% YoY (2024)

- Mitigation: framework agreements, hedging

- RATCH: multi-market sourcing lowers single-point supplier risk

Financing providers’ terms

- lenders: set covenants, pricing, security

- rates: Fed 5.25–5.50% (2024) raises capital costs

- PPA/credit enhancements: tighten spreads for RATCH

- green/SLL: ~10–25 bps cost reduction (2023–24)

Supplier power high: concentrated gas, LTSAs restrict IPPs; polysilicon $12-15/kg, copper +6%

Supplier power is high: gas market concentrated (PTT-dominant), long-term contracts limit IPP options and RATCH’s >5 GW gas fleet has few fuel substitutes. OEM LTSAs (5–15 yrs) raise switching costs and O&M share (~20–30%). Renewables face module/inverter bottlenecks; polysilicon ~$12–15/kg and copper +6% YoY (2024) tightened supplier leverage.

| Factor | 2024 datapoint |

|---|---|

| Gas concentration | PTT-dominant |

| RATCH capacity | >5 GW |

| Polysilicon | $12–15/kg |

| Copper YoY | +6% |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and rivalry specific to RATCH Group—highlighting regulatory/grid access barriers, PPAs and fuel supply dynamics, and emerging renewable competitors as key disruptive threats to market share and profitability.

A clear, one-sheet summary of all five forces for RATCH Group—perfect for quick strategic decisions on generation mix, regulatory exposure and market-entry risks.

Customers Bargaining Power

Single-buyer utility structure

Thai IPPs predominantly sell to EGAT under a single-buyer, regulated framework, concentrating buyer power and leaving little room for price negotiation; standardized PPAs impose strict performance, availability and fuel clauses. RATCH gains predictable offtake and stable revenue visibility but faces constrained pricing flexibility and margin upside. Creditworthy counterparties like EGAT and state utilities reduce payment and counterparty risk.

Long-term PPAs dampen leverage

Take-or-pay and availability-based PPAs, typically 20–25 year contracts in Thailand, limit buyers’ day-to-day negotiating power and lock in volumes. Indexed fuel pass-throughs for conventional plants largely protect RATCH’s margins against spot fuel swings. RATCH reports a high share of capacity under long-term contracts, giving multi-year revenue visibility. Repricing generally happens only at contract renewal or via regulatory changes.

Merchant and C&I exposure abroad

Merchant and C&I exposure abroad increases RATCHs sensitivity to wholesale price swings and negotiators among savvy commercial customers. Large C&I buyers can insist on bespoke pricing, offtake flexibility and greener power, raising bargaining power. Effective contract structuring and hedging are critical to lock margins and transfer risk. The portfolio mix—merchant versus contracted assets—shapes the net buyer power effect.

Quality and reliability expectations

Buyers prioritize grid stability and dispatch reliability, raising performance accountability for RATCH and driving stricter availability and response-time requirements.

Penalties and curtailment clauses in PPAs shift bargaining power toward buyers, so RATCH must sustain high availability and fast ramping to avoid revenue loss.

Digital O&M and predictive maintenance platforms are deployed to defend service levels and reduce unplanned outages.

- Focus: grid stability

- Risk: PPA penalties

- Requirement: high availability

- Defense: digital O&M

ESG-driven preferences

Buyers increasingly favor lower-carbon power, shaping contract awards and renewals and pressuring thermal pricing; corporate and utility buyers in 2024 prioritized renewables in procurement cycles. RATCH’s balanced portfolio (c.5 GW total capacity in 2024) aligns with evolving demand, while certification and attribute-tracking (I-REC/GS) strengthen its contracting position.

- Buyer emphasis: lower-carbon procurement

- Pressure: downward on thermal margins

- RATCH 2024: c.5 GW portfolio

- Advantage: certified clean attributes

Single-buyer PPAs lock stable offtake but cap margin; renewables demand boosts attribute play

Buyers wield limited day-to-day price leverage under Thailand’s single-buyer EGAT framework and 20–25 year PPAs, giving RATCH predictable offtake but capped margin upside. Merchant and C&I contracts abroad raise customer bargaining on price and green attributes; 2024 corporate procurement favored renewables. RATCH reported c.5 GW capacity in 2024, using attribute certification to compete on green procurement.

| Metric | Value |

|---|---|

| RATCH capacity (2024) | c.5 GW |

| PPA length (Thailand) | 20–25 years |

| Major buyer | EGAT (single-buyer) |

| 2024 buyer trend | Renewables preference |

Preview Before You Purchase

RATCH Group Porter's Five Forces Analysis

This preview shows the exact RATCH Group Porter's Five Forces Analysis you'll receive after purchase—no samples, no placeholders. It contains the full, professionally formatted evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitution, and concluding implications for RATCH. Once you buy, this identical file is available for immediate download and use.