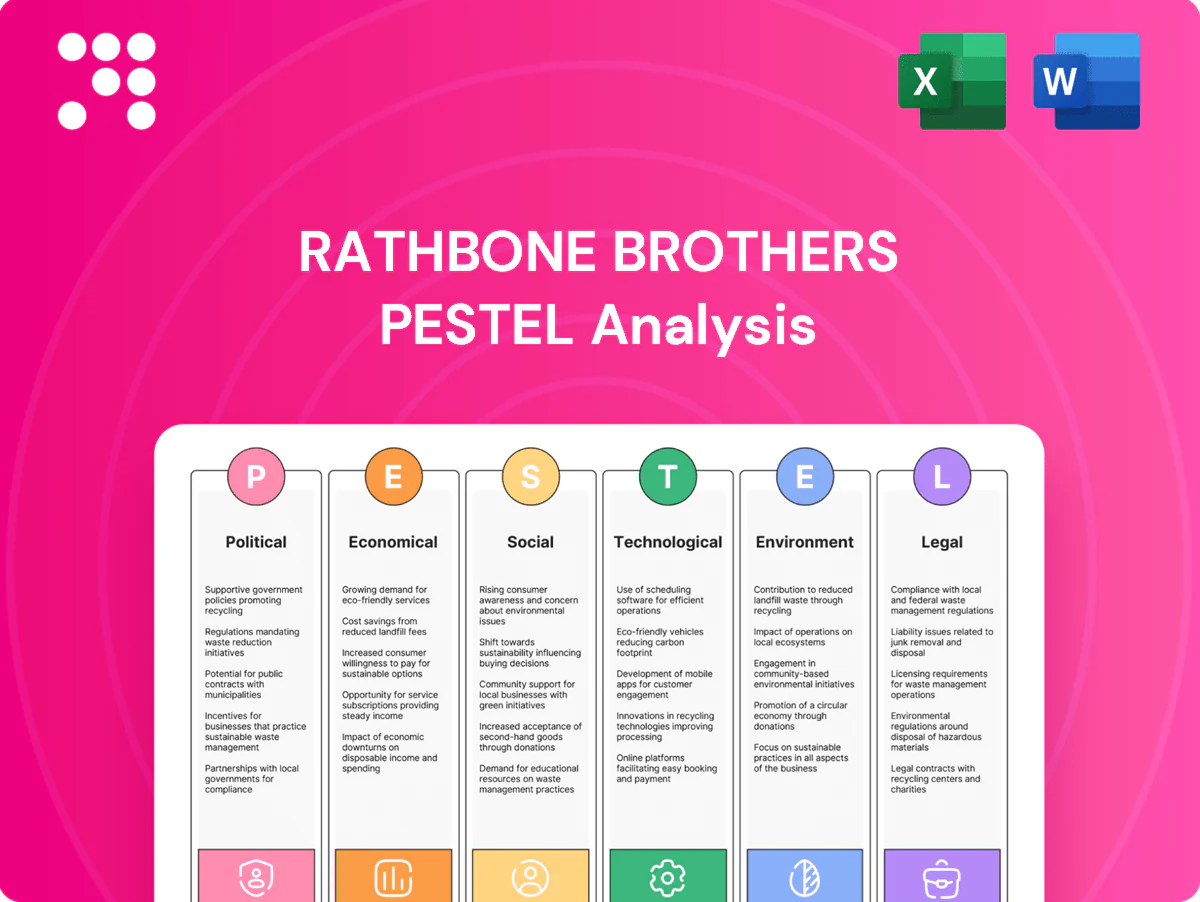

Rathbone Brothers PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, social trends, and regulatory changes are reshaping Rathbone Brothers’ strategy in our concise PESTLE briefing—perfect for investors and strategists. Dive deeper with the full, ready-to-use analysis to inform decisions and spot risks and opportunities; purchase the complete report now.

Political factors

UK regulatory direction

HM Treasury policy shifts and FCA rulemaking—notably the Consumer Duty (effective 31 July 2023, with product review deadline 31 July 2024)—directly reshape Rathbones’ conduct standards, advice guidance and capital planning, increasing compliance costs. The FCA ran dozens of consultations in 2024 and issues Dear CEO letters that require close monitoring. Proactive engagement with regulators can smooth implementation and reduce compliance shocks.

Tax policy on wealth

Alterations to CGT (annual exempt amount £3,000 in 2024/25), dividend allowance (£500 in 2024/25), IHT nil-rate band (£325,000) and pension rules materially shift client demand and portfolio structuring. Budget cycles force rapid tax-planning and product redesign, as seen after 2023–24 allowance changes. Scenario planning across tax bands improves retention. Close coordination with financial planning teams is critical.

Geopolitical and UK-EU ties

Brexit ended EU passporting in 2021 and comprehensive EU equivalence for UK financial services remained limited through 2024, constraining cross-border permissions and complicating servicing of expatriate and EU clients.

Geopolitical tensions since 2022 have driven higher volatility in global allocations, increasing rebalancing and liquidity needs.

Sanctions regimes demand enhanced screening and monitoring, while diversified research supports policy-driven positioning; Rathbones reported AUM/A at £63.7bn (Sept 2024).

Public spending and fiscal stance

Public spending and fiscal stance drive gilt yields and risk appetite; 10-year UK gilt yields hovered near 4.3% in mid-2025, so deficit management and consolidation materially affect portfolio risk pricing. Shifts into public investment redirect sector rotations toward infrastructure and construction while higher issuance can reprice duration in client portfolios. Clear communication of macro implications strengthens client confidence and reduces redemption risk.

- Deficit control → gilt yield pressure

- Public investment → sector rotation (infra, construction)

- Higher issuance → duration repricing in client books

- Transparent communication → client confidence

Devolution and regional policy

Devolution means Scottish, Welsh and Northern Irish tax and welfare choices (eg Scottish income tax bands) change local tax dynamics and client cashflow needs; Rathbones (around £67bn AUM in 2024) must adjust advice for regional allowances. Regional economic strategies shape SME and charity pipelines (UK has ~5.7m private sector businesses and ~168,000 charities). Location choices respond to talent pools and regulation; tailored regional propositions can capture growth.

- Regional tax divergence: impacts personal tax planning

- SME/charity mix: alters service demand

- Location: hires cost/talent/regulatory fit

- Tailored offers: opportunity to grow market share

Regulatory, tax and geopolitical shifts reshape wealth demand; AUM ~£67bn

Regulatory change (Consumer Duty effective 31 Jul 2023), active HM Treasury/FCA rulemaking and UK tax shifts (CGT AE £3,000; dividend allowance £500 in 2024/25) raise compliance and reshape client demand, while Brexit, sanctions and geopolitics drive cross-border constraints and volatility; Rathbones reported ~£67bn AUM (2024).

| Item | 2024/25 |

|---|---|

| AUM | ~£67bn |

| CGT AE | £3,000 |

| Dividend allowance | £500 |

| 10y gilt (mid-2025) | ~4.3% |

What is included in the product

Explores how macro-environmental factors uniquely affect Rathbone Brothers across Political, Economic, Social, Technological, Environmental and Legal dimensions, backed by current data and trends to identify threats, opportunities and forward‑looking scenarios; formatted for direct use by executives, advisors and investors.

Concise, visually segmented Rathbone Brothers PESTLE that distills external risks and opportunities into an editable, shareable summary—ready to drop into presentations or planning sessions to speed alignment and support strategic decision-making.

Economic factors

Interest rate trajectory

BoE Bank Rate at 5.25% (July 2025) directly shapes Rathbone Brothers’ income strategies and valuation discount rates; a move lower would boost duration assets’ capital values but squeeze deposit margins, while further rate rises would lift cash yields yet depress equities and bond prices—necessitating active asset-liability and duration positioning to protect net interest margins and client income targets.

Market volatility cycles

Equity drawdowns and wider credit spreads drive AUM swings that compress fee revenue; for example the S&P 500 fell 19.4% in 2022, shrinking industry AUM and fee bases. Volatility raises trading and rebalancing needs but can deter net inflows. Clear risk frameworks sustain client trust during stress. Opportunistic deployment during drawdowns can boost long-run returns.

Inflation and real returns

Persistent inflation erodes client purchasing power and reshapes asset mix versus the Bank of England 2% target, increasing demand for inflation-linked gilts and real assets in discretionary mandates. Inflation-linked and real assets gain relevance in client portfolios as hedges; Rathbones must emphasise these in advice. Cost pressures can compress operating margins if not offset by efficiency improvements, while clear, data-driven inflation narratives aid client retention.

Wealth creation and GDP trends

- GDP growth: ~0.6–0.8% (2024)

- FTSE 100 dividend yield: ~3.5–3.8% (2024)

- Unemployment: ~4.2% (mid-2024)

- Mitigation: international revenue mix lowers UK risk

FX and global exposure

Sterling swings (GBP/USD ~1.27 June 2025) materially alter overseas asset valuations and client outcomes; a 5-10% FX move can shift portfolio returns significantly. Hedging policies determine risk reduction versus recurring hedging costs. Regional macro spreads (US/EU/EM) enable tactical tilts while multicurrency reporting and compliance complexity rise.

- FX rate: GBP/USD ~1.27 (Jun 2025)

- Hedging trade-off: risk vs cost

- Tactical: exploit US/EU/EM spreads

- Reporting: higher multicurrency complexity

Regulatory, tax and geopolitical shifts reshape wealth demand; AUM ~£67bn

BoE rate 5.25% (Jul 2025) shapes discount rates and deposit margins; rate cuts raise asset values but squeeze margins. Equity drawdowns and wider credit spreads compress AUM/fee income; volatility increases trading costs but creates deployment opportunities. Inflation above target boosts demand for ILGs and real assets; slower UK GDP (~0.6–0.8% 2024) limits new wealth flows.

| Metric | Value |

|---|---|

| BoE Bank Rate | 5.25% (Jul 2025) |

| GBP/USD | ~1.27 (Jun 2025) |

| UK GDP | 0.6–0.8% (2024) |

| FTSE 100 yield | ~3.6% (2024) |

| Unemployment | ~4.2% (mid-2024) |

Preview Before You Purchase

Rathbone Brothers PESTLE Analysis

The Rathbone Brothers PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with charts and clear headings. No placeholders or teasers—this is the final file you’ll download immediately after payment.

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, social trends, and regulatory changes are reshaping Rathbone Brothers’ strategy in our concise PESTLE briefing—perfect for investors and strategists. Dive deeper with the full, ready-to-use analysis to inform decisions and spot risks and opportunities; purchase the complete report now.

Political factors

UK regulatory direction

HM Treasury policy shifts and FCA rulemaking—notably the Consumer Duty (effective 31 July 2023, with product review deadline 31 July 2024)—directly reshape Rathbones’ conduct standards, advice guidance and capital planning, increasing compliance costs. The FCA ran dozens of consultations in 2024 and issues Dear CEO letters that require close monitoring. Proactive engagement with regulators can smooth implementation and reduce compliance shocks.

Tax policy on wealth

Alterations to CGT (annual exempt amount £3,000 in 2024/25), dividend allowance (£500 in 2024/25), IHT nil-rate band (£325,000) and pension rules materially shift client demand and portfolio structuring. Budget cycles force rapid tax-planning and product redesign, as seen after 2023–24 allowance changes. Scenario planning across tax bands improves retention. Close coordination with financial planning teams is critical.

Geopolitical and UK-EU ties

Brexit ended EU passporting in 2021 and comprehensive EU equivalence for UK financial services remained limited through 2024, constraining cross-border permissions and complicating servicing of expatriate and EU clients.

Geopolitical tensions since 2022 have driven higher volatility in global allocations, increasing rebalancing and liquidity needs.

Sanctions regimes demand enhanced screening and monitoring, while diversified research supports policy-driven positioning; Rathbones reported AUM/A at £63.7bn (Sept 2024).

Public spending and fiscal stance

Public spending and fiscal stance drive gilt yields and risk appetite; 10-year UK gilt yields hovered near 4.3% in mid-2025, so deficit management and consolidation materially affect portfolio risk pricing. Shifts into public investment redirect sector rotations toward infrastructure and construction while higher issuance can reprice duration in client portfolios. Clear communication of macro implications strengthens client confidence and reduces redemption risk.

- Deficit control → gilt yield pressure

- Public investment → sector rotation (infra, construction)

- Higher issuance → duration repricing in client books

- Transparent communication → client confidence

Devolution and regional policy

Devolution means Scottish, Welsh and Northern Irish tax and welfare choices (eg Scottish income tax bands) change local tax dynamics and client cashflow needs; Rathbones (around £67bn AUM in 2024) must adjust advice for regional allowances. Regional economic strategies shape SME and charity pipelines (UK has ~5.7m private sector businesses and ~168,000 charities). Location choices respond to talent pools and regulation; tailored regional propositions can capture growth.

- Regional tax divergence: impacts personal tax planning

- SME/charity mix: alters service demand

- Location: hires cost/talent/regulatory fit

- Tailored offers: opportunity to grow market share

Regulatory, tax and geopolitical shifts reshape wealth demand; AUM ~£67bn

Regulatory change (Consumer Duty effective 31 Jul 2023), active HM Treasury/FCA rulemaking and UK tax shifts (CGT AE £3,000; dividend allowance £500 in 2024/25) raise compliance and reshape client demand, while Brexit, sanctions and geopolitics drive cross-border constraints and volatility; Rathbones reported ~£67bn AUM (2024).

| Item | 2024/25 |

|---|---|

| AUM | ~£67bn |

| CGT AE | £3,000 |

| Dividend allowance | £500 |

| 10y gilt (mid-2025) | ~4.3% |

What is included in the product

Explores how macro-environmental factors uniquely affect Rathbone Brothers across Political, Economic, Social, Technological, Environmental and Legal dimensions, backed by current data and trends to identify threats, opportunities and forward‑looking scenarios; formatted for direct use by executives, advisors and investors.

Concise, visually segmented Rathbone Brothers PESTLE that distills external risks and opportunities into an editable, shareable summary—ready to drop into presentations or planning sessions to speed alignment and support strategic decision-making.

Economic factors

Interest rate trajectory

BoE Bank Rate at 5.25% (July 2025) directly shapes Rathbone Brothers’ income strategies and valuation discount rates; a move lower would boost duration assets’ capital values but squeeze deposit margins, while further rate rises would lift cash yields yet depress equities and bond prices—necessitating active asset-liability and duration positioning to protect net interest margins and client income targets.

Market volatility cycles

Equity drawdowns and wider credit spreads drive AUM swings that compress fee revenue; for example the S&P 500 fell 19.4% in 2022, shrinking industry AUM and fee bases. Volatility raises trading and rebalancing needs but can deter net inflows. Clear risk frameworks sustain client trust during stress. Opportunistic deployment during drawdowns can boost long-run returns.

Inflation and real returns

Persistent inflation erodes client purchasing power and reshapes asset mix versus the Bank of England 2% target, increasing demand for inflation-linked gilts and real assets in discretionary mandates. Inflation-linked and real assets gain relevance in client portfolios as hedges; Rathbones must emphasise these in advice. Cost pressures can compress operating margins if not offset by efficiency improvements, while clear, data-driven inflation narratives aid client retention.

Wealth creation and GDP trends

- GDP growth: ~0.6–0.8% (2024)

- FTSE 100 dividend yield: ~3.5–3.8% (2024)

- Unemployment: ~4.2% (mid-2024)

- Mitigation: international revenue mix lowers UK risk

FX and global exposure

Sterling swings (GBP/USD ~1.27 June 2025) materially alter overseas asset valuations and client outcomes; a 5-10% FX move can shift portfolio returns significantly. Hedging policies determine risk reduction versus recurring hedging costs. Regional macro spreads (US/EU/EM) enable tactical tilts while multicurrency reporting and compliance complexity rise.

- FX rate: GBP/USD ~1.27 (Jun 2025)

- Hedging trade-off: risk vs cost

- Tactical: exploit US/EU/EM spreads

- Reporting: higher multicurrency complexity

Regulatory, tax and geopolitical shifts reshape wealth demand; AUM ~£67bn

BoE rate 5.25% (Jul 2025) shapes discount rates and deposit margins; rate cuts raise asset values but squeeze margins. Equity drawdowns and wider credit spreads compress AUM/fee income; volatility increases trading costs but creates deployment opportunities. Inflation above target boosts demand for ILGs and real assets; slower UK GDP (~0.6–0.8% 2024) limits new wealth flows.

| Metric | Value |

|---|---|

| BoE Bank Rate | 5.25% (Jul 2025) |

| GBP/USD | ~1.27 (Jun 2025) |

| UK GDP | 0.6–0.8% (2024) |

| FTSE 100 yield | ~3.6% (2024) |

| Unemployment | ~4.2% (mid-2024) |

Preview Before You Purchase

Rathbone Brothers PESTLE Analysis

The Rathbone Brothers PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with charts and clear headings. No placeholders or teasers—this is the final file you’ll download immediately after payment.

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, social trends, and regulatory changes are reshaping Rathbone Brothers’ strategy in our concise PESTLE briefing—perfect for investors and strategists. Dive deeper with the full, ready-to-use analysis to inform decisions and spot risks and opportunities; purchase the complete report now.

Political factors

UK regulatory direction

HM Treasury policy shifts and FCA rulemaking—notably the Consumer Duty (effective 31 July 2023, with product review deadline 31 July 2024)—directly reshape Rathbones’ conduct standards, advice guidance and capital planning, increasing compliance costs. The FCA ran dozens of consultations in 2024 and issues Dear CEO letters that require close monitoring. Proactive engagement with regulators can smooth implementation and reduce compliance shocks.

Tax policy on wealth

Alterations to CGT (annual exempt amount £3,000 in 2024/25), dividend allowance (£500 in 2024/25), IHT nil-rate band (£325,000) and pension rules materially shift client demand and portfolio structuring. Budget cycles force rapid tax-planning and product redesign, as seen after 2023–24 allowance changes. Scenario planning across tax bands improves retention. Close coordination with financial planning teams is critical.

Geopolitical and UK-EU ties

Brexit ended EU passporting in 2021 and comprehensive EU equivalence for UK financial services remained limited through 2024, constraining cross-border permissions and complicating servicing of expatriate and EU clients.

Geopolitical tensions since 2022 have driven higher volatility in global allocations, increasing rebalancing and liquidity needs.

Sanctions regimes demand enhanced screening and monitoring, while diversified research supports policy-driven positioning; Rathbones reported AUM/A at £63.7bn (Sept 2024).

Public spending and fiscal stance

Public spending and fiscal stance drive gilt yields and risk appetite; 10-year UK gilt yields hovered near 4.3% in mid-2025, so deficit management and consolidation materially affect portfolio risk pricing. Shifts into public investment redirect sector rotations toward infrastructure and construction while higher issuance can reprice duration in client portfolios. Clear communication of macro implications strengthens client confidence and reduces redemption risk.

- Deficit control → gilt yield pressure

- Public investment → sector rotation (infra, construction)

- Higher issuance → duration repricing in client books

- Transparent communication → client confidence

Devolution and regional policy

Devolution means Scottish, Welsh and Northern Irish tax and welfare choices (eg Scottish income tax bands) change local tax dynamics and client cashflow needs; Rathbones (around £67bn AUM in 2024) must adjust advice for regional allowances. Regional economic strategies shape SME and charity pipelines (UK has ~5.7m private sector businesses and ~168,000 charities). Location choices respond to talent pools and regulation; tailored regional propositions can capture growth.

- Regional tax divergence: impacts personal tax planning

- SME/charity mix: alters service demand

- Location: hires cost/talent/regulatory fit

- Tailored offers: opportunity to grow market share

Regulatory, tax and geopolitical shifts reshape wealth demand; AUM ~£67bn

Regulatory change (Consumer Duty effective 31 Jul 2023), active HM Treasury/FCA rulemaking and UK tax shifts (CGT AE £3,000; dividend allowance £500 in 2024/25) raise compliance and reshape client demand, while Brexit, sanctions and geopolitics drive cross-border constraints and volatility; Rathbones reported ~£67bn AUM (2024).

| Item | 2024/25 |

|---|---|

| AUM | ~£67bn |

| CGT AE | £3,000 |

| Dividend allowance | £500 |

| 10y gilt (mid-2025) | ~4.3% |

What is included in the product

Explores how macro-environmental factors uniquely affect Rathbone Brothers across Political, Economic, Social, Technological, Environmental and Legal dimensions, backed by current data and trends to identify threats, opportunities and forward‑looking scenarios; formatted for direct use by executives, advisors and investors.

Concise, visually segmented Rathbone Brothers PESTLE that distills external risks and opportunities into an editable, shareable summary—ready to drop into presentations or planning sessions to speed alignment and support strategic decision-making.

Economic factors

Interest rate trajectory

BoE Bank Rate at 5.25% (July 2025) directly shapes Rathbone Brothers’ income strategies and valuation discount rates; a move lower would boost duration assets’ capital values but squeeze deposit margins, while further rate rises would lift cash yields yet depress equities and bond prices—necessitating active asset-liability and duration positioning to protect net interest margins and client income targets.

Market volatility cycles

Equity drawdowns and wider credit spreads drive AUM swings that compress fee revenue; for example the S&P 500 fell 19.4% in 2022, shrinking industry AUM and fee bases. Volatility raises trading and rebalancing needs but can deter net inflows. Clear risk frameworks sustain client trust during stress. Opportunistic deployment during drawdowns can boost long-run returns.

Inflation and real returns

Persistent inflation erodes client purchasing power and reshapes asset mix versus the Bank of England 2% target, increasing demand for inflation-linked gilts and real assets in discretionary mandates. Inflation-linked and real assets gain relevance in client portfolios as hedges; Rathbones must emphasise these in advice. Cost pressures can compress operating margins if not offset by efficiency improvements, while clear, data-driven inflation narratives aid client retention.

Wealth creation and GDP trends

- GDP growth: ~0.6–0.8% (2024)

- FTSE 100 dividend yield: ~3.5–3.8% (2024)

- Unemployment: ~4.2% (mid-2024)

- Mitigation: international revenue mix lowers UK risk

FX and global exposure

Sterling swings (GBP/USD ~1.27 June 2025) materially alter overseas asset valuations and client outcomes; a 5-10% FX move can shift portfolio returns significantly. Hedging policies determine risk reduction versus recurring hedging costs. Regional macro spreads (US/EU/EM) enable tactical tilts while multicurrency reporting and compliance complexity rise.

- FX rate: GBP/USD ~1.27 (Jun 2025)

- Hedging trade-off: risk vs cost

- Tactical: exploit US/EU/EM spreads

- Reporting: higher multicurrency complexity

Regulatory, tax and geopolitical shifts reshape wealth demand; AUM ~£67bn

BoE rate 5.25% (Jul 2025) shapes discount rates and deposit margins; rate cuts raise asset values but squeeze margins. Equity drawdowns and wider credit spreads compress AUM/fee income; volatility increases trading costs but creates deployment opportunities. Inflation above target boosts demand for ILGs and real assets; slower UK GDP (~0.6–0.8% 2024) limits new wealth flows.

| Metric | Value |

|---|---|

| BoE Bank Rate | 5.25% (Jul 2025) |

| GBP/USD | ~1.27 (Jun 2025) |

| UK GDP | 0.6–0.8% (2024) |

| FTSE 100 yield | ~3.6% (2024) |

| Unemployment | ~4.2% (mid-2024) |

Preview Before You Purchase

Rathbone Brothers PESTLE Analysis

The Rathbone Brothers PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with charts and clear headings. No placeholders or teasers—this is the final file you’ll download immediately after payment.